Dan Kitwood

Introduction

This is the second article regarding the food delivery industry, and after talking about Just Eat Takeaway.com (OTCPK:JTKWY) it is now Deliveroo’s (OTCPK:DROOF) turn. I have already expressed in depth in the previous article many of the concepts and opinions about the industry in which these companies operate, which I invite you to catch up if you were interested. I will try to briefly resume the most relevant parts avoiding repetition, but trying to highlight the differences between these companies (this disclaimer will also apply to the third and final article regarding Delivery Hero).

Of the three companies covered in this analysis, Deliveroo is my favorite in terms of its expansion strategy. It is in fact focused exclusively on organic growth, not resorting to acquisitions to quickly attack a new market. This different strategy clearly has its strengths and weaknesses, which I will elaborate on in the course of the discussion, but in my opinion it is not the only element that distinguishes Deliveroo from the other two companies.

Business Model

Deliveroo generates its revenue mainly from commissions generated from Gross Transaction Value (GTV), paid by partners and consumers. In addition to these, it also receives online payment processing fees. Residually we find the revenue generated from advertising, amounting to 0.6 percent of GTV in 2022, and a subscription service that offers the advantage of not paying delivery fees for orders above the minimum spend (Deliveroo Plus). There is currently a partnership with Amazon to offer Deliveroo Plus to Amazon Prime members for one year, in my opinion a great way to advertise and build customer loyalty, however, it will be to be seen how many people will continue to pay for this subscription after the promotion ends.

The company divides its operations into two segments: UK & Ireland (UKI) and International. UKI in FY23 accounted for 59.2 percent of GTV, 59.5 percent of sales, and 58.4 percent of orders. Compared to the other two companies in this comparison, Deliveroo operates in far fewer countries, the International segment in fact includes: France, Belgium, Italy, Singapore, Hong Kong, the United Arab Emirates, Kuwait and Qatar. In recent years, management made the decision to exit several markets, such as Australia, the Netherlands, and Spain, because it believed it had no chance of achieving dominance in an economically viable way.

Deliveroo’s strategy is to focus on cities and consequently on countries where they are market leaders, or believe they are likely to be market leaders in the future. We can call this a “bottom-up” strategy, focused on winning relevant market share in cities or areas that offer higher profitability, and then eventually aiming for national leadership. It is exactly opposite to the strategy adopted by Just Eat Takeaway.com and Delivery Hero, which aim to acquire companies with good national leadership to quickly enter new markets.

Annual Report FY21-22 and Q4 Trading Update FY23

2021 was the best period for these companies, having received a strong boost from the lockdown. Orders declined less than JTKWY’s seen in the previous article, in fact compared to the highs of 2021, Deliveroo saw a decrease in orders of about 3.6%, significantly less than JTKWY’s -19%. In terms of Monthly Active Consumers, the decrease was also slight (-5.3%), but it is excellent to observe an increase in Average Order Frequency and Average Basket Value. These data may indicate to us that although they have fewer active users than in 2021, those remaining are more “loyal”, use the platform more and spend more within it.

In the next section we will analyze the two business segments separately and compare them with the performance of other companies.

Financial Performance

TIKR

The image shows revenue trends from FY19 to FY22. In the latest Trading Update, the company reported that annual revenue for FY23 will be £2.03 billion, up 2.8%.

Q4 Trading Update

Although the company has not yet recorded a positive profit, it has been able to increase Gross and Operating Margin, thereby reducing losses due to the economies of scale achieved. Indeed, Gross Margin went from being 24.4 percent in 2019 to 32.6 percent in 2022, while Operating Margin from a -41.4 percent in 2019 to -8.9 percent in 2022. For fiscal 2023 the company expects a positive Adjusted EBITDA, slightly higher than the guidance given which estimated it to be between £60-80 million, a very good improvement over the previous year’s loss. It still expects an operating loss around £100 million.

UK & Ireland:

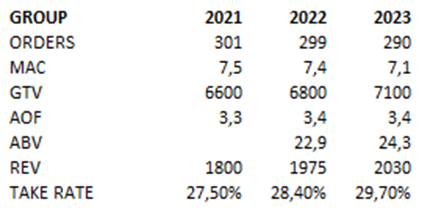

Resuming the comparison made in the previous article, we can compare the performance of Deliveroo’s UKI segment with that of Just Eat Takeaway.com, keeping in mind that the third company covered by this analysis (Delivery Hero) does not operate in this area.(All values are reported in millions with the exception of ABV)

Deliveroo’s Annual Report FY21-22 and JTKWY’s Annual Report FY21-22

Starting with the most easily comparable metric, the number of orders, we can see how, in the case of Deliveroo these have increased slightly since 2021, as opposed to JTKWY, which sees them decreasing by nearly 15 percent from their 2021 peak. We can also see an outperformance of Deliveroo in terms of GTV growth. In fact, JTKWY’s GTV in this segment is equal to that of 2021, as opposed to Deliveroo’s GTV, which is up 17 percent. Deliveroo’s volumes still remain lower than JTKWY’s as GTV in FY23 was about €4.8 billion, compared to JTKWY’s €6.6 billion (using an average gbp/eur exchange rate of €1.1492). Although smaller, Deliveroo seems to have achieved economies of scale sooner, perhaps favored by a higher frequency of purchases and a higher ABV (30.22 euros vs. 26.95 euros). Consequently, this leads to a better and especially positive Adj. EBITDA. Another competitor of Deliveroo in the UK is definitely Uber Eats and according to some old statistics, the two companies should have a very similar market share, unfortunately it is difficult to isolate the results of Uber Eats for this geographic region.

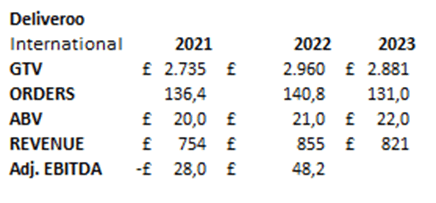

International:

This segment includes eight different states: France, Belgium, Italy, Singapore, Hong Kong, the United Arab Emirates, Kuwait and Qatar. Finding information for each of these particular markets is very difficult, but in most of them Deliveroo has a good market share and in some it has managed to increase it over the years. Performance in this segment is weaker than in UKI.

Annual Report FY21-22 and Q4 Trading Update

As can be seen from the numbers in the table, the performance of this segment was worse than in UKI, partly due to a lower uptake of this kind of service in southern European countries than in the UK.

Food delivery market share, Italy (Measurable AI, Linkedin) Food delivery market share, Hong Kong (Measurable AI, Linkedin)

Hong Kong is probably the most promising market within the International segment.

Having decided to operate exclusively in markets where it has a good chance of becoming, or remaining, among the market leaders, in my view profitability in this segment is much closer and “more predictable” than in JTKWY’s secondary segments (the others outside Northern Europe). This consequently makes results at the group level less uncertain. Clearly, “less uncertain” does not mean easily predictable. The market is constantly evolving and since there is no switching cost (for both partners and consumers) market shares can easily change, either in Deliveroo’s favor or against it.

Management

In the previous article, I was extremely critical of JTKWY’s management because of its M&A management and its ability to execute. In this case, however, I am more supportive of the decisions made by CEO Will Shu and his team, although I do not understand the rationale behind some of the decisions.

The expansion strategy more focused on organic growth rather than M&A fits well with my investment strategy and what I personally would like to see from a company’s management. In my view, it also demonstrates a greater ability to execute and manage deals outside the core market.

On the negative side, I personally do not understand the reason for buybacks at this stage of growth for the company. In fact, at the end of October the company announced its intention to buy back £250 million of its own shares. In my opinion, the company at this time should focus all financial resources on improving its business and winning market share, and not on returning capital to shareholders. Also because, since it has never recorded a positive profit or fcf, it is using capital raised from shareholders to carry out this operation. Shareholder compensation policies should come only after the company has been able to generate value for several years, not before. This concept can be found expressed very clearly in any basic corporate finance book, but I have the feeling that CEOs today are thinking more about the stock price rather than the welfare of the company. This criticism obviously also applies to the management of JTKWY, which has equally announced a plan of buybacks.

As for the remuneration report, on the other hand, bonuses obtainable by management are linked to growth in GTV and Adjusted EBITDA. Again, as in that of JTKWY, there are no targets in terms of return on capital, but at least stock performance is excluded.

Risks

Unlike my usual, this time I decided to put the paragraph on risks before the one on valuation, to make it even clearer how difficult it is to evaluate a company in this industry. Indeed, the uncertainty is very high, and any attempt at assessment, no matter how accurate, will almost certainly be wrong.

One of the main risks, concerns the food delivery industry in its entirety. In the last article, I stated that it is a market that is highly dependent on economies of scale and is predisposed to the creation of oligopoly or monopoly situations, where the companies that are able to operate profitably and continuously in a given market will be the largest ones making it difficult for smaller competitors to compete. However, the fact remains that switching costs, both for partners and consumers, are very low if not absent, and it has been seen in the past how particularly aggressive marketing policies, can easily shift market share among the various leaders in a given area. Indeed, if one takes into account the two or three largest companies in a market, the difference in service level, thus in terms of number of restaurants and speed of delivery, is practically absent, making it difficult to identify companies with lasting competitive advantages.

It is very likely that the food delivery market will continue to grow in the coming years, and also that the current leaders will be the ones to benefit most from this growth. But in a market where service delivery is a “commodity,” how can we be sure that the company we have invested in will be able to maintain its market share?

This condition makes the future of these companies very uncertain and consequently also makes it difficult, if not impossible, to evaluate companies in this industry. Clearly, the difficulty in identifying a competitive advantage may be my own limitation due to not fully understanding this industry. I invite you to write your opinion about it, in case you feel that I am missing something important.

Valuation

In the previous paragraph I made all the necessary assumptions about the valuation of these companies, so without repeating myself unnecessarily, I will try to make some estimates about the future of Deliveroo. Unlike my usual, I will not use a DCF but will try to figure out what EBIT this company can generate in five years’ time. The fundamentals of this industry in my opinion are too unpredictable to make estimates with a longer time horizon.

According to Statista’s forecast, the food delivery market in the UK will grow at a rate of 8.5 percent CAGR, from 2024 to 2028. For the same time period, the European market is forecast to grow at a 9.5 percent CAGR.

TIKR

Analysts’ estimates seem to me to be very optimistic, especially regarding EBITDA. The current target of many companies in the industry is to achieve an Adj. EBITDA margin of 5 percent vs. GTV. JTKWY in 2022 in the Northern Europe segment, where it is the undisputed market leader, achieved an Adj. EBITDA margin of around 4.2 percent. To achieve an EBITDA of £330 million in 2027, assuming Deliveroo’s GTV grows like the industry, would imply an Adj. EBITDA margin around 11-12%. In my opinion, these margin forecasts are overly optimistic. If one takes these estimates as a reference, the company would not seem overvalued, considering a capitalization around £1.8 billion. If we make more conservative estimates in terms of margins we notice a radical change.

Assuming that the GTV in the UKI segment grows like the market (8.5% CAGR to 2028) in the International segment I assume growth equal to that of the European market for the first two years (9.5% to 2025) and slightly lower in the following three years (8.5% to 2028). This would lead the company to have a total GTV of £10.7 billion in 2028.

Author’s estimate

Assuming a constant take rate we observe that revenue is consistent with that predicted by analysts, also for depreciation and amortization I used their estimates, while I reduced the Adj. EBITDA margin. As you can see, the results are radically different, in this case Deliveroo would only achieve positive EBIT in 2027. Assuming an Adj. EBITDA margin of 6 percent in 2028, possibly boosted by higher high-margin advertising revenue, EBIT in 2028 would be roughly £51 million. These more pessimistic forecasts clearly make the current valuation of £1.8 billion less attractive.

As mentioned in the previous paragraph, competition in this area will remain high in the future, even though there may be fewer companies in the same geographic area. In my opinion, therefore, expenses in marketing will always have to be high, and there may also be price competition (on the fees charged to partners or consumers) from companies with the largest sales volumes. These factors weigh heavily on a company’s margins, which is why I find the analysts’ forecasts overly optimistic.

Conclusion

We have reached the conclusion of the second article of three on the food delivery market. Wanting to make a comparison between Deliveroo and Just Eat Takeaway.com (covered in the previous article), I personally prefer Deliveroo’s business model and management, which is much more focused on organic growth and better able to effectively execute its strategy.

The main concerns are the same as in the previous analysis, and are related to the sector in which these companies operate. It is worth repeating that the food delivery sector is extremely competitive, and even if it predisposes the creation of local oligopoly situations, switching costs are zero, and since there are no particular differences between the services offered by these companies, the creation of a lasting competitive advantage is difficult.

I hope this article has been helpful in learning more about this industry and putting into perspective what was said in the Just Eat Takeaway.com article. In the coming weeks, I will publish the last article in this series on Delivery Hero to complete the analysis of the three main companies in this industry based in Europe.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")