6381380/iStock Editorial via Getty Images

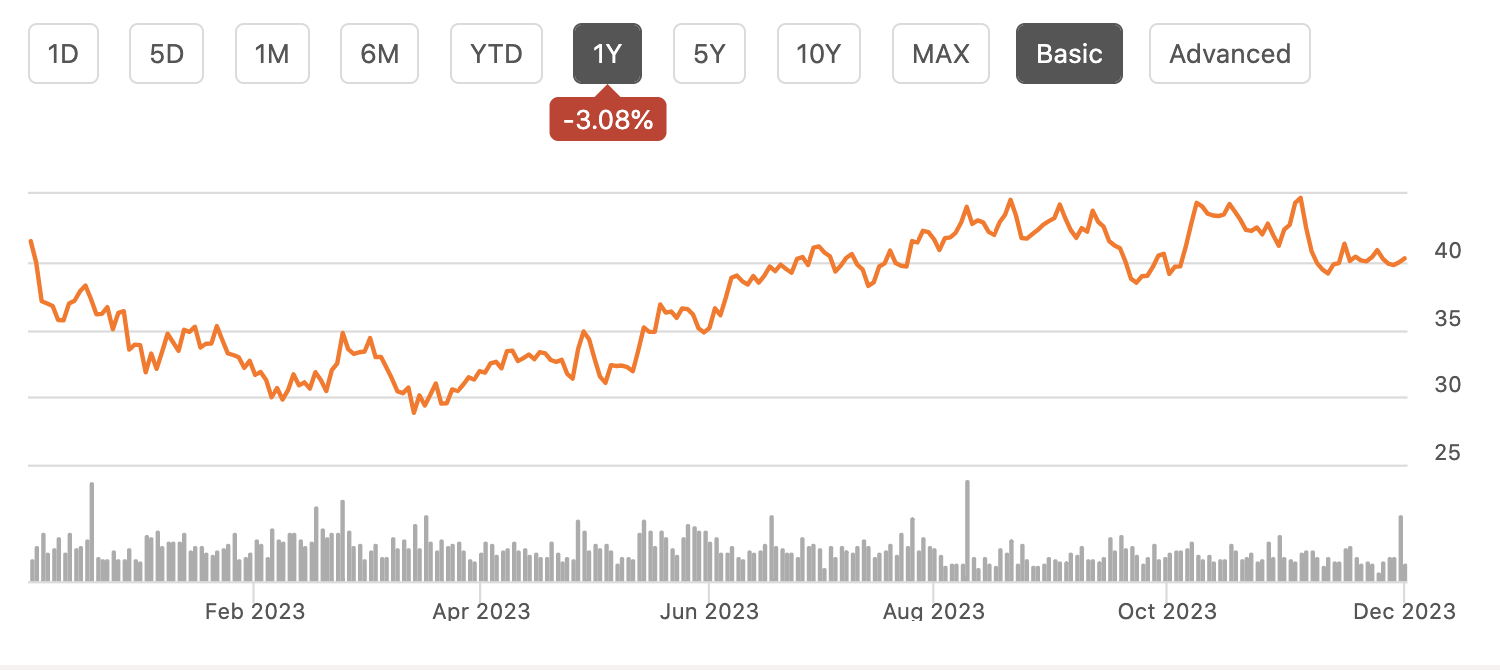

Shares of EQT Corporation (NYSE:EQT) have recovered nearly all of their losses this year, down just marginally from twelve months ago. This has been despite meaningfully lower natural gas prices, which have weighed on profitability. While hedges do furnish some near-term protection, the natural gas market has proven surprisingly weak, and I expect the company to fall short of its longer-term cash flow goals as a result.

Seeking Alpha

In the company’s third quarter, EQT earned $0.30, defying expectations for a loss of $0.10. Still, revenue was down 43% from last year when the company had $1.85 in GAAP EPS. The primary driver of weaker absolute results has been lower prices while solid operating performance explains why results have not been as bad as feared. EQT had average realizations of $2.28/mcfe from $3.41/mcfe last year, At this realization, EQT is essentially operating at cash flow breakeven, burning $2 million of free cash flow, though year to date it has still generated $642 million, given higher prices in H1.

Thanks to ongoing productivity improvements, EQT has reduced operating costs to $1.29/mcfe from $1.42 last year. On top of this, its cap-ex program costs $445 million in cap-ex, or $0.85/mcfe. That resulted in a cash cost of $2.27, which after net interest expense, left the company with a modest cash shortfall. This realization was even aided by hedges. The average natural gas price was $2.68, but it faced a $0.93 differential because production out of the Marcellus and Utica has been strong, leaving Northeast inventories high. It then earned back $0.12 from basis hedges and $0.27 from natural gas price hedges, for a $2.14 natural gas price. With higher prices on liquids, it earned an average of $2.28.

Now based on October natural gas pricing of $3.40, Management expects about $1.7 billion in 2024 free cash flow. However, natural gas prices have continued to fall, and are now solidly below $3. This market has essentially erased all gains seen last year when Russian gas exports to Europe stopped, forcing them to buy up as much LNG as possible.

Seeking Alpha

The fundamental problem is that while oil essentially functions as on global market, natural gas is still largely a local market. LNG capacity is fairly limited, given the costs, limited vessels, and few export facilities. Now, EQT aims to advance about 20% of its production to the Gulf Coast for export, but about 80% is trapped inside the US. Because firms admire EQT have found so much and keep getting better at producing it for less, local markets are staying weak and pricing loose.

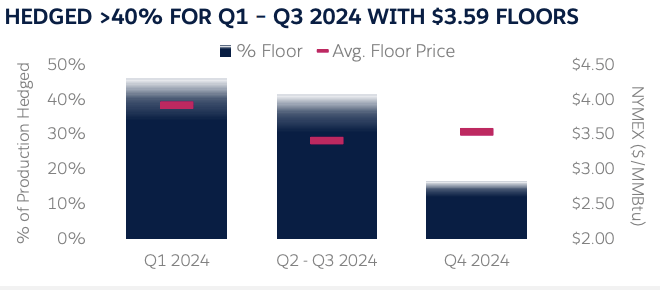

Now, fortunately, management has been hedging production via options to guard against a fall. It now has locked in about 40% of Q1-Q3 production at $3.59, though with the wide basis, its actual realization will be less. While this helps to insulate cash flow, the majority of its production is still unhedged, and hedges do not last forever. EQT said it expects to produce $14 billion of free cash flow through 2028 assuming $3.41 natural gas next year and $3.88 on average through 2028. While this may true, given that assumption, that strikes me as an overly optimistic assumption to base an investment on, given where natural gas trades today and what its demand dynamics are.

EQT

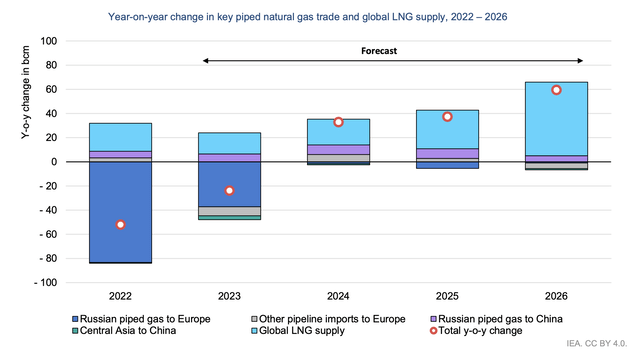

Given the War on Ukraine, piped gas to Europe fell significantly in 2022 and advance this year (as Russia was still supplying Europe in early 2022), according to data from the International Energy Agency. As you can see, growth in LNG has helped to offset this reject. LNG growth is expected to continue and should fully offset this lost gas by 2026. Frankly, given the fact markets are still relatively tight globally, it has been surprising to me natural gas prices have fallen quite as much as they have domestically, Europe’s shortfall has partially been negated by the fact some emerging countries pivoted slightly back to coal when gas prices rose so high

IEA

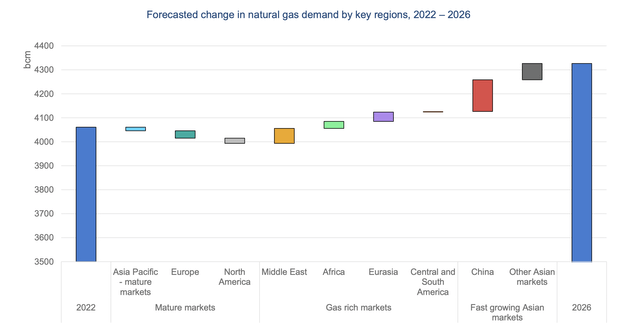

Now looking out several years, global gas consumption is still rising, as you can see below. China and the Middle East produce almost all net growth though as developed world growth is expected to be negative, given increases in renewables. Because natural gas operates as a semi-local market, the fact growth is largely overseas does not help firms admire EQT as much as if growth were here. Because trade and transport of this commodity are not frictionless, wide differentials across global markets can persist in a structural manner.

IEA

Global demand growth should furnish some tailwind, just not as large of one as was initially expected. Fundamentally, investors need to ask themselves, if one of the most important gas-producing nations can stop entirely gas exports to the world’s largest economic bloc, and natural gas prices cannot stay above $4, what possibly could make them do so? If commodity prices are going to stay relatively low, investment returns are unlikely to be strong, even if the company continues to produce productivity savings.

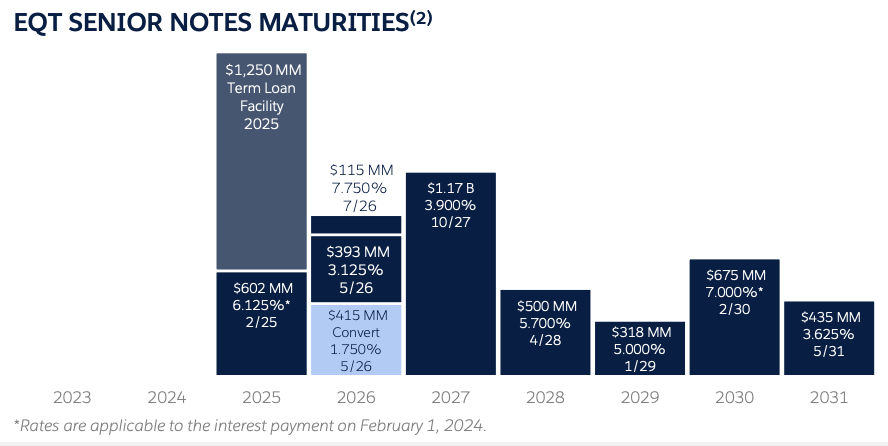

If we assume natural gas prices would average $3.00 over the next five years, EQT would likely produce about $8 billion in free cash flow instead of the $14 billion. Now, the company is currently carrying $5.9 billion in net debt. However, it is targeting 1-1.5x leverage at $2.75 natural gas, or $3.5 billion in debt, in keeping with its recently attained investment-grade ratings. As you can see, the company has no near-term maturities, a positive. I would expect it to pay down some debt at maturity in 2025-2026 as well as opportunistically repurchase debt in the open market.

EQT

After paying down debt, that leaves about $5.6 billion in free cash flow that it can return to investors over the next five years, still substantial, but half of the $11.6 billion, it could if natural gas is $3.88. Now, I am not arguing for certain that natural gas will be $3, rather I am highlighting the sensitivity of cash flow to prices. If natural as averaged $4.50, free cash flow would likely exceed $20 billion. However, given the nature of the commodity, I believe risks are skewed to lower than higher prices, especially considering how well the market responded to such a massive supply shock.

Hedges should keep free cash flow around $1-1.2 billion next year, even in $2.80-3 natural gas environment, but we will need to see natural gas rally to achieve $1.7, and all else equal, free cash flow would reject if prices persist at current levels in 2025 as hedges roll off.

At my midpoint $1.1 billion in free cash flow, shares have about a 6.7% free cash flow yield, on a company still aiming to reduce debt. I prefer the dynamics in the oil market where OPEC is aiming to limit supply, and demand is more global in nature. With companies admire Diamondback (FANG) trading with wider free cash flow yields in a market I view more constructively, I see better opportunities than EQT. I see fair value about 15% lower or about $34-35, at which point it would offer an 8% free cash flow yield. Given how much it has outperformed its underlying commodity, shares are now a sell.

Q2 2024 Earnings Call Transcript")