Gervais Williams says he is more bullish about UK equities than he has been at any time in his 30-year City career.

Williams, head of equities at investment house Premier Miton, believes a combination of imminent interest rate cuts, economic recovery, and the end of globalisation, could spark a revival in the UK stock market over the coming months.

‘We’re in a beautiful place,’ he says. ‘The next five years could present investors in the UK stock market with some exciting returns, especially in terms of beautiful growing income.’

Williams is a fund manager who specialises in UK investments. Together with Martin Turner, he runs several investment funds and stock market-listed investment trusts for Premier Miton. They include funds UK Smaller Companies, UK Multi Cap Income, and investment trust UK MicroCap.

The duo also oversee The Diverse Income Trust, which, as its name implies, delivers income from across the UK stock market.

That means holding staple dividend-friendly stocks such as energy giants BP and Shell, as well as income-friendly shares that are off the radar of most investors.

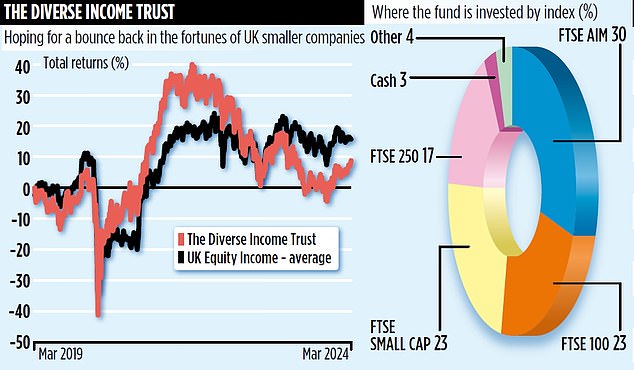

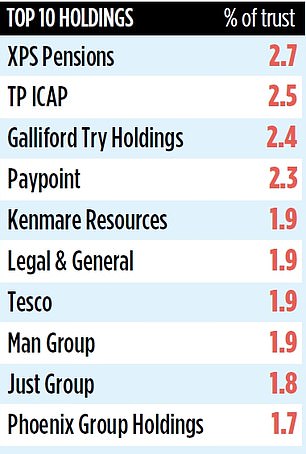

The result is a portfolio comprising 107 holdings, with a bigger exposure to the FTSE Aim Index (30 per cent) than to the FTSE100 (23 per cent). ‘We hunt down income wherever we can find it,’ says Williams. ‘Growing income is the goodness in the portfolio.’

In terms of income, the trust has been a success since it was launched in April 2011 with Williams at the helm – Turner joined a month later.

The total annual income paid to shareholders has gently risen, although occasional one-off special dividends (for example, in the year to the end of May 2019) mean it can’t lay claim to a long track record of consecutive yearly dividend increases – like competing UK equity income trusts such as City of London and JPMorgan Claverhouse.

In the current financial year (to the end of May 2024), the £268 million fund has so far made two quarterly payments of 1p a share, a small 0.05p rise on the equivalent dividends paid in the previous year. To put these into context, the trust’s shares trade at around 85p, with the annual dividend equivalent to a yield of 4.8 per cent.

Yet, like many UK focused investment funds with a lot of exposure outside the FTSE100 Index, the overall capital returns have been meagre. Over the past three years, for example, shareholders have experienced overall losses of nearly 14 per cent.

Williams, however, is convinced that a turnaround is coming – and the short-term numbers suggest it may already have begun. Over the past month, the trust has made a gain of 2.9 per cent.

‘Interest rate cuts are around the corner,’ he says. ‘The ability to raise capital is getting easier for UK companies. It’s all rather exciting.’

Successful investments include Aim-listed energy company Yu Group, which the trust invested in six months ago.

‘It is way ahead of rivals in terms of customer service,’ says Williams. Its shares are up more than 20 per cent since the trust bought into it.

Toilet paper supplier Accrol, a trust holding, is currently a takeover target of Portuguese rival Navigator. Williams is unimpressed. ‘We don’t want the companies we hold to be taken over,’ he says. ‘We have them in the portfolio because we like them.’

The trust has a stock market identification code of B65TLW2 and a market ticker of DIVI. Annual charges are just below 1.1 per cent.

Q2 2024 Earnings Call Transcript")