batuhanozdel/iStock via Getty Images

Empire State Realty Trust, Inc. (NYSE:ESRT) has had a stellar year against wider doom calls from bears about the end of urban US office real estate. The REIT is up 44% year-to-date to cap a stunning recovery from a Fed-induced selloff. Whilst there are concerns about whether or not the rally has overextended itself, the near-term outlook for the REIT is strong with headline CPI continuing to refuse to set the backdrop for interest rate cuts in the first half of 2024. REITs have positive duration risk and have been near-toxic investments since the Fed embarked on its battle with inflation. Whether to build a position in ESRT against what’s now a 9.7x price to annualized 2023 third-quarter FFO multiple will depend on the direction of what’s currently bullish macroeconomic indicators. US GDP is growing, inflation is falling, and the Fed has indicated at least 3 interest rate cuts next year. This is the Goldilocks scenario for bulls and the worst-case scenario for REIT bears.

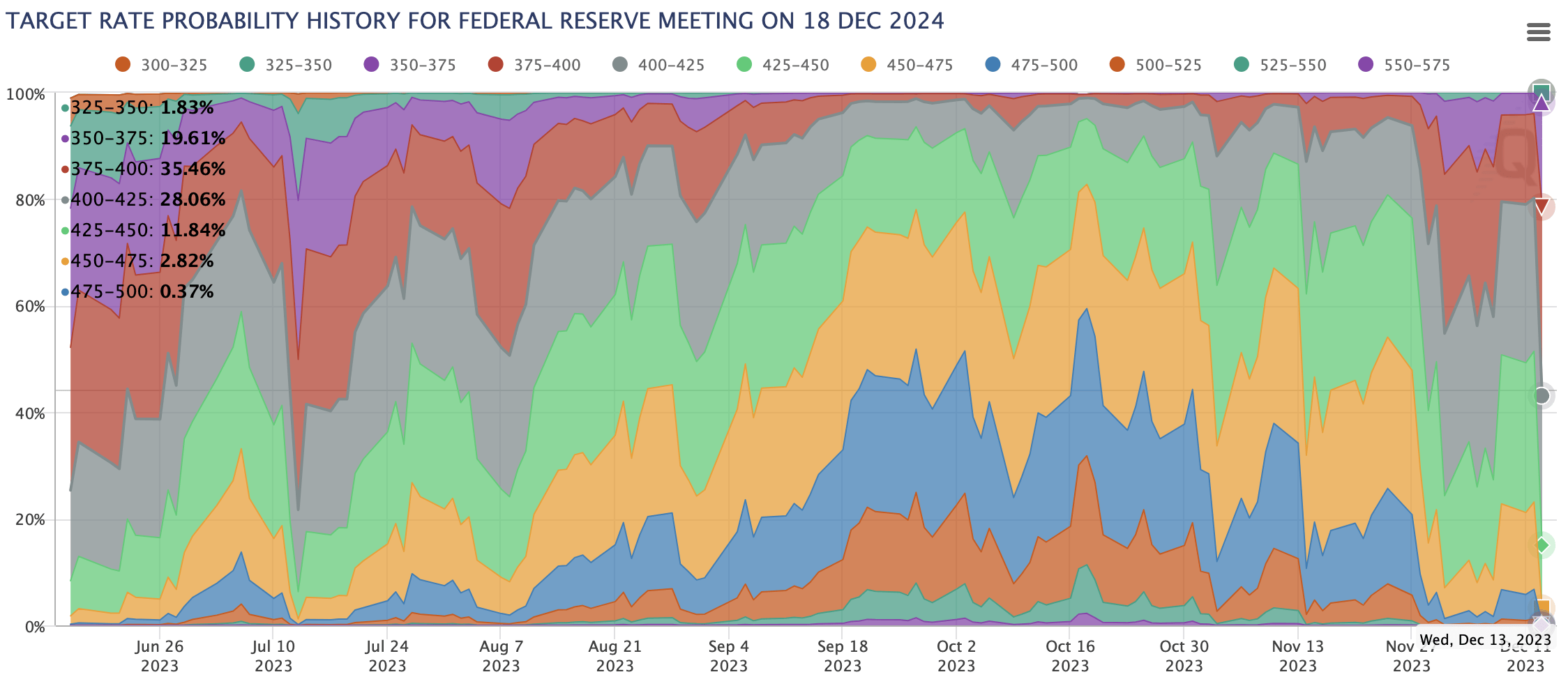

CME FedWatch Tool

The likelihood of interest rates being at their present 5.25% to 5.50% at the end of 2024 is essentially zero with the market as per the CME FedWatch Tool pricing in the chance of rates having been cut by 150 basis points to 3.75% to 4.00% as the base scenario for next year. ESRT held a total debt balance of $2.24 billion at the end of its third quarter with roughly 3.86% of this balance, around $86.54 million, coming due next year. Critically, interest rate cuts will set the backdrop for the favorable refinancing of debt with ESRT facing more material principal payments from 2025. It’s hard to see the bearish base remaining through 2024.

Empire State Realty Trust Fiscal 2023 Third Quarter Form 10-Q

Occupancy Gains And NOI Growth

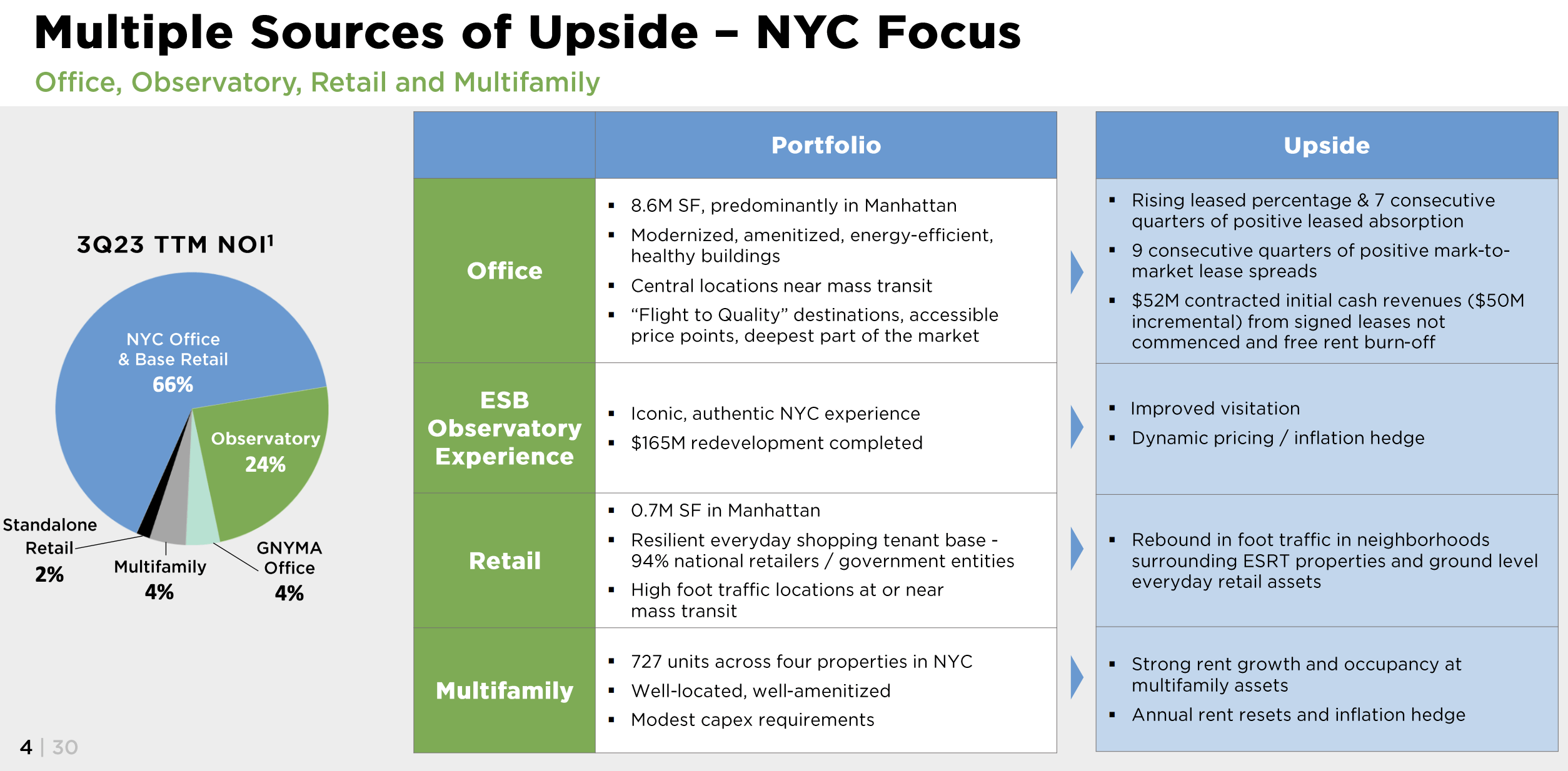

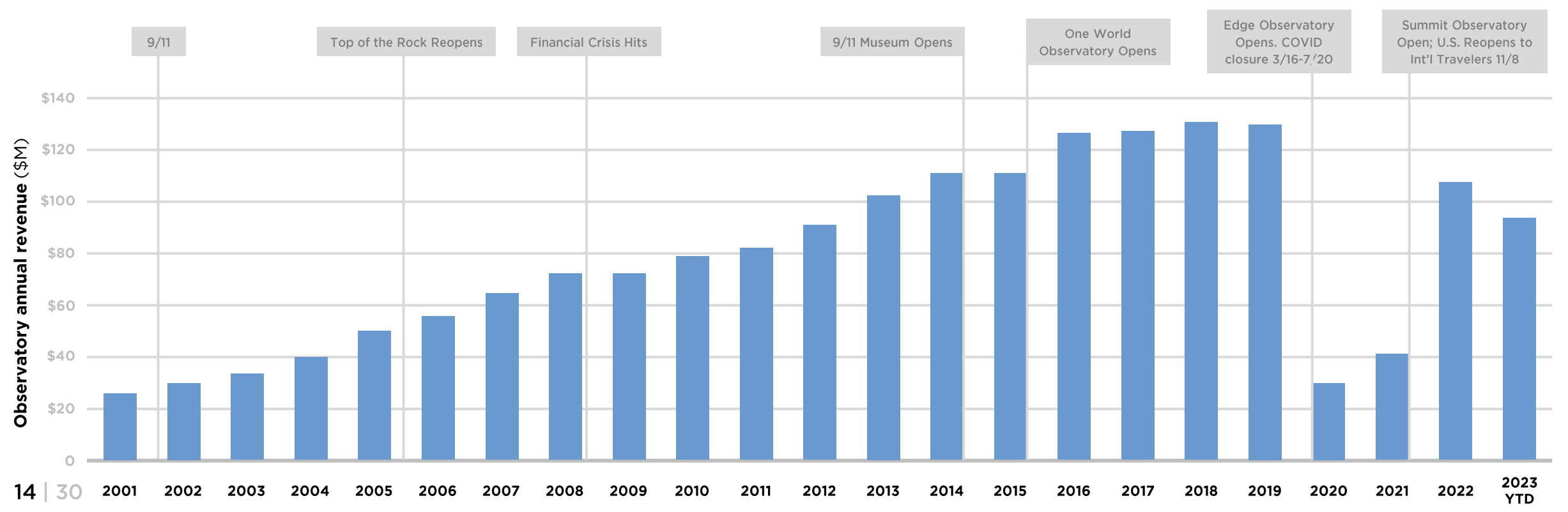

To be clear, ESRT held total cash, investments, and restricted cash of $447 million at the end of its third quarter. This is more than enough liquidity to address its maturities up until 2026. Hence, the REIT does not in the medium term face any default risk as implied by doom analysis about the trajectory of office real estate. ESRT’s portfolio is also quite diversified and at the end of the third quarter was comprised of 8.6 million square feet of Manhattan office space, another 700,000 of retail space, four multifamily properties with 727 units, and the Empire State Building Observatory encounter on the 102nd and 86th floors of New York’s most popular building.

Empire State Realty Trust 2023 October Investor Presentation

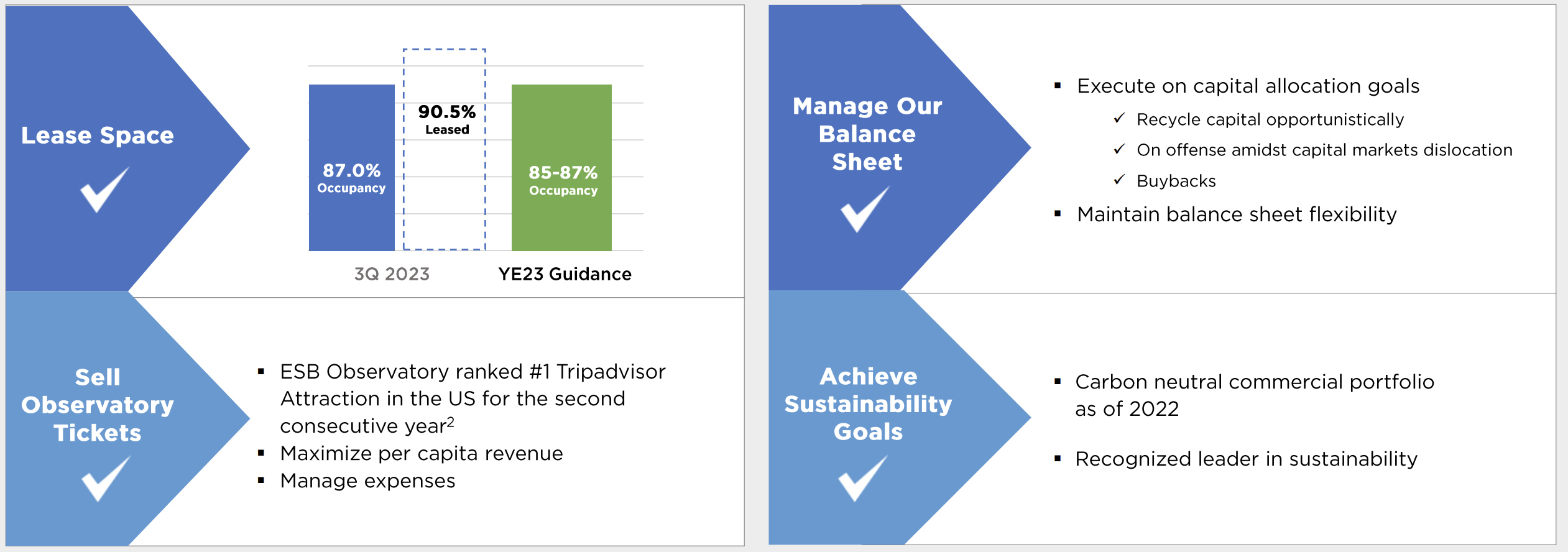

ESRT derived around 24% of its third-quarter net operating income from its Observatory with the largest share of NOI at 66% derived from its office properties. The REIT generated revenue of $191.53 million during the third quarter, up 4.3% over its year-ago comp and beating consensus estimates by $6.14 million. Third-quarter core funds from operations at $0.25 per share was up 4 cents from the year-ago period, driven by same-store property cash NOI which grew by a terrific 8.8% over its year-ago comp. advocate, the office component of the portfolio saw its leased rate finish the third quarter at 91.9%, a 30 basis points sequential boost and an even larger 250 growth from its year-ago period. The total commercial portfolio was 90.5% leased at the end of the third quarter.

Empire State Realty Trust 2023 October Investor Presentation

ESRT is targeting growing its commercial portfolio occupancy by 200 basis points by the end of 2023, up from 85% at the end of the third quarter. This is up 460 basis points since the end of 2021 with the REIT realizing 7 consecutive quarters of positive leased percentage absorption. The REIT’s 100% carbon-neutral commercial portfolio is a plus when it comes to corporates finding new office space whilst pushing to face sustainability goals. The REIT achieved an 11% positive mark to market on office leasing spreads in the third quarter, highlighting the strength of its portfolio.

Possible Dividend Hike Helps Sets Backdrop For 2024

Seeking Alpha

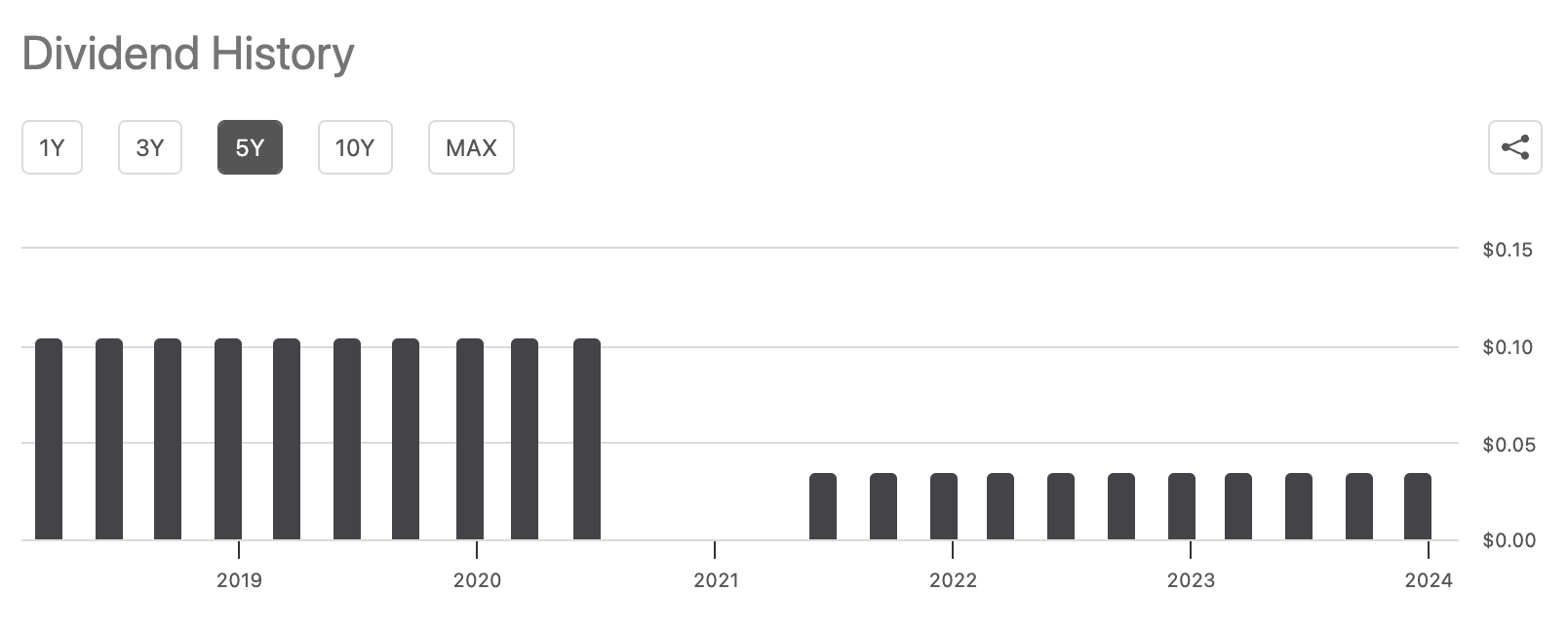

The internally managed REIT last paid out a quarterly cash dividend of $0.035 per share, unchanged from prior for what’s currently a 1.45% annualized forward dividend yield. It’s paid out 14% of its FFO for the third quarter as a dividend. Critically, the distribution still sits far below the $0.1050 per share paid out before the pandemic. ESRT was always a high-profile victim of the pandemic, but the recovery is well underway with NYC tourism numbers ticking up and well on track to outperform their pre-pandemic levels. The observatory has significant upside potential with revenue on the up. This will continue to drive FFO growth for the REIT.

Empire State Realty Trust 2023 October Investor Presentation

ESRT Is now guiding for core FFO to come in at $0.85 to $0.87 per share for the full year 2023, an boost from prior guidance of core FFO of $0.83 to $0.86 per share. Hence, we could see quite substantial dividend hikes especially as a response to Fed rate cuts delivering a pathway for cheaper debt. The REIT is a hold for 2024 with a possible dividend hike, continued NOI growth, and occupancy gains set to drive advocate shareholder value creation.

Q2 2024 Earnings Call Transcript")