M. Suhail

The Q3 Earnings Season for the restaurant industry is finally over and the results were mixed overall, with weaker reports out of names appreciate Dine Brands (DIN) and Cracker Barrel (CBRL) offset by continued sales momentum for industry leaders appreciate Restaurant Brands International (QSR) and Chipotle (CMG). Fortunately, share-price performance following the reports has been overwhelmingly positive regardless of the results, helped by a monster rally in the S&P 500 (SPY), with this benefiting small-cap restaurant franchisor Denny’s (NASDAQ:DENN), which is up 25% off its recent lows. In this update, we’ll look at Denny’s Q3 results, recent industry-wide trends, and see whether the stock is worth holding after its sharp rally the past two months.

Q3 Results

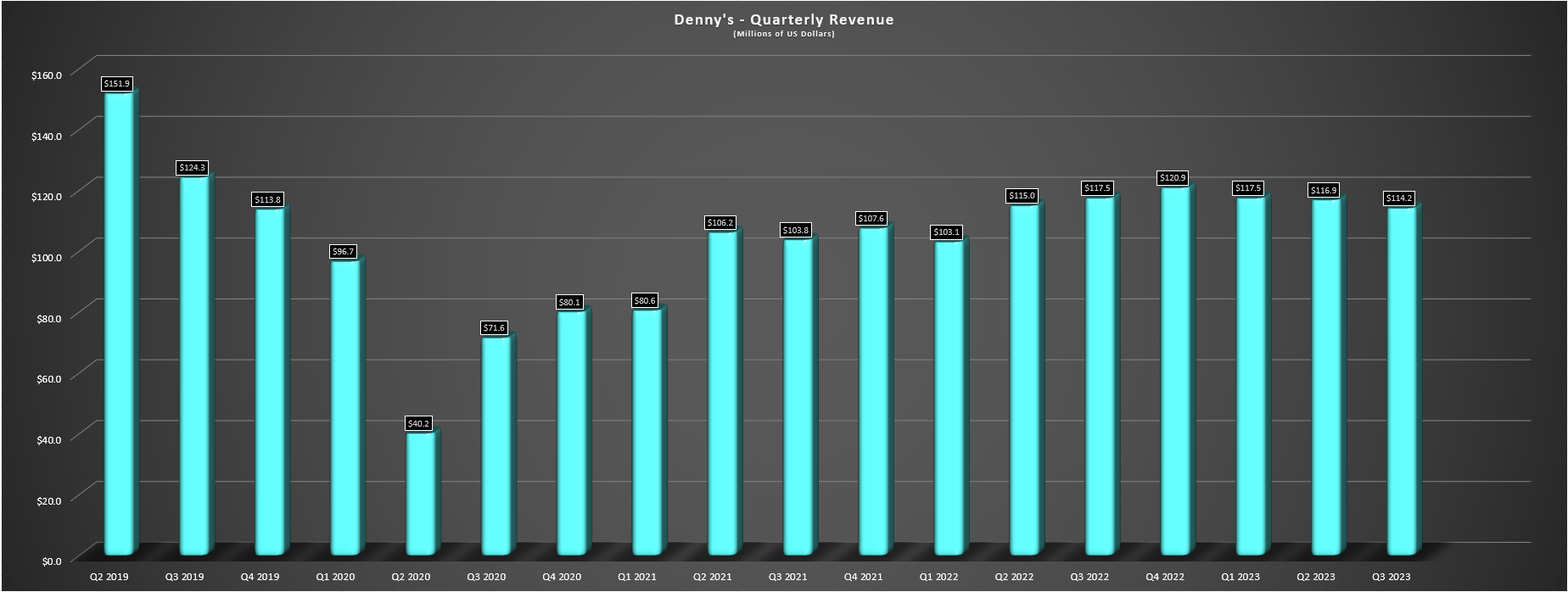

Denny’s released its Q3 results last month, reporting quarterly revenue of $114.2 million, a 3% refuse from the year-ago period. This refuse in revenue was related to lapping the kitchen modernization rollout last year which impacted franchise/license revenue ($61.0 million vs. $65.2 million), offsetting 2% growth in company restaurant sales to $53.2 million with the contribution of Keke’s Breakfast Café which was completed in Q4 of last year. Digging into the results a little closer, system-wide sales increased just 1.8% which was disappointing considering the ~8.4% pricing, while Denny’s (~96% of its system) saw same-store sales growth of 2.1% for domestic franchised restaurants and a 1.4% refuse in company-owned restaurant same-store sales. At Keke’s, the results weren’t much better, with same-store sales down 3.4% and 5.3%, respectively, for company same-store sales and franchised same-store sales, implying meaningful traffic declines.

Denny’s Quarterly Revenue – Company Filings, Author’s Chart

Moving over to margins, we fortunately saw an improvement here, with restaurant-level margins of 13.7%, up from 7.2% in the year-ago period. The margin benefits were broad-based and benefited from higher menu prices and lapping significant commodity inflation in Q3 2022, with product costs as a percentage of sales down from 27.7% to 25.6%. Meanwhile, payroll/benefits costs improved to 37.2% vs. 38.6% (though pressure will remain here with the passing of AB 1228 with ~22% of Denny’s system in California that will drive up restaurant wages, with Denny’s indirectly affected), and other operating expenses fell 250 basis points, with higher utility costs offset by lower repair/maintenance costs and lower costs for legal settlements. In addition, the company noted that it opened a new virtual brand in the period to boost sales in the dinner/late-night daypart, Banda Burrito, with early results in the evaluate market of 10 locations being positive.

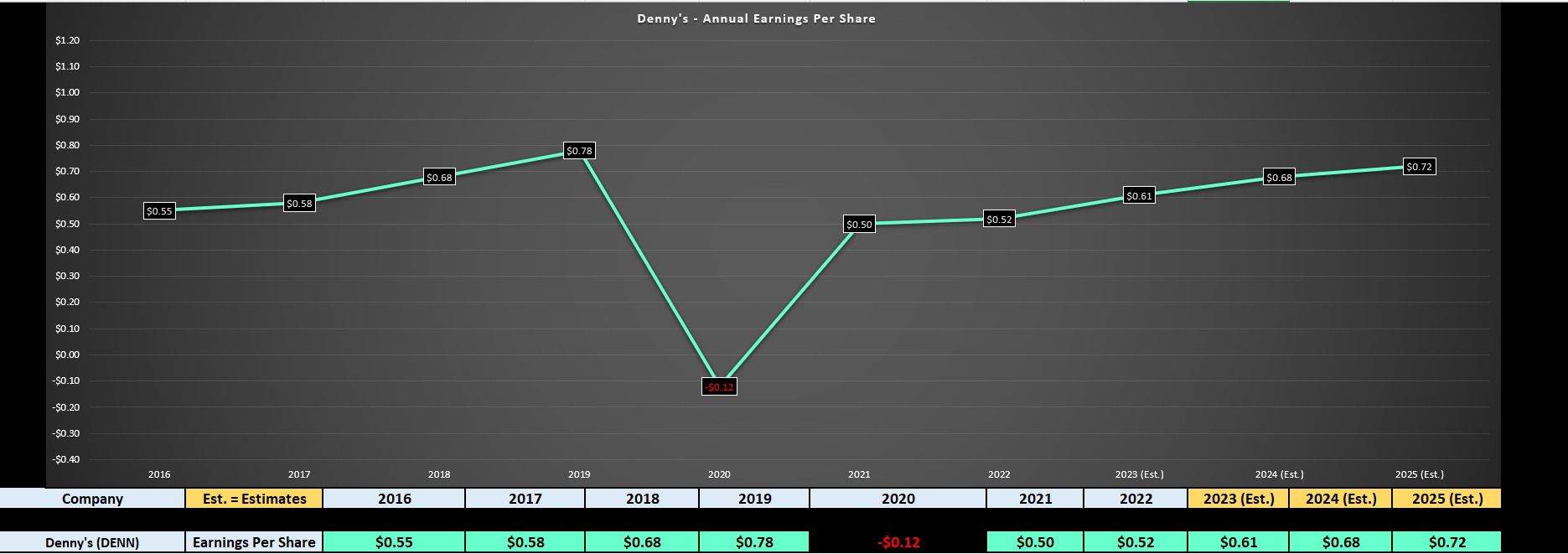

Denny’s – Earnings Trend & Forward Estimates – Company Filings, Author’s Chart, TIKR.com

As for the company’s financial results, adjusted net income increased to $9.4 million ($0.17 vs. $0.12) with higher G&A and interest expense offset by higher margins. Meanwhile, adjusted EBITDA was $22.2 million (Q3 2022: ~$19.2 million), and the company generated adjusted free cash flow of $12.0 million in the period. It’s worth noting that the company’s quarterly earnings per share growth benefited from significant share repurchases year-to-date, with ~$35 million in stock repurchased to date, and ~$16.5 million in Q3 alone at a share price of $9.70. That said, the company did guide for lower domestic same-store sales (2.75% – 3.5%) vs. its previous outlook of 3.0% – 6.0%, and also reeled in annual adjusted EBITDA to $85 to $87 million vs. $86 to $90 million previously. Finally, development delays led to fewer openings than planned, with consolidated net declines of 10–20 restaurants expected this year.

October Restaurant Sales – Black Box/Guest XM Data

Overall, the results were mediocre at best, and company commentary on traffic wasn’t great with the company noting that a slowdown began in the back half of August that continued through September with a sequential refuse into October. This was a slight divergence from other industry peers which saw a recovery in October sales, potentially explained by Florida’s brutal performance potentially caused by extreme heat (~11% of Denny’s system and the Keke’s brands is based in Florida). And this is even more disappointing considering the tailwind from lower gas prices, which has at least taken some pressure off consumers in the near-term. Let’s take a look at recent developments and industry-wide trends below:

Recent Developments & Industry-Wide Trends

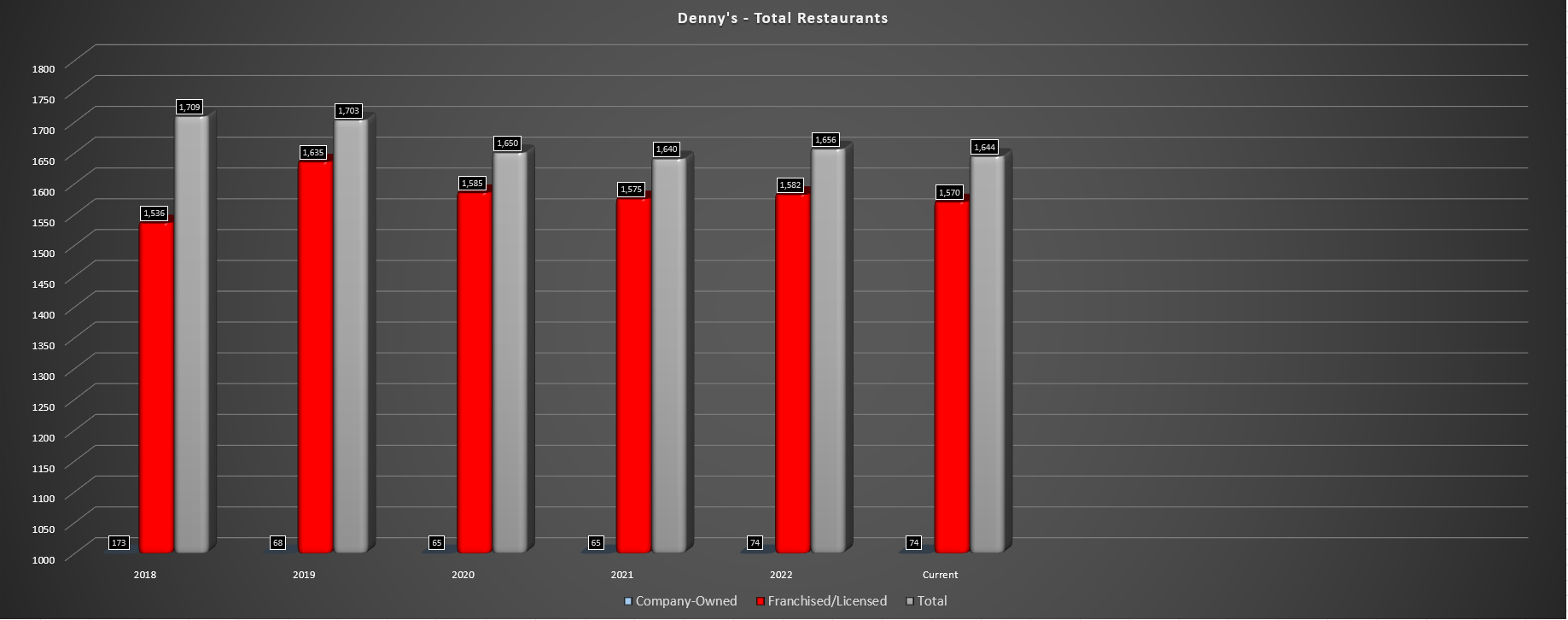

Starting with the positives, Denny’s opened one new Keke’s Cafe in Q3, has opened three year-to-date and has a development agreement for 100 new Keke’s with 14 franchisees, 11 of which are existing Denny’s franchisees. This is a massive announcement given that the 100 restaurant figure is ~60% above the current size of the system and could help offset a persistent trend of net restaurant declines for Denny’s system (shown below). In addition, while I continue to be skeptical about virtual brands as results have been mixed across different companies, Denny’s appears confident that it can drive incremental sales from its new Banda Burrito launch (in addition to Burger Den and Meltdown), with this now being rolled out across another 80 locations, with a focus on California.

Denny’s Total Restaurants – Company Filings, Author’s Chart

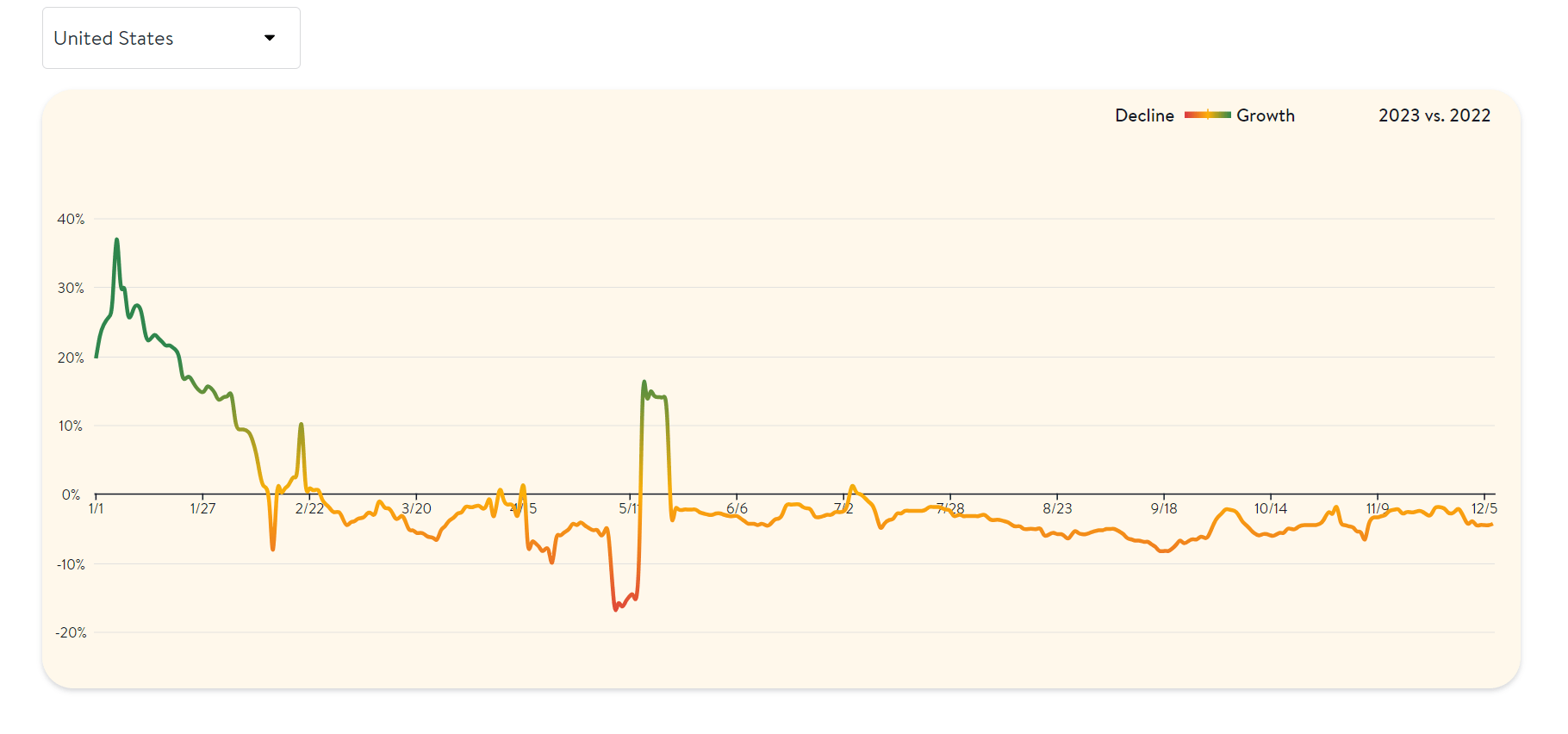

As for the negatives, industry-wide traffic has been unable to push back into positive territory for a 6+ month stretch now, with seated diners in the United States according to OpenTable data remaining negative, even if we have seen a slight recovery from the depths of Q3. This is consistent with what we’ve seen from Denny’s with negative traffic and what looks to be a encourage impact from the record temperatures in Florida. The company is working to offset the difficult environment with new menus and leaning into value with its $5.99 Grand Slam special showing positive results with a profitable traffic lift and minimal negative impact to the overall check. The company noted that this can be rolled out across other markets to help improve traffic trends, and this can hopefully supply a lift to November/December sales in what’s been a difficult environment with persistently lower traffic for the casual dining space.

United States Seated Diners Growth – OpenTable

The last positive worth noting is that despite high single-digit pricing, the company appears to be doing a good job of taking price where it can strategically as its net sentiment is outperforming peers:

“So when you look at net sentiment, we are outpacing both the casual dining players, and our family dining players in a pretty material way. So we believe that you kind of put that together, you keep your head down, you give value, you focus on breakfast, you get the right pricing strategies and while this in the very short term it may be working against us, we really see all of these things kind of coming together to look more towards a much brighter future.”

– Denny’s, Q3 2023 Conference Call

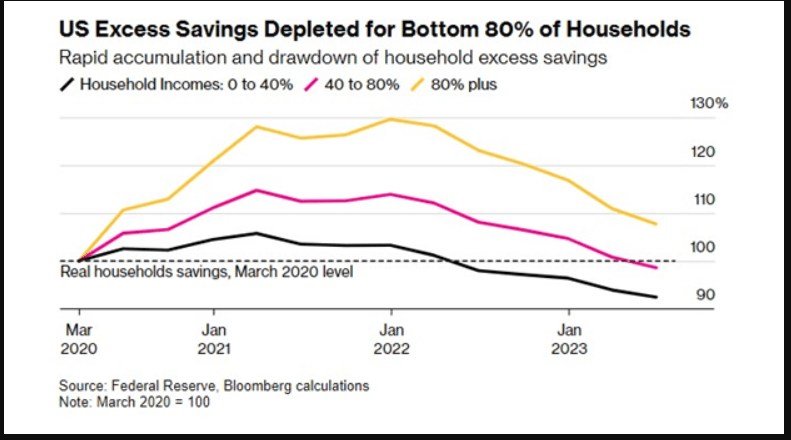

Overall, the Keke’s news is extremely positive and could help to finally return Denny’s to growth if momentum continues at this newly acquired brand. That said, the outlook for traffic growth is not great even with levers Denny has at its disposal (virtual brands, leaning into value more), especially when it seems that fewer consumers are dining out given the pinch to their wallets. It’s also worth noting that the lower gas prices last year helped to drive a recovery in traffic for all restaurant brands, but this is not occurring thus far despite a steep refuse in gas prices, suggesting that many consumers may simply be tapped out and much more judicious on how they spend. In summary, while Denny’s has done a solid job improving margins, it’s tough to be bullish on the 2024 outlook with depleting excess savings for the bottom 80% of US households, as shown below.

US Excess Savings Bottom 80% Of Households – DiversifiedTrust.com

Valuation

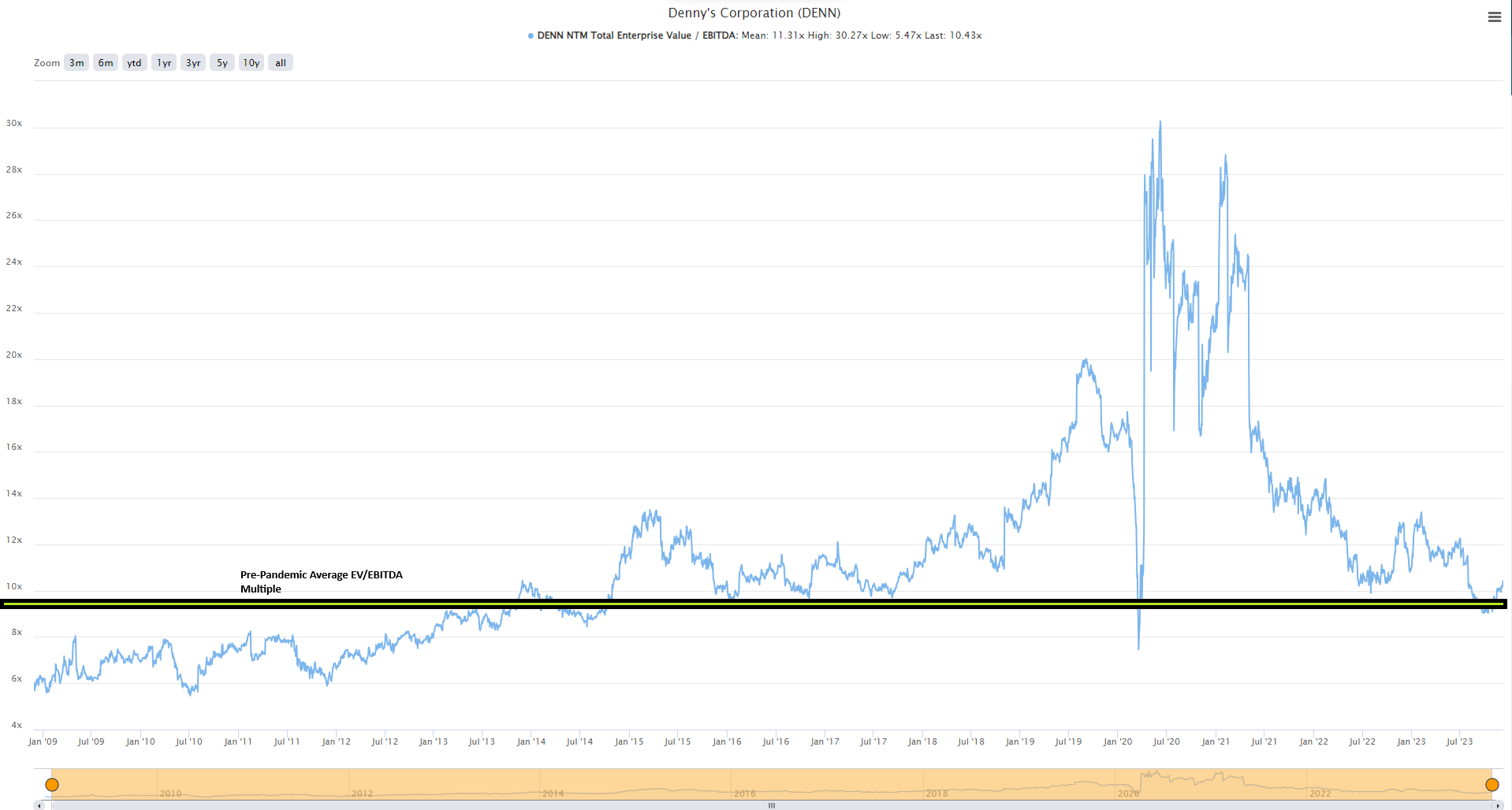

Based on ~53 million shares and a share price of $10.30, Denny’s trades at a market cap of ~$550 million and an enterprise value of ~$930 million. This makes it one of the smaller capitalization names in the restaurant industry and leaves the stock trading at approximately ~10.8x EV/EBITDA vs. the midpoint of its updated FY2023 guidance. This is a slight premium to its pre-pandemic average EV/EBITDA multiple (2010-2019) of ~10.0x, which is not expensive by any means, but not all that cheap considering the higher interest-rate environment, lower restaurant-level margins than pre-pandemic levels (Q3 2017 through Q3 2019 average of 15.8%), and a challenging macro environment.

DENN EV/EBITDA Multiple & Pre-Pandemic Average EV/EBITDA Multiple – TIKR.com

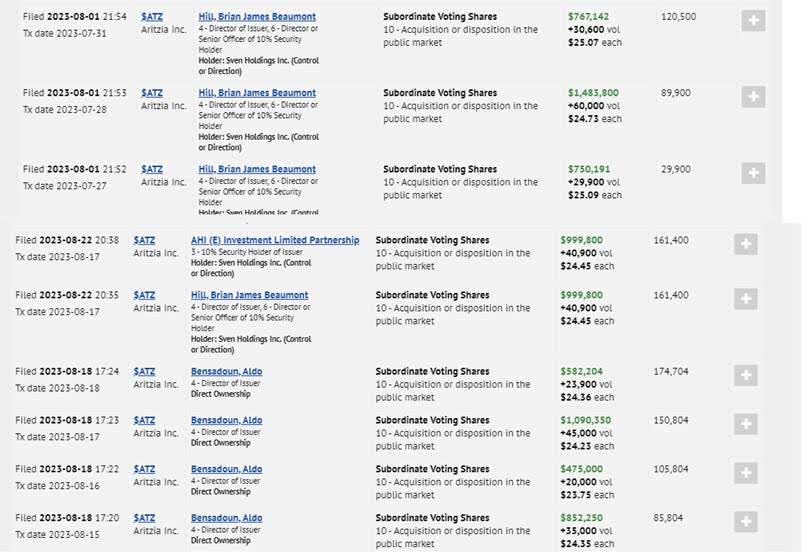

Using what I believe to be a more conservative multiple of 10.5x EV/EBITDA, estimates of $90 million in FY2024 EBITDA and ~50.5 million shares, I see a fair value for the stock of $11.05, pointing to an 8% upside from current levels after the stock’s recent rally. That said, I am looking for a minimum 30% discount to fair value to preserve starting new positions in small-cap names, translating to an ideal zone for Denny’s of $7.75 or lower. Hence, while the stock could head higher with momentum at its back, I still don’t see anywhere near enough margin of safety at current levels. And if I was going to pay a high single digit forward EV/EBITDA multiple, I would much prefer owning a high-growth name appreciate Aritzia (ATZ:CA), which has quadrupled sales since 2016 (~C$540 million to ~C$2.20 billion), is enjoying higher unit growth than Denny’s, and has seen significant insider buying over the past year.

Aritzia Insider Buying – SEDI Insider Filings

Summary

Denny’s had a mediocre Q3 report and there wasn’t much to be encouraged about from a traffic standpoint based on commentary, with October traffic not picking up from September levels appreciate some of its industry peers. That said, the new development agreement for 100 Keke’s is certainly a positive, its opportunistic share buybacks will help to enhance its annual EPS, and the inflationary environment has improved, helping to offset of the upcoming impacts from AB 1228. That said, I prefer to own growing businesses trading at a steep discount to fair value and with Denny’s still reporting net unit declines and trading in line with its historical EV/EBITDA multiple, I don’t see nearly enough margin of safety today. In summary, while the stock is not expensive and could see encourage upside momentum, I would view any rallies above US$11.65 before March as an opportunity to lighten up positions.

Q2 2024 Earnings Call Transcript")