ADragan/iStock via Getty Images

Introduction

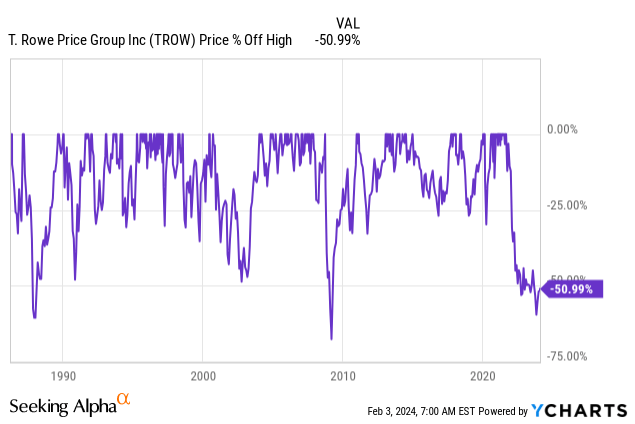

It’s time to talk about a company I have never discussed before. That company is the T. Rowe Price Group (NASDAQ:TROW), one of the world’s largest asset managers and a company whose stock price has lost roughly half of its value from its prior peak, as we’ll discuss in the valuation part of this article.

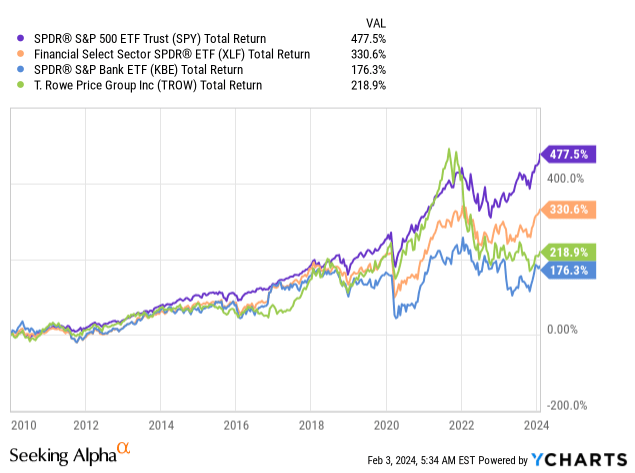

When it comes to stocks in the financial sector, I prefer to invest in service-based companies over banks, which account for roughly a quarter of the sector’s exposure – using State Street’s (XLF) ETF as a benchmark.

Although I have nothing against banks, I, generally speaking, dislike their risk/reward due to often low-moat business models and severe sell-offs during recessions.

Since January 2010, the S&P 500 has returned 478%, beating the 176% return of the SPDR S&P Bank ETF (KBE) by a huge margin. Financial stocks returned 330%. TROW returned just 219%, which is mainly the result of poor performance over the past two years.

Since 2003, TROW shares have returned more than 12% per year despite the post-pandemic share price decline.

With close to 40 consecutive annual dividend hikes, the Dividend Aristocrat now yields 4.5% and has a highly favorable valuation.

So, let’s get to it!

Making Money From Other People’s Assets

In my dividend growth portfolio, I currently own one financial stock – CME Group (CME). CME owns some of the nation’s largest exchanges, covering NYMEX, CBOT, and others. It makes money whenever people trade futures like S&P 500 e-minis, corn, gold, WTI crude oil, and so much more.

In financial services, I want to own companies that make money on very “basic” operations, including trading, investing, and other things.

That’s where T. Rowe Price comes in.

Established in 1937 by Thomas Rowe Price, Jr., the company has evolved into a financial services powerhouse, offering a wide range of U.S. mutual funds, sub-advised funds, and separately managed accounts.

The company’s expertise extends to collective investment trusts, catering to the unique needs of a diverse client base that includes institutional investors, financial intermediaries, and individual investors worldwide.

While I would make the case that TROW operates in an industry with somewhat low entry barriers, the company has excellent connections that are hard to replicate and can be seen as a vehicle that grows when investment volumes grow.

Furthermore, in 2021, the company bought Oak Hill Advisors, which gave the company access to alternative credit management.

On October 2, 2023, the company announced the launch of a private credit fund for income-oriented investors.

T. Rowe Price Group

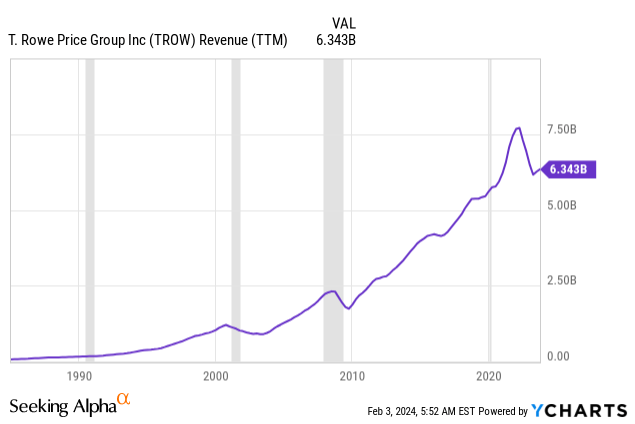

As we can see below, it’s fair to say that the company grows with the economy. The only thing that has briefly interrupted its growth in the past three decades is recessionary pressures in the early 2000s, the Great Financial Crisis, and some periods with subdued growth and stock market headwinds (like 2014-2015).

Essentially, consistent growth has allowed the company to become a go-to place for income growth.

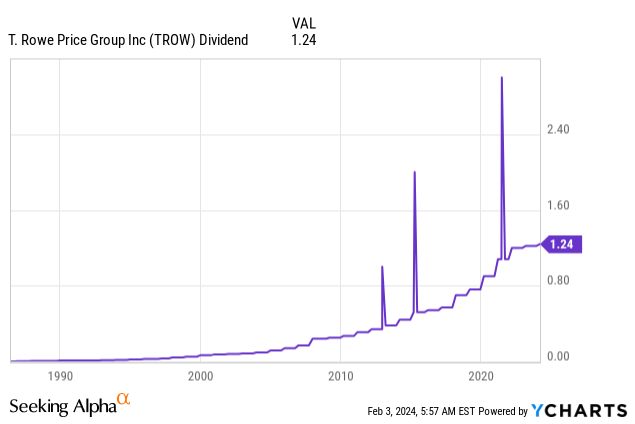

After hiking its dividend by 1.6% on January 30, it now pays $1.24 per share per quarter, which translates to a yield of 4.5%.

This makes TROW a high-yield stock.

Moreover, although its most recent dividend hike may have been a bit underwhelming, its five-year dividend CAGR is 11.8%!

Adding to that, the company has a history of 37 consecutive dividend hikes, making it a Dividend Aristocrat.

Its dividend is protected by $7.44 in 2024E EPS, which translates to a payout ratio of roughly 67%.

With that in mind, as we can see in the revenue chart below, the company’s stock price weakness comes with poorer financial results.

After all, in 2021, the company’s stock traded north of $220. It currently trades at $110, which is 50% lower…

Where’s The Value In TROW?

In its most recent quarter, 3Q23, the company reported adjusted earnings per share of $2.17, which is way up from the previous quarter’s $2.02 result.

This was mainly driven by elevated investment advisory revenues and higher income from carried interest.

Despite a decline in end-of-period AUM (assets under management) to $1.35 trillion, down 3.8% from the previous quarter due to market fluctuations, the average AUM for Q3 stood at $1.4 trillion. This average marked a 2.7% increase from Q2 and a notable 3.4% rise from the prior year quarter.

Using the overview below, we see that during the pandemic, the company’s AUM exploded, which was a result of excess savings, low rates, subdued inflation, and a general surge in people’s desire to make money on the stock market.

Between 2019 and 2021, AUM surged by more than $480 billion!

T. Rowe Price Group

Since then, AUM has normalized again, which is reflected in its stock price.

Furthermore, net flows for Q3 were characterized by $17.4 billion in outflows, largely attributed to three U.S. large-cap growth equity strategies.

T. Rowe Price Group

However, multi-asset fixed income and alternative asset classes experienced inflows, mitigating the impact of outflows.

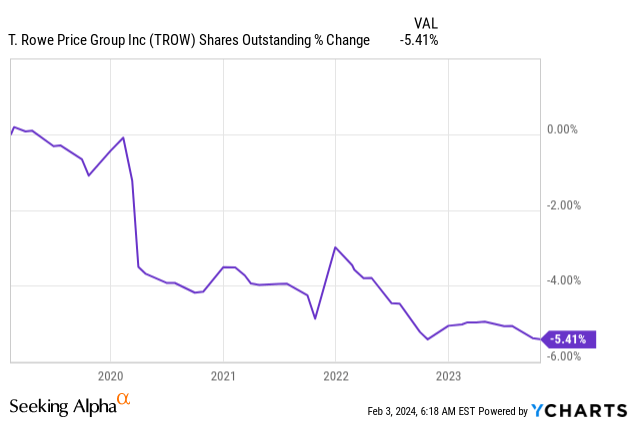

With that said, before we spend too much time discussing old financial data, the company repurchased over 977,000 shares at an average price of about $108 in 3Q23, totaling $106 million.

3Q23 year-to-date share repurchases amounted to just over 1.4 million shares, totaling slightly over $150 million.

As TROW is a >$24 billion business, it is no surprise that buybacks do not have a major impact.

Over the past five years, the company bought back 5.4% of its shares. That’s not bad, but it’s not anywhere close to what buyback-focused companies have achieved during this period.

Hence, during its earnings call, the company noted that it remains committed to a recurring dividend, with approximately $992 million returned to stockholders through buybacks and dividends year-to-date.

As we can see below, dividends have always been the company’s top priority, and I have little doubt that it will remain that way.

T. Rowe Price Group

With that in mind, analysts are very upbeat about the company, which makes for a great valuation in light of the poor stock price performance in recent years.

Using the data in the chart below:

- TROW currently trades at a blended P/E ratio of just 14.9x, which is well below its long-term normalized P/E ratio of 19.5x.

- In 2024, analysts expect the company to grow its EPS by 1%, which is expected to gradually improve to 4% in 2025 and 18% growth in 2026.

- While these numbers are subject to change, they indicate a consistent recovery similar to upswings like the one after 2016.

- With that said, to value TROW, I would use a 17x earnings multiple, which is below its normalized P/E ratio. I believe it makes sense to go with a lower multiple in an environment of sticky inflation, which could keep a lid on people’s ability to put excess cash to work in long-term investments.

- Based on a 17x EPS multiple, the expected EPS growth trajectory, and its dividend, TROW has a 16% total return potential through 2026.

FAST Graphs

To put things into perspective, one of the reasons why the stock is likely to beat its 12% annual return since 2003 is the fact that it is currently in one of the worst stock price declines of the past 40 years!

While a big part of the sell-off is caused by a massive stock price performance during the pandemic, I believe the risk/reward for TROW is quite good at current prices.

In other words, if I were to expand my portfolio with consistent growth in the asset manager industry, I would likely go with attractively valued TROW shares.

On a side note, the company is scheduled to report earnings on February 8 before the market opens. Analysts expect the company to generate $1.60 in EPS, which is based on seven estimates – five of which were upgraded over the past four weeks.

Nasdaq

After two blowout reports in 2Q23 and 3Q23, I would not be surprised if 4Q23 were a blowout quarter as well. After all, market sentiment has massively improved in the fourth quarter, which could allow the company to hint at higher-than-expected AUM and fees.

However, I would not expect a significant stock price movement, as expectations seem to have been adjusted accordingly in recent weeks.

The main risk is a prolonged stock market decline, which could be caused if the Fed is unable to achieve a soft landing. An event of sticky inflation and poor economic growth could put pressure on TROW’s fee income and assets.

Takeaway

Investing in T. Rowe Price presents a compelling opportunity for income growth and value.

As a Dividend Aristocrat with 37 consecutive dividend hikes, TROW offers a high yield of 4.5%.

Despite what its recent stock price weakness may suggest, the company’s consistent growth, diversified financial services, and strategic acquisitions position it for resilience.

With a favorable valuation, analysts project a recovery in EPS growth.

At a blended P/E ratio of 14.9x and a 16% total return potential through 2026, TROW stands out as an attractively valued choice in the asset manager industry.

Q2 2024 Earnings Call Transcript")