JHVEPhoto

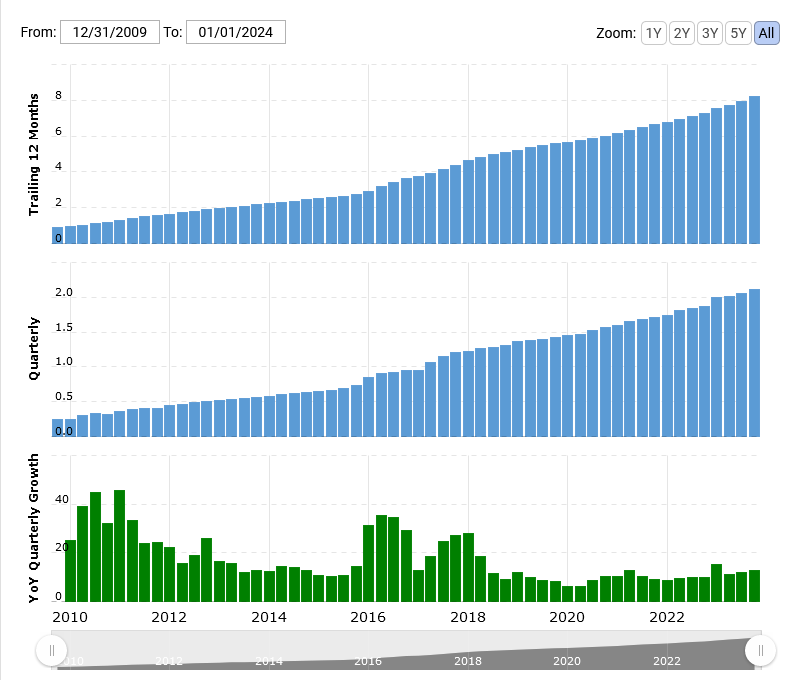

Last month, the world’s leading data center REIT, Equinix Inc. (NASDAQ:EQIX), reported fourth quarter and full-year results for FY 2023. In a previous article published in May, I pointed out that Equinix had managed to grow the top-line for 80+ uninterrupted quarters, the longest growth streak amongst S&P 500 companies. Quite naturally, that was the first line item I was interested in and, thankfully, it did not disappoint. Equinix reported Q4 revenue of $2.11B (+12.8% Y/Y), in-line with the Wall Street consensus, while Q4 FFO of $5.54 beat by $0.24. For the full year, annual revenues increased 13% year-over-year to $8.2 billion, which the company attributed to a ‘’…record 90 megawatts of xScale leasing in the fourth quarter, the result of increased hyperscale demand to support artificial intelligence and cloud deployments.’’ Equinix reported a surge in demand for hyperscale infrastructure to support AI and cloud initiatives. The company finished the year with a total xScale leasing capacity of 300 megawatts globally.

Equinix issued what I consider a healthy but, rather conservative, FY 24 guidance as follows:

-

Full-year revenue $8.793 and $8.893 billion, good for an 8.0% Y/Y increase over the on an as-reported basis

-

Adjusted EBITDA is expected to range between $4.089 and $4.169 billion, good for an 11.5% Y/Y increase at the mid-point

-

Adjusted EBITDA margin of 47%, good for a 200 basis-point increase over the previous year

-

AFFO of $3.306 – $3.376 billion, representing 10% growth over the previous year on both an as-reported basis

-

AFFO per Share of $34.58 – $35.31, representing a 9% Y/Y increase.

The long-term outlook for Equinix and data center companies in general remains positive. Last year presented a seismic shift in data center buildouts with providers overwhelmingly shifting their infrastructure investment priorities from general purpose computing and storage to AI and accelerated computing infrastructure. Consequently, AI workloads are projected to represent 25% of annual data center capex by 2028. Morgan Stanley has picked Equinix as one of the companies that could benefit as Europe upgrades its data centers to handle increased AI workloads.

BofA Securities’ analysts have described the unfolding phenomenon as a “virtuous investment cycle” for the big names thanks to artificial intelligence. Global data center capex is projected to grow at a robust 18% CAGR to $200 billion by 2028, of which hyperscalers including Amazon Inc. (NASDAQ:AMZN), Microsoft Inc. (NASDAQ:MSFT), Alphabet Inc. (NASDAQ:GOOG) and Meta Platforms (NASDAQ:META) will represent nearly half. The four companies are expected to spend $180B on capex in 2024, up 27% year-over-year.

That said, one thing in particular in Equinix’s latest report caught my attention: In Q4, Equinix purchased the company’s London 8 IBX data center. Revenues from owned assets increased to 66% of recurring revenues, stepping up 2%, as the company continues to progress on ownership and long-term control of assets.

Long-Term Control Of Assets

Majority of bearish theses on Equinix that I have come across focus on the company’s lofty valuation, an issue I discussed in my last Equinix piece. EQIX is by no means cheap: P/ AFFO [FWD] of 25.55 is nearly double the sector’s median at 14.60; P/S of 10.78 vs. 4.40 and EV/EBITDA (TTM) of 34.85 vs. 16.63. In its defense, the valuation gap between Equinix and its peers has been narrowing, while its Cash per Share reading of $22.18 is incomparable to the sector median at $0.78.

However, analysts tend to overlook the risk posed by Equinix’s earlier model of leasing a large percentage of its data center space from a growing rival, Digital Realty (NYSE:DLR). After a wave of takeovers in the past few years, Equinix, Digital Realty and Iron Mountain Inc. (NYSE:IRM) have been left standing as the only pure-play data center companies.

Equinix operates a global network of 260 data centers, including 11 xScale builds representing nearly 20,000 cabinets of retail and more than 50 megawatts of xScale capacity. On the other hand, Digital Realty manages a network of 314 data centers, providing 2,352 megawatts of IT load capacity in white space and nearly 40 million net rentable square feet. Equinix leases large spaces from wholesale data center operators, such as Digital Realty, then subdivides these into smaller, retail colocation services to its customers through short-term licenses. This way, the company provides the necessary space, power, cooling, physical security, and connectivity services for its customers to operate and interconnect their IT equipment, thus significantly reducing their costs and complexity.

The relationship between Equinix and Digital Realty stretches back decades, with Equinix at times leasing more than two dozen data center locations from Digital Realty. Unfortunately, their once symbiotic relationship started showing serious cracks ever since Digital Realty acquired Telx for ~$1.9 billion in October 2015, as digital infrastructure firm Dgtl Infra has noted. Telx provided retail colocation services comparable to those of Equinix, essentially positioning Digital Realty as a direct competitor to Equinix. Relations between the two companies came to a head after Equinix filed a lawsuit against Digital Realty in 2019 over an occupational dispute regarding a 1.1 million-square-foot, 9-story, highly interconnected data center located at 350 East Cermak Road in the South Loop close to Chicago, Illinois. Long story short: Equinix wanted to extend its lease on one of the most important “carrier hotels” in all of the U.S. based on a Right of First Offer (ROFO) clause in their agreement, while Digital Realty wanted to use it to expand its growing colocation business. Although the feud was litigated in Digital Realty’s favor in April 2023, it underscores the risk of the two companies doing business across numerous data centers, encompassing commitments totaling over $500 million in rent.

Thankfully, Equinix has been cutting its reliance on Digital Realty, with the company currently leasing 15 data center locations from Digital Realty, down from 26 in 2020. Meanwhile, Equinix has seen a continuous decrease in its weighted average remaining lease term (WALT), from ~11 years in 2020 to ~7.5 years currently. This pattern has several explanations:

- Digital Realty is forcing Equinix to sign shorter-term leases.

- Equinix is no longer interested in signing longer-term leases.

Either way, Equinix is increasingly relying on its own properties. In its latest report, Equinix revealed that 66% of its recurring revenue now comes from owned assets, up 2 percentage-points Q-on-Q. This minimizes the risk of losing valuable space to competitors.

Other than a moderate (and somewhat expected) slowdown in top-line growth, most of Equinix’s key growth metrics remain healthy. I reiterate my Buy recommendation for EQIX.

Equinix Revenue Growth (MacroTrends)

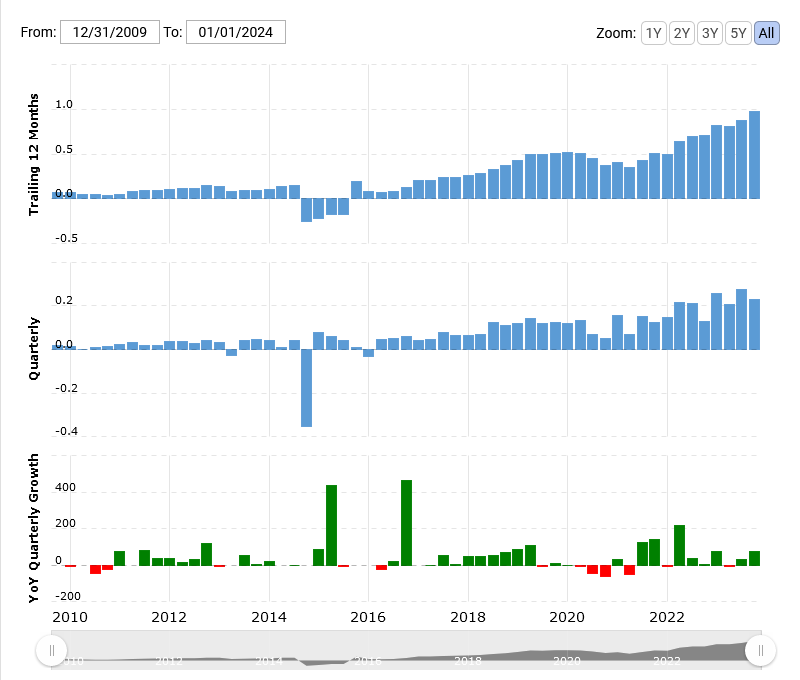

Equinix Net Income (MacroTrends)

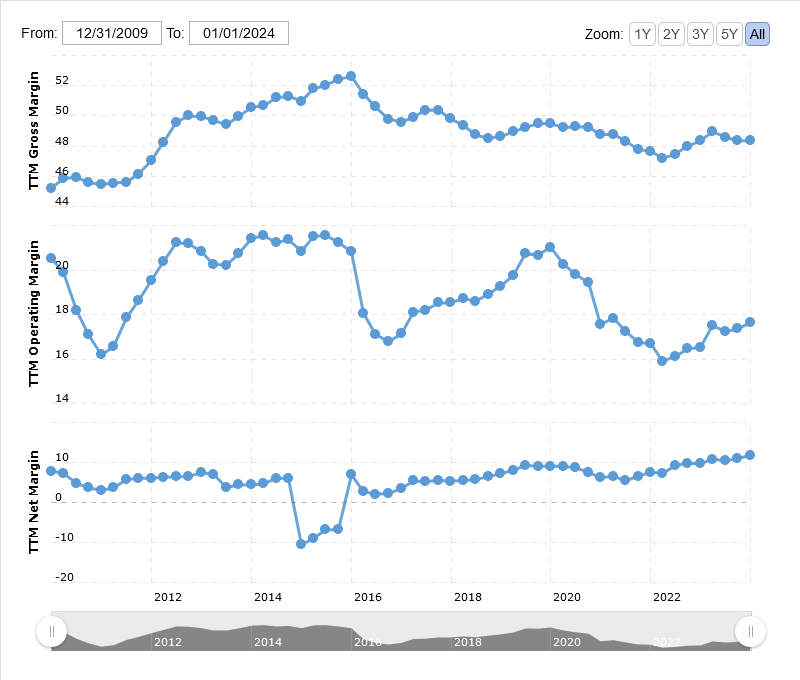

Equinix Profit Margin (MacroTrends)

Q2 2024 Earnings Call Transcript")