PM Images

It was four years ago when markets were in absolute freefall. The reality of the pandemic’s impact on humanity was being felt in markets, with global equities falling multiple percentage points each session. As markets do, a discounting effect took place by late March 2020, however.

Stocks bottomed out despite the worst of COVID-19’s human toll being months down the line. In that perspective, it feels trite to analyze ETF performance charts, but people’s financial lives were also at stake back then. Today, amid record highs across the US stock market and with foreign shares notching their best levels since April 2022, times feel much different for investors.

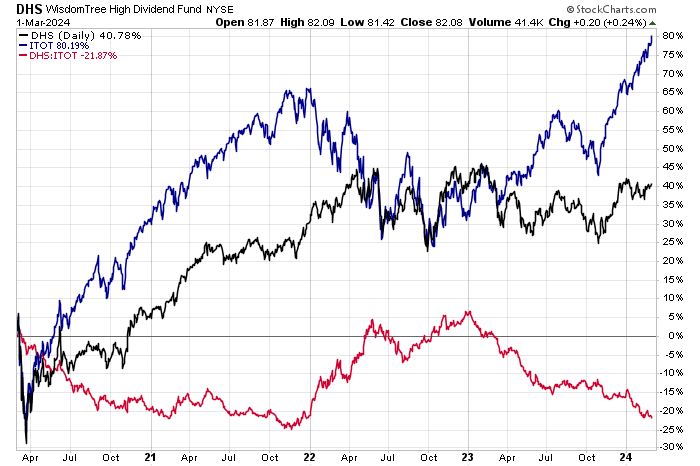

Today, I am revisiting the WisdomTree U.S. High Dividend Fund ETF (NYSEARCA:DHS). I’ve had a buy rating on this factor ETF for several quarters, and I assert that sticking with it remains a solid move. Despite underperformance to the total US stock market since the start of last year, its valuation and quality yield are compelling factors. I will highlight a trouble spot on the chart, though.

DHS: Weak Relative Returns Since Early 2023 As Mega-Caps Have Shined, Near Relative Support

Stockcharts.com

For background and according to WisdomTree, DHS seeks to track the investment results of high-dividend-yielding companies in the US equity market. Investors can use the ETF to get targeted exposure to domestic stocks across market cap sizes of high-yield companies. The fund can also be used to replace a value strategy to achieve demand for both growth potential and income returns.

DHS is a small fund with just $1.1 billion in assets under management as of March 1, 2024. It pays a high 4.3% trailing 12-month dividend yield, and the ETF’s annual expense ratio is low to moderate at 0.38%. Share-price momentum has been lackluster lately, but I make the case that as market sentiment shifts away from strictly favoring mega-caps and toward other size profiles, DHS could be the high-dividend winner in its category. The risk rating is somewhat soft at a C+ by Seeking Alpha, but liquidity metrics are healthy given the ETF’s historical volume profile and low median 30-day bid/ask spread of four basis points.

What sets DHS apart from other domestic high-dividend ETFs is that the fund has ample SMID-cap exposure. The 3-star, bronze-rated portfolio by Morningstar features just a 47% allocation to large caps, with 30% in US mid-caps and a material 23% in small caps.

DHS: Portfolio & Factor Profiles

Morningstar

Given strength among the largest US stocks over recent months, it has underperformed some of its high-dividend ETF peers, such as the Vanguard High Dividend Yield ETF (VYM) and the Schwab U.S. Dividend Equity ETF (SCHD). All three funds, however, are oriented to the value style rather than growth. Should a continued broadening out of market performance take place as 2024 presses on, then DHS and its peers could be attractive places to allocate capital.

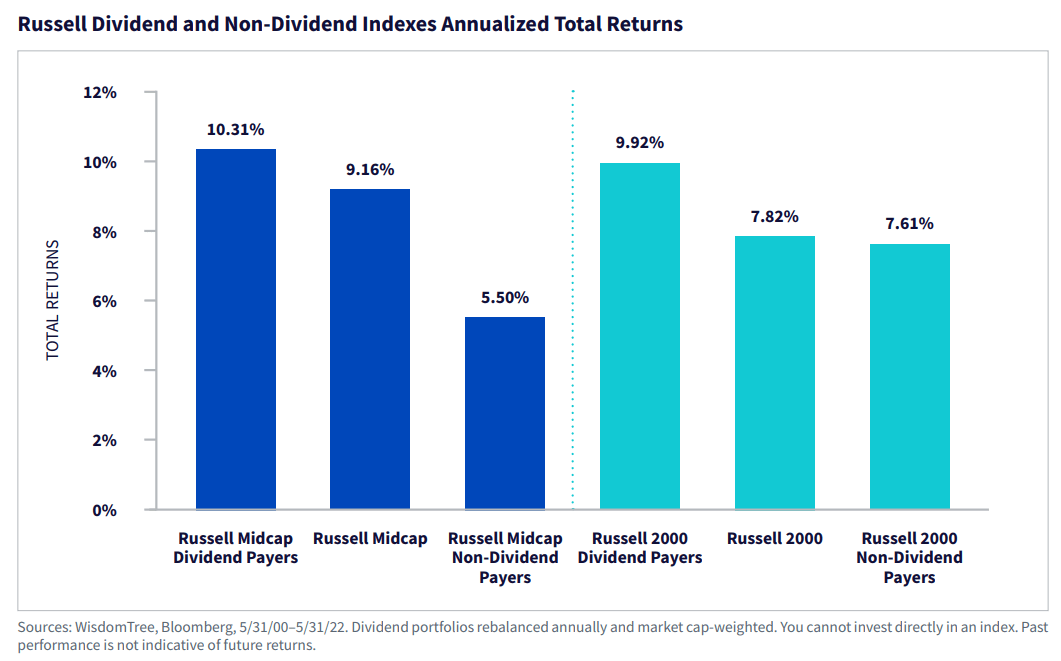

I assert that as participation in the bull market expands, then the once-underperforming SMID-cap niche could lead the way. That would be a boon for DHS, considering that its weighted average market cap plots in the mid-cap section of the style box. Mid-cap dividend stocks, as illustrated below, have posted strong returns since 2000, outperforming Russell Midcap Non-Dividend payers, per WisdomTree.

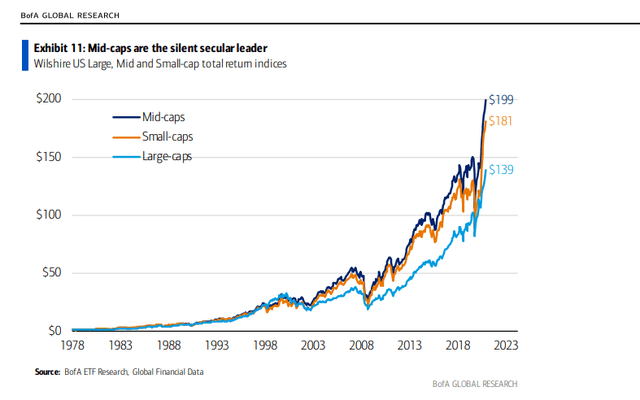

Bigger picture, mid-caps have produced alpha compared to the Russell 2000 Small Cap Index. As I like to say, investors should stop leaving out the mid-caps – it is always a large vs. small debate on financial TV when, according to history, mid-caps have outperformed.

Russell Midcap Dividend Payers Shine Since 2000

WisdomTree

Mid-Caps Have Produced the Best Long-Run Returns

BofA Global Research

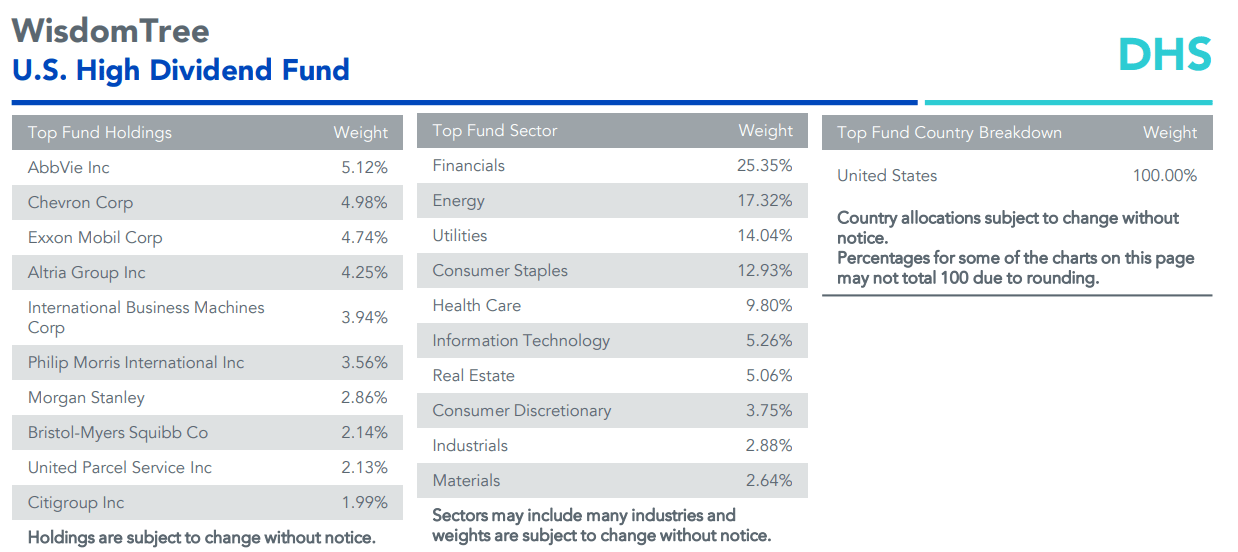

Digging into the portfolio, DHS has a high 25% weight in the cyclical Financials sector. With that area of the market breaking out to fresh highs since early 2022, there is a case to be made that momentum may persist for value areas. Moreover, oil’s move toward $80 last week – a four-month high – could benefit DHS’s high 17% Energy sector position.

What’s not encouraging is that Utilities has been the worst sector so far this year, and DHS has undoubtedly been hurt by a nearly 10 percentage point overweight to that rate-sensitive area. Tech is just 5% of DHS, so it will move materially differently than the S&P 500 and even other high-dividend funds. In all, DHS trades just 12.3x forward earnings today. Contrast that to the S&P 500’s lofty 20+ estimated P/E.

DHS: Financials, Energy, Utilities Overweight

WisdomTree

Seasonally, DHS tends to post mixed returns over the coming months. The March through May period has produced about flat returns over the past 10 years, with the bulk of the fund’s total return not coming until Q4.

DHS: Mixed Seasonal Trends through Q2

Seeking Alpha

The Technical Take

With a low valuation, high yield, and as market trends may be shifting in favor of cyclicals, DHS’s technical chart has its challenges. Notice in the graph below that there’s key resistance in the $83 to $84 range. I would like to see the fund breakout above that point of polarity. Should it do so, then a bullish inverse head and shoulders reversal pattern would be triggered. An upside measured move price objective to about $94 – an all-time high – would be in play based on the height from the head ($73.48) to the neckline (near $84), with that range being added on top of the neckline.

For now, with a flat 200-day moving average, the trend on DHS remains a battle between the bulls and bears. Moreover, the RSI momentum gauge at the top of the graph shows merely moderate price strength lately. Finally, with a high amount of volume by price up to the $90 spot, a sustained rally is doable, but the onus will be on the bulls to work through significant overhead supply.

Overall, with significant negative alpha versus the broad market and some of its high-dividend ETF peers, DHS has its technical troubles.

DHS: Key Resistance Near $84, Bullish Inverse Head & Shoulders In Play

Stockcharts.com

The Bottom Line

I reiterate my buy rating on DHS. Now trading at just 12 times forward earnings estimates and with a portfolio that holds a significant amount of value and cyclical stocks, this fund could be a good place to be allocated as a shift from mega-caps continues.

Q2 2024 Earnings Call Transcript")