DaLiu

Deutsche Telekom (OTCQX:DTEGY) has good fundamentals in the European telecom sector, but this seems to be currently reflected in its valuation and its shares are therefore a ‘Hold’.

As I’ve covered in a previous article, Deutsche Telekom has better growth prospects than most of its peers, due to its strong large exposure to the U.S., through its stake in T-Mobile US (TMUS). As I’m an income-oriented investor, I was not much attracted by its below-average dividend yield, but its shares have outperformed most of its closest peers since my last article, showing that Deutsche Telekom’s investment case is mainly geared to growth rather than income.

In this article, I update the company’s most recent financial performance and its investment case, to see if it is currently a good growth pick in the European telecom sector or not.

Financial Overview

Deutsche Telekom has reported a positive operating environment over the past few quarters, supported by its several business units, even though T-Mobile continues to be its major growth engine. The company continues to benefit from its strategy to invest in infrastructure, namely in its 5G network in the U.S., which has been a distinctive factor over its competitors Verizon (VZ) and AT&T (T). This has enabled T-Mobile to report strong customer growth and market share gains over the past couple of years, a trend that has not reversed in recent quarters.

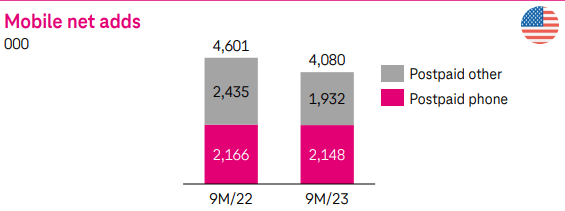

This backdrop explains why Deutsche Telekom continues to report strong growth in the U.S., as T-Mobile was able to grow its net customer count by more than 4 million in the mobile segment, during the first nine months of 2023, still a very good outcome even though its growth has slowed down compared to the same period of the previous year.

Net adds (Deutsche Telekom)

This was a strong support for service revenue growth, which was up by 3.6% YoY in Q3 2023, but this was not enough to offset lower revenue from equipment revenue. Indeed, sales of smartphones have been weak over the past few quarters across the industry, justified by rising interest rates and higher cost of living, leading to overall T-Mobile revenues of $19.2 billion in the last quarter, a decline of 1.3% YoY.

In other geographies, Deutsche Telekom also reported positive customer growth, especially in broadband and TV, leading to group service revenue growth of 3.3% during 9M 2023. However, due to lower equipment sales, overall group revenue was €82.6 billion in the first nine months of the year, a decline of 2.4% YoY.

Despite lower reported revenue, its profitability increased a little bit due to lower costs, also impacted by the deconsolidation of GD Towers its tower business in Germany and Austria, in which Deutsche Telekom sold 51% of its ownership to DigitalBridge and Brookfield. Its adjusted EBITDA in 9M 2023 was nearly €30.5 billion, an increase of 0.8% YoY, boosting its EBITDA margin to 36.9%.

Due to the sale of GD Towers and its Dutch business, which impacted its net profit by €11 billion, its reported profit was nearly €19 billion in 9M 2023 (vs. €7 billion in 9M 2022), but adjusted for this effect, its net profit amounted to €6.1 billion (-13.8% YoY). This drop is mainly explained by positive one-off effects in the previous year, which boosted its net income, making annual comparisons more difficult for the company. Regarding its cash flow generation, Deutsche Telekom has decided to reduce its capital expenditures, which amounted to €13.4 billion in 9M 2023, a decline of 13% YoY, being a decisive factor for higher free cash flow during the period to €11.8 billion (+25% YoY).

Given this strong backdrop across its businesses, Deutsche Telekom raised again its guidance for the full year, expecting to achieve an adjusted EBITDA of about €41.1 billion in 2023 and its free cash flow to be above €16.1 billion, slightly up from its previous guidance as shown in the next graph, showing that its positive operating momentum is expected to continue in Q4.

Key financial metrics (Deutsche Telekom)

Regarding its balance sheet, Deutsche Telekom’s net debt was €137 billion at the end of last September, down by more than €5 billion during 9M 2023, mainly due to its net proceeds from the sale of its stake in GD Towers. The combination of slightly higher EBITDA and lower net debt, led to a declining leverage position, reporting a net debt-to-EBITDA ratio (including leases) of 2.94x at the end of last quarter. This is still somewhat above the sector’s average and the company’s own desired range of between 2.25-2.75x over the medium term but considering its good cash flow generation capacity and growth prospects, I think Deutsche Telekom will be able to reduce leverage organically to its desired range over the next few years.

This means Deutsche Telekom does not need to retain much cash to strengthen its balance sheet, enabling it to distribute a good part of its earnings and cash flows to shareholders. Indeed, this has been its policy in recent quarter, both at its T-Mobile unit and at the group level. Due to share buybacks, its stake in T-Mobile has increased in recent quarters and the company has now reached a majority stake in the U.S. business, holding a 52.1% stake at the end of last September. This was a strategic goal for Deutsche Telekom and something it has been working for during the past three years, from its 43% stake in 2020 when T-Mobile US merged with Sprint.

T-Mobile US also started to distribute dividends in the last quarter, expecting to distribute some €3.75 billion between Q4 2023 and the end of 2024. Deutsche Telekom therefore expects to receive some €1.8 billion in dividends after tax during this period, which is an important support for its own dividend and balance sheet deleveraging efforts.

Related to its 2023 earnings, Deutsche Telekom has already announced that it intends to distribute an annual dividend of €0.77 per share, an increase of 10% compared to the previous year, expected to be paid next April. At its current share price, Deutsche Telekom’s forward dividend yield is about 3.4%, which remains lower than its closest peers, thus its income appeal is not fantastic right now compared to other telecom companies and other fixed-income alternatives, such as bonds or banking deposits.

Conclusion

Deutsche Telekom has maintained a positive operating performance across the group in recent quarters, with the U.S. remaining its main growth engine. This profile is not expected to change much in the near future, considering that current street estimates expect Deutsche Telekom to maintain a single-digit revenue and earnings growth path in the coming years.

This means that in the telecoms sector, Deutsche Telekom offers above-average growth prospects, as most of its peers struggle to grow their businesses. Due to this different profile, Deutsche Telekom does not offer the same income appeal as some of its peers, making its investment case mostly geared for growth.

Regarding its valuation, Deutsche Telekom is currently trading at some 12.2x forward earnings, almost in line with its historical valuation over the past five years of 12.8x. Thus, even though it has better growth prospects than most telecom companies, its shares don’t appear to be undervalued right now and are a ‘Hold’ for the time being.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")