2023 was a great year for the stock market. But outperforming years make stocks more expensive, so folks looking for opportunities in 2024 may find themselves having to pay a premium for top companies, especially growth stocks.

However, there were pockets of the market that didn’t have such a great 2023. After surging in 2021 and 2022, energy stocks cooled off last year. As a result, many energy companies with rock-solid earnings are also trading at bargain prices.

Here’s why Devon Energy (DVN -1.88%), Diamondback Energy (FANG 1.62%), and ConocoPhillips (COP 0.63%) are three overlooked dividend stocks worth scooping up this year.

Image source: Getty Images.

Devon Energy’s dividend can help power your passive income

Scott Levine (Devon Energy): Everyone loves a bargain. But to find an ultra-high-yielding dividend stock sitting in the bargain bin? That’s an opportunity that doesn’t come around often. Fortunately for income investors, though, this is exactly the situation with Devon Energy. Shares of the energy exploration and production company are available on sale, and at its current share price, its dividend yields 6.3%.

Unlike oil supermajors that operate throughout the energy value chain, Devon Energy is singularly focused on oil and natural gas production from its assets located in the United States including (but not limited to) the Delaware Basin, Eagle Ford Shale, and the Anadarko Basin.

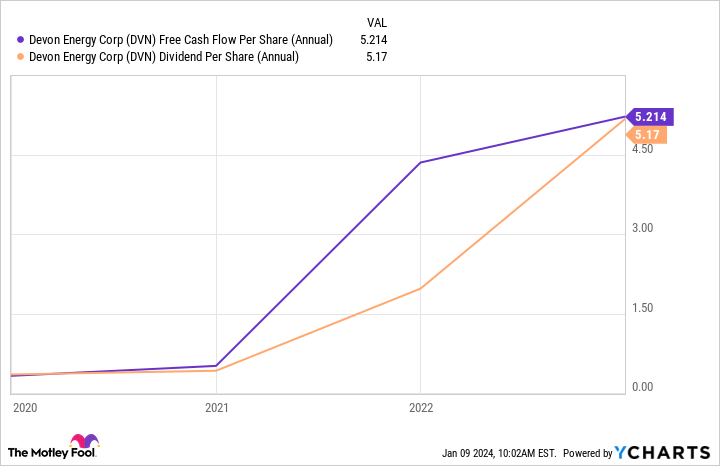

Cautious investors might balk at the company’s ultra-high-yielding dividend, but after drilling down into the company’s financials, they’ll find that the distribution doesn’t represent as much risk as they might have initially feared. Devon Energy’s dividend is split between a fixed payout and a variable payout that’s based on the company’s free cash flow generation. It’s clear, therefore, that the dividend is quite sustainable and isn’t jeopardizing the company’s financial well-being.

DVN Free Cash Flow Per Share (Annual) data by YCharts.

This trend is expected to continue in 2024. In Devon Energy’s third-quarter 2023 earnings presentation, management projected that the company will allocate 30% of its 2024 free cash flow to retiring debt and strengthening its balance sheet. It plans to return about 70% of free cash flow to shareholders.

Investors can gas up their portfolio with Devon Energy’s stock on the cheap. Shares are valued at 4.4 times operating cash flow, a discount to their 5-year average of 5.1.

Diamondback Energy seeks to create a more dependable dividend

Lee Samaha (Diamondback Energy): The revenue, earnings, cash flow, and, ultimately, dividend prospects for oil and natural gas exploration and production companies are led by energy prices. While that statement rings true for Diamondback Energy, it would be a mistake to conclude that the stock is simply a leveraged play on the price of oil.

Diamondback Energy, similar to its peer Devon Energy, is trying to create more certainty around its dividend outcomes by dividing its payouts into a fixed base component and a variable component. In Diamondback’s case, the current base dividend (protected down to the price of oil of $40 a barrel using hedging instruments) stands at $0.84 a quarter. Annualized, that quarterly base dividend comes to $3.36, offering a base dividend yield of 2.2% at the stock’s current price. Based on management’s projections, that’s the least you can expect down to $40 a barrel.

However, Diamondback isn’t a hedge fund. Its downside hedges start at $55 a barrel, meaning it has upside exposure to a price of oil above $55 a barrel. According to management’s last letter to stockholders: “We still expect to realize at least 95% of WTI when WTI is at least $65 per barrel, with most quarters above that number.”

Management’s capital allocation policy involves returning its free cash flow to investors after the base dividend is paid and stock repurchases are made, up to a limit of 75% of overall free cash flow. For a taste of the results of this strategy, Diamondback paid a variable dividend of $2.53 in the third quarter, making a total dividend payout of $3.37. Annualizing that figure would give the stock a dividend yield of 8.6%.

While it’s unrealistic to expect that payout on an ongoing basis, it’s reasonable to assume a yield (based on the current stock price) in the range of 2.2% to 8.6% based on the price of oil ranging from $40 to $80 per barrel, making the stock attractive if you are comfortable with those ranges.

ConocoPhillips is returning gobs of cash flow to shareholders

Daniel Foelber (ConocoPhillips): Over the last year, there has been a ton of mergers and acquisitions (M&A) activity in the oil patch. Enbridge bought three natural gas utilities from Dominion Energy. ExxonMobil is buying Pioneer Natural Resources, Chevron is buying Hess, and Occidental Petroleum is buying CrownRock. Within the last two weeks, APA announced it is buying Callon Petroleum. And on Thursday, Chesapeake Energy announced it is merging with Southwestern Energy.

Given all the M&A action, it may seem strange that ConocoPhillips, one of the largest U.S.-based exploration and production companies, has been relatively quiet. Part of the reason is that ConocoPhillips completed its acquisition of Concho Resources in January 2021. That was a massive deal for ConocoPhillips, and in many ways, it set the stage for the flurry of M&A activity that followed. But another reason is that ConocoPhillips tends to be fairly conservative.

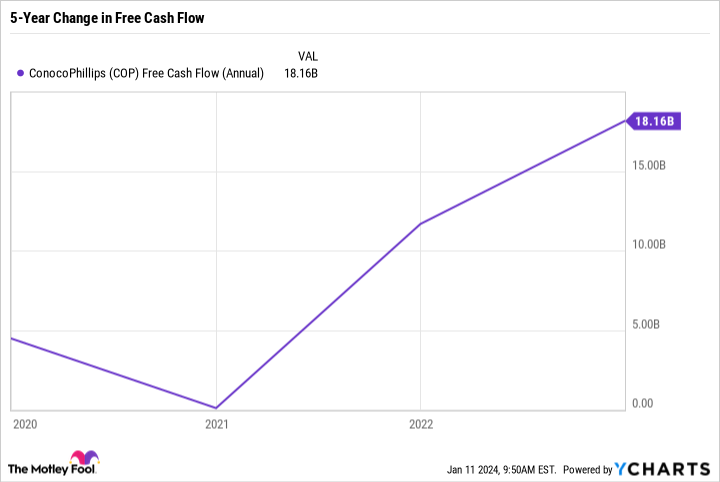

The company operates an efficient business centered around low production costs and high cash-flow generation. Like its peers, ConocoPhillips was stress-tested in 2020. Impressively, it generated positive free cash flow even though WTI oil prices averaged below $40 that year. Since then, ConocoPhillips has been raking it in, including a record year for free cash flow in 2022.

COP Free Cash Flow (Annual) data by YCharts.

On its Q3 earnings call, the company said it expects close to $22 billion in operating cash flow for 2023 and plans to return half of that to shareholders. ConocoPhillips’ dividend payouts consist of a set quarterly “ordinary” dividend, plus a variable dividend that depends on the performance of the business.

In 2023, ConocoPhillips paid $2.11 per share in ordinary dividends and $2.50 per share in variable dividends, good for $4.61 per share total and a yield of more than 4% based on the current price of the stock.

The system is effective because ConocoPhillips has a relatively low ordinary dividend obligation, so it won’t have to cut its base dividend even during weak periods in the energy sector’s cycle. But investors also directly benefit when the company generates outsized profits.

At a price-to-earnings ratio of merely 12.2 and price-to-free-cash-flow ratio of 13.1, ConocoPhillips is simply too cheap to ignore.

Q2 2024 Earnings Call Transcript")