Hispanolistic

Introduction

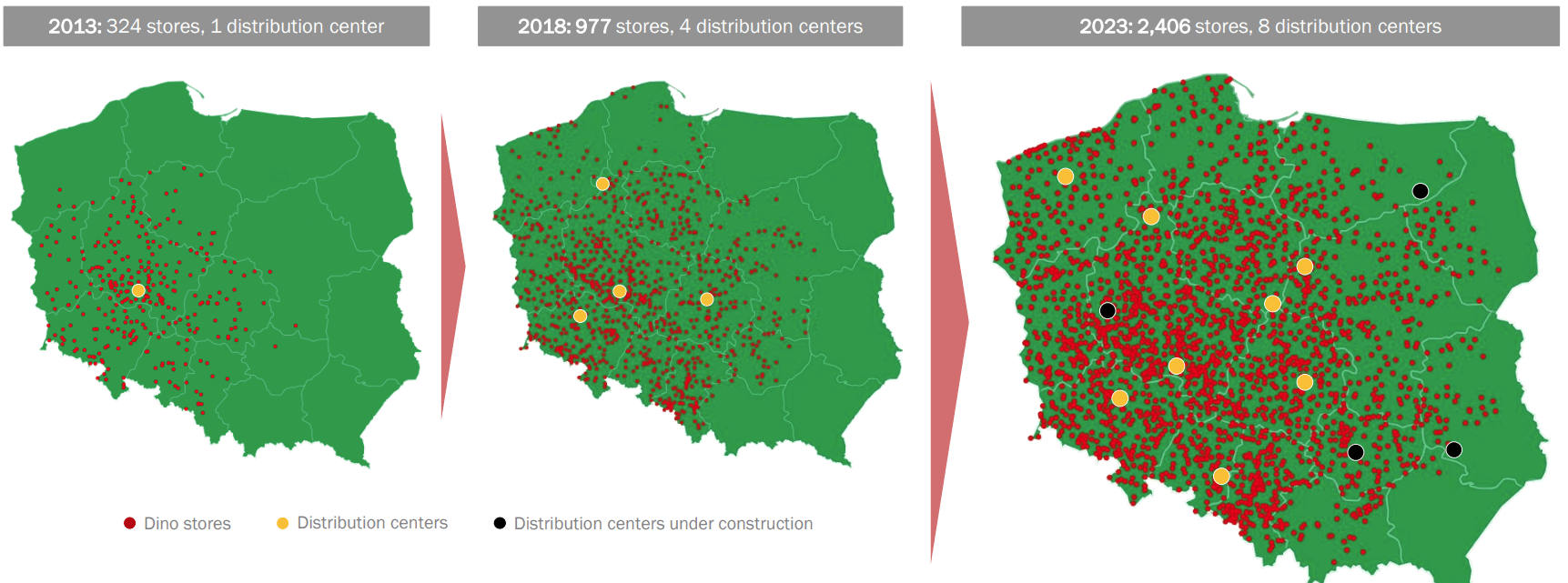

Dino Polska S.A. (OTCPK:DNOPY) is a Polish food retailer operating over 2,400 grocery stores around Poland. The company operates in the mid-sized supermarket segment and focuses its growth investments on rural small towns or outskirts of larger cities in Poland. Dino has invested significantly in the growth of its store network and currently focuses only on the Polish market. The chain has expanded from 111 stores at the end of 2010 to 2,406 stores as of 31st of December 2023, indicating a strong ability to expand its store network. Growth has been profitable, and Dino has been able to deliver an average EBITDA margin of 9.4% between 2017 and 2023. Dino’s market share is estimated to be between 5-10% of the Polish grocery retail market, which indicates that there is still room for growth.

Location development 2013-2023 (Dino Polska 2023 results presentation)

Investment Thesis

Dino is a rare growth company in the food retail industry. Usually, European food retailers are old companies in the mature phase of their growth story. The closest example would be Dino’s main competitor Biedronka, which is owned and operated by Portuguese multinational food retailer Jerónimo Martins, which was founded over 200 years ago. Dino is a relatively young operator that was founded during Poland’s first post-Soviet decade in 1999.

Since the beginning, Dino has been growing strongly, and profitable growth is the backbone of the buy recommendation for Dino’s stock. The company valuation metrics are extended for a food retailer, but when considering the growth prospects, a higher valuation can be accepted. Dino’s management has built a growth strategy on three pillars. First, they aim to continue rapid organic growth in the number of stores. Secondly, they aim to continue growth in like-for-like (same-store revenue) revenue. Thirdly, they aim to consistently improve profitability. If the company can execute the three pillars of management’s strategy, higher valuation metrics can be accepted.

Why Growth Seems Likely to Continue

Dino has a proven track record in the expansion of its store network. Therefore, it is likely that the company can continue on the same track. Between 2016 and 2022, the company opened 237 stores per year, and in 2023 it opened 250 new stores. During Q1’2024, the company opened 32 new stores, which on an annualized basis would mean 128 new stores for 2024. Therefore, the store network expansion pace would be slower for 2024 than 2023, but still, it would mean an approximately 5% increase in the total store count.

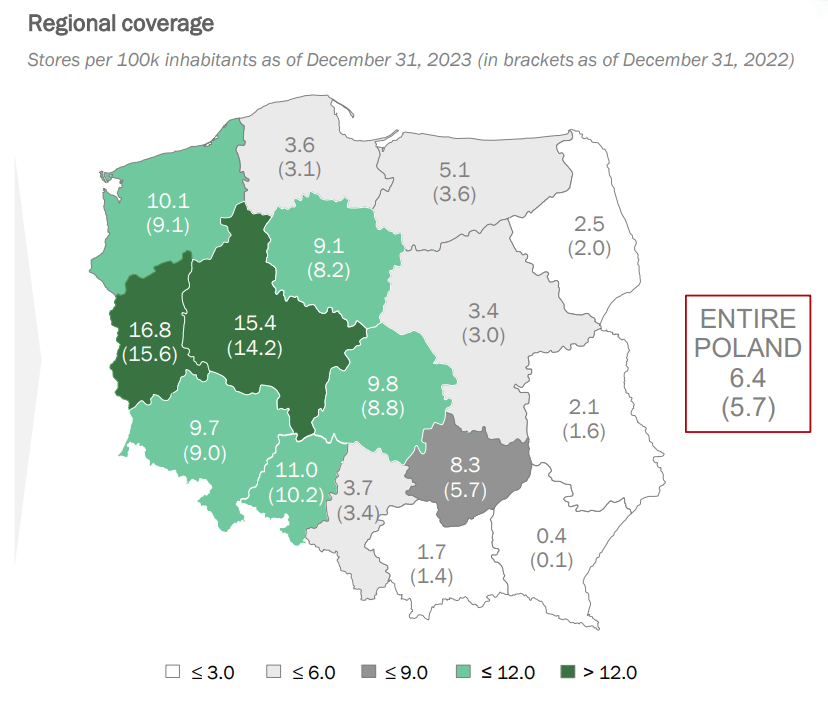

Stores per 100k inhabitants as of 31.12.2023 (Dino Polska 2023 results presentation)

To understand why Dino can continue its expansion and capital investment needed can be justified, we need to understand Dino’s current network in Poland. We can look at this in detail by analyzing the regional map above, which shows the amount of Dino stores per 100k inhabitants in different regions of Poland. Dino’s market penetration in western parts of Poland starts to be high, as western regions have 10-17 Dino stores per 100k inhabitants. Dino has focused on the western parts of the country, as it originally began trading in the Wielkopolski region, which on the map is the region with 15.4 Dino stores per 100k inhabitants. The company has organically expanded its network town by town, focusing on the areas where it already has operations and a logistics network in place. As we see from the map, the market penetration in the eastern parts of Poland is small in comparison to the western parts. This means that Dino still has room for growth in the eastern regions, which validates their strategy. Dino will be able to expand its store network in the eastern parts of Poland thanks to the three distribution centers which are currently under construction in the region.

Financials

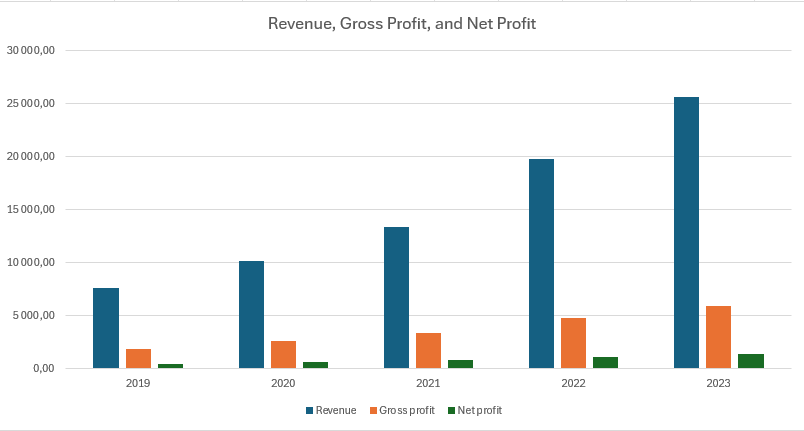

Revenue, gross profit and net profit 2019-2023 (million PLN) (Author, values from Seeking Alpha)

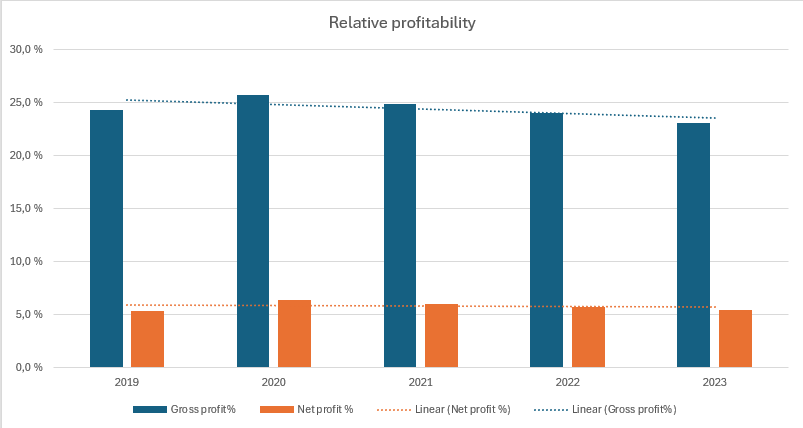

It is critical to analyze the profitability profile of the company to confirm its ability to continue the expansion of the store network. As we can see from the chart above, Dino has been able to increase its total revenue from 7 646.5 million PLN in 2019 to 25 666.3 million PLN in 2023. During the same period, the relative profitability of the company has remained constant. As we can see from the chart below, the gross profit has been slightly trending downwards but is still at a healthy level of 23.1% in 2023 with a 5-year average of 24.4%. The net profit has remained strong at around 5.8% over the 5-year period. Significant increases in the absolute revenue and stable profit margins indicate that the unit economics of Dino stores are strong, and the company can simply add the number of stores to make a higher absolute profit.

Gross and net profit margin 2019-2023 (Author, values from Seeking Alpha)

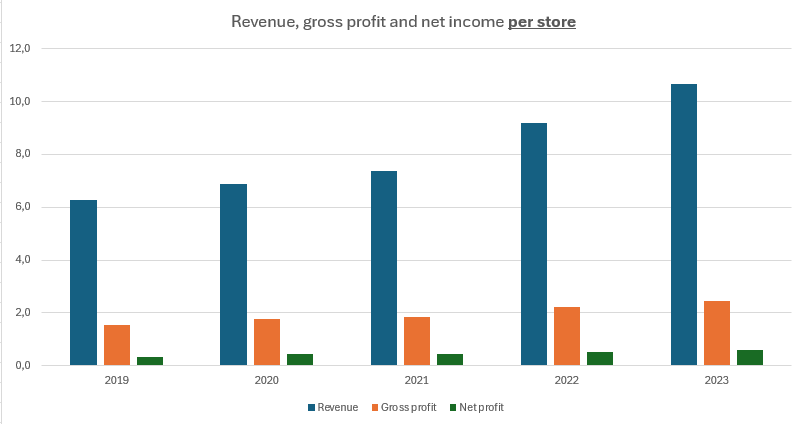

What is interesting is the revenue and profitability development of an average Dino store. As you can see from the table below, during the 5-year period from 2019-2023, the average Dino store has been able to increase its revenue from roughly 6 million PLN to above 10 million PLN. Of course, inflation partially explains the development of a single-store revenue and profitability increase, but still, Dino’s like-for-like revenue increase is above the Polish food inflation (see the chart in the Risks section). In the big picture, this suggests that Dino’s assortment and position in the market are adding value for the Polish consumer as they visit stores increasingly.

Per store revenue and profitability development 2019-2023 (Author, values from Seeking Alpha and Dino Polska annual reports)

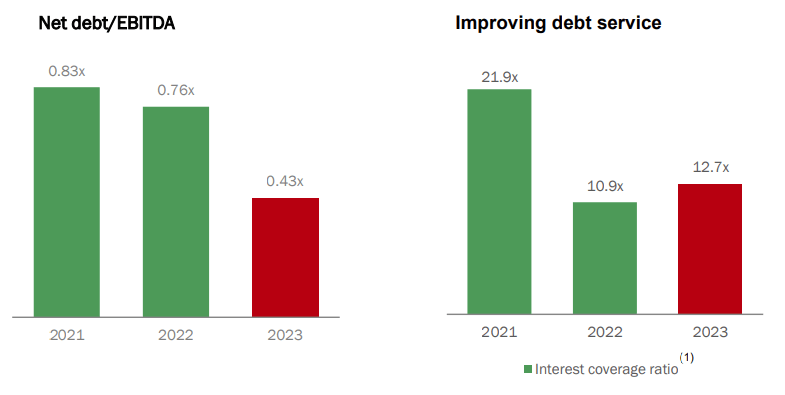

From a balance sheet perspective, the main highlight is that the majority of the growth is financed by operating cash flows rather than by debt. As you can see from the debt ratio picture below, the net debt / EBITDA has decreased, and the interest coverage ratio has remained strong. Overall, Dino had only approximately 9% of long-term debt on its balance sheet as of 31st of December 2023. End of the year 2023, the liquidity of the company was good; cash and cash equivalents were at 218,389 thousand PLN. This represents around 1.5 months of operating cash flow if cash generation continues at a similar rate as in 2023.

Debt ratios (Dino Polska 2023 results presentation)

From a cash flow perspective, Dino’s strategy is clear. The company simply uses cash generated from operating activities to invest in the expansion of its store network. Of course, partial cash from operations is used on the debt service. Dino does not pay dividends, which is extremely good for investors as it enables the company to focus capital on the growth of its store network. In 2023, 66% of the total operating cash flow was used for the purchase of property, plant, and equipment, which in Dino’s case means the expansion of the store network.

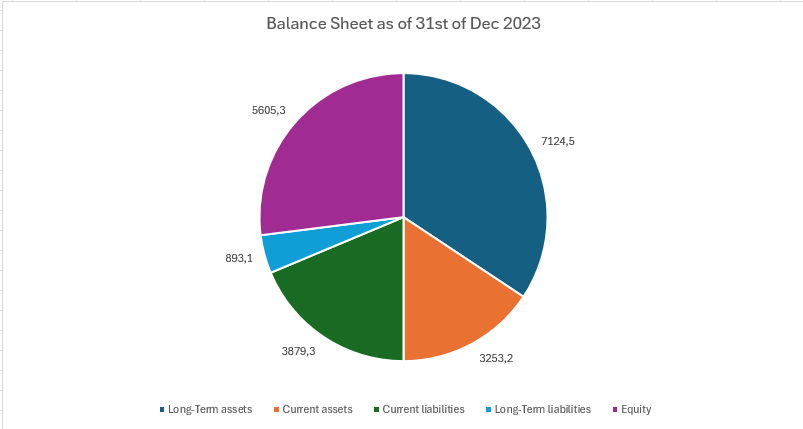

Balance sheet as of 31st of Dec 2023, million PLN (Author, values from Seeking Alpha)

Valuation

5-year stock price chart, Warsaw Stock Exchange (Google Finance)

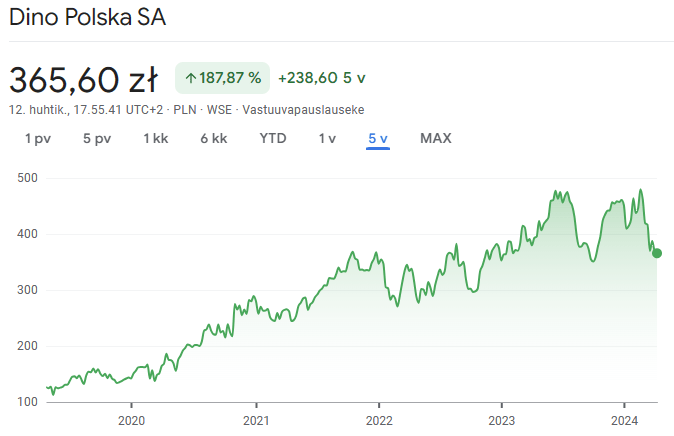

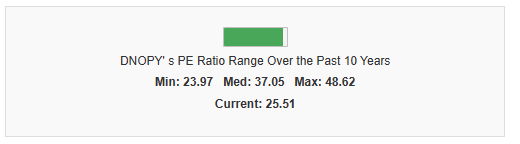

Dino Polska’s stock price development has been a one-way journey upwards. From a valuation perspective, Dino is a challenging stock to analyze. In general, food retailers don’t trade with higher valuation metrics. Usually, P/E-ratios are expected to be low single digits, but for Dino Polska the story is different. Currently, Dino trades at approximately 25 P/E ratio. This means that investors expect Dino’s profitability growth to continue. It must be noted that from a P/E perspective, Dino is currently at the low end of its historical P/E development. According to gurufocus.com (see below) the median P/E for Dino has been around 37 in the past. As I don’t see an indication that would significantly affect Dino’s ability to continue growth, I conclude that a high earnings multiplier is accepted. As long the P/E multiplier is below the long-term average, Dino is a buy stock. Of course, if fundamental growth prospects disappear, high P/E multipliers would not be accepted.

DNOPY’s PE ratio (gurufocus.com)

Risks

Investors planning to invest in Dino Polska must be aware of the risks associated with the development of the company. Even though the company has been able to grow strongly and profitably in the past, it is not a confirmation of future performance.

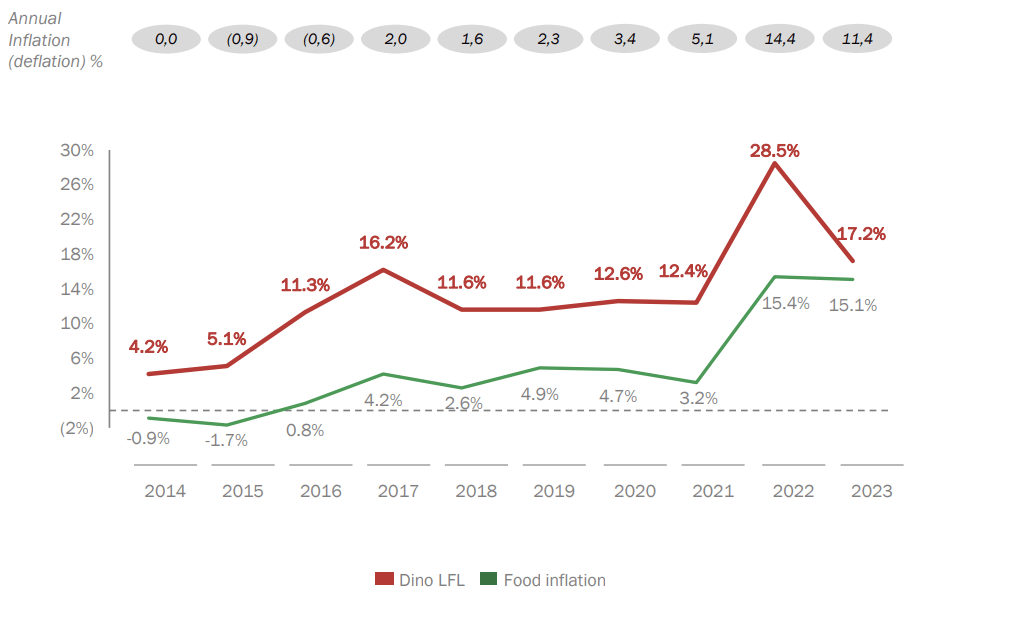

Dino like-for-like sales vs food inflation in Poland (Dino Polska 2023 results presentation)

Dino has been historically able to increase its prices faster than food inflation in Poland, but this does not guarantee that a similar trend will continue. In 2023, the spread between food inflation and Dino’s like-for-like revenue growth was only 2.1 percentage points, which is significantly less than in earlier years. It is possible that Dino is not able to increase its price faster than inflation, which would mean a decrease in its inflation-adjusted revenue growth.

Even though the total debt on Dino’s balance sheet is small, it does not fully hedge the company against increased interest rates. It may be possible that higher interest rates decrease the net profitability of the company, and growth may be slower when capital is used on debt service rather than growth investments.

Dino has been able to improve its position in the Polish grocery market, but it still has multiple competitors. Dino has tried to position itself as an operator in rural areas, where competition is not as harsh as in urban city centers. This strategy is not a guarantee that competitors wouldn’t try to copy Dino’s strategy. The Polish food retail market includes huge multinational players, including Biedronka (Jeronimo Martins), Lidl, Auchan, and Carrefour who have the financial ability to start competition in the same locations as Dino. However, Dino has a competitive advantage to continue the acquisition of good store locations thanks to its related party entity Kron-Invest which is a construction company focusing only on site development for Dino.

Conclusion

In conclusion, Dino Polska is a company with a strong track record of profitable growth. The company has a clear strategy and the Polish food retail market still has untapped opportunities in the eastern parts of Poland. Dino will publish Q1 2024 results on the 9th of May and to confirm the Buy-thesis, I expect that the company has been able to increase its revenue, and cash generated from operations must be on a similar level as in Q1 2023.

Even while the company is trading at a high P/E multiple, the growth prospects seem clear which gives confidence for a buy rating on Dino’s stock at current prices as of mid-April 2024.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")