Monty Rakusen

By Andrew Prochnow

Since hitting a low point in mid-December, crude oil prices have surged by approximately 15% over the past eight weeks, reaching a recent peak of around $78 per barrel.

Throughout the last quarter of 2023, oil prices faced downward pressure amid worsening outlooks for the global economy. However, the recent uptick indicates a potential shift in sentiment among market participants, hinting at a reassessment of the likelihood of a global economic resurgence in the second or third quarter of 2024.

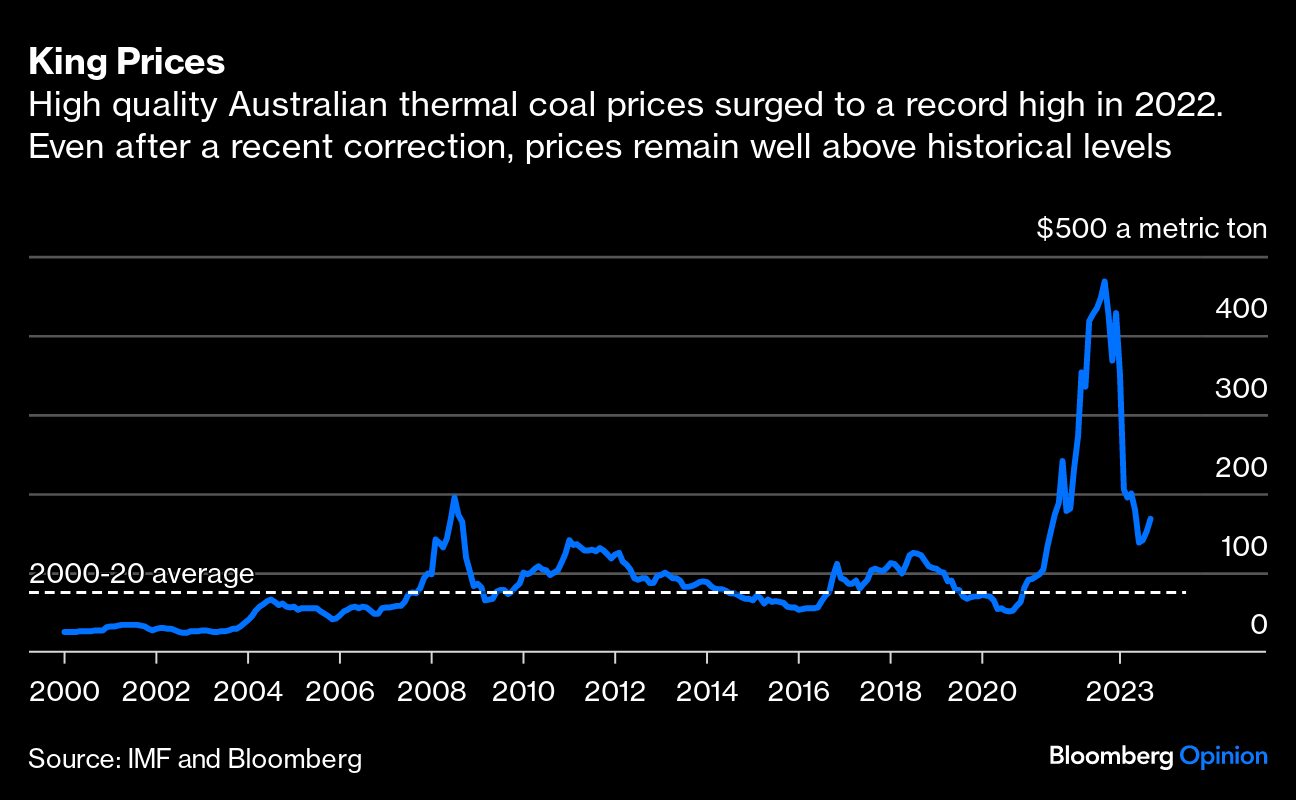

If the rally in oil continues, one of the big beneficiaries could be the coal market. Newcastle coal futures (an industry benchmark) have corrected by about 70% since peaking above $400/ton in September of 2022. And as of early February, they have settled all the way down at around $120/ton.

Bloomberg

Similar to crude oil, coal prices are highly sensitive to prevailing economic conditions, as demand in the coal market tends to fluctuate with the strength or weakness of the underlying economy. Like other commodity markets, coal prices are also greatly influenced by supply-side factors.

When coal supplies are scarce and demand is on the rise, prices typically trend upward. Conversely, in periods of ample supply and declining demand, prices tend to decrease. However, the current market environment introduces additional factors to consider.

Presently, global coal inventories are relatively abundant. Last year, global coal production reached a record high of around 8.7 billion metric tons, marking a 2% increase from 2022.

Despite the ample coal supply, it’s worth noting that prices have been on a downward trajectory for approximately 17 months, plummeting to roughly 70% lower than their peak in September 2022. Given this prolonged decline, a sudden surge in demand could potentially serve as a catalyst for price reversal.

Coal-fired energy is predominantly used for electricity generation worldwide. Therefore, if economic growth surpasses expectations in 2024, an increase in demand could trigger a substantial turnaround in coal prices, akin to what was witnessed in the iron ore market during the last quarter of 2023.

Current Dynamic in the International Coal Market

When it comes to demand in the international markets, China and India are two of the world’s largest importers of coal. That’s not necessarily surprising, given that these two countries are the most highly populated of any on earth, and also constitute a couple of the world’s largest economies.

In absolute terms, China has long been the world’s number one importer of coal. But over the last couple of years, India’s economy has been growing at a faster pace than China’s. During 2022 and 2023, India’s GDP grew by about 7% annually.

And much like China, India relies heavily on coal to power their electric grid. According to The Times of India, coal-fired power accounts for roughly 70% of India’s total electricity on an annual basis. That means if India’s economy continues to grow at a rapid pace in 2024, additional coal imports will likely be required.

Corroborating that outlook, the International Energy Agency [IEA] recently stated that increased coal demand from India will be the primary driver of growth in this sector for the next several years.

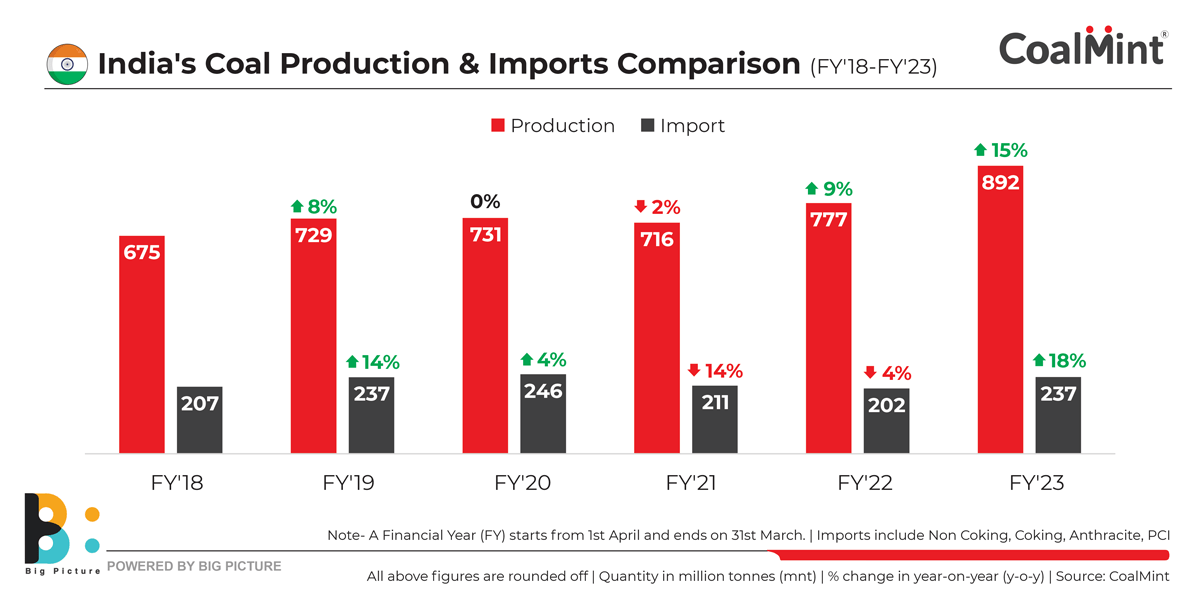

To satisfy this level of demand, India has been producing more coal domestically, and importing more from abroad. As highlighted in the graphic below, India’s coal imports rose by 18% in 2023 as compared to the year prior.

CoalMint

The aforementioned data indicates that continuing strength in the Indian economy will be a lynchpin for the global coal market in 2024. But what about China?

As most investors and traders are well aware, the Chinese economy (and stock market) have been under pressure since early 2021 (when the stock market selloff first started). And based on recent data, China’s economy continues to be mired in the doldrums.

In the last quarter of 2023, the Chinese economy grew by 5.2%, which was below expectations—and also well below India’s current pace of growth.

But what if China’s economy were to bounce back in Q2 or Q3 of 2024? If that comes to pass, the bull case for coal prices gets even stronger. Along those lines, a general uptick in global economic activity would also suffice to help push coal prices higher, even if the Chinese economy continues to move sideways.

Key Investment/Trading Takeaways

Based on the aforementioned information and data, investors and traders bullish on the Indian and Chinese economies—or the broader global economy—might consider a long position in the coal market at this time. On the other hand, market participants that think the global economy will continue to slow in 2024, may want to hold off before initiating a new position in the energy sector.

Prior to the pandemic, thermal coal prices were trading between $60-$70/ton. That means if the current selloff continues, coal prices could drop further. However, with India’s economy still humming, and the summer season approaching, that seems fairly unlikely.

According to India’s Central Electricity Authority (ICEA), electricity demand in the country tends to peak during the summer months, particularly in May and June, when temperatures soar to their highest levels. Power utilities and grid operators must therefore anticipate and manage this seasonal spike in demand to ensure the reliability and stability of the electricity supply.

Similar to India, electricity demand in China also tends to increase during the summer months due to increased usage of cooling systems, particularly air conditioners. China, with its vast territory and diverse climatic zones, faces varying levels of temperature extremes during the summer season, with some areas experiencing sweltering heat.

Taken all together, this information suggests that the recent slide in coal prices may represent an opportunity for those that are bullish on a potential economic rebound in 2024, especially with the hot summers in India and China drawing closer on the calendar.

To track and trade the coal sector, readers can add the following names to their watchlists:

-

Alliance Resource Partners (ARLP)

-

Alpha Metallurgical Resources (AMR)

-

Arch Resources (ARCH)

-

BHP Group (BHP)

-

Consol Energy (CEIX)

-

CNX Resources (CNX)

-

Hallador Energy (HNRG)

-

NACCO Industries (NC)

-

Natural Resource Partners (NRP)

-

Peabody Energy (BTU)

-

Ramaco Resources (METC)

-

SunCoke Energy (SXC)

-

Teck Resources (TECK)

-

Warrior Met Coal (HCC)

Andrew Prochnow has more than 15 years of experience trading the global financial markets, including 10 years as a professional options trader. Andrew is a frequent contributor Luckbox magazine.

Q2 2024 Earnings Call Transcript")