Joe Hendrickson/iStock Editorial via Getty Images

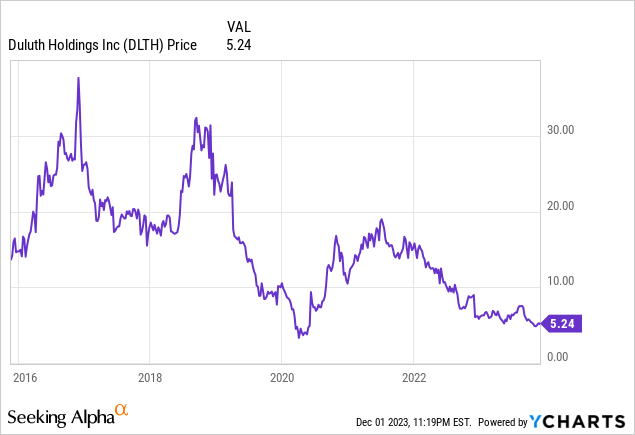

Duluth Holdings Inc. (NASDAQ:DLTH) has struggled through a challenging macro environment in recent years amid declining sales and poor earnings. The apparel retailer just reported its latest quarterly result, which missed estimates while management offered soft guidance. The setup here doesn’t look good with the stock down more than 40% over the past year.

That being said, the company has a turnaround scheme and we can point to some areas of strength within its brand portfolio. We believe 2024 will be critical for the company to verify it can stabilize sales and drive an earnings rebound to maintain a more sustained rally in the stock.

DLTH Earnings Recap

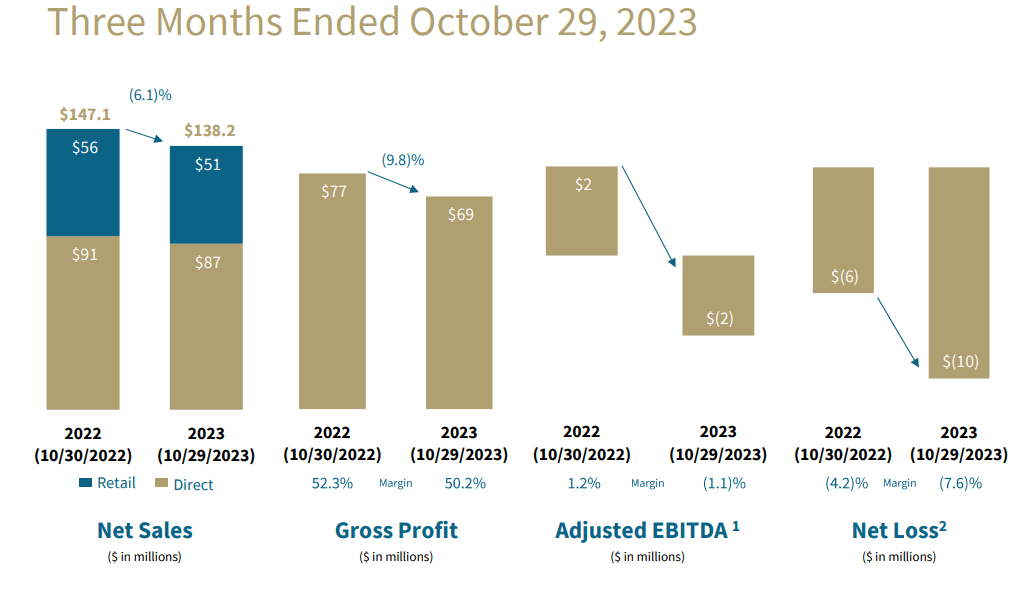

DLTH reported a Q3 EPS loss of -$0.32, $0.08 below estimates, and down from the -$0.19 loss in Q3 2022. Revenue of $138 million was down by 6.1% y/y, also coming in under expectations.

The weakness here was across the board with the direct-to-consumer sales of $87.0 million down by -4.4%, with management citing a reject in site visits. Similarly, foot traffic was slower across the company’s 62 retail locations where sales declined by -8.8% to $51.2 million.

We mentioned a silver lining, in this case, the company has found success with its Women’s “AKHG” sub-brand with sales increasing by 19% from the period last year. Duluth has also made progress in adjusting its inventory levels, down by 15%, although this has been achieved through discounting which was reflected in a lower gross margin.

Even as SG&A declined by -2.9% y/y through some corporate efficiency efforts, this was still not enough to balance the weaker top line. The adjusted EBITDA at -$1.6 million reversed a positive $1.7 million in Q3 2022.

source: company IR

In terms of guidance, management expects full-year 2023 net sales of between $640 and $655 million. Notably, this was revised lower compared to the prior target between $645 and $660 million announced with the Q2 results. If confirmed, the trend represents a reject of around 2% from 2022.

The full-year adjusted EBITDA target between $35 and $39 million is down from the prior $41 million midpoint calculate. On a GAAP basis, an EPS loss between -$0.25 and -$0.15, reverses a profit of $0.07 reached last year.

During the earnings conference call, management attempted to project some confidence by focusing on an improving sales mix that is expected to maintain margins into the spring season while noting that inventory levels are now healthy. The early read into Q4 is that trends during the Black Friday shopping week were “solid”.

Finally, we can cite that the company ended the quarter with $8.2 million in cash against $36.2 million in long-term debt. Considering the adjusted EBITDA trajectory, a net leverage ratio under 1x suggests the balance sheet is stable.

What’s Next For DLTH?

It’s clear that the trends are not moving in the right direction, and there are plenty of reasons to be skeptical of any turnaround opportunity. Duluth has disappointed investors going back to a period even before the pandemic and there is some concern that the brand momentum is missing.

Ideally, we want to see a scenario where growth re-accelerates with a path for earnings to trend higher. Whether or not that’s possible will start with the ability of management to execute its “Big Dam Blueprint” growth strategies. The idea here is for the company to kickstart some operational momentum by focusing on its strengths by targeting value-added opportunities.

Duluth wants to push its accomplish across digital while optimizing its retail footprint with advocate efficiency efforts. On that point, a recent development has been the rollout of a new automated fulfillment center expected to improve order processing and inventory management. Ultimately, the scheme is to deliver sustainable growth and profitability.

source: company IR

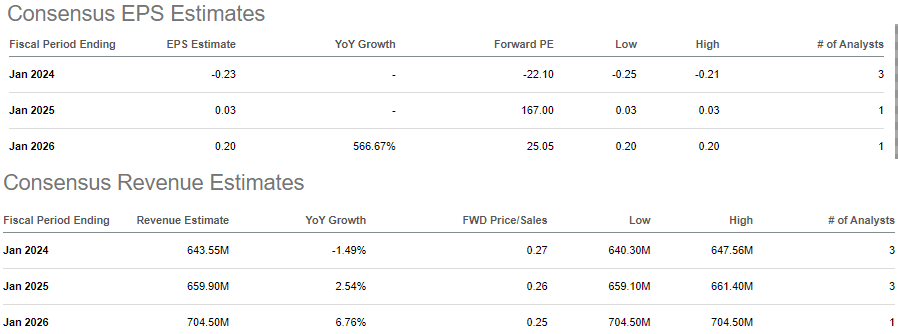

According to consensus estimates, Duluth sales are seen rebounding through 2024 while the company reclaims profitability next year towards an EPS of $0.03. Again, we can take these estimates with a grain of salt and recognize the significant uncertainty. The first step will be for sales to stop declining while a 2024 guidance update expected with the next quarterly results will be important to set the stage for the year ahead.

Seeking Alpha

The other issue comes down to valuation. Taking the management guidance for the current year adjusted EBITDA of around $37 million, DLTH is trading at an EV to forward EBITDA multiple of approximately 11x.

While this level is not necessarily “expensive”, the ratio is at a premium to the broader apparel retailer industry. The problem is that a few more quarters of disappointing results could open the door for a larger repricing lower and selloff in the stock.

Seeking Alpha

Final Thoughts

We rate DLTH as a hold, giving the company the benefit of the doubt that the worst is over and the turnaround strategy can work. It’s fair to assume the weakness in shares over the past year has already incorporated many of the weak points with the outlook.

The bullish case for DLTH is that results going forward outperform expectations with the possibility of the company benefiting from an improving macro environment.

On the other hand, the risk that a sales rebound fails to materialize would likely force a more extensive restructuring effort that would impair the earnings outlook. Without a clear improvement in financial conditions, we expect shares to remain volatile.

Q2 2024 Earnings Call Transcript")