Bloomberg/Bloomberg via Getty Images![]()

Introduction

This is the last article in my series that began three weeks ago with the analysis of Just Eat Takeaway.com and Deliveroo. Delivery Hero SE (OTCPK:DLVHF) is the last remaining European food delivery company to be analyzed, and given the similarity to the companies analyzed previously, I will avoid repeating topics already covered in depth in the other articles.

In terms of size, complexity of the organization, and expansion strategy, Delivery Hero is very comparable with Just Eat Takeaway.com, given the global scale of both companies, although they differ in some aspects. Before I start with the analysis, I would like to point out that the goal of the three articles I wrote was to delve into the business of these companies, without necessarily giving price targets, which is why I gave all three companies a neutral rating of “hold.”

Business Model

Annual Report FY22

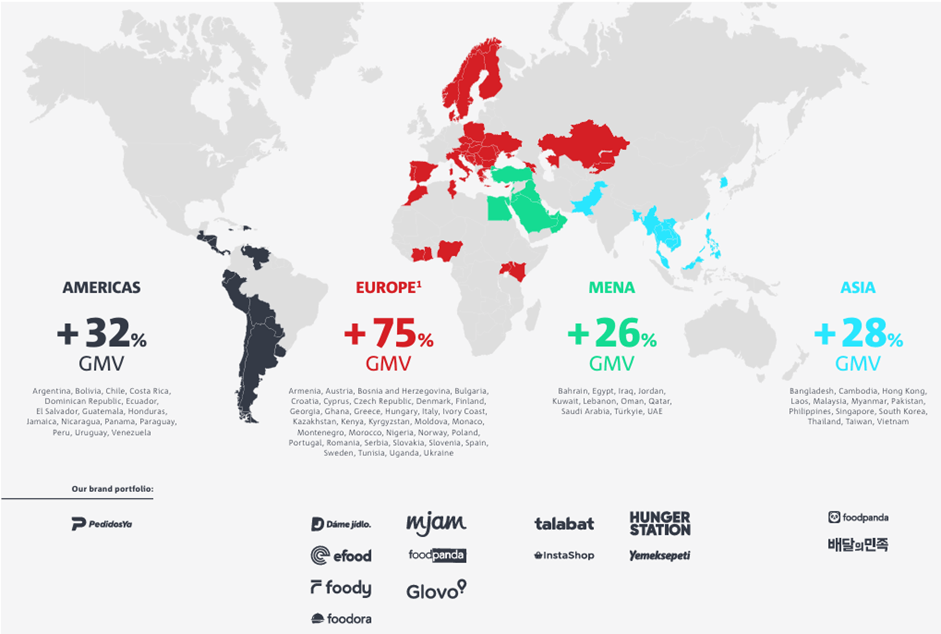

Delivery Hero offers online food ordering, quick commerce and delivery services in a variety of countries, divides its operations into four geographical segments: Asia, MENA, Europe, Americas. The company’s fifth segment is Integrated Verticals, which consists of operating company-owned warehouses (Dmarts) from which goods are delivered to the end consumer in a very short time. Unlike the other businesses that generate commission revenue on the GMV, in this case Delivery Hero sells goods directly and the revenue is recognized as GMV (Gross Merchandise Value) net of VAT.

Unlike JTKWY, Delivery Hero has decided to maintain the identity of the companies it has acquired, thus not changing their brand. This slightly differentiates the management of Delivery Hero’s business, which operates as a true holding company.

Annual Report FY22

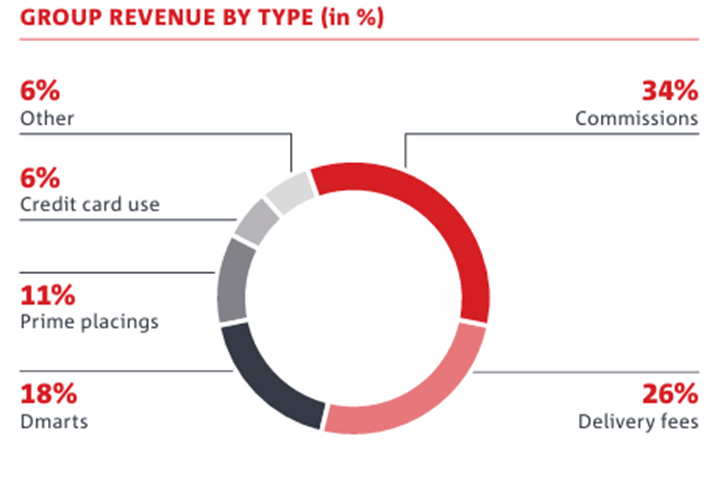

Delivery Hero generates its revenues in the same way and in roughly the same proportions as the other two companies analyzed, the most notable difference being the Integrated Verticals segment that includes the Dmart network of stores.

Annual Report FY22

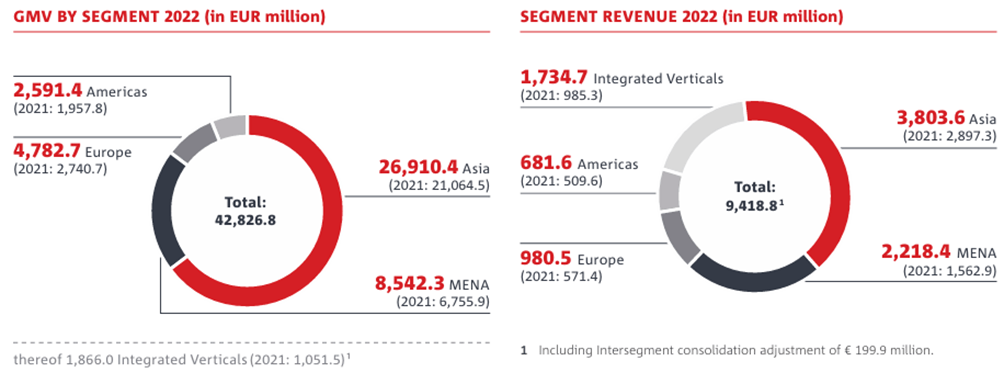

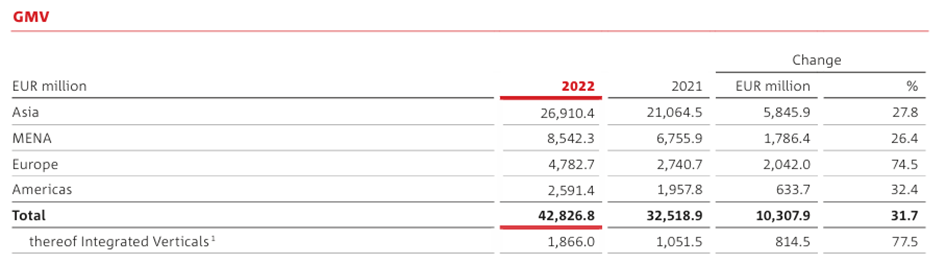

Despite being a company born and based on the European continent, Europe as a segment, accounts for just over 11% of GMV (FY22). In fact, the most important geographic area for the group is Asia, which accounts for about 63% of GMV (FY22), followed by the Middle East and Africa with 20% of GMV (FY22). While in the next section we will focus on the analysis of the different geographic areas, in this one I want to look deeper into the Integrated Verticals segment, which is the main difference between Delivery Hero and the other two companies.

Integrated Verticals

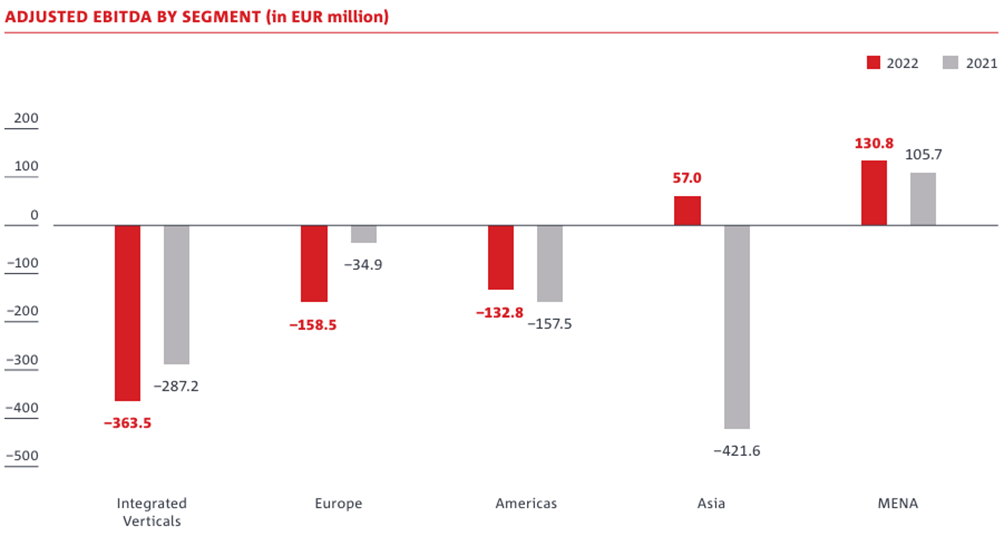

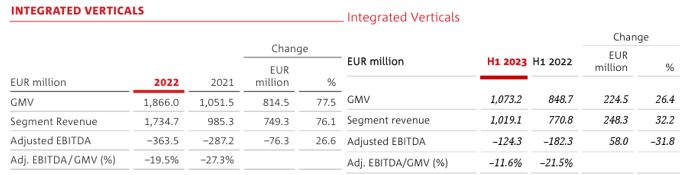

This segment consists of company-owned warehouses called Dmarts, where Delivery Hero sells products directly. To explain it in simple words, these are supermarkets from which one can buy exclusively online and which deliver products very quickly thanks to the network of couriers already operating for the company’s other business activity. The sector in which Dmart operates is called “Quick Commerce” and is seen as the next step in ecommerce, and the difference from an operational point of view is the speed with which the order is delivered. Delivery Hero is the benchmark company in this type of retailing and, starting with grocery, is expanding into other merchandise sectors as well. The company generated 1.7 billion euros in revenue in 2022 with 1,126 Dmart at the end of 2022, but it is also the worst performing segment in terms of Adjusted EBITDA.

Annual Report FY22 Annual Report FY22, Half Year Report FY23

At the end of June 2023, operating Dmarts declined to 982 stores, in the first nine months of FY23 sales were about 1.5 billion, up 11%, due to a sharp slowdown in Q3 where sales declined about 17.5%. By eliminating less profitable stores, they managed to decrease the loss in fact, in the first six months of the year the adj. EBITDA margin was -11.6%, a marked improvement from -21.5% in the previous year.

Financial Performance

TIKR

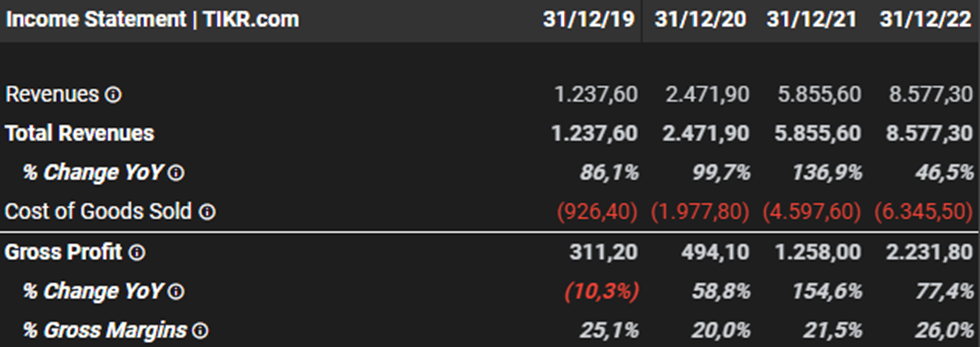

As in the case of the other two companies analyzed, revenues increased significantly, thanks to the boost given by the pandemic and the various acquisitions made. In 2022 gross margin was slightly higher than in 2019, but there was a marked improvement in the reduction of operating loss. In 2019 operating income was -51.7% while in 2022 it was -16.5%. In 2022 revenue growth was driven not only by organic growth but also by the contribution of Woowa (acquired in 2021) at 25.3% of revenue and Glovo (included in July 2022) at 5.7% of revenue. Vouchers increased in absolute terms, touching 795 million, but declined in relation to sales (12.1% in 2021, 8.6% in 2022) and GMV (2.4% in 2021, 1.9% in 2022). Woowa helped improve the group’s EBITDA, which was, however, held back by Glovo. The Adj. EBITDA margin finally improved from -2.4% in GMV to -1.1% in 2022. There were also improvements in marketing expenses; in fact, although they increased in absolute terms, exceeding 1.1 billion, their weight in relation to GMV decreased, from 4% in 2021 to 3.6% in 2022.

Annual Report FY22

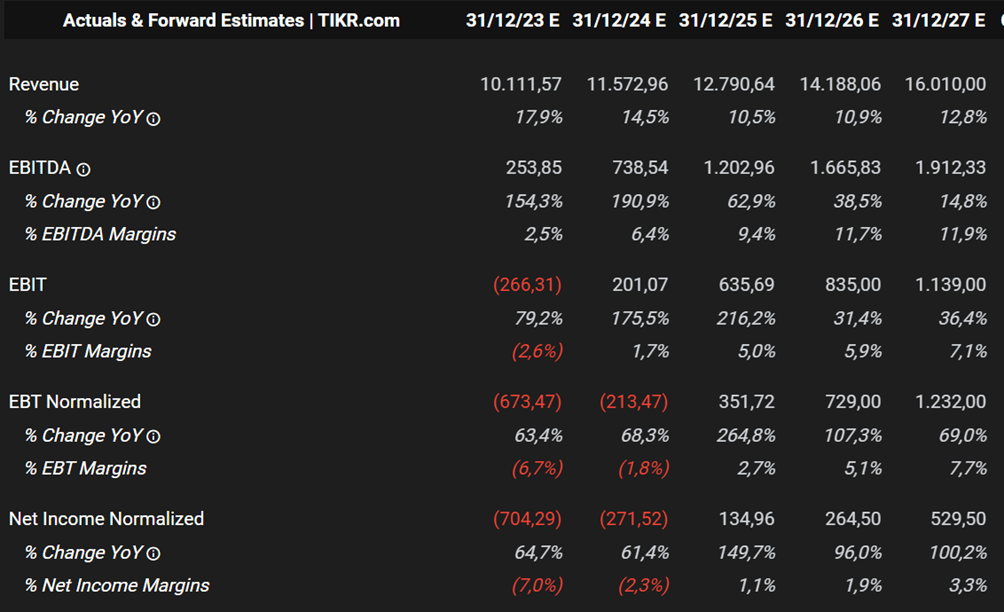

Since the data for Q4 has not yet been released, the data for the full fiscal year 2023 take into account analysts’ estimates for this last quarter. Revenues are expected to grow by 18 percent slightly exceeding 10 billion euros, positive EBITDA of 254 million (2.5 percent EBITDA margin), still negative EBIT of 266 million (6.7 percent EBIT margin), and a net loss of 700 million euros. Before going to the analysts’ future estimates, it is appropriate to dwell on past performance by analyzing each segment.

Asia

Annual Report FY22

In December 2019, Delivery Hero entered into an agreement to acquire 88.5% of the South Korean company Woowa, but it was not until February 2021 that they received approval from the Korea Fair Trade Commission (KFTC) and the transaction officially closed on March 4, 2021, with the payment of 1.6 billion euro cash and 39.6 million new shares, valued at a price of 103.35 euro, bringing the total cost of the acquisition to 5.6 billion euros. In order to approve the deal, however, the KFTC required Delivery Hero to sell the “Delivery Hero Korea” division, which was sold at the end of October 2021 for 536 million euros.

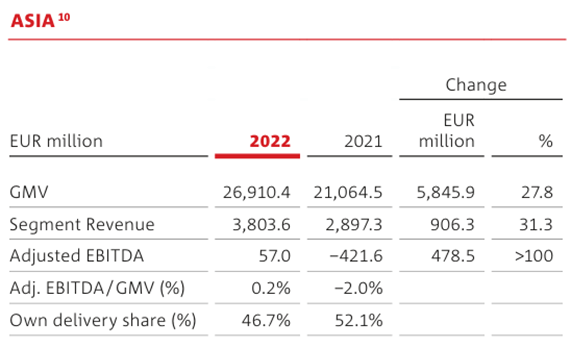

As a consequence of this acquisition, we see strong growth in GMV and sales in 2021, amounting to +304% and +142.2%, respectively (also clearly influenced by organic growth). Moreover, we can also observe a marked improvement in the Adj. EBITDA margin, which went from -8.8% in 2020 to -2% in 2021, this due to the inclusion of Woowa’s business and the exclusion of Delivery Hero Korea. Woowa is, in fact, mainly a marketplace business, thus more profitable, and has evidence of its contribution we can also consider the delivery share, which decreased from 76.8% in 2021 to 52.1% in 2021.

GMV growth in 2022 was 27.8%, boosted by the inclusion of Woowa’s business for 12 months versus 10 in the previous year; organic growth, on the other hand, was more moderate at +6.5%. This resulted in the Asia segment weighing 62.8% of the group’s GMV (2021: 64.8%). There was also a significant improvement in Adj. EBITDA, which amounted to 57 million (2021: -421.6 million), again helped by the contribution of Woowa and the divestment of the activities in Japan. There were also improvements in foodpanda’s efficiency in spending on marketing. Also in 2022, Woowa reduced delivery share by dropping it to 46.7 percent, but management said the focus is to increase delivery business in the following years.

In the first six months of 2023 GMV decreased by 5.9% caused by a normalization of order frequency, the weight of Asia on the group’s GMV decreased further to 56.7% (H1 22: 67.1%). Revenues were only -1.8%, thanks to an increase in advertising revenues that partly offset the decrease in commissions. Adj. EBITDA improved significantly, from -80.5 million to +173.7 million, aided by better performance of the delivery business, involving lower costs per order and reduced marketing expenses. In Q3, the decline in GMV and sales continued and was -6.2% and -4.2% respectively. In the major countries in which they operate in this region, they remain market leaders with significant market share with both foodpanda and Beamin (owned by Woowa).

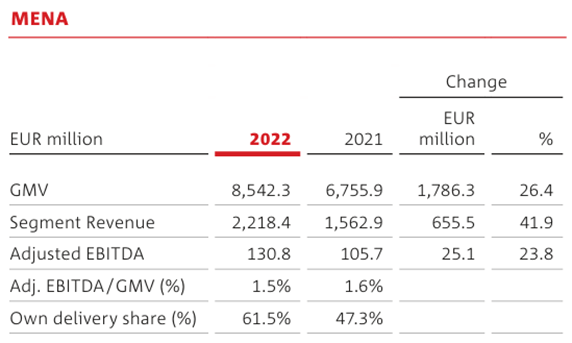

MENA

Annual Report FY22

GMV growth was achieved organically through increased use of delivery services that were supported by initiatives to increase minimum basket value and order frequency. Talabat and HungerStation continued to grow their GMV and strengthened their leadership position. The total weight of the MENA segment on the group’s GMV was 19.9 percent, down slightly from 20.7 percent in 2021. The increase in revenue was helped by the introduction of service fees in selected markets and the increased weight of non-commission-based revenue such as subscription models and advertising products. Adj. EBITDA continues to be positive, although the margin over GMV decreased slightly. A weight on the performance of this segment was the operations in Turkey due to the hyperinflationary situation that is affecting this country.

In H1 2023, organic growth in this segment continued, leading GMV to grow by 15.8% and sales by 22.7%. Excellent improvements were also achieved in terms of Adj. EBITDA, which grew 178% and reached 111.5 million, with a margin over GMV of 2.4% (H1 22: 1%). This improvement was achieved through an increase in non-commission-based revenues and an optimization of expenses in marketing. In Q3, the segment continued to grow, both in terms of GMV (+20.2%) and revenues (21.8%).

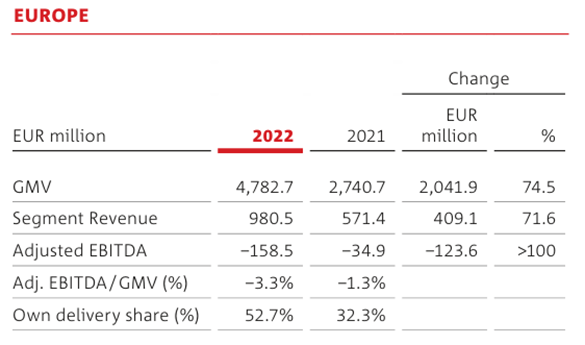

Europe

Annual Report FY22

In July 2022, Delivery Hero finalized the Glovo acquisition, acquiring 50.2% of the company for €564.8 million, part of which was paid for with 10.3 million new shares worth €394.8 million, the remainder of which involves share-based payment replacement awards of €123 million and €47 million concerning other financial instruments. Glovo’s entire business was included in the Europe segment, even though it includes operations outside Europe, such as in Africa. The increase in GMV was mainly driven by the acquisition, and starting in July 2022, Glovo’s revenues were approximately 353 million. However, the acquisition negatively affected profitability; in fact, losses increased and the Adj. EBITDA margin was -3.3% (2021: -1.3%).

In the first half of 2023, the inclusion of Glovo’s business increased GMV significantly (+160%), but organic growth was only 1.9%. Europe now has a weight of about 16.4% on the GMV of the whole group (H1 22: 7%). The inclusion of Glovo’s business worsened Adj. EBITDA, which was -98.3 million, compared to -20.3 million in the previous year. Even excluding Glovo the performance of this segment was significantly worse than that of the others, Adj. EBITDA actually decreased by -37.1 percent due to a major increase in marketing expenses. However, in Q3 GMV and revenue grew by +13.4% and +18.3% respectively.

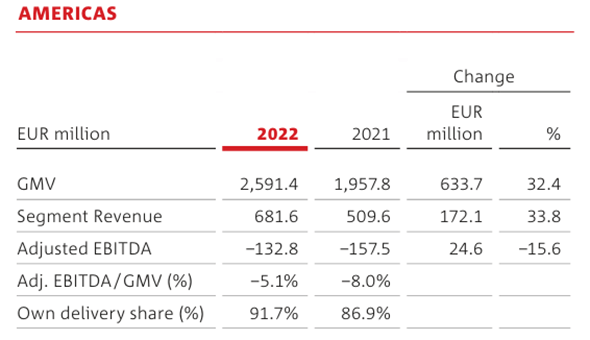

Americas

Annual Report FY22

Due to an increase in active users, order frequency, and a higher average order value, GMV in 2022 increased by a 32.4%, revenue increased in tandem thanks to advertising revenue. The improvement in order frequency and AOV also helped reduce the loss, bringing the Adj. EBITDA margin to -5.1% compared to -8% in 2021.

With the acquisition of Hugo in November 2022, Delivery Hero further consolidated its position in Central America by integrating Hugo’s operations with those of PedidosYa. The acquisition in 2022 did not greatly affect the segment’s performance. GMV further increased by 15.5% in the first quarter of 2023, thanks in part to the Hugo acquisition. An optimization of marketing expenses also enabled the improvement of Adj EBITDA, at -53.4 million (H1 22: -80 million) with an Adj. EBITDA margin of -3.7% (H1 22: -6.5%). In Q3, on the other hand, performance was stagnant in terms of both GMV and sales.

Management

From the results achieved by the different segments over the years, I believe that the management of Delivery Hero has been much better able to manage operations on a global scale than that of Just Eat Takeaway.com. While in the case of JTKWY the only segment that has managed to achieve consistent results over the years is Northern Europe, in the case of Delivery Hero, all segments have made progress over the years, both in terms of growth and profitability. Probably, greater decentralization of decision-making power and greater autonomy of the subsidiaries has improved the management’s ability to execute.

Annual Report FY22

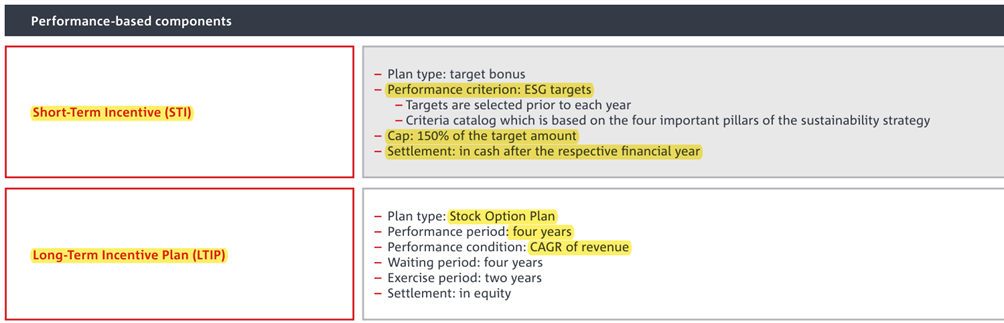

Referring to the 2022 compensation report, we can see that the focus is on revenue growth. Unlike the other two companies, we do not find targets in terms of EBITDA, and again there is a lack of incentives in terms of return on capital.

Although I still dislike expansion strategies based mainly on acquisitions, I evaluate Delivery Hero’s management more positively than JTKWY’s having been better at managing and executing M&A deals. I have some doubts regarding the Integrated Verticals segment, which covers a market that is perhaps even more competitive than food delivery and is currently the group’s weakest business, both in terms of performance and future prospects. That said, it should also be kept in mind that according to analysts’ estimates, Delivery Hero would be the first of these three companies to become profitable and generate positive cash flow. Needless to say, these estimates can be disproved at any moment.

Risks

In previous articles on Just Eat Takeaway.com and Deliveroo, I talked about the risks of this industry and the doubts I personally have about the business model of these companies. To avoid repeating myself unnecessarily and rewriting the same things, here I would like to draw attention to a risk factor that I did not talk about in the other cases. I am talking about the risk of regulation of gig workers. Many states are considering reforms to protect the rights of these workers, who are growing in number. In some states such as Italy or Spain, the status of “self-employed worker” has been challenged by the courts, and they have declared that these workers should be recognized as employees in their own right, with the duties and rights that attach to this status. If these companies were to be forced to change the contracts of their couriers, recognizing them with the rights of an employee, personnel costs would increase significantly and consequently, the cost of fulfilling each order would also increase.

A peculiar risk of Delivery Hero is the Integrated Verticals segment, currently it is the segment that is slowing down the most in achieving profitability for the entire group, but operating in an extremely competitive market there is a lot of uncertainty about the future of Dmarts as well. Last quarter’s performance was not exciting, and there is a lot of uncertainty regarding both future growth and profitability. Therefore, this segment could significantly slow the group’s growth and also reduce the valuation of the company as a whole.

Delivery Hero currently has 1.9 billion in cash and short-term investments, 285 million in short-term borrowings and 4.9 billion in long-term debt. The balance sheet situation is worse than the other two companies analyzed, and if it fails to generate positive cash flow in the coming years due to tougher-than-expected competition, they may be forced to further dilute shareholders, and even in a possible next recession the company would not be in a good situation.

Valuation

TIKR

Future growth projections are very positive, and better than both JTKWY and Deliveroo in terms of profitability. With a current market capitalization of 5.1 billion, the P/FCF multiple considering the 2027 forecast would be 5. If the company can meet analysts’ expectations, the potential performance could be very attractive, as the P/FCF multiple could be between 15 and 20. To make a comparison, DoorDash is currently the only food delivery company with positive FCF and has a P/FCF multiple of around 35. Even if we consider the EV of 8.8 billion, the opportunity still looks good, as the company could double its valuation through an expansion of multiples (assuming a forward P/FCF around 16).

However, I think these estimates are too optimistic, and do not sufficiently take into account an increase in competition, which would lead to an increase in marketing expenditures (which have been declining in recent quarters), especially in the weaker segments such as Europe and Americas. Probably the rest of the investors also believe that they are excessive as estimates, this would explain the current apparent undervaluation.

I tried to do a DCF of Delivery Hero but realized that Europe and the Integrated Verticals segment are a big uncertainty as far as profitability is concerned, even though they represent a small part of GMV. Estimating margins and cash flows for these segments is almost impossible. Given the high debt, I think the worst-case scenario is worse than the other two companies, a market slowdown could bring difficulties in generating positive cash flow and would force the company to finance itself by significantly diluting shareholders. As in the case of Just Eat Takeaway.com, I am unable to make a serious assessment of Delivery Hero. This company’s profitability history is still too short to use it to make useful estimates. The best thing to do is probably to wait and see if they will be able to reduce losses in the less profitable segments and maintain margins in the profitable ones. In recent quarters, they have been able to improve Adj. EBITDA is mostly due to a reduction in marketing expenses, but if competition were to increase in the coming years, would they be able to maintain, or increase, margins even with higher marketing expenses? I cannot answer this question with sufficient certainty, and consequently do not feel confident in making estimates.

Conclusion

This article starring Delivery Hero concluded my analysis of the European food delivery industry. I hope to have been helpful in offering a starting point for the analysis of this sector. The preconceptions I had about this sector before I began the analysis have unfortunately been confirmed. I personally find it difficult to identify a lasting competitive advantage in these companies, and the doubts I had about the profitability of this business model remain. After spending almost a month analyzing and studying this industry, in the next articles I will focus on analyzing other companies with business models that I find more interesting than this one. I do not rule out the possibility of doing an article later on DoorDash, the biggest company in food delivery and which might also help to better understand the future of these three companies.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")