grandriver

Investment Rundown

EnLink Midstream, LLC (NYSE:ENLC) is a midstream company with a pretty well-diversified footprint in the US right now. The company has had a decent in the last 12 months, with the shares up by over 5%, but also up very impressively from the bottom of $8.4 per share it had in May of this year. However, with the FWD P/E GAAP at over 25, I find there to be quite little value to be had here right now, unfortunately. The company needs to rapidly extend its bottom line, which of course is driven by more positive commodity prices, but I think it is fair to say it may have run a little too far and a correction may be due soon.

I think that the dividend seems well-supported in all honesty, and sitting on shares in ELNC over the long term doesn’t seem admire a bad option. both oil and gas are going to be here for decades still. What ENLC is advance doing is quickly expanding into appealing markets in the US admire the Permian Basin, for example, one that could derive significant growth opportunities for the business. With the current premium so high though I won’t be a buyer here but rather a holder sitting tight and collecting a solid dividend.

Company Segments

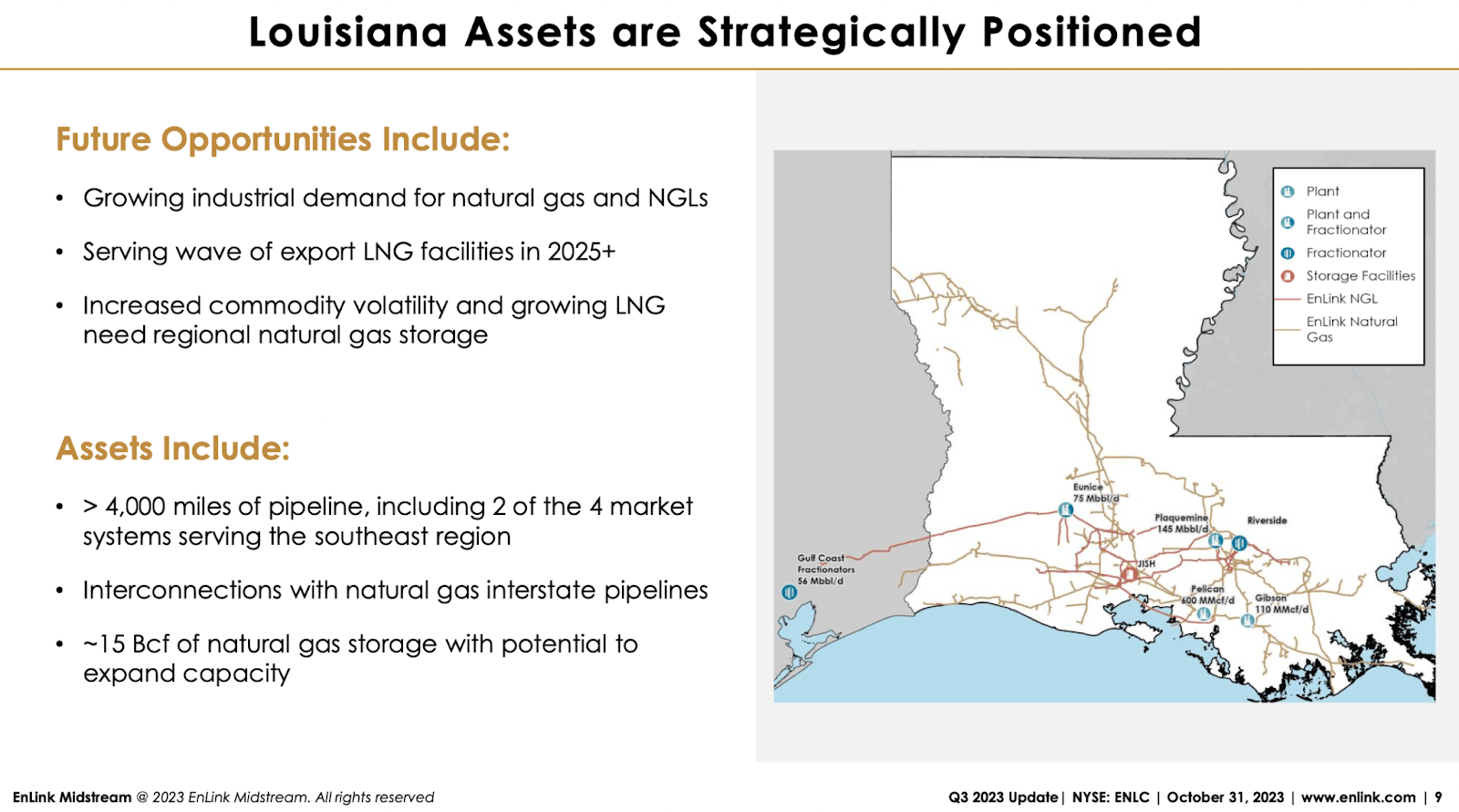

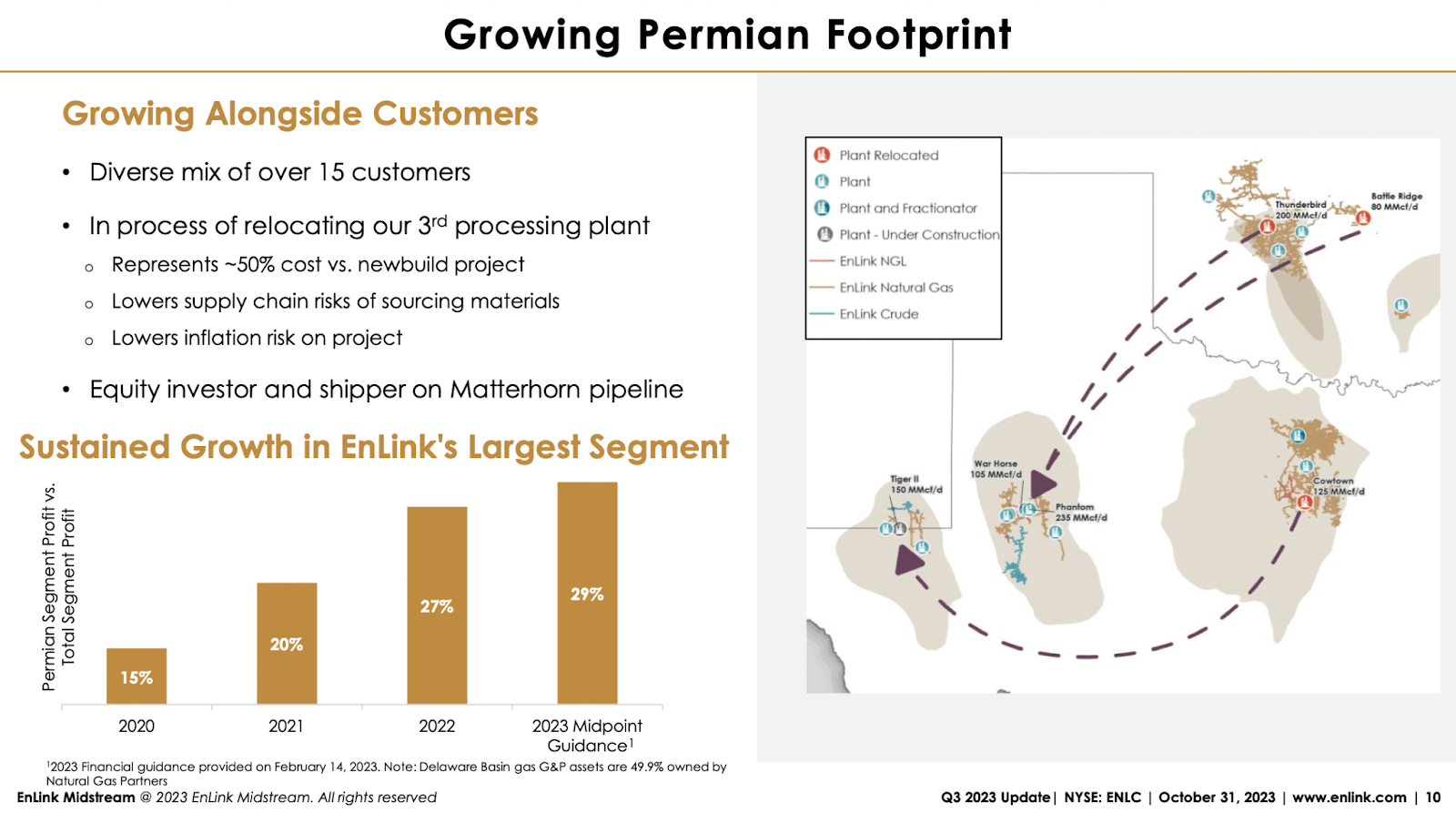

ENLC stands as a mid-sized player in the dynamic midstream sector, strategically positioned across key basins in the south-central United States. The company operates in significant regions, including the Permian Basin, Anadarko Basin, Barnett Shale, and Haynesville Shale. This diversified approach allows ENLC to tap into the energy potential of various basins, enhancing its adaptability and strategic strength in the ever-evolving energy industry.

Asset Allocations (Investor Presentation)

ENLC engages in a comprehensive spectrum of activities within the energy sector. Its operations encompass gathering, compressing, treating, processing, transporting, and selling natural gas. Additionally, the company is involved in the fractionation, transportation, storage, and sale of natural gas liquids. advance diversifying its portfolio, ENLC plays a role in gathering, transporting, stabilizing, storing, trans-loading, and selling crude oil and condensate. This broad range of activities positions the company as a key player in the intricate web of processes essential to the energy value chain.

Market Footprint (Investor Presentation)

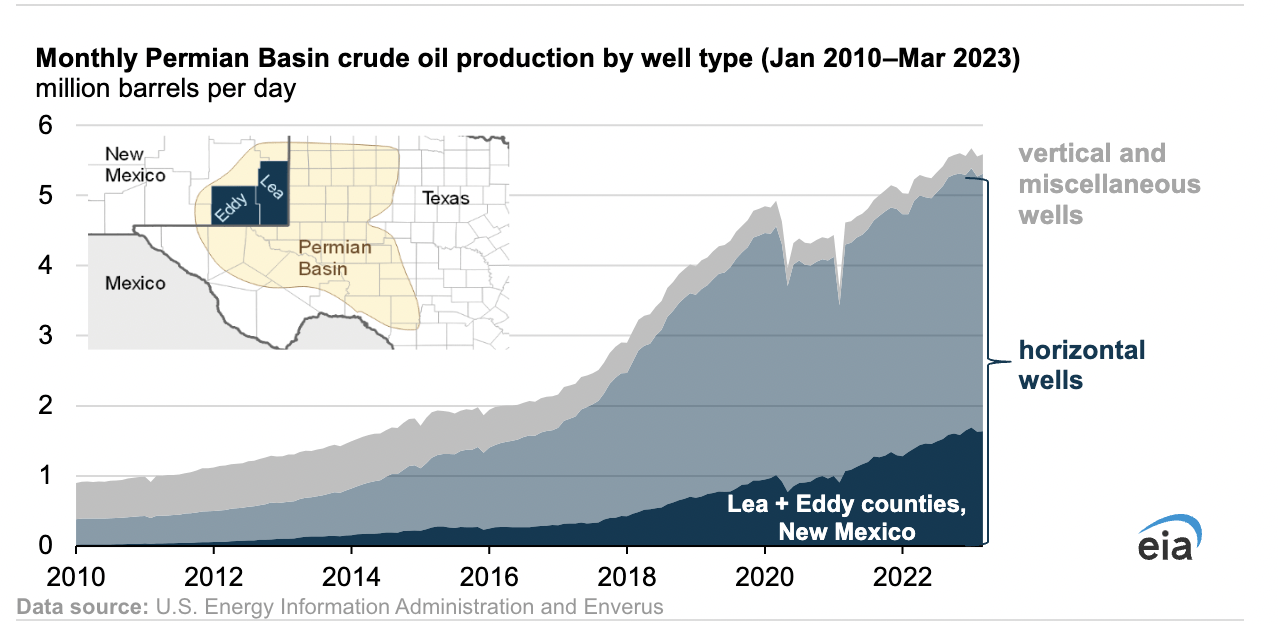

The Permian Basin stands as one of the most prolific oil and natural gas regions in the United States, playing a pivotal role in the nation’s energy landscape. Known for its vast hydrocarbon resources, the Permian Basin has been a major contributor to the surge in U.S. oil production over the past decade. Its strategic significance is underscored by the abundance of shale formations, particularly the Wolfcamp and Spraberry plays. The outlook for oil and natural gas in the Permian Basin remains positive, driven by ongoing advancements in extraction technologies and the region’s substantial reserves.

Permian Basin (US Energy Information)

With oil and gas continuing to be vital parts of our energy generation, I think having some exposure to these markets is still very much appealing. With ENLC, for instance, you are getting a very solid business with a devotion to reward shareholders through its dividend program, which right now is yielding above 3.8%. With that said, though, the current valuation of the business is on the other hand not that appealing. The FWD P/E GAAP is 137% above the sector average, and I find this to be quite a problem if we are to make a buy case. The price does not offer enough incentive of value to be a buy. I will be discussing it a little bit more below, but in conclusion, investors are better off holding onto shares and collecting the solid dividend the company has.

Markets They Are In

Market Outlook (MarketsandMarkets)

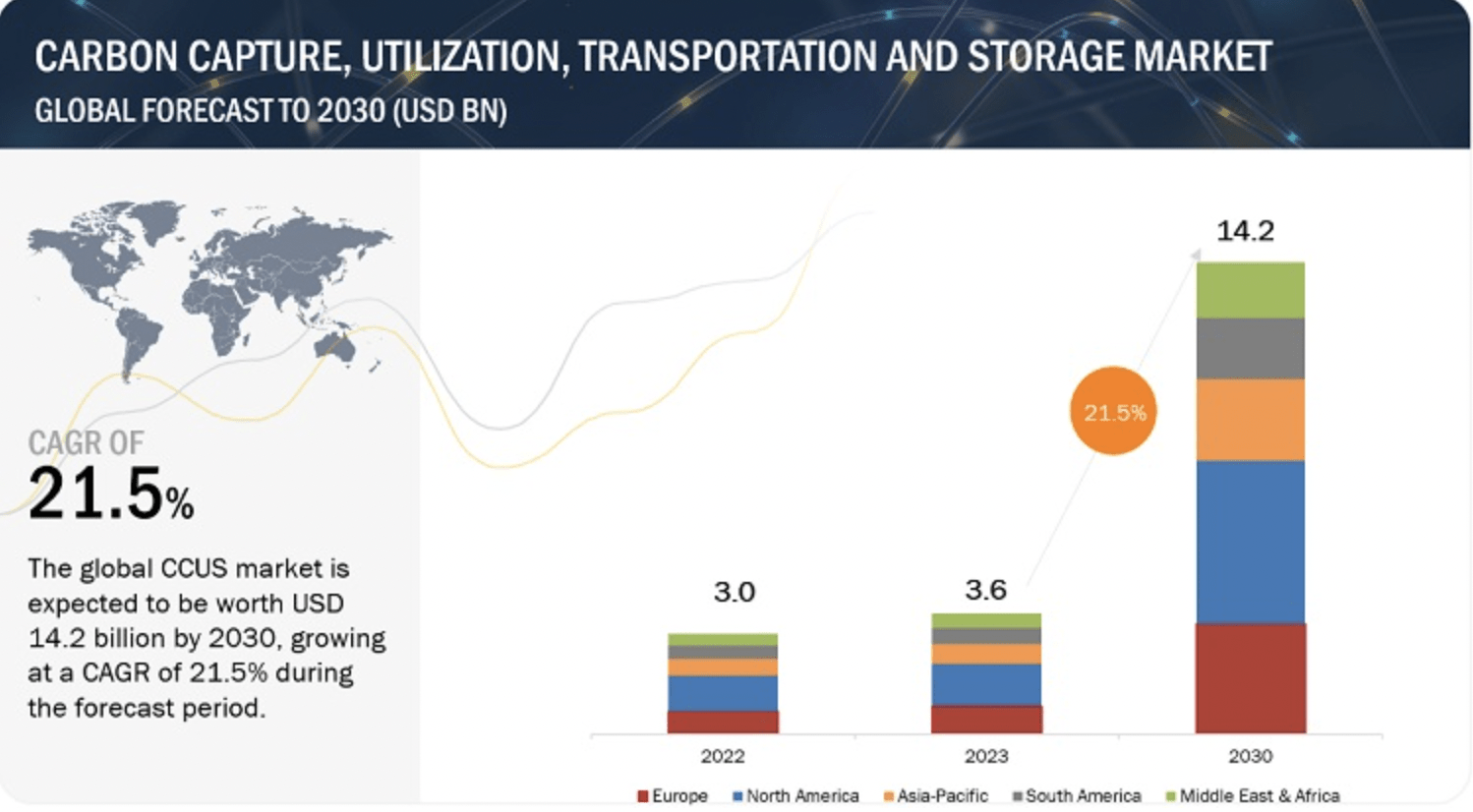

Carbon Capture and Storage (CCS) and Carbon Capture, Utilization, and Storage (CCUS) represent pivotal processes designed to capture carbon dioxide emissions, primarily from industrial activities such as steel and fertilizer production. Rather than releasing this CO2 into the atmosphere, these processes aim to either sequester it permanently underground or repurpose it for various applications, including enhanced oil recovery or even the creation of fizziness in carbonated beverages.

ENTC has been making decent progress in expanding into these ventures and with the market outlook suggesting a 21.5% CAGR until 2030 I think ENTC is right to do as well. The company asserts that it would preserve a high single-digit adjusted EBITDA multiple by managing the initial 3.2 million tons of carbon. However, this dynamic undergoes a significant shift, transitioning to a low single-digit adjusted EBITDA multiple should the company eventually handle the full ten million tons. In terms of how this would look on the income statement for ENTC should equal around $20-50 million additional EBITDA as the upfront investments total around $200 million. Now I think it should be noted as well that the actual capturing of carbon won’t commence until 2025 so seeing steady climbs in the EBITDA won’t be visible until then. Nonetheless, by 2026 investors could expect roughly $35 million additional EBITDA added to the income statement which is roughly a 3% annual boost from the 2022 results which were $1.3 billion.

Earnings Highlights

Income Statement (Earnings Report)

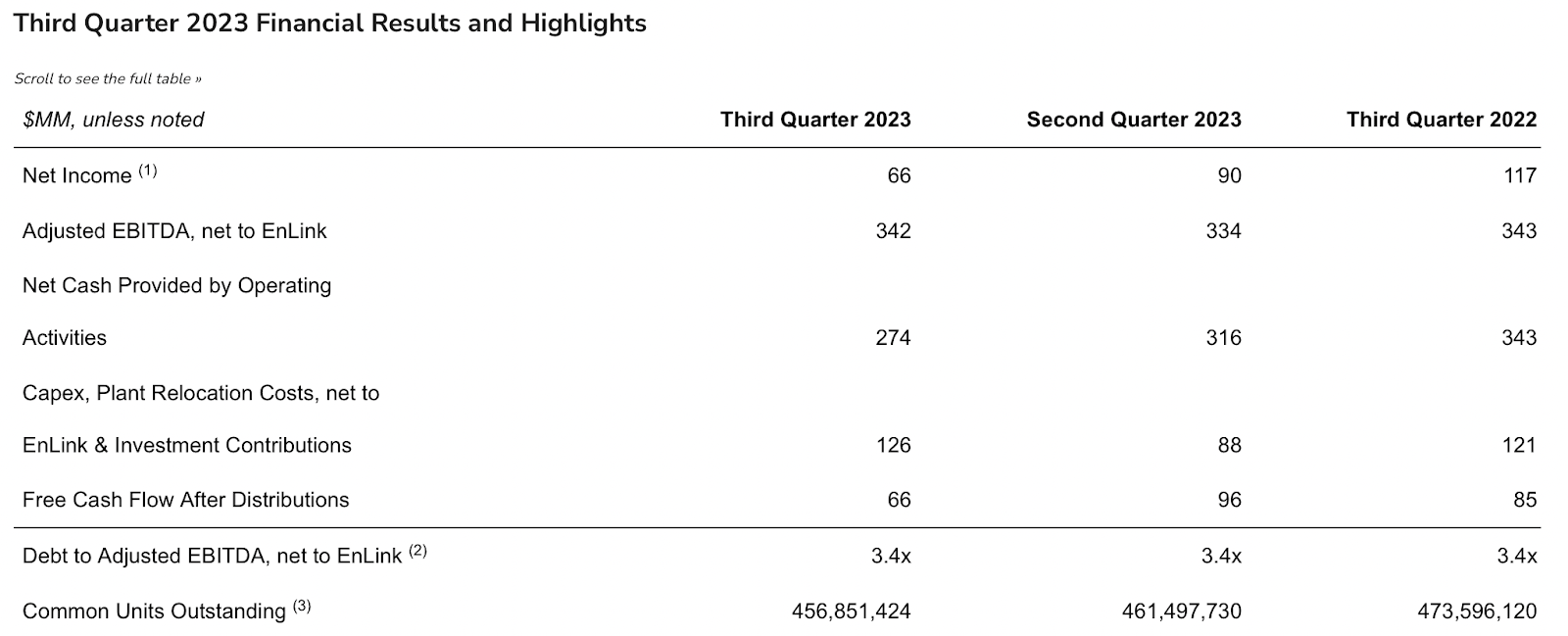

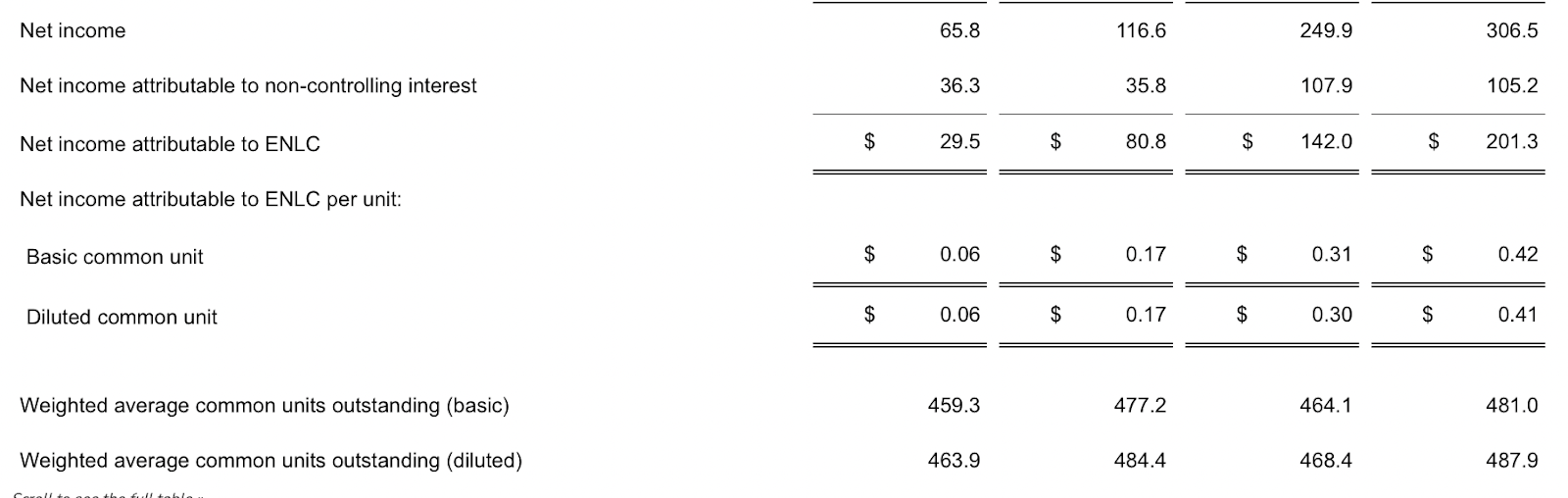

From the last income statement by the company, it was clear that the previous year’s strong commodity price environment was very beneficial. On a YoY basis, the net income for ENTC for Q3 declined by 77% in total, down to $66 million from $117 million. Much was driven by the nearly $1 billion lower in revenues the company did but also the stickiness of depreciation on its assets which was $162 million in total. I am worried about the coming quarters and the bottom-line growth for ENTC. If they are not capable of maintaining margins through tough pricing periods, then a lower valuation should be applied to adequately portray the risks involved.

Income Statement (Earnings Report)

With higher interest rates as well in the US, the company has also been forced to pay higher interest expenses, which grew by 12% YoY to $67.9 million. I think that these interest expense will just continue to climb as ENTC has a debt position of over $4.6 billion currently and are not generating enough EBITDA to sufficiently pay down large sums of it yearly, at least in my opinion. If they want to continue to invest in the CCS projects, then they will have to efficiently manage their debt levels as well. CCS projects are costly as we have discovered.

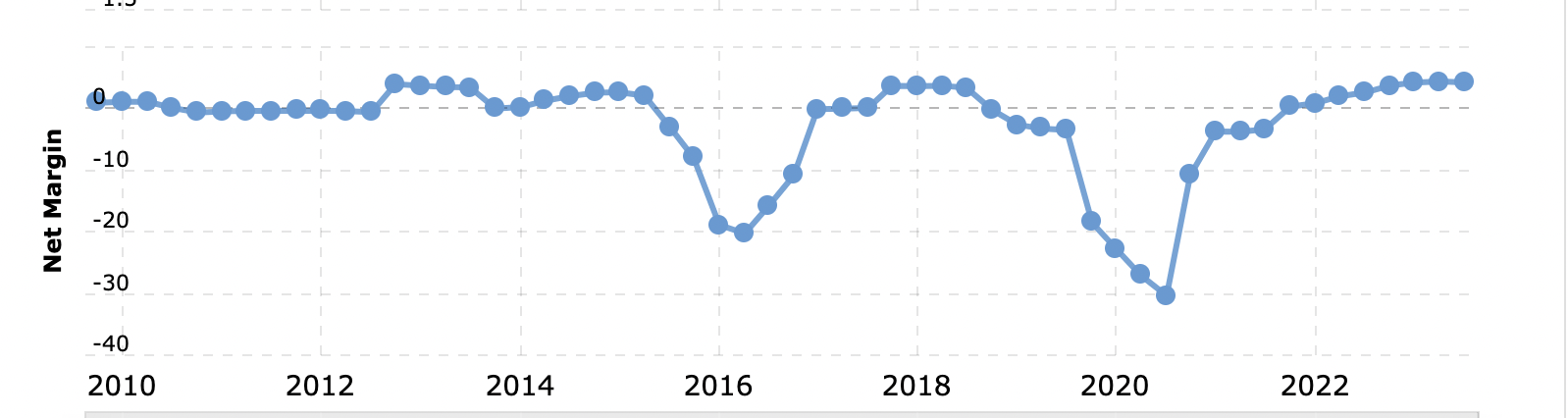

Net Margin (Macrotrends)

For the coming quarters, I want to see advance expansions in the margins. Since 2020 they have steadily been on the rise for the company but in my view, they aren’t growing fast enough to defend the current valuation. I would much prefer to buy in the range of 10-12x earnings, and that leaves a significant downside here still. But as I see ENTC as a long-term play, downside risk admire that doesn’t make me want to sell, but rather to just not buy or add more. As the price would fall, the dividend would continue to rise as well, leaving me with an even better deal.

Risks

As ENTC experiences steady growth, a notable aspect of its business trajectory has been its premium valuation. The concern arises when contemplating the scenario of stagnant or declining growth, potentially causing the share price to swiftly revisit the year lows of $8.4 per share. This apprehension stems from the perceived risk inherent in the business.

P/E (Seeking Alpha)

For investors, this risk factor should be a crucial consideration, representing a significant determinant in the assessment of whether the company can currently be regarded as a favorable investment. It emphasizes the importance of monitoring growth sustainability and the associated valuation metrics as key indicators for informed investment decisions.

Final Words

The oil and gas industry are almost the backbone of the US economy in some sense, seeing as they are responsible for powering our societies and also bring in vast amounts of revenues. ENTC has seen an impressive recovery from its lows back in May this year but is at a point where I don’t consider the price fairly valued. I would prefer something in the range of 10-12x earnings, which is similar to its sector but also means ENTC trades at a significant premium to that. My reasoning behind a hold comes from the fact I think the dividend is solid and something that makes me still get some value from holding shares. Should we see the price return to the $8-9 range again, I think I would turn more bullish

Q2 2024 Earnings Call Transcript")