BalkansCat/iStock Editorial via Getty Images

Introduction

De’Longhi (OTCPK:DELHF) (hereafter ‘DeLonghi for simplicity sake) is an Italian company mainly known for its household appliances. The company is over 100 years old and started out as a manufacturer of industrial components before it ventured into making household appliances using its own brands as well as other brands. The brand portfolio currently has three main brands, the De’Longhi main brand (focusing on coffee-related household items), Kenwood (which produces kitchen tools and could be seen as the European counterpart of KitchenAid) and a license on using the Braun brand name (best known for its shaving equipment).

De’Longhi Investor Relations

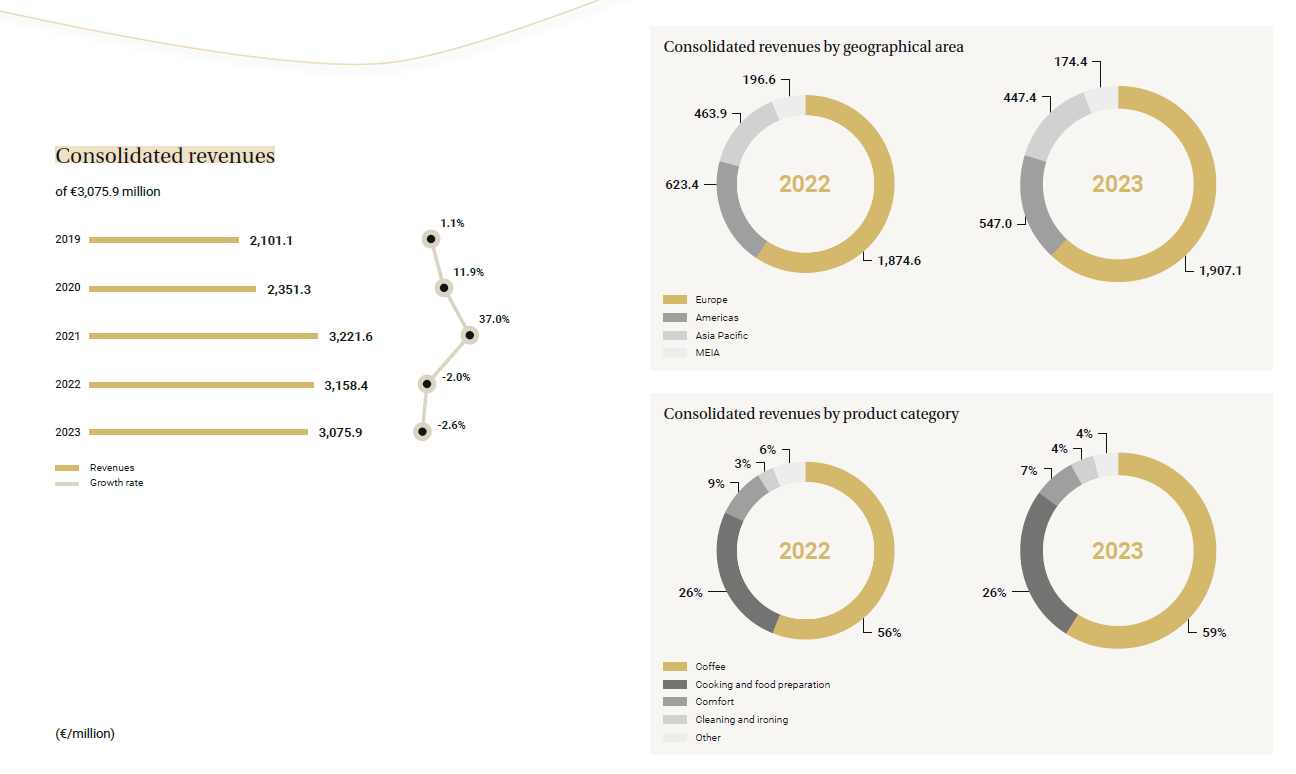

In 2023, about 62% of its total revenue was generated in Europe with the Americas being a very distant second-largest market representing just under 18% of the revenue. As the image above shows, roughly 60% of the consolidated revenue came from coffee-related appliances, while the cooking and food segment represented just over a quarter of the total revenue.

Yahoo Finance

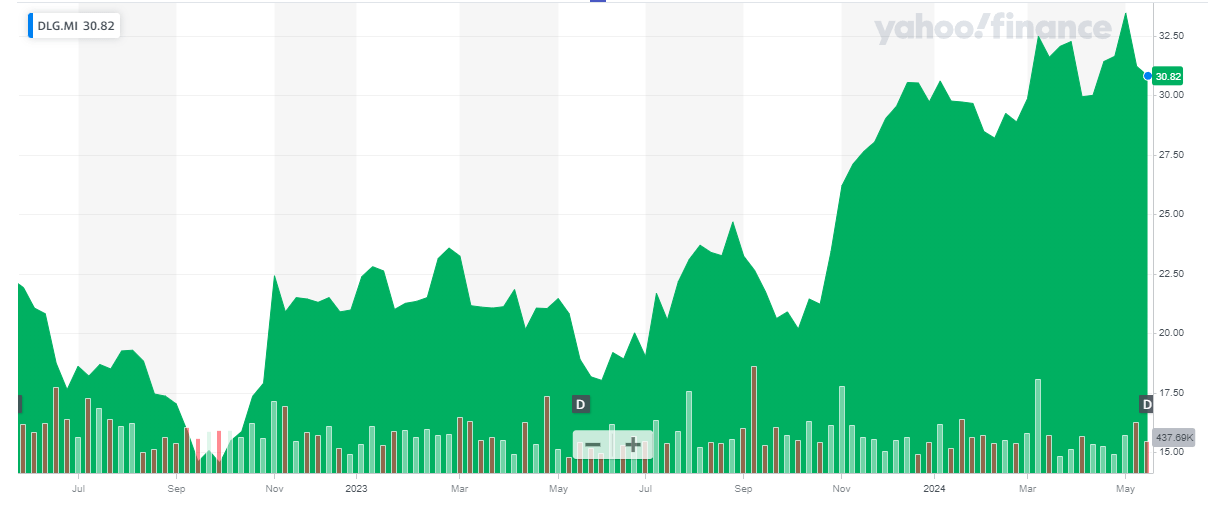

De’Longhi’s main listing is in Italy where it is listed on Euronext Milan with DLG as its ticker symbol. The average daily volume in Italy exceeds 100,000 shares, making it the preferred trading venue. There are approximately 150M shares outstanding, resulting in a market capitalization of approximately 4.6B EUR.

A 10% revenue increase in Q1 bodes well for 2024

I wasn’t quite sure what I could expect from a European producer of household appliances. Consumer confidence isn’t exactly at a very high level and the high interest rate means consumer spending definitely isn’t at its peak.

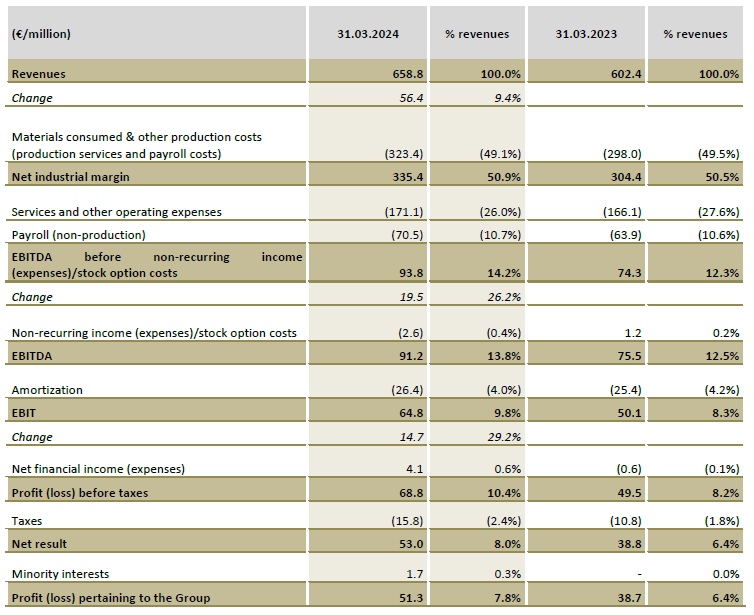

Despite that, DeLonghi announced a total revenue increase of 9.4% to almost 659M EUR. This includes a 5.9% revenue increase on a like for like basis and a 7.4% increase on a like for like basis and applying a constant currency exchange rate. The company is obviously pleased with this performance as this is the third consecutive quarter the nutrition and food preparation division shows a high single digit revenue increase. Additionally, the revenue is helped by the combination of La Marzocco and Eversys brands, and the first quarter of the financial year included just one month of consolidation, so the non-organic revenue growth will still be present in the second quarter of the year as that will be the first full quarter wherein both brands will be consolidated.

De’Longhi Investor Relations

As you can see in the income statement above, the total revenue jumped to almost 659M EUR and the net industrial margin (‘gross profit margin’) increased from 50.5% to 50.9%. Meanwhile, some of the other operating expenses decreased at a much slower pace than the revenue increase and that’s what helped the EBITDA margin, which increased from 12.3% to 14.2%. The higher margin, in combination with a higher revenue, boosted the reported EBITDA by 26% to 93.8M EUR on a recurring basis while the reported EBITDA was approximately 91.2M EUR including a 2.6M EUR non-recurring expense.

With an EBIT of 64.8M EUR and a net finance income of 4.1M (thanks to a very robust net cash position), the pre-tax income jumped to 68.8M EUR resulting in a net profit of 53M EUR of which 51.3M EUR was attributable to the shareholders of De’Longhi. There are approximately 150M shares outstanding, resulting in an EPS of 0.34 EUR.

A decent result, but unfortunately De’Longhi does not provide a detailed outlook for the current financial year. It does mention it expects a revenue increase and improving margins, but isn’t ready (yet?) to go on record with a more detailed guidance. We saw some more details in the Q1 report and the company is now aiming for an adjusted EBITDA of 500-530M EUR. The lower end of the guidance implies a 12% increase compared to the 444M EUR the company generated in FY 2023.

A look back at 2023 to provide more context

As the company only publishes condensed financial statements and financial results after the first quarter, I thought it would be a good idea to have a quick look back to the FY 2023 results, as that will help us to understand how the seasonality has an impact on the company’s financial results.

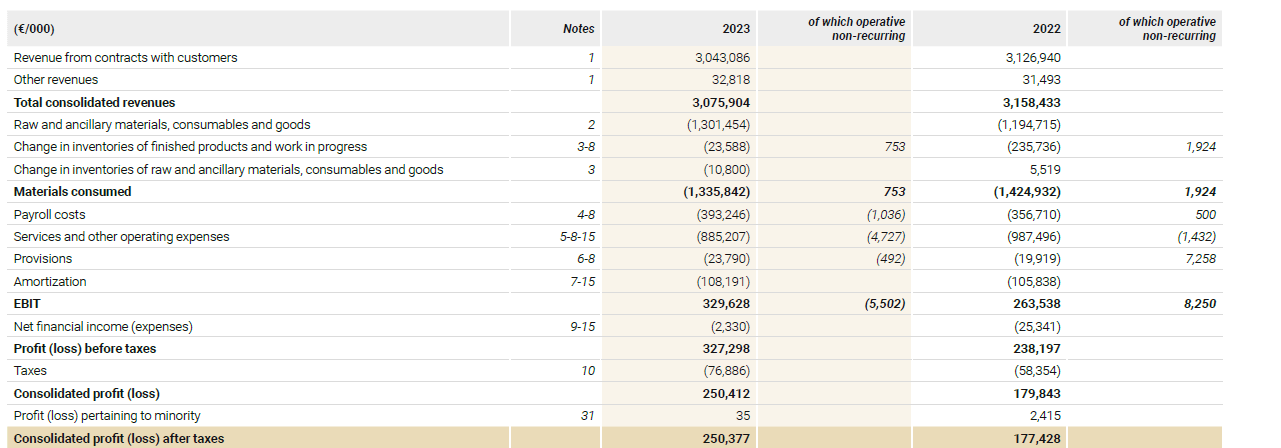

The total revenue in 2023 was approximately 3.08B EUR (which already helps to explain the seasonal effect as even in 2023 just 20% of the full-year revenue was generated in the first quarter). And as you can see below, the net income in the financial year was approximately 250M EUR, resulting in an EPS of 1.67 EUR.

De’Longhi Investor Relations

I’m more interested in De’Longhi’s ability to generate a strong free cash flow result.

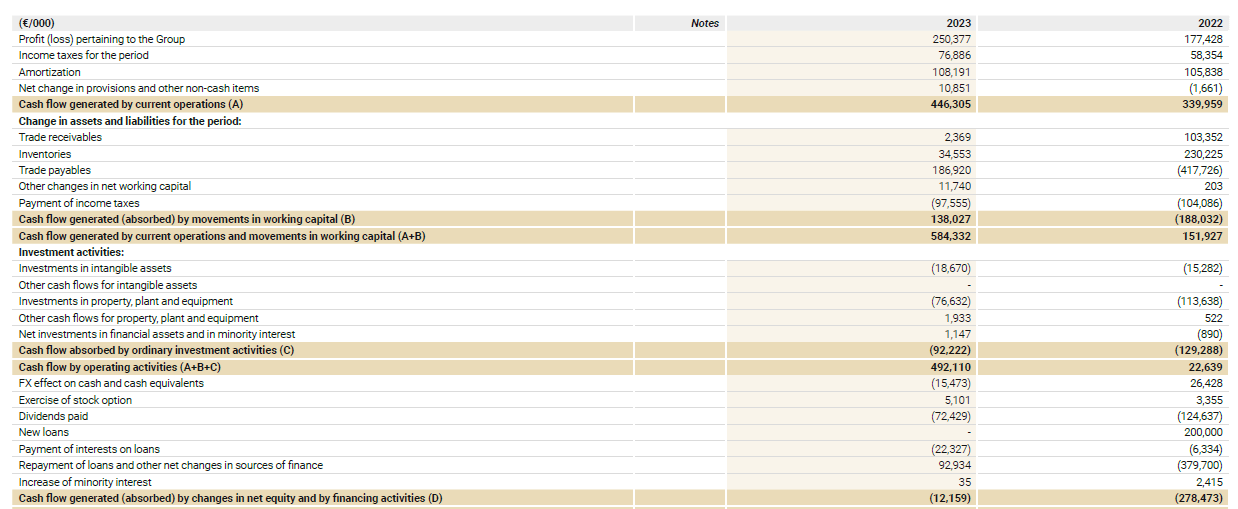

The cash flow statement below shows a total operating cash flow of 446M EUR before changes in the working capital position, but we should still deduct the 22.3M EUR in interest payments and the 77M EUR in taxes (I’m using the amount of taxes owed as per the income statement rather than the almost 100M EUR in taxes paid during the year). This results in an adjusted operating cash flow of 346.7M EUR.

De’Longhi Investor Relations

The total capex was approximately 95M EUR, resulting in an underlying free cash flow result of approximately 251.5M EUR and 230M EUR after taking lease payments into account. This represents approximately 1.53 EUR per share. Lower than the reported net income, mainly because the 116M EUR in depreciation and lease payments exceeds the 108M EUR in depreciation and amortization.

We now know the EBITDA will increase by at least 56M EUR to 500M EUR, which is the lower end of the full-year guidance. That 56M EUR will entirely trickle down to the pre-tax profit and after applying a tax rate of 24% (the average of the past two years), the net free cash flow will increase by 42M EUR or 28 cents per share to 1.81 EUR per share, keeping all other elements unchanged.

Investment thesis

Paying 30.8 EUR per share for a company that is generating 1.81 EUR per share in EPS does not sound like a very good move considering we would be paying approximately 17 times earnings. That being said, the balance sheet contains 308M EUR in net cash (and the net cash position continues to increase after a temporary acquisition-related cash outflow), which means the stock is trading at an FCF yield based on the enterprise value of 6.3%. Acceptable, but not a bargain. But that’s where the analyst consensus estimates come into the picture. The consensus EBITDA estimate for 2026 is 600M EUR, and this is anticipated to result in an EPS of 2.25 EUR per share. Meanwhile, the net cash position will increase to approximately 800M EUR again representing in excess of 15% of the current market capitalization. This means De’Longhi is currently trading at a forward EV/EBITDA of around 6.5 based on the 2026 consensus estimates. That’s in line with the 2026 guidance provided by the company.

I currently have no position in De’Longhi but I am considering writing some put options that are slightly out of the money. The P30 for September, for instance, currently trades at around 1.10 EUR per share and I think that offers an attractive risk/reward ratio. If the put option expires in the money, I would establish an initial long position at 28.90 EUR/share. And if the put option expires out of the money, I can just pocket the 1.10 EUR option premium.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")