BAY ISMOYO/AFP via Getty Images

I. Introduction

Disruption and disruptive are now part of the business vocabulary but are so widely applied as to be almost meaningless. Clayton Christensen, who was a Harvard Business School strategy professor, made the term central to his PhD thesis turned best-seller, The Innovator’s Dilemma: When New Technologies Cause Great Firms to Fail (1997). He defined it as “an attack from below” where a new technology allows a small player to compete against a dominant firm with a cheaper product that initially has lower performance along one or more dimensions but has some new attribute that allows it to find buyers. Over time the disruptor is able to improve on weaker features and move upmarket, disrupting the dominant firm.

| The Silicon Valley gospel of “disruption” has descended into caricature… | |

| Cory Doctorow, Locus, January 7, 2019 |

A consummate salesman, Christensen leveraged “disruption” into a lucrative consulting business. Perhaps he was too good a salesman: his central case, the computer hard drive industry, is a tale of teams headed by Alan Shugart leaving one firm for another to continue improving hard drives. No disruption there, as Jill Lepore argued in the New Yorker in June 2014. Similarly, in a 2015 Sloan Management Review article King and Baatartogtokh were unable to replicate the “disruption” claim for 70 out of 77 cases used in the 2003 follow-up Christensen co-authored with Michael Raynor, The Innovator’s Solution. Other research found that new technologies just as frequently enter from above, are launched by incumbents, or fall behind subsequent improvements in incumbent technologies. Furthermore, “technology” is not the only competitive factor, with branding, service, and superior operations often more important. Even Christensen eventually adapted to the fact that most “disruptive” technologies soon fail and shifted his claim to the importance of “disruptive [technology] strategies.”

So, why does this matter when examining potential investments in players in the Chinese auto market? It is in fact crucial because many on Seeking Alpha seem to build their portfolio strategies around claims of “disruptive” strategies and the assumption that automotive is a winner-takes-all industry. Another caution: Christensen himself shut down an investment portfolio built around “disruption” after large losses.

More centrally, passenger vehicles are highly differentiated consumer durables. Shifts in automotive technology and business models over the past century, helped by growth in their home markets, saw Japanese, Korean, German, French, and Italian automakers evolve into global companies. However, no firm dominates the industry. We will likely see several new entrants from China become global players, and at least for now Tesla (TSLA) has created a strong brand. However, it remains but one strong brand among many. (Most automotive startups fail, it’s disingenuous to attribute their exit to Tesla.)

My purpose below is to examine disruption and differentiation, based on the Chinese New Energy Vehicle market of EVs and PHEVs.

I structure my argument by starting with GM Wuling (II), then turn to Tesla (III), and follow up with BYD (IV). I pull together in an analytic summary (V). I digress to examine over market dynamics in China (VI). While 2024 is coming off of a record-setting 12 months, sales are down sharply from Dec 2023 despite the Lunar New Year holiday falling in February. Investors looking at firms whose performance hinges on China should be cautious. Finally, I surveyed other Chinese EV plays (VII).

II. GM Wuling: Disruptive Strategy but no Disruption

Overview

SAIC GM Wuling is a multiparty joint venture between SAIC, GM, and Wuling, that initially was selling over 1 million units a year of small box trucks and pickups aimed at rural markets, mostly using ICE drivetrains. In 2020, however, GM Wuling entered the passenger vehicle market with the Wuling Hongguang Mini EV. (See my Seeking Alpha article here GM, BYD And Tesla: Strategy Comparison In China EV Market | Seeking Alpha for details on the Hongguang Mini.)

This is the quintessential disruptive strategy: entering the market from below with a low-cost product that offers fewer features. Prior to the Hongguang Mini, the A00 sub-subcompact segment was trivial in size, with just 6 models selling a total of 3,817 units in January 2020, or under 0.3% of the market. However, packaging challenges made it easy to engineer very small cars such as EVs. By eschewing performance – low acceleration, low top speed, modest range – they could employ small, low-voltage drive motors, inexpensive power electronics, and small battery packs that did not need active heating or cooling. A00s are light; the Hongguang Mini EV has a curb weight under 1,500 lbs.

Author database

The Hongguang Mini quickly dominated the segment, and initially seemed poised to disrupt the overall EV market, topping the Chinese sales chart in August 2022 at 55,742 units and holding 2.8% of the overall passenger car market in December 2022. Others rushed to enter with their own sub-subcompacts, and by March 2022 the A00 segment accounted for 6.8% of the total market. But A00’s only briefly surpassed NEV sales in the compact “A” and subcompact “A0” segments, then faded. It didn’t help that Shanghai, China’s single largest EV market, refused to register new vehicles in the A00 segment. A00 cars haven’t disappeared, but in December 2023 they held only 3.3% of the total car market. Despite growth of the total NEV market, A00 NEV unit sales in 2023Q4 remained below the level of 2021Q4.

Subsequently, GM Wuling launched a series of follow-on products, including a subcompact (A0 segment) sedan, the Binguo, in March 2023, and A class (compact) sedans and SUVs. From its second month the Binguo was selling over 10,000 units and month, and from October 2023 over 20,000 units. But it ends there. With only 2 models selling over 20,000 units a month, Wuling is not disrupting the market. Furthermore, while the overall passenger vehicle market is dominated by compact or smaller models of sedans and SUVs, that market is shrinking, not expanding: in 2020Q1 small vehicles were 66.3% of the market, but by 2023Q4 the share had fallen to 58.0%. As in the US and Europe, those with the wherewithal to purchase new vehicles increasingly prefer large vehicles, though China is idiosyncratic in that sedans remain popular.

Author database

In sum, the auto industry has proved immune to disruptive strategies. The Model T proved a flash in the pan, as by the mid-1920s it was displaced by larger cars with better interiors. Ford Motors itself ceased US production for several months in 1927 to retool to produce the larger, more expensive Model A. Ford has never regained the top spot. Similarly, as seen in the chart above, Wuling has so far been unable to leverage its success in the A00 segment to a larger market presence.

By the 1920s industry soon understood that new car purchasers were higher in income than the average car owner and that small models had to be priced low to be competitive with used cars in the next larger size segment. While smaller cars might allow market entry, the money was to be made from luxury and near-luxury products, Toyota with Lexus, and VW with Audi.

Wuling Brand Models

January 2020 models were primarily sold as commercial vehicles; that is also true of the MPVs and vans that it sold at end-2023. (I do not have data for models sold exclusively as commercial vehicles.) It’s impressive to see the sheer dynamism. Despite that, Wuling has been unable to replicate its success with the Hongguang MINI EV, maintains a minor presence in the growing “A” compact segment, and has nothing in the “B” segment. So to date, its “disruptive” strategy has not borne fruit.

Author database

III. Move Upmarket, No, Move Downmarket: Tesla’s Strategic Incoherence

Initially, Tesla appeared to be following the opposite strategy: enter at the boutique end with the Roadster, move downmarket with the Model S/X, and move further downmarket with the Model 3/Y. However, what’s next? – a move back upmarket with the new Roadster, which in fact appears to have been moved to the back burner? a move into the higher-margin pickup truck market, exemplified by the Cybertruck? Now we have plans to instead move downmarket with a “Model 2.” How concrete those plans are remains uncertain. (Apparently, Tesla has just broken ground at its new Mexican site.)

With the Cybertruck and the Roadster, Tesla’s most recent product decisions seem to be dominated by Musk and “bro” culture. That is Donald Davis’ “Conspicuous Production” thesis, with Detroit’s pre-1920 elite entering the industry, only to founder by crowding the market with models aimed at their country club brethren. Ultimately these firms were rendered irrelevant by the outsider, Henry Ford, and finally driven from the market by the technocrats at General Motors, who had no ties to the fin-de-siecle Michigan elite.

It’s not that the initial ventures funded by Detroit’s old elite didn’t have their moments. To cite Davis,

Between 1899 and 1903 Olds paid cash dividends of 105 percent while increasing its capital from $350,000 to $2,000,000. As its story became known, Detroit’s old families scrambled to invest in the automobile industry; and by 1905 they enjoyed a virtual monopoly over local profits from auto manufacturing. That year their companies – Olds, Packard, Northern, Cadillac, and Wayne – produced some 12,000 motor vehicles, or more than half the national total.” (pp 33-34, Donald Davis, “Conspicuous Production,” JSocHist 1982; see his subsequent book, Conspicuous Production: Automobiles and Elites in Detroit, 1899–1933. Temple Univ Press, 1988.)

Davis goes on to trace the exit of the owning families from their initial automotive ventures, their inability to co-opt executives at Ford and the East Coast financiers who controlled GM into their circle, and their failure to make Detroit a banking center.

Approaching the industry on a model-by-model basis is also idiosyncratic; Ford survived the Model T debacle of the mid-1920s only by shifting to a full-model-line strategy, which allowed it to be the major player alongside GM in the various (and varied) European, South American, and colonial markets. Toyota, VW, and Stellantis are similar, with multiple brands that span an array of segments and price points. Will Tesla henceforth focus on the Model 2, which will provide the potential to sell globally? Of course, as a latecomer, it will face direct competitors who are now on their second generation of A-segment products. In addition, Tesla’s branding is “performance” – over 40 NEV sedans in China are already priced below Tesla’s $25K target, so announced plans aren’t actually for a mass-market model. I believe the most sensible strategy would aim to become another BMW, with a full line of modest-volume upmarket offerings. The portfolio approach provides insurance, too, against the failure of a single model. Remember the “Edsel”?!

Neither past product decisions nor the slow pace of new model development gives me confidence Tesla can engage in a full-model press. In my judgment, the most likely trajectory is that Tesla will slide into irrelevance as the Model 3/Y age, and the Cybertruck hits the limits of its niche – pickup trucks are rural work vehicles in Europe and China. To repeat, Musk has provided no coherent vision and has not been good at execution. It’s sad, because Tesla still isn’t the strongest brand in the industry, but without fresh product, it has no value.

One thing remains clear: while Tesla may have encouraged regulators to push for electric vehicles, and executives at firms new and old to chase its stock multiples, Tesla has not been disruptive in Christensen’s sense of the term.

Table: Tesla China Sales: Jan 2020 vs Dec 2023

|

Drivetrain |

Model |

Brand |

Base price |

Segment |

Jan 2020 |

Nov 2023 |

|

|

EV |

Model 3 |

Tesla |

26.0 |

B car |

0 |

15,627 |

|

|

EV |

Model Y |

Tesla |

26.4 |

B SUV |

0 |

49,877 |

Source: Author database

IV. Full-court press: BYD’s product line strategy

BYD (OTCPK:BYDDF) is representative of the core of the Chinese passenger vehicle industry, which with sales (including exports) of 24 million units is almost 50% larger than the US market. Now entry modes varied, with BYD (and the privately owned Great Wall) starting with buses and trucks, respectively, before moving into passenger vehicles. For that matter, the long-time market leaders VW and GM entered the Chinese market via joint ventures that initially made a single model. Today, VW covers all segments except for A00 sub-subcompacts, with both sedans and SUVs in each segment. It also covers the luxury segments with domestically made Audi’s, as well as imports of Porsche’s and a variety of Audi models not made in China.

Back to BYD. In January 2020, BYD had only 6 models that sold more than 1,000 units: one A0 SUV, two A cars, one A SUV, one B SUV, and one MPV (a van rather than an off-roader). Subsequently, two of them have been relaunched, with new vehicles bearing the same name; two are no longer produced; and two remain but have never been more than weak sellers. At end-2023, BYD now has 10 models with sales over 10,000 and has added the Denza and Fangchengbao luxury brands and the Yangwang super-luxury brand. Between them, BYD models cover the A0, A, B, C, MPV, and D segments, with bargain offerings such as the Seagull, mid-range offerings such as the Seal and Han, and Denza models priced comparable to Tesla.

To repeat: in 10 years BYD has launched 4 brands. In the past 4 years, it’s launched 12 new models and phased out 4 models (by ceasing production or replacing with a totally new car). It’s engaged in a full-court press.

Table: BYD Sales in China, Jan 2020 vs Dec 2023

Author database

Notes: Lower-volume models (less than 5K/month) not detailed are BYD series: BYD D1, BYD e6; Warship series: Corvette 07; Imperial series: Yuan Pro; Denza brand: Denza N7, Denza N8. Other models are no longer being sold: BYD F3, Denza X, and Song. Too unwieldy to include!

V. Comparative Analysis: Why BYD Can Grow

Motor vehicles are highly differentiated durable goods. Use cases vary. Commercial vehicle markets are highly fragmented, but even the personal vehicle market must serve families small and large: with cars used only occasionally and driven hours a day; and for incomes high and low. Tastes vary, too, from the comparatively utilitarian to individuals for whom a personalized drive is a core part of their lives. That’s not a recent phenomenon, as highlighted in Tom Wolfe’s seminal 1963 Esquire story, “There Goes (Varoom! Varoom!) That Kandy-Kolored (Thphhhhhh!) Tangerine-Flake Streamline Baby (Rahghhh!) Around the Bend (Brummmmmmmmmmmmmmm)…”

[Mea Culpa: The late Tom Wolfe, an alumnus of where I taught, once spent 90 gracious, delightful minutes chatting with my undergrad auto industry class. He himself had “pimped” a white Cadillac with white sidewall tires and a white interior. Cars are prominent in his novels.]

Cars are also durable goods. Henry Ford belatedly discovered that the Model T’s greatest direct competitor was not some model from Chevrolet but used Model Ts. To keep from sales being cannibalized, GM and eventually even Ford learned to update models frequently, from biennial refreshes to full model changes every 4 years or so for the top-selling models that upon leaving the dealership lot constituted a large fleet of resalable used cars.

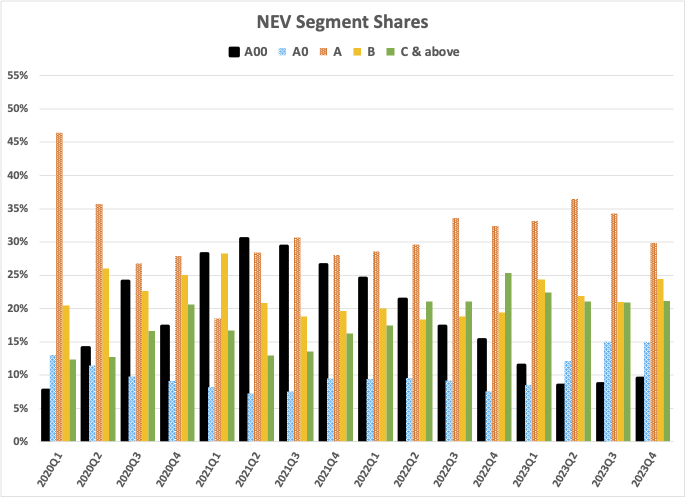

There’s lots of variation, but the imperative is clear: long-term success in the automotive industry requires offering a wide array of models that are updated on a regular basis. The increasing pace of change over the past 25 years adds one more factor: meeting new regulations and employing new technologies requires new platforms and models. But across the past 4 years segments have remained relatively stable, with only a slight shift away from sedans.

(click charts to expand; side-by-side below with same scale

Author database |

Author database |

Conclusion One: In automotive winner does not take all, and second movers often do better than those who bring new technologies to market. IP rights – strong patents – don’t change that: no major manufacturer wants to be beholden to a single supplier, and it’s typical that after the first generation of products, car companies mandate cross-licensing to competitors before making a technology standard across their product lines. First-to-market remains the most important automotive IP strategy.

Conclusion Two: Variety is of the essence. That comes home if you tour the Ford Piquette Avenue Plant in Detroit, where the Model T was originally assembled. (To my knowledge, it’s the only extent pre-WWI production facility anywhere.) Now a Model T museum, it highlights the huge variety of vehicles that resulted once a Model T was purchased. While Ford offered a standardized product available only in black, they were converted into omnibuses, snowmobiles, luxury coaches, and work trucks of amazing variety and reflecting great ingenuity.

Lemma One: Not every new model hits a sweet spot. Every seasoned executive knows that they’re playing a high-stakes game of craps. A new model on an existing platform requires at least $100 million up front for engineering and tooling before the first car is sold. Design and performance must be locked in today (early 2024) for a car that goes on sale in 2026. It needs to sell well for four years to be really profitable. Not every car that looks wonderful to management when they sign off on it in February 2024 will still sell well in January 2030, and in both China and Europe. A few will be full-fledged flops. Only a broad portfolio provides insurance against misreading styling cues or which segment will be popular. A broad portfolio also mutes the impact of winners.

In any case, managers don’t get feedback on whether a car will be a hit for 3 or more years. By that time, the design and features of other models will be locked into place. The larger the ship, the harder it is to turn, for worse as well as for better.

Lemma Two: Successful models get tweaked, not redesigned. The stronger the brand, the greater the pressure to be conservative: the downside from not attracting cross-shoppers is offset by the increased likelihood that existing customers stick with you. (Think from the opposite end: a radical redesign risks turning away current owners while not attracting new customers.)

Today Tesla has only one strong seller, the Model Y. If well managed, Tesla won’t kill the golden goose, but serving the same old thing won’t create the enthusiasm needed to attract new customers. If they do a radical redesign, the downside can be disastrous. Tesla needs a portfolio.

Conclusion Three: It’s absurd to speak of a “Tesla Killer” or a “Model 3 Killer”. Competition is on multiple margins, some with little impact. Over time, however, cannibalization increases as used cars become available and styling and technology age. As electric vehicles proliferate, “performance” will become less of a distinguishing feature. Potential purchasers may still be blown away by the acceleration of a dual-motor Tesla but will decide they’d rather have great acceleration and less excitement in a more opulent, less plastic-feeling interior. Those wanting safety will have more, and more affordable, options for sophisticated driver assist systems. Tesla needs a portfolio.

Conclusion Four: It’s absurd to talk of EVs “killing” the ICE. EVs are simply the wrong option for many use cases. Many car owners around the world don’t have a dedicated spot where they can install trickle charging and don’t have time to loiter at a public charger that requires a detour and a surcharge for a high current draw. A contractor may have an irregular but tight schedule and frequent long drives.

VI. Macroeconomic Trends: No Red Flags, No Checkered Flags

A quick digression, since I track the larger market. The floating Chinese (Lunar) New Year fell in January last year, distorting YoY comparisons. The good story is that the last 12 months set a new record even without taking exports into account. The bad news is that the first 4 weeks of January 2024 are down 15% from December 2023, and EV manufacturers that release data early are down even more: a drop of 41% for BYD, 38% for Li, 59% for XPeng and 44% for NIO. The Lunar New Year falls in this month (February) so sales will also be off by – but from a high level. EV sales weren’t up in December, and for many firms were down sharply in January (See CnEVPost for press releases).

So four graphs: sales since Jan 2020, the 12 ms rolling average, the 3 ms rolling average, and monthly sales since 2015. So far a declining driving-age population, a real estate crash, and poor employment prospects for new school leavers haven’t made a dent. Given seasonal factors at the start of the year, I see no reason that we’ve reached an inflection point – but no indication that we haven’t.

(click charts to expand)

Author database |

Author database |

Author database |

Author database |

Notes: Chinese Passenger Vehicle Market is Jan 2020 – Dec 2024. Other charts extend through Dec 2024 and extrapolate to Jan 2024 using Jan 1-28 data.

VII. Lessons for Investors: Competitive Analysis

I’m not into short-term stock plays. I like small-stakes poker with friends, but I’m not wealthy enough to play with real money. When I pick a stock, it’s because of a sound underlying strategy and reasonable execution. For automotive, does a firm have a portfolio strategy? Does it have a track record of launching new products with a regular cadence? Does it give evidence of the organizational ability to cut losses when things aren’t going well? How well do they resist fads, driven by management chasing P/E today to lock in fat bonuses? (My list is a bit different for automotive suppliers.)

GM Wuling: They have a disruptive strategy, but from their starting point as a regional specialist in small commercial vehicles they are ill poised to move upmarket in passenger vehicles. Furthermore, there’s no direct play: you can’t invest in GM Wuling, Wuling, or (from the US) joint-venture partner SAIC. Furthermore, the total profits that can be earned from being successful at selling low-priced models simply won’t move the needle at firms the size of GM or SAIC. The technology also won’t transfer to other, more profitable segments; the engineering tricks used to keep A00 segment prices low don’t scale to larger segments.

Tesla: Tesla has no clear product strategy. A single platform with only two “top hats” generates almost all of its revenue and profits. It has an abysmal track record of developing and launching new products in a timely manner. The list of bets is long: the Roadster, the Semi, the CT, a robot, a supercomputer, a go-it-alone approach to driver assist systems, software engineers seconded to X, big bets on castings and a breakthrough in battery manufacturing, and now a Model 2 that would continue Tesla’s march downmarket from the original Roadster and then the Models S/X. Solar. Storage. I see divergent pressures, not coherence.

BYD: BYD clearly has a strategy of developing a broad product portfolio, segmented vertically with BYD, the upscale Denza brand, a luxury brand, and a new supercar “halo” brand. Not every model has done well, but the phenomenal growth of the firm shows the strength of developing products targeting an array of price segments and use cases. They’ve also been lucky, with incumbents targeting segments that are too up-market (NIO), or launching hybrids that make good environmental sense but that policymakers aren’t willing to sell to politicians (Toyota). Competing new entrants are, well, too new or made early missteps from which they, as small firms with few models, can’t readily recover.

- Li (LI) currently has 3 models; all sell over 10,000 a month, giving reasonable economies of scale. Spy shots of “mules” are now online of the L6, to be launched later this year. To its credit, Li has been the strongest player of any type of drivetrain in the two larger, higher-margin large SUV segments. Growth, however, is thus capped as these segments are small. To generate greater volume it needs another factory (which is under construction) and to move downmarket. That, however, will result in lower prices and hence lower profits the same capital-equal investment as its upscale models, even assuming it maintains margins, which I find unlikely. They’ve been lucky with their early products, and earning money gives them the time to broaden their portfolio in a measured manner.

- NIO’s offerings hit two segments with both SUVs and sedans. However, they are priced well above same-segment offerings. NIO also made a big, early bet that battery swapping would become standard, and around its standard. It lost that bet. That makes expanding its geographic reach capital-intensive, as it also chose the direct sales route so can’t let dealers – local entrepreneurs who know their market – finance new sales/service points. Only one model exceeds 5,000 units a month, but sales of that model declined in the past 5 months. NIO was an early entrant to the EV market but then took 2 years to launch additional products. They have a flawed strategy and are moving too slowly.

- XPeng (XPEV) has added one model a year. None have been hits, no flops. They seem to have a sensible strategy, but unlike Li none of their products have the combination of margins and volume to make the company cash-flow positive. They are a late mover, and they didn’t luck out with an initial hit product.

Author database Author database Author database

Afterward / Notes

My database covers domestically produced passenger vehicles from Jan 2020 through Dec 2023. I update on the 15th of each month when I can access detailed data, cross-check across multiple sources, and check drivetrains of new models on car shopping sites. The model-level data exclude imports (about 700K), exports (about 3,525K including trucks), and commercial vehicles (about 4,000K). My database thus covers 21.8 mil out of 30 mil in motor vehicle sales.

I have tentative data on sales by model in revenue rather than units. So far I have not tried to analyze it in detail. In terms of revenue, the biggest player by far is the VW group. Second is Toyota. Including imports, Mercedes is probably in third place. I don’t have revenue data for imports, but those of VW (Audi, Porsche) and Toyota (Lexus) would increase their lead over all other firms, and probably push the total revenue of Mercedes above BYD. Ditto BMW.

Thirty years ago Chinese provinces imposed tariffs, backed by armed customs booths on their borders with neighboring provinces. There was no national market. That began changing with a reorganization of China’s fiscal system in 1994. Auto firms started narrowly regional in sales, and that legacy continues to affect the industry. I have access to data on the geography of sales, but the underlying source is not organized in a manner that makes assembling data easy. Tentative analysis finds Tesla sales concentrated in a dozen large cities, with no sales in rural areas and smaller cities. In contrast, BYD is national in scope, including cities large and small, and rural areas. GM Wuling sales appear to be regional, reflecting its origins as a small commercial vehicle producer, and skewed towards smaller cities and rural areas.

Oh, and I believe all the Chinese-focused firms I mention in this article are overpriced.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")