fhogue/iStock Editorial via Getty Images

Electronic Arts (NASDAQ:EA) is advancing its operations through prudent integrations of AI, which its CEO describes as having the potential to increase its network by 50% and increase business efficiency by 30%. As such, this seems like a prudent time to become or to stay an EA shareholder. In addition, based on my value analysis, the company looks moderately undervalued based on my conservative model, and it has a strong capital structure compared to its peers.

Overview & Updates

Electronic Arts, also known as EA, is a leading global interactive entertainment business well known for its catalog of video games, which span console, PC, mobile and other devices. The majority of EA’s operating revenue comes from sales related to consoles. Consider the following business and geographic breakdown of operating revenue:

Segment breakdown:

- Console: 59.8% of operating revenue.

- PC and other: 23.3% of operating revenue.

- Mobile: 16.9% of operating revenue.

Geography breakdown:

- Switzerland: 55% of operating revenue.

- United States: 42% of operating revenue.

- Other: 3% of operating revenue.

EA’s most successful games include:

- FIFA Series

- The Sims Series

- Need for Speed Series

- Madden NFL Series

- Battlefield Series

Recently, Andrew Wilson, EA’s CEO, expressed his positive sentiments about the role generative AI will play in potentially making game development more efficient by 30%. Currently, game development cycles can last up to six or seven years, and AI should help to significantly shorten this by automating specific tasks. Speaking at the Morgan Stanley Technology, Media & Telecom Conference, Mr. Wilson mentioned the full effects he expects from the integration of AI into game development:

If you fast forward this over a five-year-plus time horizon, you think about where we’ve gotten to in terms of efficiency, what I would like to believe is 30% more efficient as a company, where we can attract 50% more people into our network, and hopefully by virtue of the nature of the content that we can create through generative AI, which will be created faster, and more personal to every player, then there’s 10 to 20% more monetization opportunity to us on an ARPU level. – Electronic Arts CEO Andrew Wilson

I think this is an extremely strong position for EA to be taking, considering this is a time when generative AI has the capability to make or break many companies, particularly in the field of technology. EA’s intent to aggressively adopt AI places it at the forefront of revolutionary capabilities that should drive significant benefits for shareholders in terms of income and cash flow. While its ambition to attract 50% more people into its network is ambitious, it is achievable if it drives brand awareness with surplus capital generated from lower headcount as a result of some automated development processes.

Readers will notice from the quote that higher efficiency is not all that Mr. Wilson wants to use AI for. He also plans to leverage AI for deeper personalization within games, adding new features that he believes will drive customer acquisition through better quality and fuller gaming experiences. This is a significant factor he believes will contribute to his 50% network expansion goal. Consider that in EA Sports FC 24, generative AI has increased player run cycles from 12 in FIFA 23 to 1,200, massively improving in-game details.

I’m both amused to see what EA creates and cautiously optimistic about the outcome. I believe mastering AI for creative pursuits requires a fine line drawn between heightened efficiency and careful human direction. Without the latter and too much emphasis on the former, the company runs the risk of gameplay becoming artificial, stale and lacking in spirit.

Further Key Growth Drivers & Competitive Positioning

While AI is a significant core growth driver for EA in the coming years, there are other high-value changes the firm is making to drive expansion and shareholder value. For example, it is establishing Ridgeline Games, which is a new studio led by the co-creator of Halo, Marcus Lehto. Its focus will be narrative campaigns in the Battlefield universe, and the initiative showcases the firm’s significant commitment and investment to quality in content, showing its recognition of the continued need for great human talent at the forefront of its creative strategy.

But its Battlefield universe plans do not stop there. It is also planning the coordination of multiple studios, including DICE, Ripple Effect Studios, and Industrial Toys, among others, to turn Battlefield into a higher-value first-person-shooter series.

What first comes to mind is that EA is going to compete more significantly with Microsoft (MSFT) and its Activision subsidiary who own the Call of Duty series. I believe the competition here is very high, and CoD could be an unbeatable nemesis for EA. Yet, EA’s ambition and direction seem apt to me, with unfortunately higher trends toward militarism across the world right now; one fortunate effect on gaming companies that embody army narratives is higher enthusiasm from the gaming community for their products. I have witnessed this enthusiasm firsthand from my connections to and time spent around military servicemen. Higher government spending on defense leads to higher recruitment budgets, which leads to higher enthusiasm for military careers, which in turn generates enthusiasm for war games.

In terms of investment case analysis but also operational threat, EA faces significant competition from the following companies. I have included only a few that focus solely on gaming and are of similar market cap to EA for the purposes of thorough financial peer comparison to come:

- Take-Two Interactive (TTWO): Competes with EA through blockbuster games like Grand Theft Auto, Red Dead Redemption, and NBA 2K.

- Ubisoft (OTCPK:UBSFY): Its portfolio includes Assassin’s Creed and Far Cry, competing with EA in similar genres.

- Roblox (RBLX): Offers a unique platform-centric offering, targeting a younger demographic with a competitive advantage in a stronger community-driven gaming ecosystem than EA.

Financial Considerations

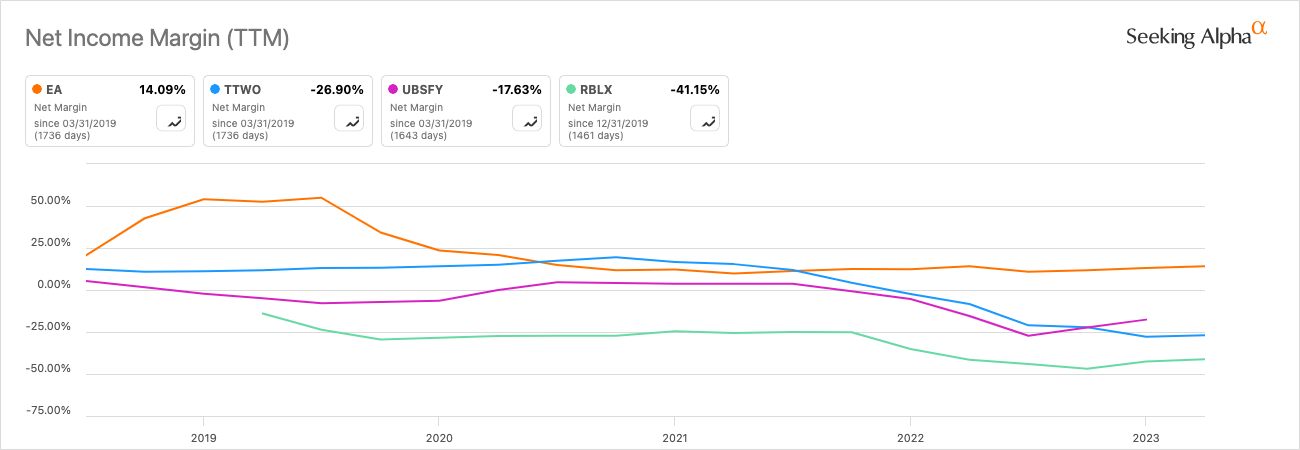

First of all, let’s look at the four peers I have outlined on specific metrics. Firstly, net income margin. Not only can we see that EA has the highest net margin of the four at the time of this writing, but it is also the only one not to be operating at a loss. Consider that in 2019, when all of the firms other than Roblox commanded a net profit, EA was still the leader. This track record is a significant strength for EA:

Author, Using Seeking Alpha

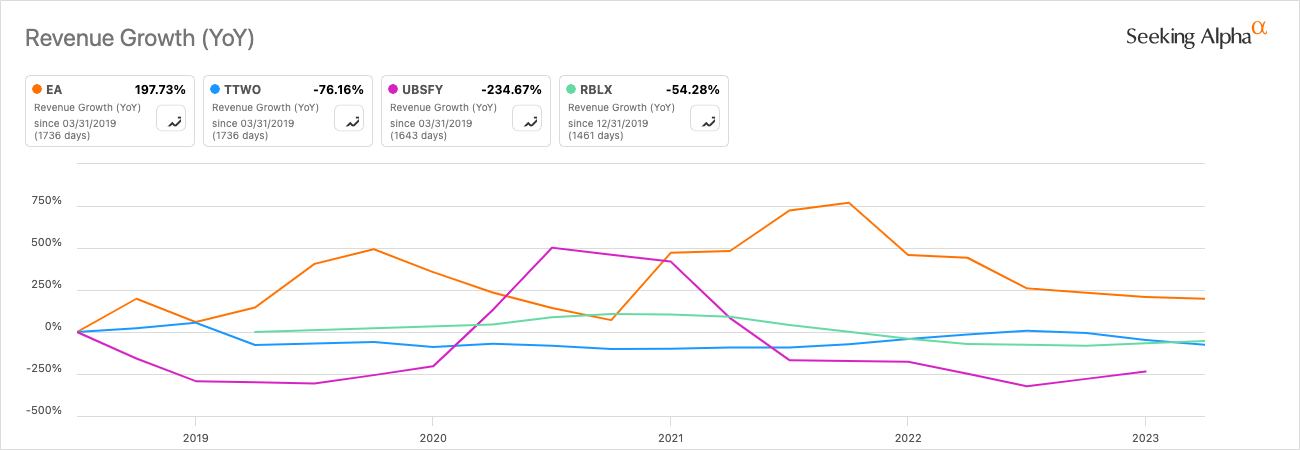

Also, consider how EA has much higher YoY revenue growth at this time compared to its peers, and once again, it has managed to command a leading position quite consistently:

Author, Using Seeking Alpha

Lastly, consider the following breakdown of each firm’s balance sheet:

| Equity-To-Asset | Cash-To-Debt | Debt-To-Equity | |

| Electronic Arts | 0.55 | 1.59 | 0.26 |

| Take-Two Interactive | 0.57 | 0.26 | 0.41 |

| Ubisoft | 0.33 | 0.53 | 1.58 |

| Roblox | 0.01 | 1.24 | 23.11 |

Notably, Roblox has considerably worse financials at this time as it is a very new company in comparison to the others, with its IPO in just 2021. Nonetheless, of its peers, EA commands what I consider to be the best balance sheet of them all, with a healthy amount of total equity compared to assets and a lot of cash on hand to pay off its moderate amount of debt. My balance sheet analysis makes EA look very good indeed against its peers.

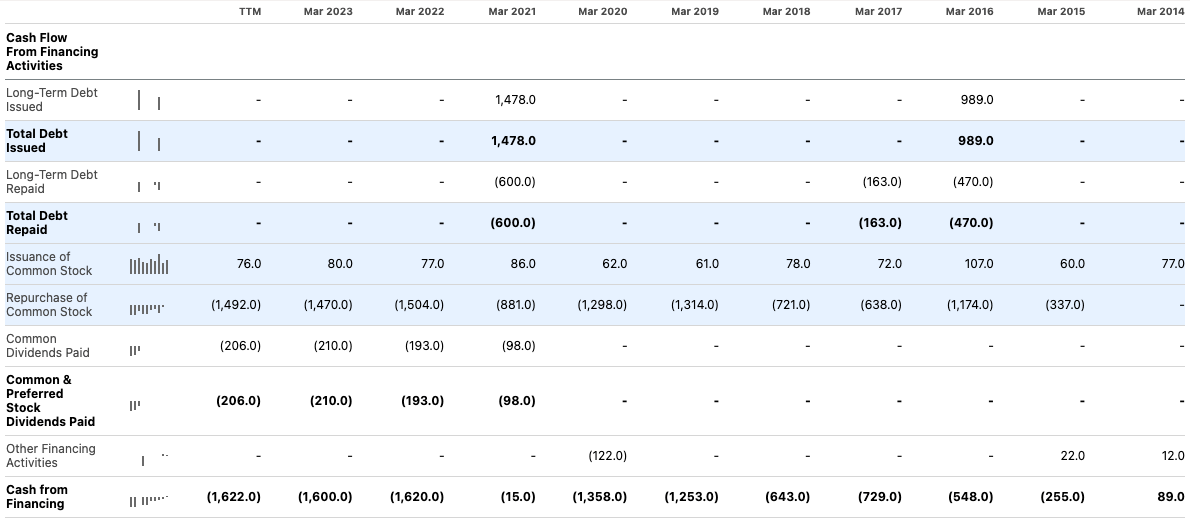

EA’s cash flow statement also shows further strength. Specifically, it does not issue debt frequently, with only two issuances over the past decade, and while its repayments are also infrequent, they are sufficient given its equity-to-asset ratio of 0.55. Its high repurchase of common stock every year is also warranted by the well-managed balance sheet, and this is significantly increasing shareholder value. It does issue common stock almost every year on record but at a minuscule proportion to the amount it repurchases. I like the financial management of the company a lot, and I think it shows a prudent awareness of the need to not be overleveraged whilst also highly valuing shareholder interests. While not perfect, its capital structure is hard to find significant fault in.

Seeking Alpha

Valuation

EA is currently selling at a GAAP price-to-earnings ratio of 33.5, which is very close to its five-year average of 34. Yet, its forward price-to-earnings ratio of 28.81 is a -17.78 % difference from its five-year average of 35. As such, I believe there is a compelling opportunity here in terms of the stock valuation to buy good growth at a reasonable price.

The significant potential discount of around 18% is aided by 10.5% EPS growth expected on consensus for fiscal 2024, 6.6% expected for fiscal 2025, and 11.69% expected for fiscal 2026.

As the company typically trades at around a 50% premium to the industry median P/E ratio, I have discounted this from the indicated 18% margin of safety based on EA’s historical forward price-to-earnings ratios versus its present forward price-to-earnings ratio. Therefore, my estimated margin of safety for the stock at this time is 9%.

Readers should bear in mind that I have not included a P/E comparison to my group of peers as they are all trading at a loss at this time other than EA, so it would not be meaningful.

Risks

While I have attempted to add a layer of conservatism to my value analysis by integrating a discount based on the difference in the value of EA to the entire industry, there is some doubt that this is enough of a security measure to guard against not performing a discounted cash flow analysis. However, multiple analysis becomes one of the only ways to properly gauge a fair stock price when high levels of investor sentiment are present, as forecasted earnings unfortunately do not capture this. Nonetheless, if investor sentiment changes, even if the fundamentals are strong, the stock could see a significant drop in price.

Additionally, there is an opportunity in this new age of artificial intelligence for disruptive new game studios to transform what is popular in the industry, and I believe EA will face significant competition in new technologies, consoles and platforms that could reduce its market share unless it makes careful acquisitions, strategy pivots and hires the right people to remain relevant. It is taking all of the correct steps with its aggressive integration of AI at this time, but as immersive content becomes more available and user-friendly, EA might find it is out of its depths with its current infrastructure.

Closing Thoughts

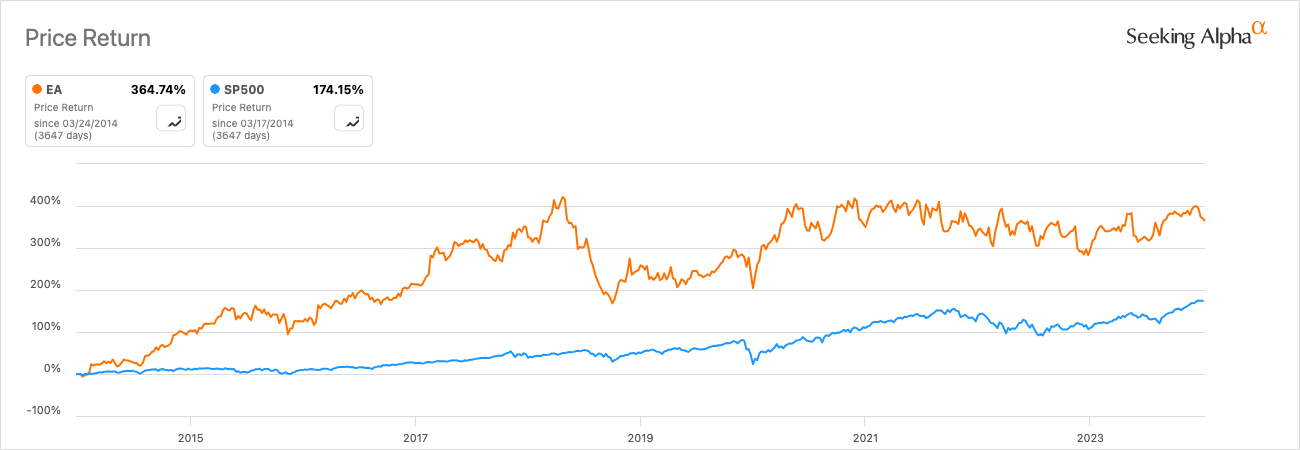

Overall, EA stock is a Buy based on my analysis. I consider it to be extremely well-positioned in the industry, with prudent future operational strategies and very well-managed financials. I would be surprised if it doesn’t outperform the S&P 500 (SP500) over the next 10 years, and based on its integration of AI for efficiency and customer acquisition, its returns could be higher than in the past decade.

Seeking Alpha

Q2 2024 Earnings Call Transcript")