AlexRaths

Diageo (OTCPK:DGEAF) (NYSE:DEO) is a global leader in alcoholic beverages, with iconic brands across categories admire whiskey, vodka, tequila, rum, and gin. With a market cap around £63 billion and a trailing earnings multiple of 17x, the stock appears modestly valued given Diageo’s competitive advantages. However, changing consumer dynamics create uncertainty around long-term growth prospects. This report aims to supply an in-depth analysis of Diageo as an investment.

Competitive Positioning

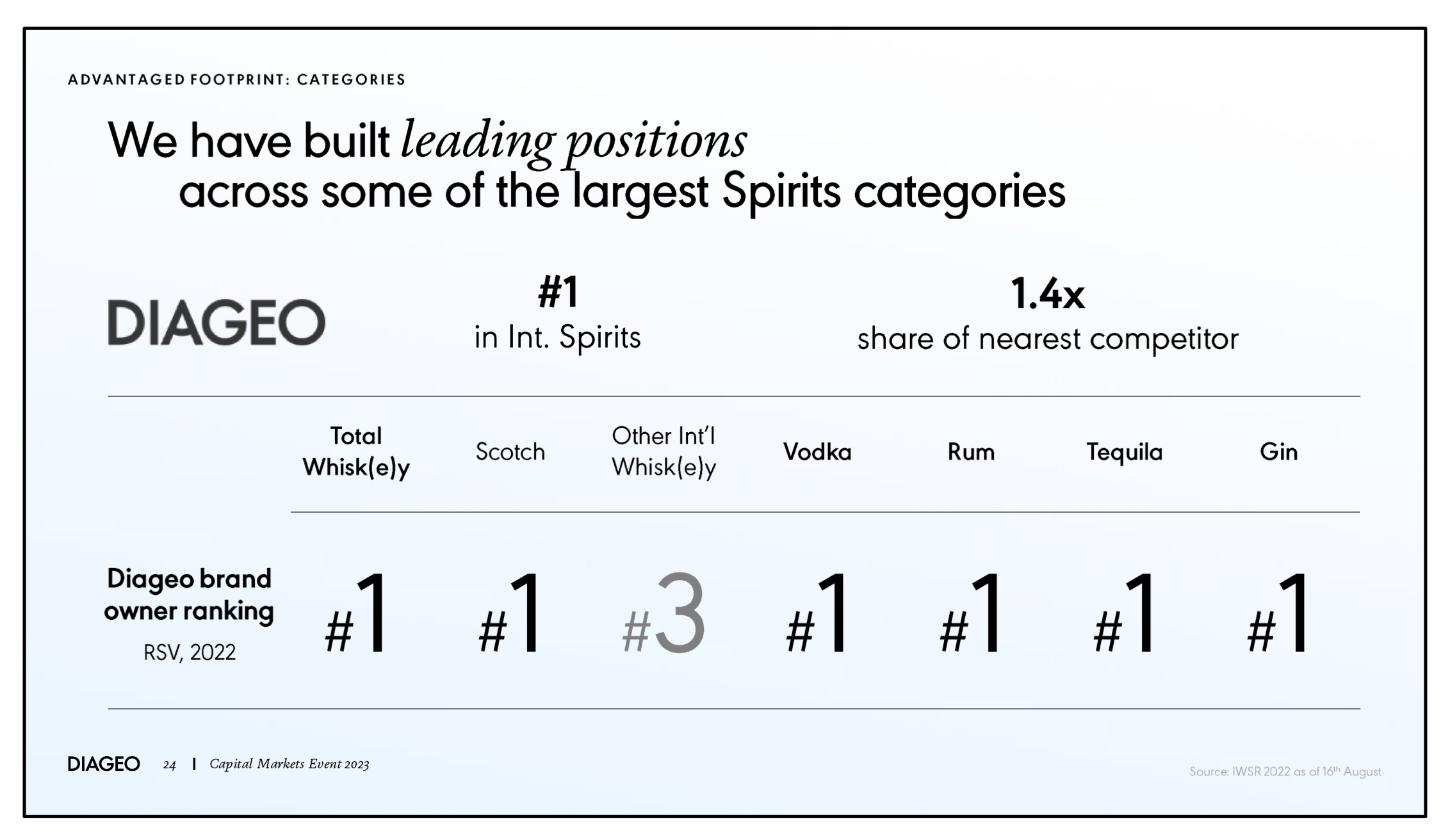

As the largest spirits company globally, Diageo possesses enviable competitive advantages. First the company owns a rich portfolio of category-leading brands: Crown Royal (whiskey), Smirnoff (vodka), Captain Morgan (rum), Don Julio (tequila), Tanqueray (gin). These command pricing power and customer loyalty over long periods.

company presentation

Diageo also has production expertise and capacity built over decades that newcomers cannot easily replicate. For example, a bottle of tequila can take 8- 10 years to evolve and proper whiskey aging requires inventory planning over 10-20 year horizons.

Moreover, the company has an unequalled global distribution footprint. Diageo can access 180 countries worldwide through owned distribution in key markets admire North America (37% of sales)

These advantages have allowed Diageo to deliver consistent top-line growth historically, even through recessions. From FY2000-2022, Diageo grew net sales at a CAGR of 5.4%.

Growth Outlook

Management is very clear on its view that it can continue to drive 5-7% annual top-line growth. It thinks growth can be achieved through the following paths:

- Premiumization trend globally where consumers trade up to higher quality liquor

- Expansion in emerging markets admire India, China, Latin America, Africa

- Innovation by extending brand lineages (e.g. super premium Crown Royal expressions)

- Potential M&A of craft brands

However, growth prospects face a number of countervailing headwinds:

- Slowing alcohol consumption, especially in North American market. Per-capita alcohol refuse accelerated post-pandemic for 21-34 year old cohort. This demographic represents an important segment for building long-term branded spirits loyalty.

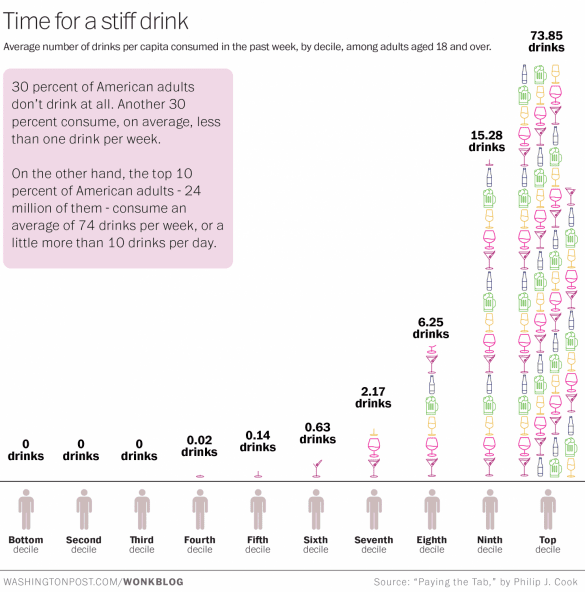

- Potential impact of “super consumers” on volumes. Research shows the top 10% of drinkers account for over 70% of total alcohol consumption in the US. So while broader per-capita measures are declining, the spending habits of these super consumers is crucial. If regular consumers and/or higher-income professionals curb drinking due to health/wellness reasons, it could disproportionately affect overall market volumes. Losing a slice of the super consumer segment would represent an outsized headwind for Diageo’s growth.

- New sobriety-promoting drugs admire Ozempic that may curb drinking longer-term.

On balance, 4-6% sales growth seems reasonable assuming no major global slowdown. Apply a steady 22% net margin and £5 billion profits could be achievable by FY2027.

Valuation

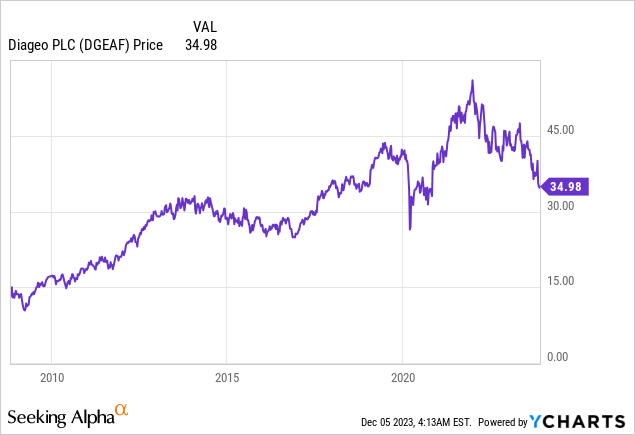

At a £63 billion market capitalization and £3.7 billion trailing earnings, Diageo currently trades at 17x P/E multiple.

Assuming 6% sales CAGR and stable margins for 5 years, a forward P/E of 17-19x would be appropriate. This implies a share price range of £41-45 by 2027. Including dividends at 2% yield, total expected return is 10-12% annualized over the next 5 years.

With Spirit category leadership and geographic diversification, Diageo deserves a premium multiple. While not excessively cheap currently, reasonable upside exists from today’s share price.

Risks

Downside risks beyond the growth concerns mentioned earlier include:

– Persistent inflationary pressures limiting consumer discretionary spend- Geopolitical conflicts or trade wars affecting input costs and global supply chains- Foreign exchange volatility as Diageo derives over 50% of sales internationally

The company seems well-positioned to steer normal economic cycles. But a protracted demand slump could hamper earnings.

A Key Question For Investors

There’s no doubt that younger generations in Western nations are drinking less alcohol and this is a trend that seems unlikely to reverse. At the same time, GLP-1 weight loss drugs clearly supress the desire to drink alcoholic beverages.

While this may seem insignificant, the impact of a small number of super consumers has the potential to meaningfully affect sales. A report in the Washington Post, for example, claims that the top 10% of Americans account for over 70% of US alcohol consumption.

Washington Post

It is this narrative that has contributed to a 20% year-to-date drop in Diageo stock. A key question for investors, therefore, is how significant these trends are and whether they can be offset by other segments.

For example, while younger people may be turning away from alcohol, there’s evidence that older generations are drinking more. And the trend away from alcohol is unlikely to be so prevalent in emerging nations such as India, China and Africa. This is likely to be the key for Diageo stock going forward.

Conclusion

Diageo possesses an elite collection of spirit brands and geographic diversification that warrants a premium valuation. The company is targeting steady top-line growth which could produce low double-digit returns for shareholders if achieved. However, changing consumer dynamics create uncertainty over the long-term thesis. On balance the risk/reward seems reasonable at current prices, though not compelling enough to rate Diageo a strong buy. Consistent with management’s perspective, a neutral rating seems appropriate today.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")