adventtr

Diodes Incorporated (NASDAQ:DIOD) is a semiconductor company specializing in the DAO market segment. We analyzed the company following its recent earnings briefing, as its revenue declined in 2023 by 16.9%. Our analysis delved into the breakdown of the company’s business segments across various end markets to evaluate its overall performance. We examined its potential to capitalize on the anticipated recovery in the semiconductor industry in 2024. Additionally, our analysis extended to the company’s product developments within each segment, aiming to identify its strategic focus on specific end markets for sustained long-term growth. Furthermore, we assessed the company’s profitability, noting a decline in margins in 2023, and explored the prospects of improvement in 2024 and beyond.

Strong Growth Across Segments

Company Data, Khaveen Investments

|

Diodes Revenue Breakdown ($ mln) |

2014 |

2015 |

2016 |

2017 |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

Average |

|

Industrial |

303 |

272 |

198 |

242 |

316 |

350 |

283 |

415 |

540 |

467 |

|

|

Growth % |

11.0% |

-10.3% |

-27.2% |

22.5% |

30.2% |

10.8% |

-19.2% |

46.9% |

30.1% |

-13.6% |

8.1% |

|

Communications |

178 |

153 |

273 |

274 |

304 |

287 |

258 |

289 |

300 |

205 |

|

|

Growth % |

-10.2% |

-14.2% |

78.8% |

0.3% |

10.7% |

-5.3% |

-10.2% |

11.9% |

3.9% |

-31.6% |

3.4% |

|

Consumer |

178 |

178 |

226 |

264 |

291 |

287 |

307 |

343 |

380 |

299 |

|

|

Growth % |

13.4% |

0.1% |

26.8% |

16.5% |

10.6% |

-1.4% |

7.0% |

11.6% |

10.8% |

-21.3% |

7.4% |

|

Computing |

196 |

204 |

179 |

190 |

206 |

200 |

246 |

542 |

480 |

381 |

|

|

Growth % |

12.9% |

4.0% |

-12.1% |

6.0% |

8.8% |

-3.2% |

23.0% |

120.3% |

-11.3% |

-20.7% |

12.8% |

|

Automotive |

36 |

42 |

66 |

84 |

109 |

125 |

135 |

217 |

300 |

310 |

|

|

Growth % |

43.6% |

19.1% |

55.4% |

27.9% |

29.6% |

14.3% |

8.2% |

60.2% |

38.5% |

3.3% |

30.0% |

|

Total |

891 |

849 |

942 |

1,054 |

1,214 |

1,249 |

1,229 |

1,805 |

2,001 |

1,662 |

|

|

Growth % |

7.7% |

-4.7% |

11.0% |

11.9% |

15.2% |

2.9% |

-1.6% |

46.9% |

10.8% |

-16.9% |

8.3% |

Source: Company Data, Khaveen Investments

Based on the table above of the company’s revenue segment breakdown, the company’s total revenue declined by 16.9% for the full year in 2023 with negative growth across all segments except for Automotive. This is a stark contrast to its past growth track record which averaged at 8.3%. In particular, its Automotive and Computing segments have the highest average growth, both of which are higher than its total average of 8.3%. However, Automotive slowed down sharply in 2023 as the company highlighted “softness” in the automotive market while Computing declined by 20.7% as the PC market declined by 13.9% according to the IDC.

IC Insights, WSTS, Company Data, Khaveen Investments

In terms of market share, the company’s share in the DAO market has been quite stable, with a slightly increasing trend over the past 8 years with an average share of 2.1%, which is in line with our estimated share for the company in 2023 Thus, we believe this indicates it has had stable market positioning in the DAO market and the company’s 2023 decline primarily attributed due to the semicon industry downturn in 2023, which fell by 8.2% based on WSTS. Specifically, the analog market was estimated to have declined by 8.9% in 2023. However, the industry sales growth is projected to recover in 2024 with a growth of 13.1%, which could bode well for Diode’s prospects of a recovery in 2024.

Moreover, from its latest earnings briefing, management emphasized that it sees “customer inventory levels returning back to normal levels” and expects to experience a recovery in Q2 2024 onwards. In 2024, we previously projected for the PC market to rebound back to positive growth (18.7%) after 2 years of decline following the surge in shipments during the pandemic period. Additionally, we believe the growth of ADAS and EV adoption could continue to spur the automotive market.

Overall, we believe that while the company experienced a slowdown in revenue growth with a prorated growth rate of 16.9% as the semicon industry faced a downturn, the company could be poised to benefit from the anticipated semicon market recovery from 2024 with a positive growth rate of 13.1%. Additionally, our view of a recovery year aligns with management expectations as it highlighted its customer inventory levels have normalized. In particular, we see the PC market rebounding as well as the automotive market growth continue to be driven by ADAS and EV technologies, supporting the company’s growth recovery in 2024.

Product Developments for Long-term Growth

Furthermore, according to the company’s investor presentation and earnings briefing, the company’s R&D efforts highlighted its long-term focus on the Industrial and Automotive segments which could support its growth outlook. In 2023, the company highlighted that it “increased investments in new product development which result in the over 350 new automotive-compliant products”.

We compiled the company’s product developments in the past 1 year based on its press releases and categorized them into product types and its end market segments to determine its focus.

|

Summary Table |

SiC |

LED Driver |

Switch |

Power Semicon |

Sound Drivers |

Sensors |

Connectivity |

Total |

Company Average Growth (%) |

Market Forecast CAGR |

|

Industrial |

2 |

1 |

0 |

2 |

1 |

1 |

1 |

8 |

8.8% |

12.95% |

|

Communications |

2 |

1 |

0 |

1 |

0 |

0 |

0 |

4 |

3.9% |

8.0% |

|

Consumer |

0 |

1 |

0 |

3 |

1 |

0 |

1 |

6 |

8.0% |

8.0% |

|

Computing |

1 |

1 |

1 |

2 |

0 |

0 |

0 |

5 |

13.3% |

23.8% |

|

Automotive |

3 |

2 |

3 |

6 |

0 |

1 |

1 |

16 |

30.8% |

10.1% |

|

Total |

3 |

2 |

3 |

9 |

1 |

1 |

1 |

20 |

8.9% |

8.0% |

|

Market CAGR (%) |

34% |

24.6% |

7.10% |

4.90% |

2.47% |

9.40% |

15.06% |

|||

|

Market Size (2022) ($ bln) |

1.46 |

5.68 |

16.92 |

48.9 |

27.49 |

199.5 |

71.6 |

Source: Company Data, Semiconductor Today, Precedence Research, Spherical Insights, Allied Market Research, Data Bridge Market Research, Zion Market Research, Market and Markets, Khaveen Investments

As seen, the majority of the company’s product developments are concentrated in power semiconductors followed by SiC and switches. According to Allied Market Research, the power semicon market is forecasted to grow at a CAGR of 4.9%.

Moreover, by end market segment, the majority of the company’s product developments are focused on the Automotive segment with 80% of total product developments. The automotive market segment has a strong forecast CAGR of 10.10%, and Diodes’ Average revenue growth for the Automotive Segment is 30.8%, the highest growth of all segments and 3x higher compared to the average total revenue growth.

Besides that, the Industrial segment has the second highest product developments such as Dual Digital Interface, Multi-Channel LED Driver and new sound driver ICs. Additionally, the industrial semicon segment market forecast CAGR is 12.95%, and Diodes’ average revenue growth in this segment is 8.8%.

While the company could benefit from the anticipated overall semicon industry recovery in 2024, we also believe the company’s focused product developments on high-growth automotive and industrial end markets could support its long-term growth outlook. For example, we highlighted the Automotive and Industrial segment CAGR of 10.1% and 12.95% respectively, higher than the average of 8%. Additionally, both these segments combined share of revenue increased further to 46% of total revenue in 2023, highlighting the significance of its revenue contribution and could increase its total company growth outlook due to the increased revenue contribution from these segments.

Profitability Margins Benefit From Recovery

Company Data, Khaveen Investments

|

Earnings & Margins |

2018 |

2019 |

2020 |

2021 |

2022 |

2023 |

|

Gross Margin (%) |

35.86% |

37.29% |

35.07% |

37.14% |

41.35% |

39.61% |

|

EBIT Margin |

12.67% |

14.11% |

10.94% |

15.30% |

20.24% |

15.05% |

|

Net Margin (%) |

8.57% |

12.27% |

7.98% |

12.67% |

16.56% |

13.67% |

|

Free Cash Flow Margin (Total Investing Cash Flow) |

8.48% |

10.72% |

7.22% |

10.96% |

6.54% |

6.37% |

|

Free Cash Flow Margin (Capex Only) |

8.59% |

10.87% |

9.74% |

11.12% |

9.22% |

7.47% |

Source: Company Data, Khaveen Investments

Finally, in terms of profitability, the company’s margins have declined in 2023. Based on the chart above, the company’s margins appear to be heavily influenced by its revenue growth. This indicates that the company’s margins are primarily affected by economies of scale. During 2015 and 2020 when its growth was negative, its margins were impacted negatively. Thus, we believe the company’s margin decline is due to its negative growth in 2023 affecting its economies of scale.

As we expect the company’s revenue growth outlook to be positive in 2024 amid the anticipated overall semicon market recovery and its long-term growth outlook being supported by its focus on automotive and industrial segments, we believe this could bode well for the company’s profitability outlook as well. This is as the company’s margins had been heavily influenced by its revenue growth due to economies of scale. Thus, as we see its revenue growth recover positively from 2024 onwards, we expect its profit margins could continue to improve as it achieves a larger scale. Furthermore, our expectations are also in line with the company’s outlook as it previously emphasized it expects to return to growth and focus on achieving its profitability target of $1 bln in gross profit.

Risk: Competition

Despite its stable market share, the company is relatively smaller compared to the top companies within the DAO market. Additionally, market leader TI (TXN) also focuses on Industrial and Automotive end markets, which could pose a competitive threat to Diodes. As covered in our past research, we determined that larger analog competitors such as TI, ADI (ADI) and NXP (NXPI) have a wide product breadth which gives them an advantage.

Verdict

Following its full year 2023, the company revenue had contracted by 16.9%, a significant decline compared to its past average growth of 8.3%. However, in 2024, we believe the company is well-positioned for recovery, as the semicon industry is projected to grow by 13.1% in 2024. We believe our projected rebound in PC market shipments as well as continued growth in ADAS and EV adoption could support the company’s recovery in 2024. For its long-term outlook, we identified its focus on high-growth automotive and industrial segments, which now account for a significant portion of revenue combined (46%) and bodes well for its future growth opportunities. Finally, in terms of profitability, we expect its margins to benefit from the revenue recovery following a decline in 2023 as its margins are closely aligned with its revenue growth.

|

Top Analog Companies |

EV/EBITDA (‘TTM’) |

EV/EBITDA (5-year) |

|

Diodes |

7.66x |

9.47x |

|

Texas Instruments |

17.54x |

17.38x |

|

ADI |

16.38x |

20.16x |

|

NXP |

13.21x |

15.17x |

|

Infineon |

8.37x |

13.14x |

|

STMicro |

6.16x |

9.90x |

|

Skyworks |

11.89x |

12.31x |

|

Renesas |

9.48x |

10.68x |

|

Average |

11.34x |

13.53x |

Source: Seeking Alpha, Khaveen Investments

Moreover, in the table above of a peer comparison with top analog companies’ EV/EBITDA multiples, Diodes’ EV/EBITDA (‘TTM’) of 7.66x is 48% below the average ratio of 11.34x. While this may indicate an undervaluation, its 5-year average EV/EBITDA (9.47x) had been 43% lower than the 5-year average of the top companies (13.53x). We believe its lower EV/EBITDA than competitors reflects its smaller scale as it only has a 2% market share, compared to larger players such as ADI and TI which have much higher multiples.

Hence, we believe valuing it on the basis of its historical average multiples is more reasonable.

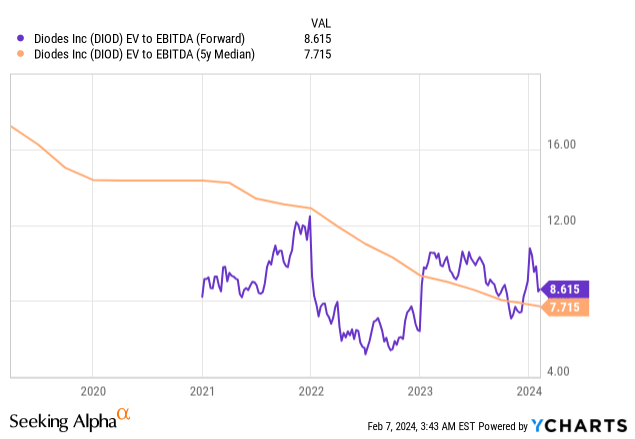

YCharts

The company’s forward EV/EBITDA is 11% higher than its 5-year median of 7.7x, indicating its limited upside from its current valuation. Based on analyst consensus estimates, the company has an average price target of $71.22, which is an upside of only 4.4%, thus we rate it as a Hold.

Q2 2024 Earnings Call Transcript")