metamorworks/iStock via Getty Images

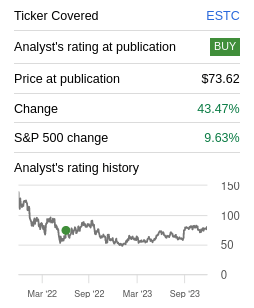

We first wrote about Elastic (NYSE:ESTC) a little over a year ago, rating it a ‘Buy’ based on its strong competitive moat derived from its network effects resulting from its open source model and from high customer switching costs. Not everything was perfect, though, as growth had slowed and there were high levels of stock-based compensation. The company just announced excellent Q2 2024 results, which made the shares soar past $100, meaning that it has more than quadrupled the performance of the market since we published our Elastic article. Given the change in share price, and the recent results, we’ll scrutinize the company to execute if a change in rating is warranted.

SeekingAlpha

Q2 2024 Results

Second quarter 2024 results were encouraging, with revenue growing 17% year over year, and Elastic Cloud growing particularly fast with 31% year over year growth. The company attributed growth in Cloud to improvement in cloud consumption as well as some impact from its success in generative AI. Elastic believes that explore is a critical part of the infrastructure for AI, and that they stand to benefit from this important trend. Still, the company admits it will take some time for generative AI spend to become a significant driver of its revenue, and they see it mostly as an exciting long-term opportunity.

Elastic reported a record non-GAAP operating margin of 13% for the quarter, and diluted earnings per share of $0.37. It is important to recollect that these numbers are non-GAAP, and that the company remains loss-making using GAAP accounting. Subscription as a percentage of total revenue was roughly 93%.

The company shared a lot of excitement around AI applications, including high expectations for its Elasticsearch Relevance Engine, or ESRE, to build generative AI applications. There were also several important wins in the quarter where they displaced competitors. For example, Elastic shared that they signed a multiyear marketplace deal with DocuSign (DOCU), and they closed a multiyear 8-figure deal with a leading global wealth management company.

Elastic Investor Presentation

Financials

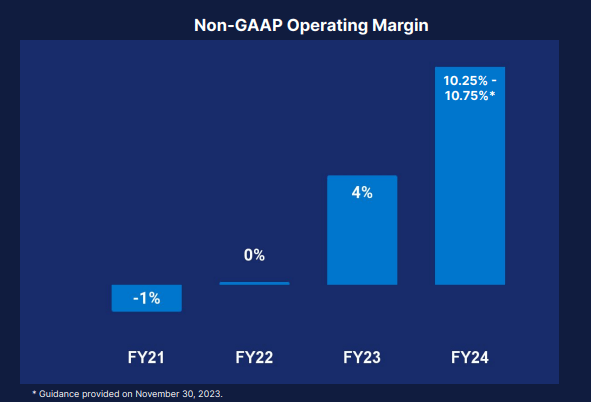

We believe part of the excitement, and why shares are up more than 30% today, is that the company is forecasting significant profitability improvement for FY2024. As can be seen in the graph below, guidance is for the Non-GAAP operating margin to be around 10% for fiscal year 2024.

Elastic Investor Presentation

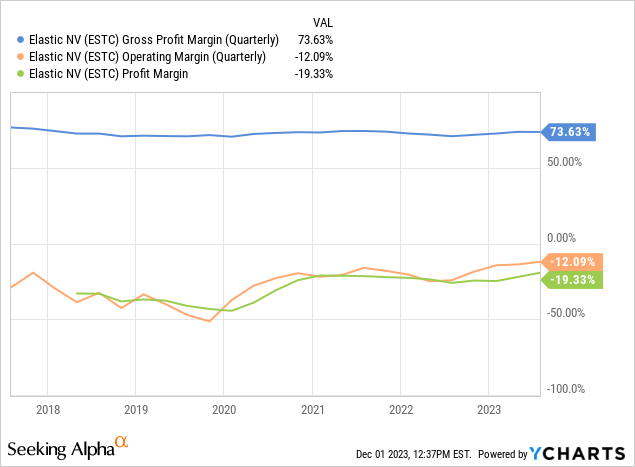

The profitability improvement is definitely good news, but we would appreciate to caution readers that things do not look as rosy when using GAAP accounting. This can be seen in the graph below, and while Elastic has a wonderful gross operating margin, it has yet to accomplish GAAP profitability. As we’ll see below, one key reason is the significant amount of stock based compensation the company uses.

Growth

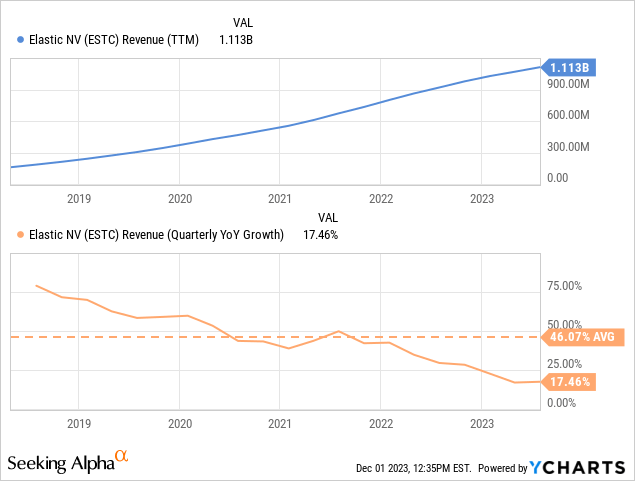

Elastic has several different growth vectors, which include new customer acquisition, customer data growth, customers adopting more of Elastic’s solutions, customers moving to the cloud and adopting higher subscription tiers, and customers adopting more use cases. Elastic has been working on all these fronts, which has resulted in significant revenue growth, surpassing $1 billion in trailing twelve months revenue. Unfortunately, revenue growth has been quickly decelerating, although it would appear many investors believe that the generative AI tailwind will start to reverse this trend.

Competitive Moat

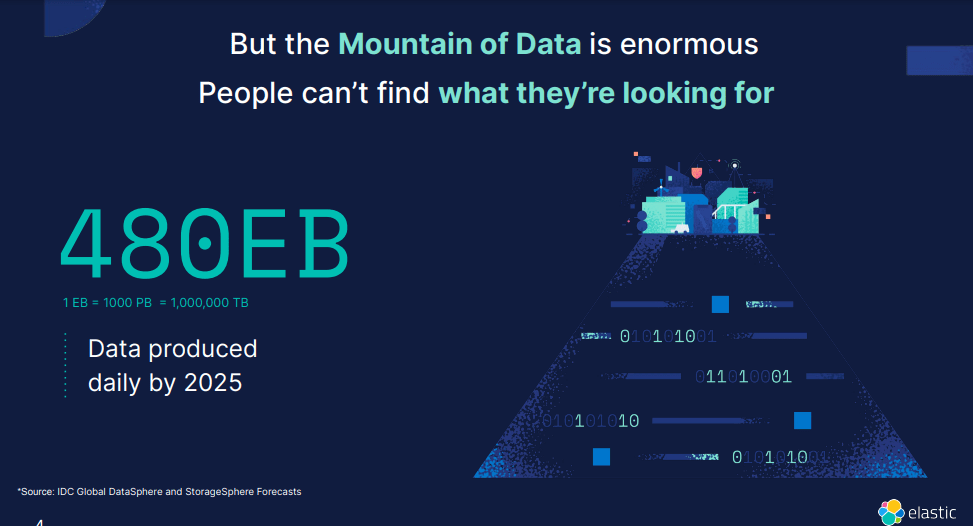

We believe Elastic does have a strong competitive moat, mostly derived from high customer switching costs. Once customers spend the time to incorporate Elastic, they will be very reluctant to spend the time and effort, plus the operational risk, to migrate to an alternative. It also benefits from scale, as lessons learned from working with one customer can then be used to encourage better its algorithms in the next version. The way Elastic likes to phrase this is “Elastic enables everyone to find the answers that matter. From all data. In real time. At scale”. In any case, it is true that the amount of data that is being generated, and which has to be searched, is constantly increasing and reaching impressive numbers. This means that explore solutions have to be really efficient, making it increasingly difficult for companies to build their own in-house explore technology.

Elastic Investor Presentation

Even Booking (BKNG) with all its resources seems to prefer using an external solution, instead of building one internally. Elastic mentioned them as one of their customers, helping them handle the roughly 100 terabytes of data per day they ingest to maintain customers. Another example of a customer shared was BMW (OTCPK:BMWYY), which has the challenge of allowing customers to explore for a huge number of different car configuration options. To encourage better their moat, Elastic recently bought a small company called Opster, which develops products for monitoring, managing and troubleshooting Elasticsearch and OpenSearch. They are the creators of AutoOps, a powerful platform that provides deep insight to detect and resolve issues with cluster health, improved explore performance and reduce hardware costs. Elastic believes this acquisition will help them in their road towards complete server-less offerings, and that it will make their platform even more resilient and easier to use.

The AI tailwind

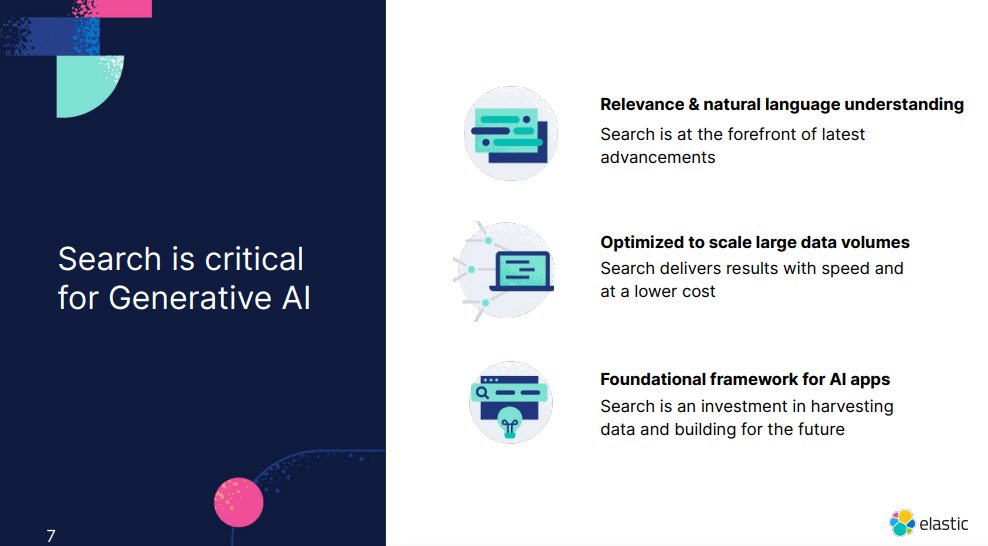

A lot of the current excitement comes from expectations that generative AI will be a significant contributor to Elastic’s growth. Elastic for its part maintains that explore is a critical component in the generative AI value chain, and its solutions give developers a powerful set of machine learning tools to build AI-powered explore applications that incorporate with large language models.

Elastic Investor Presentation

There is another benefit to Elastic from generative AI, and that is making its products easier to use. A good example is the chat capabilities with SQL integration using their AI Assistant. This allows customers to use natural language to explain a query and have the AI Assistant supply the query syntax, explain what the query does, and supply a prompt to run the requested query.

Elastic Investor Presentation

Stock-based Compensation

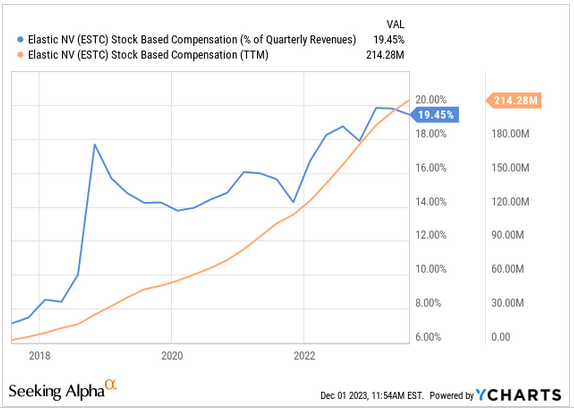

While we are big fans of Elastic’s technology and business model, we are disappointed with its lack of discipline regarding stock-based compensation. It has been growing much faster than revenues, and it has now reached roughly 20% of trailing twelve months revenues.

YCharts

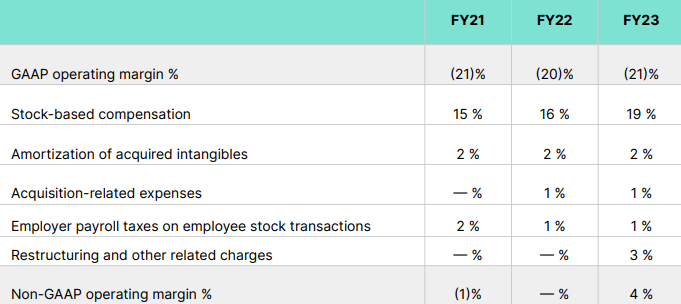

This is one of the main reasons the company remains unprofitable using GAAP accounting. This is clear when looking at the GAAP to Non-GAAP reconciliations for its operating margin.

Elastic Investor Presentation

Balance Sheet

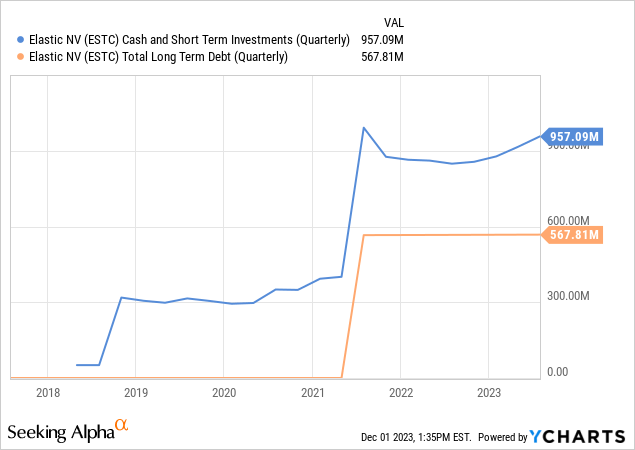

Elastic reported ending the quarter with cash, cash equivalents, and marketable securities of $966 million, and long-term debt of $568 million. This means the balance sheet remains quite solid, and showed little change compared to the previous quarter.

Outlook

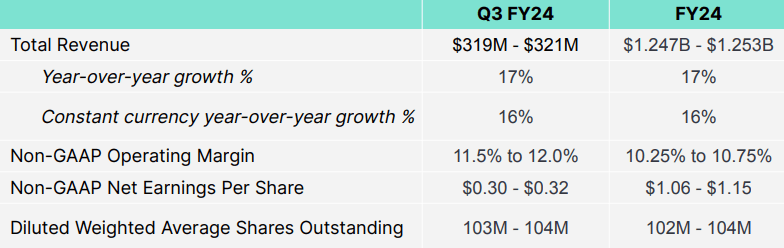

Elastic raised its FY2024 outlook, now expecting revenue in the range of $1.247 billion to $1.253 billion, this would represent 17% y/y growth. It expects non-GAAP operating margin in the range of 10.25% to 10.75% and non-GAAP earnings per share in the range of $1.06 to $1.15.

While this seems to mark an inflection point for the company, it is still too early to be convinced that the deceleration the company had been seeing to its growth is over, and it remains to be seen how much of a real impact generative AI will have on its future growth.

Elastic Investor Presentation

Valuation

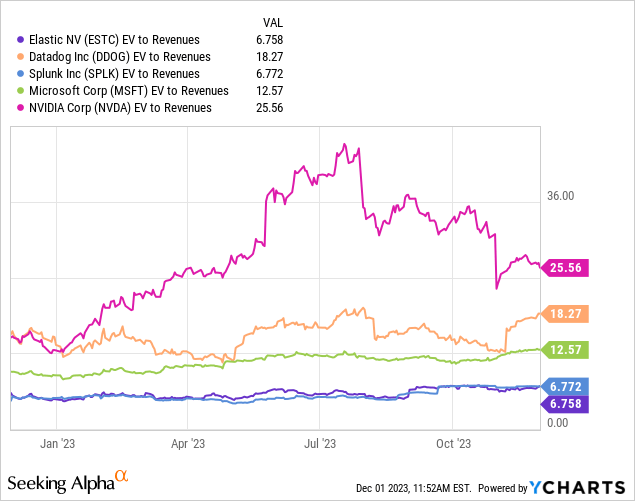

While we are optimistic that Elastic will indeed encounter tailwinds from the generative AI trend, we believe shares to be expensive. Perhaps not as expensive as other AI companies, but we are reluctant to pay an almost 7x EV/Revenues multiple for the shares.

Still, shares do not look that expensive on a relative basis compared to competitors such as Data Dog (DDOG), or Splunk (SPLK) which received an acquisition offer. Elastic even looks cheap compared to Microsoft (MSFT) or NVIDIA (NVDA), but we do believe the AI sector to be quite overvalued at the moment.

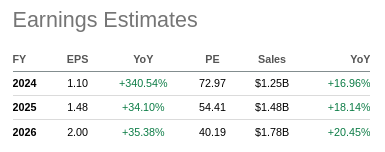

Analysts expect earnings per share to grow significantly for Elastic in the coming years, but these are non-GAAP estimates, and even looking as far out as FY26, the forward P/E multiple remains a pricey ~40x.

SeekingAlpha

Risks

We believe the biggest risk for investors in Elastic is that the share price reflects high growth expectations. Growth had been decelerating for several quarters, but it appears investors now believe the company has reached an inflection point. In particular, there are high hopes that generative AI will re-speed up revenue growth.

Earlier this year the company disappointed investors when it said it would extend its $2 billion revenue target timeline, giving difficult macro conditions as one of the reasons. One analyst asked during the Q&A session of the earnings call whether the generative AI tailwind would mean that the timeline could be moved forward again. CFO Janesh Moorjani gave what sounds appreciate an optimistic reply, but without committing to bring the target forward.

So, you know, we were through that $2 billion goal sometime back, but the way we think about this fundamentally is that we’ve got a significant opportunity ahead of us, and we are working hard to prosecute that opportunity. You’ve seen tremendous momentum here from the standpoint of the overall business, and particularly in terms of cloud growth as we address that opportunity. And all of that is additionally fueled by the momentum that we are seeing in generative AI.

So, we don’t want to get too far ahead and start to anticipate future revenue growth beyond this year at this stage. But there’s no question in our minds that we are working hard to build a multi-billion dollar Company at scale in the future. And we’ll supply you with appropriate updates as we go on that. But for now, we are focused on executing in this year and feel very good about the back half of the year.

Conclusion

There were several positives in Elastic’s Q2 2024 results, and investors appear particularly excited about the generative AI possibilities and the potential for an increased target addressable market in the long-term. Still, the company reminded investors that customers remain cost conscious, and that the generative AI impact is still not very significant, even if it makes the future look more promising. We continue to believe Elastic has a very unique technology and competitive moat, and do believe some benefits from generative AI will materialize in the future. Unfortunately the company has a huge stock-based compensation expense, making it unprofitable on a GAAP basis. Given this, we no longer find the shares particularly attractive and are therefore downgrading them to ‘Hold’. However, we remain optimistic about a potential growth inflection and believe that they are less overvalued compared to many other AI companies.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")