gaffera

Xtrackers MSCI Japan Hedged Equity ETF (NYSEARCA:DBJP) is a Yen-hedged value-weighted ETF following the most representative possible index of the Japanese market. There are myriad reasons to be bullish on Japanese equities, where in our coverage Japan remains the most overweight market. However, there are a lot of outstanding questions about the Yen and speculation around the BoJ pivot that will affect how you play the market. Importantly, data has just been released concerning the shunto and union wage pushes in Japan, that have come in at quite high figures, enough to bring real wages up more pronouncedly. Our last coverage was focused on the USD, where we were considering that the Fed had signaled its economic concerns. We consolidated that thinking recently by noticing how maturity walls may have an important effect on increasing transmission of Fed policy, which could change the dynamics. Now we want to talk about what’s going on in Japan.

We are still rather unperturbed by the shunto wage negotiation data, as our thinking that this money will be saved is the same as before and the rationale for the pivot won’t materialise as markets expect. That is what happened last time and may be a gutshot, but there are so many funds that are short the Yen in carry trades that we think it can’t possibly go lower, even without appetite from the BoJ to do stabilising Yen buying if the Yen were to test limits. While DBJP still exposes investors to upside on Japanese markets, we feel there’s no reason to not also take on the Yen with an unhedged ETF to make that possibly upside as well. Although, at some point an appreciation of the Yen would become a problem for the performance of the Japanese market.

DBJP Breakdown

Expense ratios are 0.45%. Because the Yen is being hedged, and that has a cost, this ratio is higher than on straight Japan index buys. This is another reason to look for reasons to not be hedged.

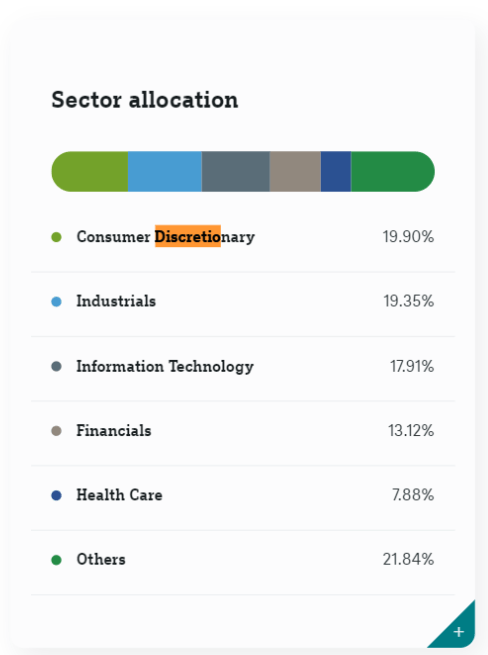

In terms of weightings in DBJP, they are indeed value-weighted according to market caps. Lots of consumer discretionary exposures due to the large car companies in Japan, and also a lot of equipment manufacturers in Japan, including automotive parts manufacturers. Then a substantial IT exposure and financial exposure as well.

Sectors DBJP (etf.dws.com)

A weaker Yen helps a lot of the consumer discretionary exposures because they have such large US and ex-Japan markets, thinking particularly about cars. Also, they are vertically integrated in Japan, and therefore pay for a lot of the services and goods which make their cars in Yen. The same arguments generally go for industrials.

Financials have not been benefiting from the current Yen situation at all. While other developed market financial exposures have been seeing major NI growth thanks to higher rates, there’s none of that in Japan. Moreover, insurance reserve portfolios aren’t benefiting from yield on fixed income and low risk instruments either due to low prevailing rates.

The other exposures have quite a lot yen denominated business, and would probably not suffer on a higher Yen in terms of stock prices, which means foreign investors would benefit from holding these Yen denominated issues.

On balance, a much stronger Yen isn’t very good for Japanese markets because it has fundamental impacts on the average Japanese listed business, which is even more reasons to be a little wary of DBJP because you may see the market react negatively without even getting the consolation of FX gains. We maintain that there still is a lot of potential for the broad markets, as PEs in Japan remain pretty low with the index at around 14x which is lower than many other developed markets, and that there is a lot of outstanding corporate governance reform outstanding that we detail here.

On the Yen

So what might actually happen with the Yen? A lot of headlines and commentators think that now is the time that rates will come up. But does the data permit it?

Firstly, we note the pretty major news that Japan’s largest labour union federation called Rengo reported that their demands were 5.85% in wage increases. That’s a lot, and a lot more than even the demands last year at 4.49%. Even if their demands aren’t fully met, that’s going to be a major inflation push from wages, which is something that Japan wants.

As an aside, Japan actually wants inflation. Not supply-side inflation which is always bad, but a benign inflation that is underlying in other economies but hasn’t been present in Japan’s stagnant economy. Wage inflation is particularly welcome because the BoJ hopes that higher wages will start virtuously cycling into spending. That absolutely didn’t happen last year. Higher wages came but consumption fell severely enough where even the growth in export surplus helped by the weak Yen wasn’t enough to stop a technical recession. In other words, there was a higher marginal propensity to save. We talked about that last time in our DBJP coverage. If that happens again it would be one less reason for the BoJ to shift its stance to a less accommodative one.

On the actual inflation data that we’ve lately seen, there is evidence pointing towards the possibility that a less accommodative stance is coming. Inflation continues to tick down, which is actually not necessarily what the BoJ wants, but it’s doing so slower than expected, with predicted inflation being lower. The slower disinflation that expected is bullish for the Yen as this is slight evidence that things may be firming up. Ueda also made statements to the affect that he also believes data points to that happening.

Firming inflation is good because it would allow the BoJ to make some space away from the interest rate floor. The combination of low rates and the possibility of consumers hoarding cash pushes things towards a liquidity trap situation which is a vulnerable position to be in, and also not good for the Yen, whose low levels has been putting pressure on consumers, even if it’s good for the export-oriented listed market.

Another reason why the Yen might rise is of course what might happen with the USD, but related to that is that the short of the Yen is a very crowded trade, since it’s been on the short end of a lot of currency pair trades for a couple of years now, with those bets only growing. Any sustained factors that might support the Yen will cause those leveraged trades to substantially unwind.

Bottom Line

We are still overweight Japan, and are especially overweight select Japanese stocks. But we acknowledge that appreciation of the Yen won’t be a positive thing for Japan’s listed giants. There could easily be a longer period of accommodation than the market expects, but the Yen is already pushed so low than any major downward moves seems unlikely at this point, so we wouldn’t be concerned about decline. In the case where the Yen increases, DBJP will face the double whammy of markets possibly not liking that development for Japanese stocks, as well as the Yen hedge losing value. For investors who want to stay long Japanese markets, we think dropping the Yen hedge makes sense as a slight adjustment from here by moving into an unhedged ETF. We’d also go further and consider getting out of Japanese large caps, which have already done very well. While they are still defensible in terms of their valuations, which are often quite compressed and offer a margin of safety, a more select approach of Japanese stocks that will not suffer on a lower Yen and are also cheap, perhaps with scope for benefits from governance reform, makes even more sense.

Q2 2024 Earnings Call Transcript")