Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Marijn Bolhuis and Neil Shenai are economists at the International Monetary Fund. All views expressed are of the authors only and do not represent the opinions of the IMF, its Executive Board or management.

In March 1989 US Treasury secretary Nicholas Brady launched a plan to resolve the festering Latin American debt crisis by helping governments via the issuance of “Brady bonds.”

These Brady bonds were created to convert the defaulted bank loans of 17 countries between 1990 and 1998 into new tradable securities with various credit and liquidity enhancements, such as interest payments secured by other high-quality assets. To ensure repayment of the new claims, countries undertook ambitious economic reforms, anchored by loans from the International Monetary Fund and the World Bank.

And it worked! The Brady Plan succeeded by providing debt relief, anchoring economic reforms, increasing productivity, and safeguarding economic reform momentum in the countries that participated.

Unfortunately, developing economies are once again facing difficulties, with debt distress risk prevalent among many of the world’s poorest countries. This has naturally rekindled interest in the Brady Plan — and rebooting some kind of modern iteration of it. Would a new form of Brady bonds work though?

To inform this debate, we first wanted to map the effect of the original Brady Plan, and see how it actually helped countries. So we analysed the impact by comparing the macroeconomic outcomes of Brady countries to 50 other emerging markets and developing economies, some of which also had to restructure their debts around the same time.

Unfortunately, there is a pretty big data sample of sovereign debt distress in the 1980s-1990s.

Our results (full paper here for the sovereign debt restructuring geeks) corroborate the view that the Brady Plan was indeed a great success.

Tl;dr: participating countries had significant declines in public and external debt, with a sharp pick-up in output and productivity growth. They tended to have a stronger commitment to structural reforms. The overall impact was stark.

In the decade prior to the first round of debt relief, Brady countries grew at an average rate of 1.5 per cent per year, whereas non-Brady countries grew at an average rate of more than 3 per cent. But during the decade following the first Brady deal in 1990, the growth rate of Brady countries more than doubled to 3.4 per cent, while economic growth in the control group was unchanged.

The average debt reduction was about 22 per cent of GDP. But notably, the impact of the Brady Plan on overall debt levels was many times greater than initial amounts of debt relief from the actual debt restructuring, indicating the existence of a “Brady multiplier” of debt reduction.

But why? What made this programme a success, when many similar efforts often fail?

We reckon the Brady Plan worked because participating countries actually used the breathing room provided by debt relief to undertake needed macroeconomic and structural reforms. They increased their openness to trade and investment, liberalised product markets, and eased barriers to domestic and external finance.

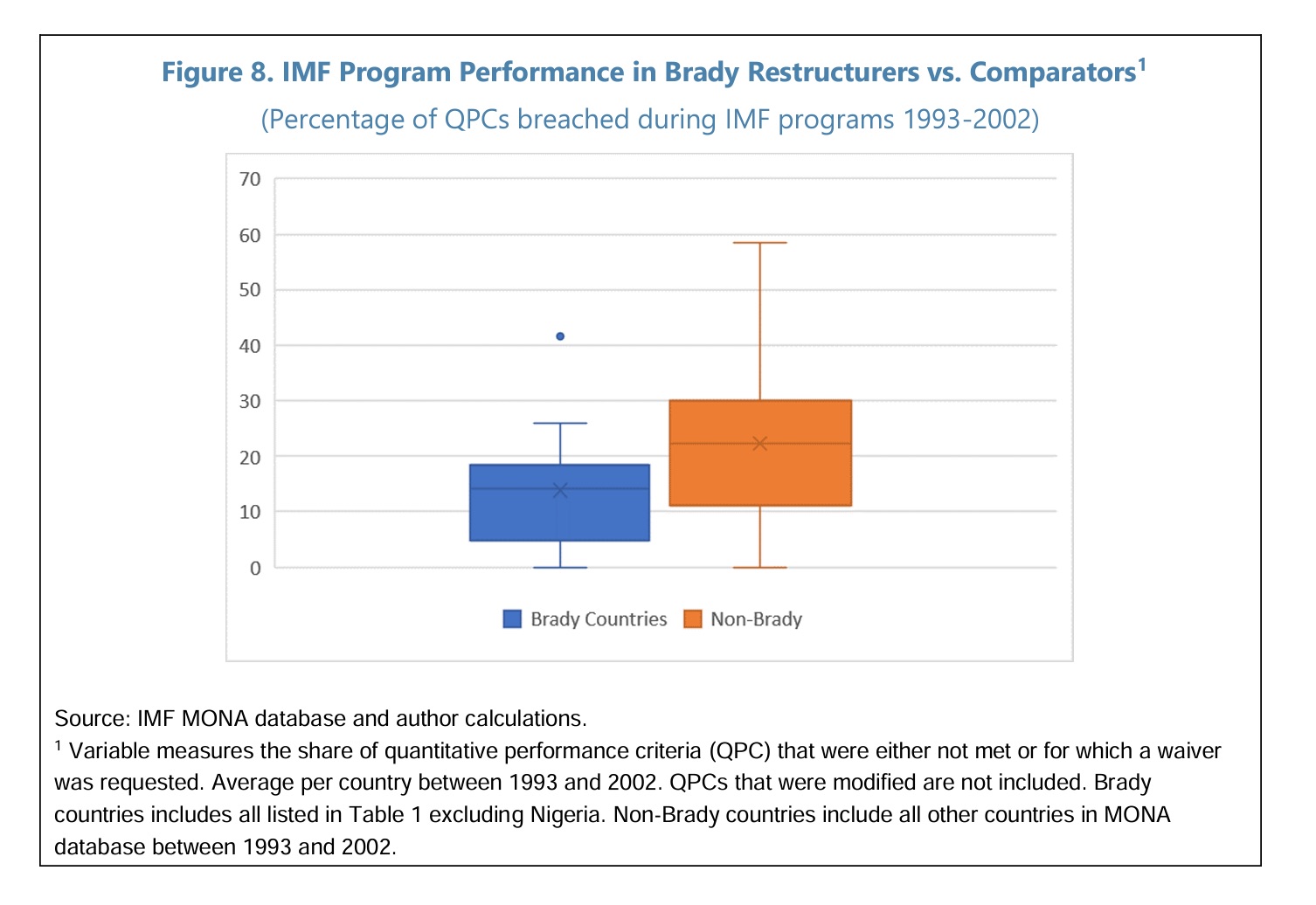

They committed to their IMF programs, performing better than their non-Brady peers (see the graphic below). In short, Brady restructurers worked hard to make the most of the Brady Plan debt relief windfalls.

So, what does this tell us about the potential for a rebooted Brady Plan today?

Ultimately, today’s challenges are different from the Brady period. As our IMF colleagues have argued, many African countries are experiencing a “great funding squeeze.” This analysis implies that liquidity — rather than solvency — is the main fiscal challenge facing most countries today.

If solvency challenges become more widespread and acute, we believe that Brady-style restructuring mechanisms could be helpful in delivering meaningful debt stock reduction in certain circumstances. But a rebooted Brady Plan would still not be a panacea.

The record of debt relief is mixed. Brady countries met specific criteria, including having strong institutions compared to, for instance, Heavily Indebted Poor Countries restructurers. Brady deals also took place at a time of strong global economic growth outlook, which can be contrasted to the tepid growth outlook today.

While Brady exchanges could be useful tools in a diverse toolkit to facilitate sovereign debt restructuring, Brady-style mechanisms alone would not solve the challenges of today’s sovereign debt landscape, including those related to creditor co-ordination, debtors’ at times weak institutions, an aversion to structural reforms, and some countries’ reliance on domestic debt, among others.

That’s why more progress needs to be made in various multilateral forums dealing with these issues, including through the G20’s Common Framework for Debt Treatments beyond the Debt Service Suspension Initiative and the Global Sovereign Debt Roundtable. Dusting off a 30-year old plan unfortunately wouldn’t be a silver bullet.

Q2 2024 Earnings Call Transcript")

{kind=link}