PonyWang/E+ via Getty Images

The Allspring Global Dividend Opportunity Fund (NYSE:EOD) is a closed-end fund that income-focused investors can employ as a method of achieving their goal of providing themselves with a very high level of current income from the assets that are in their portfolios. As the name of the fund suggests, this fund invests primarily in common equities, so potential investors do not need to sacrifice the capital gains potential that these securities possess. The fund should also do a better job of protecting its holders against the ravages of inflation than a fixed-income closed-end fund, which is something that will undoubtedly be appealing in today’s monetary and fiscal environment. After all, recent inflation data shows that the month-over-month movements in the consumer price index have been getting worse over the past few months:

Trading Economics

Equities historically provide better protection against inflation than fixed-income securities due to the fact that the profits and cash flows of the issuing companies should increase along with prices in such an environment.

The Allspring Global Dividend Opportunity Fund does reasonably well at providing investors with a high level of income as well, as it yields 9.48% at the current price. Investors who are still used to the very low-yield environment that dominated most of the past decade will certainly be attracted by the prospect of obtaining such a high yield from a common equity fund. However, let us see how well this fund’s distribution looks when compared to its peers:

|

Fund Name |

Morningstar Classification |

Current Yield |

|

Allspring Global Dividend Opportunity Fund |

Equity-Global Equity |

9.48% |

|

Clough Global Equity (GLQ) |

Equity-Global Equity |

11.47% |

|

Eaton Vance Tax-Advantaged Global Dividend Income Fund (ETG) |

Equity-Global Equity |

8.83% |

|

Lazard Global Total Return and Income Fund (LGI) |

Equity-Global Equity |

8.07% |

|

Royce Global Value Trust (RGT) |

Equity-Global Equity |

1.45% |

|

abrdn Global Dynamic Dividend Fund (AGD) |

Equity-Global Equity |

8.28% |

As we can quickly see, the Allspring Global Dividend Opportunity Fund is not the highest-yielding fund that is available in the sector. It does still manage a very good showing against its peers, though, which is likely to be rather appealing to those investors who are seeking to maximize their incomes. After all, the maximization of income is something that we all need in order to maintain the lifestyles to which we have become accustomed in today’s environment of rapidly rising prices. However, we should not buy a fund solely on yield alone, so let us investigate further.

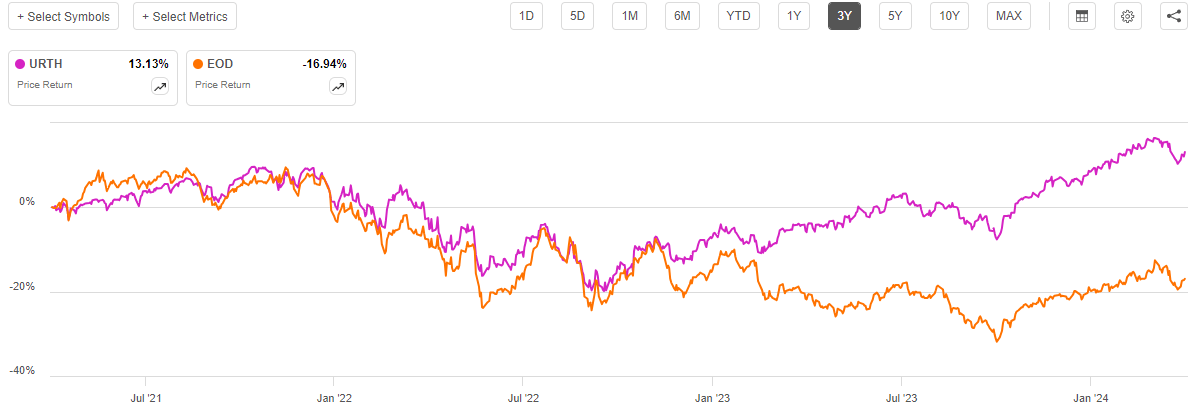

Unfortunately, a cursory glance at the fund’s recent share price performance is very discouraging. Over the past three years, shares of the Allspring Global Dividend Opportunity Fund have declined by 16.94%. This is far worse than the 13.13% gain that the MSCI World Index (URTH) has delivered over the same period:

Seeking Alpha

The fund’s performance against the index is even worse if we go back further than just three years. Over the trailing ten-year period, shares of the Allspring Global Dividend Opportunity Fund have declined by 43.35% compared to a 97.50% gain in the MSCI World Index. That alone might be enough to turn any investor away from this fund. After all, nobody enjoys losing money, and the fact that it has been going on for many years now suggests that this is not a one-time problem that is caused by a simple market hiccup.

However, as I have pointed out numerous times in the past, a simple look at the price performance of a closed-end fund does not tell the whole story. To quote a recent article:

A simple look at the share price performance of a given fund does not tell the whole story of how investors in a given fund actually did during a given time period. This is because closed-end funds pay out most or all of their investment profits to the shareholders in the form of distributions. The basic goal is to keep the portfolio size relatively stable while giving the shareholders all of the profits that are earned by the portfolio.

This is the reason why these funds tend to have a higher yield than just about anything else in the market. It also means that the shareholders are getting a return that is not reflected in the share price performance of the fund. The distributions that the fund pays will always result in the fund’s shareholders doing much better than the share price performance would suggest.

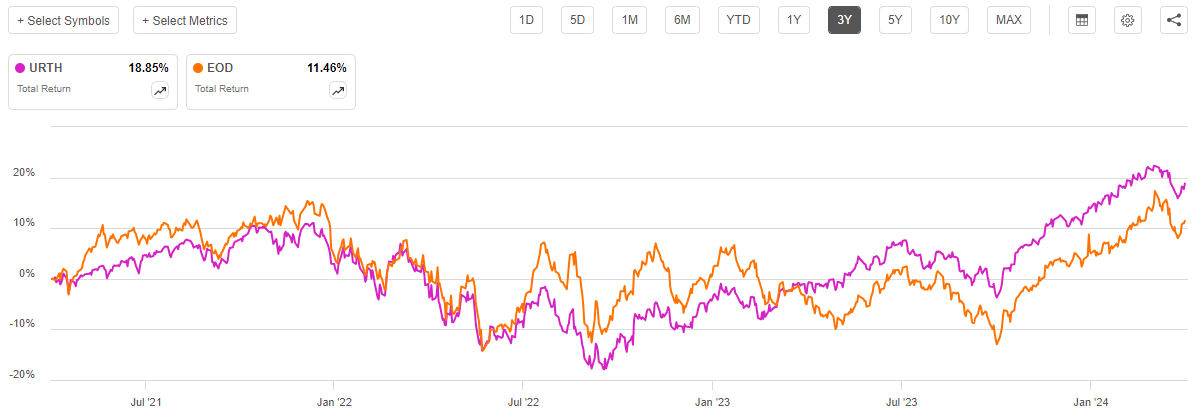

The last sentence in the above quote is key here. As I point out, shareholders in these funds always do better than the share price performance suggests, and this tends to compound over extended periods. As such, shareholders in a fund that suffers from a long-term share price decline can actually sometimes end up earning a positive return because the distributions that the fund pays out more than offset the declines in the share price. This is the case with this fund, as after accounting for the distributions that the fund paid out over the past three years, shareholders have actually received an 11.46% gain:

Seeking Alpha

This is, without a doubt, still worse than the MSCI World Index delivered over the same period. However, we can see that there were some periods in both 2021 and 2022 when the shareholders in this fund were actually doing better than investors in the index. That does not seem to be the case anymore and the MSCI World Index has been consistently beating the Allspring Global Opportunity Fund since April 2013 even when the distributions are included.

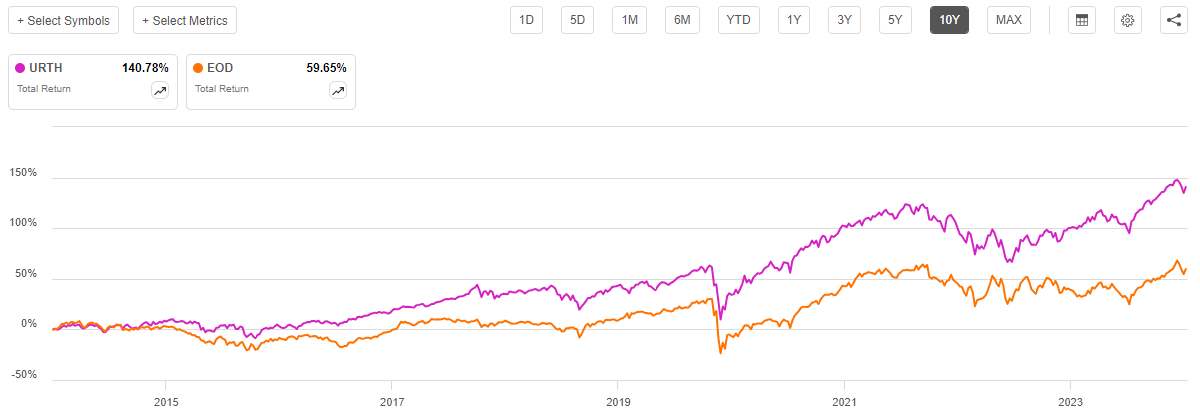

We see the same thing over the trailing ten-year period:

Seeking Alpha

In this case, investors in the Allspring Global Dividend Opportunity Fund have gained 59.65% over the period in spite of the fact that the share price itself was down. However, this was nowhere near sufficient to beat the 140.78% total return that the index delivered over the period (including dividends that the companies comprising the index paid out over the period). This certainly seems to suggest that investors who do not prioritize the high yield that the fund pays out would be better off investing in the index. However, that is typically the case with equity closed-end funds, as very few of them manage to beat a corresponding benchmark index over the long term.

The fact that this fund failed to beat the MSCI World Index over both the trailing three-year period and the trailing ten-year period is not sufficient reason to avoid the fund. After all, it might offer better diversification than the index or boast some other advantage that some investors might like to have. Let us investigate it further in order to determine whether or not this is the case.

About The Fund

According to the fund’s website, the Allspring Global Dividend Opportunity Fund has the primary objective of providing its investors with a high level of current income. The fund has the secondary objective of long-term growth of capital. The secondary objective certainly makes sense given the strategy that this fund intends to employ in pursuit of its objectives. However, it is a bit difficult to see how the fund can properly achieve its primary objective with its strategy. The fund outlines its strategy for achieving these dual objectives on its website:

Under normal market conditions, the fund allocates approximately 80% of its assets to an equity sleeve and the remaining 20% to a sleeve consisting of below-investment-grade debt.

The fact that this fund invests part of its assets in junk bonds and similar assets works pretty well with the provision of current income as a primary objective. However, we can see that its equity allocation will be significantly larger. The problem with this is that common equities are not particularly good vehicles for the provision of income. For example, consider the trailing twelve-month distribution yields of the exchange-traded funds tracking the major common equity indices:

|

ETF Name |

Index Tracked |

TTM Distribution Yield |

|

SPDR S&P 500 ETF Trust (SPY) |

S&P 500 |

1.32% |

|

iShares MSCI World ETF |

MSCI World |

1.60% |

|

iShares MSCI ACWI ETF (ACWI) |

MSCI All-Countries World |

1.78% |

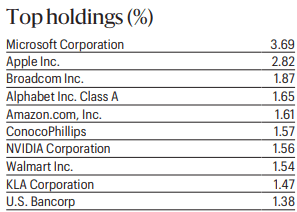

As we can immediately see, none of these index funds has a yield that is particularly attractive in today’s monetary environment. After all, an investor can easily obtain a 5% or higher yield simply by parking cash in an ordinary money market fund. In fact, even common equity sectors that are typically known for their yields such as utilities do not manage to deliver more attractive yields than the money market today. The only domestic equities that manage to deliver more attractive yields than the money market are a handful of energy partnerships, tobacco companies, and telecommunications companies. While foreign stocks do tend towards higher yields than domestic equities, most of them cannot deliver a more attractive yield than cash today. As equities account for the majority of this fund’s portfolio, it is difficult to see how it can properly pursue the provision of income. After all, this fund is not investing in energy partnerships, tobacco companies, and telecommunications firms. We can quickly see this by looking at the largest holdings in the fund, which are provided by its fact sheet:

Fund Fact Sheet

The above chart shows the largest holdings in the Allspring Global Dividend Opportunity Fund as of December 31, 2023. While that is admittedly four months out of date at this point, this is the most recent information available because this fund does not provide monthly updates of its largest holdings.

Here is the current dividend yield of each of these stocks:

|

Company |

Current Yield |

|

Microsoft Corporation (MSFT) |

0.74% |

|

Apple Inc. (AAPL) |

0.57% |

|

Broadcom Inc. (AVGO) |

1.56% |

|

Alphabet Inc. (GOOGL) |

0.48%* |

|

Amazon.com (AMZN) |

N/A |

|

ConocoPhillips (COP) |

1.78% |

|

Nvidia Corporation (NVDA) |

0.02% |

|

Walmart Inc. (WMT) |

1.38% |

|

KLA Corporation (KLAC) |

0.82% |

|

U.S. Bancorp (USB) |

4.77% |

* Alphabet’s dividend yield is calculated assuming that its recently announced $0.20 per share dividend will be paid every quarter.

As we can clearly see, none of these stocks offer a dividend yield that is higher than can be obtained by a money market fund. In fact, U.S. Bancorp is the only one that even manages to come close to that level. As such, this portfolio does not make a lot of sense if the fund is truly pursuing an income objective as it claims. It is certainly reasonable for a capital gains focus, however, since that is how the common stocks that comprise the largest positions in this fund will deliver the majority of their total investment return. This is normal for a common equity fund, although it does still pose the question of why the Allspring Global Dividend Opportunity Fund is claiming that its primary objective is the generation of current income when its portfolio is obviously constructed for capital gains.

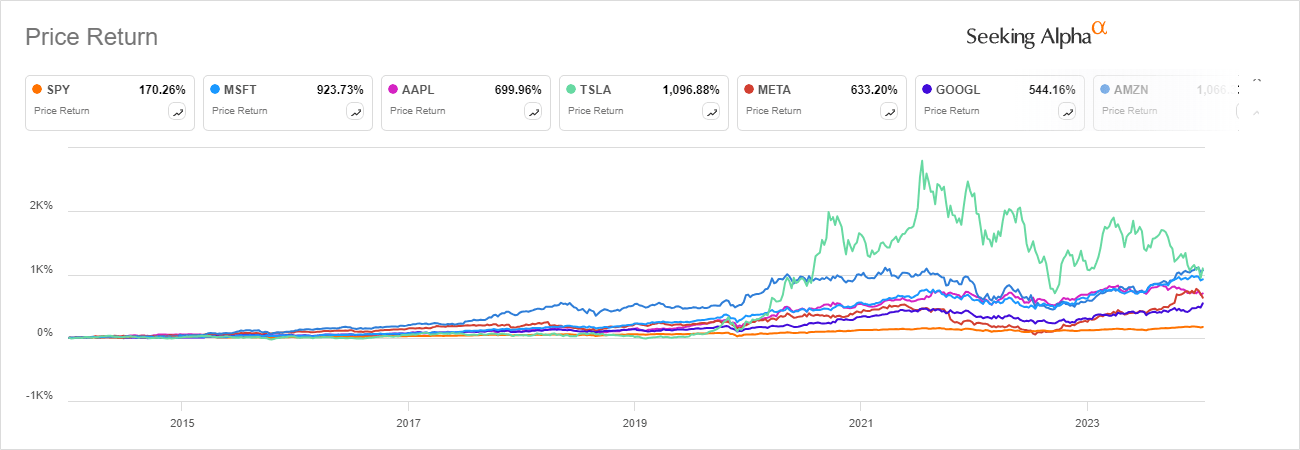

In the comments section of several of my recent articles on closed-end funds, there have been a number of readers whose comments reflect a desire to reduce their exposure to the so-called “Magnificent 7” stocks. This is a nickname given to seven American mega-cap technology companies that have been responsible for an outsized portion of the total returns of the equities market over the past several years. These seven stocks are Microsoft, Apple, Alphabet, Amazon.com, Meta Platforms (META), Tesla (TSLA), and NVIDIA. A few of these are also included in the “FAAMG” group that was responsible for a significant portion of the total return of the S&P 500 Index in the decade prior to the COVID-19 pandemic. For example, take a look at the performance of some of these stocks over the past ten years:

Seeking Alpha

The only stock that is excluded from the chart above is Nvidia, mostly because there was not sufficient room on the chart to include it. I do not think that I need to include that stock’s recent performance in order to make the point, however. In short, we can see that these stocks all outperformed the S&P 500 Index by quite a lot over the past ten years. As such, they have seen their weightings in the index increase due to the market capitalization increase (the S&P 500 Index is market-cap weighted). This also means that these stocks were responsible for a significant percentage of the total gain of the index over the period, and as such most investors in index funds now have significant exposure to them. In addition, due to the strong performance of these stocks relative to other things in the market, the managers of actively managed funds have been including them in the largest positions in their own funds. Overall, this situation has resulted in many investors having far more of their total assets tied up in these companies than they are comfortable with. This explains the desire to diversify away from these companies that I have been noticing in the comments to my articles on various closed-end funds.

Unfortunately, we can see that the Allspring Global Dividend Opportunity Fund does not seem to be a good choice for those investors who are looking to diversify away from the “Magnificent 7” technology stocks. The fund’s largest positions include five of the seven companies, with only Tesla and Meta Platforms excluded. Fortunately, the fund’s weightings to these stocks do appear to be somewhat lower than that of the MSCI World Index:

|

Company |

Weighting In Fund |

Weighting in MSCI World |

|

Microsoft |

3.69% |

4.53% |

|

Apple Inc. |

2.82% |

3.93% |

|

Alphabet Inc. |

1.65% |

1.61% |

|

Amazon.com |

1.61% |

2.64% |

|

Nvidia Corporation |

1.56% |

3.42% |

Alphabet is a strange one because of the dual-share class structure. The Class A shares alone account for 1.61% of the MSCI World Index. However, if we consider Alphabet to be one company, the Class A and Class C shares combined are 3.02% of the MSCI World Index. As such, the fund appears underweight to Alphabet relative to the index, despite the fact that its weighting in the fund is slightly above the index’s weighting to the Class A shares.

The fact that the fund appears to be generally underweight to the “Magnificent 7” might be appealing to those investors who are looking to improve the diversification of their equity assets. However, this fund does not do nearly as well at reducing an investor’s exposure to these stocks as many other funds that do not include them at all will. Unfortunately, as we have seen, these stocks have been responsible for an outsized proportion of the performance of most of the major large-cap indices over the past ten years, so most funds are almost forced to include them by default in order to avoid trailing the indices too badly.

The name of the Allspring Global Dividend Opportunity Fund suggests that the fund invests its assets all over the world. The fact sheet reinforces this conclusion, stating that:

[The equity] sleeve invests normally in 60 to 80 securities, broadly diversified across major sectors and regions.

However, we certainly do not see global or sector diversity in the fund’s largest positions. Every company in the top ten holdings list is an American company, and six of them are technology companies. That is certainly not reflective of diversity.

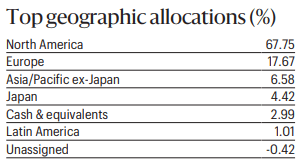

Fortunately, we do things improve in terms of international diversity when we look at the entire portfolio. As of December 31, 2023, 67.75% of the fund’s assets were invested in North American assets:

Fund Fact Sheet

The term “North America” generally means both the United States and Canada, but with the exception of energy infrastructure funds, the actual representation of Canadian companies in a fund’s portfolio is almost always very low. The fund’s January 31, 2024 holdings report states that 55.59% of the fund’s total assets are invested in American equities with an additional 18.46% of its assets invested in fixed-income securities from American issuers. That is a total of 74.05% of its assets invested in the United States alone, so Canada is almost certainly just an afterthought here. The holdings report states that 2.63% of the fund’s assets are in Canadian equities and 0.55% is invested in Canadian Yankee bonds. All of these figures are elevated a bit due to leverage, but it is still very obvious that an outsized percentage of the fund’s assets are invested in the United States, which only represents about a quarter of total economic output.

The United States accounts for 70.62% of the MSCI World Index, so it also appears that the fund’s holdings are a bit overweight to American assets relative to the index. That weighting alone suggests that the United States as a whole accounts for far more of the world’s asset valuations than is actually supported by the economic output of the nation, but that is a topic for another article. In short, this fund does not appear to be a great choice for those investors who are seeking to diversify their portfolios away from the United States. As many American investors have an outsized exposure to their home country, this is a category that probably includes a great many people. After all, we never want to have too much of our assets or financial well-being tied to any individual nation due to the risks of such a situation.

Leverage

As is the case with most closed-end funds, the Allspring Global Dividend Opportunity Fund employs leverage as a method of boosting the effective yield and total returns that it earns from the assets in its portfolio. I have explained how this works in various previous articles on other closed-end funds. To paraphrase myself:

In short, the fund borrows money and then uses this borrowed money to purchase common stocks and junk bonds issued by companies in both the United States and abroad. As long as the total return that the fund earns on the purchased assets is higher than the interest rate that it needs to pay on the borrowed money, the strategy works pretty well to boost the effective total return of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. As such, this will ordinarily be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage because that will expose us to an excessive amount of risk. I generally prefer that a fund’s leverage remain under a third as a percentage of its assets for this reason.

As of the time of writing, the Allspring Global Dividend Opportunity Fund has leveraged assets comprising 17.83% of its portfolio. This is a very reasonable amount of leverage for a global equity fund as we can see from this peer comparison:

|

Fund Name |

Leverage Ratio |

|

Allspring Global Dividend Opportunity Fund |

17.83% |

|

Clough Global Equity |

28.67% |

|

Eaton Vance Tax-Advantaged Global Dividend Income Fund |

19.80% |

|

Lazard Global Total Return and Income Fund |

29.63% |

|

Royce Global Value Trust |

5.08% |

|

abrdn Global Dynamic Dividend Fund |

1.21% |

(all figures from CEF Data)

As we can see, there are some well-regarded peer funds with higher levels of leverage than the Allspring Global Dividend Opportunity Fund. This is a positive sign as it does suggest that the fund is not employing an excessive level of leverage for its strategy. The fund also has well below the one-third of assets level that we ordinarily prefer an equity closed-end fund to possess.

Therefore, it does not appear that we need to worry too much about the fund’s use of leverage right now. The Allspring Global Dividend Opportunity Fund has a level of leverage that should allow it to strike a good balance between the rewards of using a leveraged portfolio and the risks involved in doing so.

Dividend Analysis

As mentioned earlier in this article, the primary objective of the Allspring Global Dividend Opportunity Fund is to provide its investors with a high level of current income and long-term capital appreciation. The fund pursues this objective by investing its assets in a portfolio that consists of roughly an 80/20 split between common stocks and junk bonds. This is perhaps not the best strategy for the provision of current income, but the fund can hopefully supplement the meager dividends paid by the common stocks with realized capital gains. The combination of the bond income and the capital gains should provide a satisfactory return, and this fund boosts it by borrowing money in order to control more common stocks than it could afford solely through reliance on its own equity capital. This allows it to boost its income by the difference between the money that it receives from the common stocks and bonds and the money that it has to pay in interest on the borrowed money. Finally, the fund takes all of the money that it earns from these various sources and pays it out to its shareholders, net of its expenses. We might expect that this business model would result in the fund’s shares boasting a very high distribution yield, given the high yields available on junk bonds and the capital gains from common stocks.

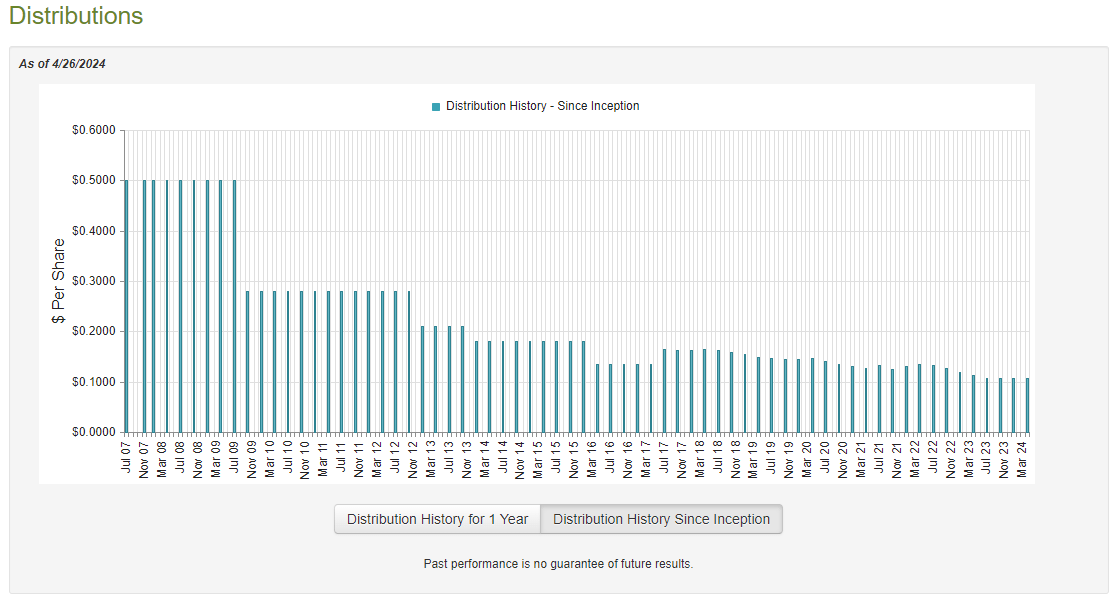

This is indeed the case, as the Allspring Global Dividend Opportunity Fund pays a quarterly distribution of $0.1080 per share ($0.4320 per share annually). This gives the fund a 9.48% yield at the current price. As we saw in the introduction, this yield compares reasonably well to that of its peers, but it is not the highest yield that is currently available in the market. Unfortunately, the fund has not been particularly consistent with respect to its distribution over the years. As we can clearly see here, the fund has raised and lowered its distribution on a very regular basis over the years:

CEF Connect

The overall trend has been for the fund to lower its distribution over time, although there have been a few times in which it raised its distribution. The fact that the distribution changes on a regular basis is not surprising considering that this fund employs a managed distribution policy. The fund’s most recent annual report explains this policy:

The Fund’s managed distribution plan provides for the declaration of quarterly distributions to common shareholders of the Fund at an annual minimum fixed rate of 9% based on the Fund’s average monthly net asset value per share over the prior 12 months. Under the managed distribution plan, quarterly distributions may be sourced from income, paid-in capital, and/or capital gains, if any. To the extent that sufficient investment income is not available on a quarterly basis, the Fund may distribute long-term capital gains and/or return of capital to its shareholders in order to maintain its managed distribution level.

Thus, to a certain extent, the fund’s distribution will vary based on the performance of its assets in the market. After all, an increase in the size of the fund’s portfolio from strong market performance should lift the average figure that it uses for its distribution. However, this policy also requires that the fund consistently return 9% in order for the fund to avoid over-distributing and destroying its net asset value. While the market tends to deliver this return on average, there is no guarantee that it always will.

The fact that the fund’s managed distribution policy results in a variable distribution will undoubtedly reduce its appeal to those investors who are seeking to earn a safe and secure income from the assets in their portfolios. However, it does make sense from the perspective of balancing the distributions with market performance. As just mentioned, though, it is certainly possible that the fund’s stated policy will result in it paying out more than the fund can really afford. We should investigate this further.

Unfortunately, we do not have an especially recent report that we can consult for the purposes of our analysis. As of the time of writing, the most recent financial report that is available for the Allspring Global Dividend Opportunity Fund is the annual report that corresponds to the full-year period that ended on October 31, 2023. A link to this report was provided earlier in this section of this article. As this report only covers the period through the end of October of last year, it will not include any information about the fund’s performance over the past seven months or so. This is disappointing because equity markets around the world began their recent rally in late October. Prior to that (through roughly mid-October), asset prices were falling, and yields were rising as investors and other market participants began to digest the very real possibility that the world’s central banks would be holding interest rates high and failing to pivot. The fund’s most recent published report will not include any information about how well it did at earning profits during the current market rally. However, it will provide us with a reasonably good idea of how well the market handled the summer of 2023, which was a bear market. As I have pointed out before, a fund’s performance during challenging market conditions is more reflective of the quality of its management than its performance during a raging bull market. After all, anyone can make money when asset prices are rapidly rising.

For the full-year period that ended on October 31, 2023, the Allspring Global Dividend Opportunity Fund received $8,934,902 in dividends along with $3,504,137 in interest from the investments in its portfolio. When we combine this with a small amount of income from other sources (mostly money market profits), the Allspring Global Dividend Opportunity Fund brought in $12,625,373 in investment income for the period. It paid its expenses out of this amount, which left it with $6,515,908 available for shareholders. As might be expected, this was not sufficient to cover the fund’s distributions, which totaled $19,317,468 for the full-year period. At first glance, this is likely to be quite concerning, as the fund did not have sufficient net investment income to fully cover its distributions.

However, there are other methods that this fund can employ in order to obtain the money that it requires to cover its distributions. For example, it might be able to sell a common stock after it rises in price in order to realize capital gains. Realized capital gains are not considered to be investment income for tax or accounting purposes, but they clearly do represent money coming into a fund that can be paid out to the shareholders.

Fortunately, the fund had a certain amount of success at earning money via these alternative sources. For the full-year period that ended on October 31, 2023, the Allspring Global Dividend Opportunity Fund reported net realized losses of $2,932,048, but these were fully offset by $13,751,787 net unrealized gains. While this was a reasonably solid performance, it was not sufficient to fully cover all the distributions that the fund paid out. Overall, the fund’s net assets declined by $2,021,557 after accounting for all inflows and outflows.

We can clearly see that the Allspring Global Dividend Opportunity Fund failed to cover its distributions for the most recent full-year period. This is not a new problem as the fund’s net assets declined by $63,047,432 after accounting for all inflows and outflows during the full-year period that ended on October 31, 2022. Thus, as of the time of the fund’s most recent financial report, it had failed to cover its distributions for two straight years.

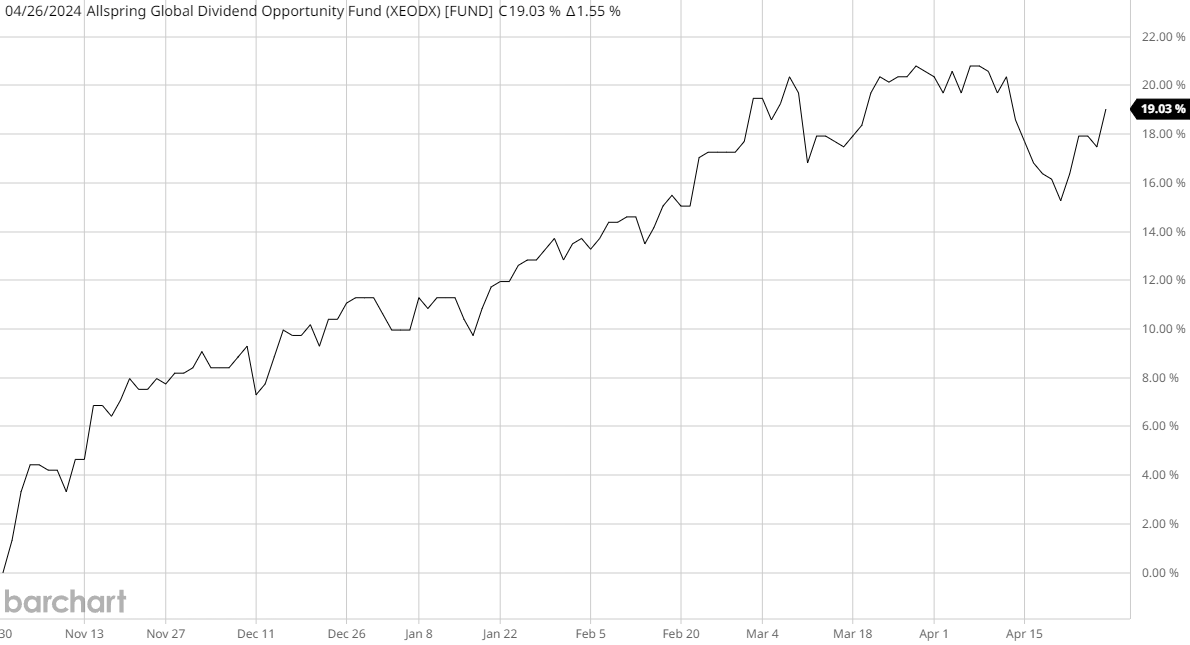

Fortunately, it does appear that the fund has solved this problem since the closing date of its most recent financial report. This chart shows the fund’s net asset value since October 31, 2023:

Barchart

As we can clearly see, the fund’s net asset value has increased by 19.03% since the closing date of the most recent financial report. This basically means that it has fully covered all of the distributions that it paid out over the past seven months, with a substantial amount of investment profits left over. As long as this continues, we probably do not need to worry too much about the fund’s distributions. However, there is no guarantee that this will be the case.

Valuation

As of April 26, 2024 (the most recent date for which data is available as of the time of writing), the Allspring Global Dividend Opportunity Fund has a net asset value of $5.38 per share but the shares only trade at $4.60 each. This gives the fund’s shares an enormous 14.50% discount on net asset value at the present price. This is an exceptionally large discount that is quite a bit higher than the 11.93% discount that the shares have traded at on average over the past month.

Thus, the current price looks like a pretty good entry point for anyone who wishes to add this fund to their portfolio today.

Conclusion

In conclusion, the Allspring Global Dividend Opportunity Fund is a high-yielding equity fund that also includes an allocation to junk bonds in order to improve its income. Despite the implication of the fund’s name, the Allspring Global Dividend Opportunity Fund is not nearly as well diversified internationally as most global investors might prefer. In fact, the fund maintains a sizable allocation to the United States, so investors who have a sizable level of exposure to the United States might want to look elsewhere. The fund also failed to cover its distributions over the past two years, but it appears that it may have improved this situation somewhat as its net asset value has risen substantially since November 1, 2023. The fund might be worth thinking about given its enormous discount if it can be put into a portfolio without resulting in concentration problems.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")