Charday Penn/E+ via Getty Images

It has been over 4 years since my last CRISPR Therapeutics (NASDAQ:CRSP) article when I was hesitant about gathering a heavy CRSP position due to the ticker’s premium valuation, volatility, and the company’s young pipeline. Yet, I was optimistic about the company’s prospects of their expansive pipeline, and partnerships. Despite my concerns, I decided to initiate a long-term investment to gain exposure to the gene editing industry and benefit from an early entry ahead of numerous catalysts slated over the next several years. At that time, CRSP was around the $40 per share level, and I have enjoyed following the price movements and catalysts to secure profits from a volatile ticker. Eventually, my CRSP position obtained a “House Money” status and I ceased all transactions as the ticker remained above my Buy Threshold. Now that CRISPR has an approved product and has some potent catalysts on the docket, I am forced to modify my plans for my dormant position and reassess my bull thesis.

I intend to provide a brief background on CRISPR Therapeutics and its recent performance. Then, I will review some of the company’s upcoming catalysts and will discuss how they could validate my bull thesis earlier than projected. Finally, I reveal how these catalysts could radically change my CRSP strategy.

Recap On CRISPR Therapeutics

CRISPR Therapeutics is at the razor’s edge of life science, supported by strategic partnerships and a pedigree of R&D excellence. The company’s core technology, CRISPR/Cas9 gene editing, allows for precise modification of genetic material, containing immense potential for the treatment of a plethora of genetic diseases. With a robust pipeline covering numerous therapeutic areas, including oncology, hematology, autoimmune disorders, and cardiovascular diseases, CRISPR parades a differentiated portfolio of transformative therapies than reset the treatment paradigm.

One of CRISPR’s most notable accomplishments is the approval of CASGEVY (autologous CD34+ cells encoding the β-globin gene) for transfusion-dependent β-thalassemia (TDT) and sickle cell disease (SCD). This milestone approval makes CASGEVY the first CRISPR-based medicine approved by the FDA, signifying a reset in the standards of how providers can treat SCD and TDT. Developed with Vertex Pharmaceuticals (VRTX), CASGEVY offers a theoretically curative treatment for TDT and SCD, which not only provides hope for patients, but could be an attractive alternative for both providers and payers.

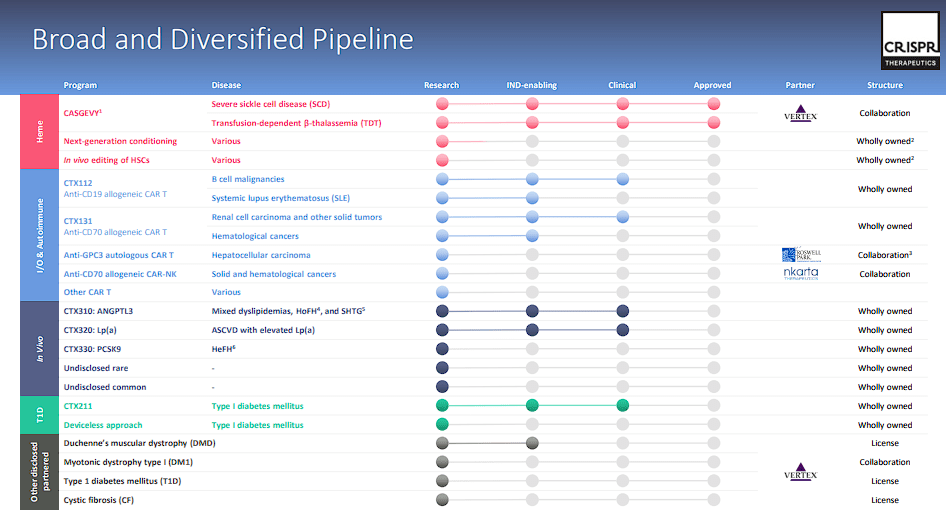

In addition to CASGEVY, CRISPR has a multitude of pipeline programs aiming at a variety of disciplines and indications.

CRISPR Therapeutics Pipeline (CRISPR Therapeutics)

Leveraging internal GMP manufacturing capabilities, CRISPR is advancing multiple next-generation gene-edited allogeneic CAR T candidates in the fields of Immuno-Oncology and Autoimmune diseases. The company maintains a commitment to continuous innovation across multiple next-generation technologies, driving progress in therapeutic development. Notably, it is spearheading efforts to address diabetes without chronic immunosuppression through stem cell-derived beta cells. With a focus on both rare and common diseases, the company has commenced clinical programs targeting cardiovascular disease.

Financials

In terms of financial performance, CRISPR beat the Street’s Q4 EPS estimates by roughly $1.33 per share with a net income of $98.1M versus a net loss of $104M ion Q4 of 2022. CRISPR received partnership revenue from Vertex for license agreements and related milestones. In addition, the company reported a drop in both R&D and SG&A expenses due to a reduction in external costs. The company’s financial position remains healthy, reinforced by a recent $280M registered direct offering, bringing its cash position to over $2.1B as of February 21, 2024.

Charting Compelling Catalysts

CRISPR Therapeutics anticipates a catalyst-rich almanac that should reveal state-of-the-art candidates across their platform from a broad range of therapeutic disciplines, including oncology, autoimmune diseases, cardiovascular diseases, and diabetes. If the data is positive, these catalysts could validate and expedite my bull thesis for CRSP.

CASGEVY Updates

CASGEVY’s FDA approval will undoubtedly be one of CRISPR’s most important milestones in the company’s history. However, CASGEVY still has plenty of other catalysts to contribute. Primarily, CASGEVY has other regulatory milestones to hit in the coming months and years. The European Commission (EC) has already made its decision to conditionally approve CASGEVY for the treatment of SCD and TDT. As of now, CASGEVY is approved in the U.S., EU, Great Britain, Saudi Arabia, and Bahrain. However, the company announced that they are awaiting CASGEVY’s regulatory approval in Switzerland, along with a submission in Canada for the first half of this year, thus, expanding their commercial footprint.

In addition to these regulatory actions, CRISPR and their partner, Vertex Pharmaceuticals (VRTX) are working on a successful launch of CASGEVY in the U.S. and Europe. As of the company’s last earnings report, CASGEVY has 12 authorized treatment centers ((ATCs)) in the U.S. and 3 in Europe, which dramatically improves patient access and capacity. As a result, we should have early commercial launch numbers this year and will be able to track CASGEVY’s sales throughout 2024 and into the future.

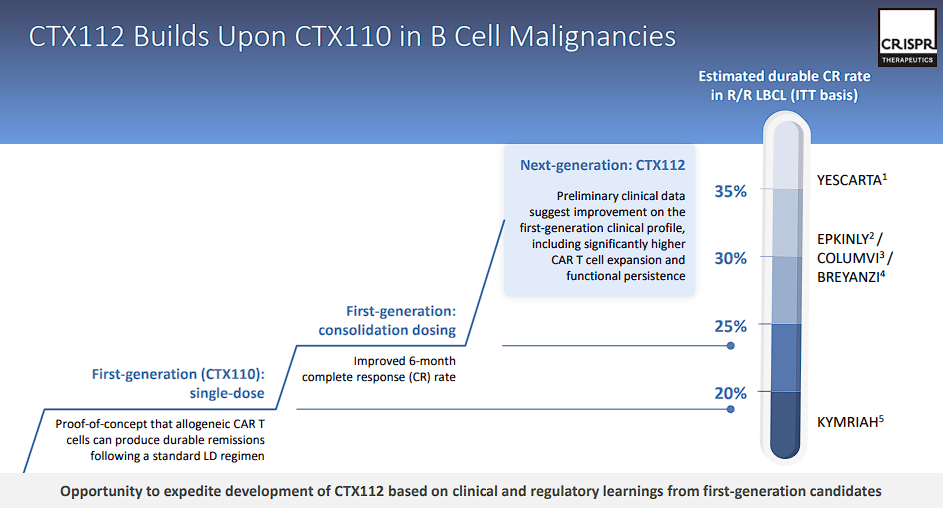

CTX112

The CTX112 program has the potential to be a key catalyst for CRISPR Therapeutics. As the company continues to move deeper into the field of gene-edited allogeneic CAR T cell therapies. With its focus on autoimmune disorders, CTX112 has the prospects to address B-cell malignancies and systemic lupus erythematosus (SLE).

CRISPR Therapeutics CTX112 (CRISPR Therapeutics)

With plans to initiate a Phase I trial and data updates expected in 2024, results could confirm this novel approach’s therapeutic potential and validate CRISPR’s ability to apply their technology to cell therapies. In addition, the early data could encourage CRISPR to take on additional autoimmune indications down the road.

CTX131

Another important program in CRISPR Therapeutics’ pipeline is CTX131. With its focus on CTX1131 has the prospects to change how we treat of Heme and solid tumors. The initiation of their Phase I clinical trial in the first half of 2024 marks a crucial milestone in advancing CTX131 and moving closer to verifying their efforts in oncology. The company expects to report data at some point in 2024.

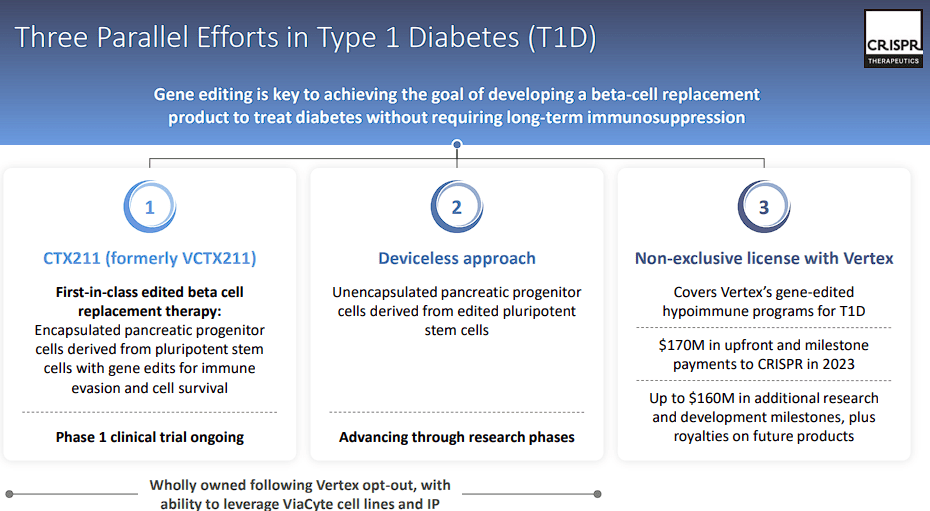

CTX211

Type 1 diabetes remains a perplexing condition to manage, requiring lifelong treatment with insulin. CRISPR Therapeutics’ ongoing trial for CTX211, is aimed at addressing Type 1 diabetes devoid of chronic immunosuppression measures. By adding patients to the initial cohort, the company hopes to collect further data on the safety and efficacy of this potentially game-changing therapy.

CRISPR Therapeutics CTX211 (CRISPR Therapeutics)

Vertex has non-exclusive rights to certain CRISPR Therapeutics’ technology for potentially curative cell therapies for Type 1 diabetes. Vertex has already paid $170M in payments, and CRISPR Therapeutics remains eligible for $160M in R&D milestones as well as royalties. So, positive data and continued development of CTX211 would provide CRISPR with payments and validate that their CRISPR/Cas9 technology can be a viable option for one of the world’s most challenging health concerns.

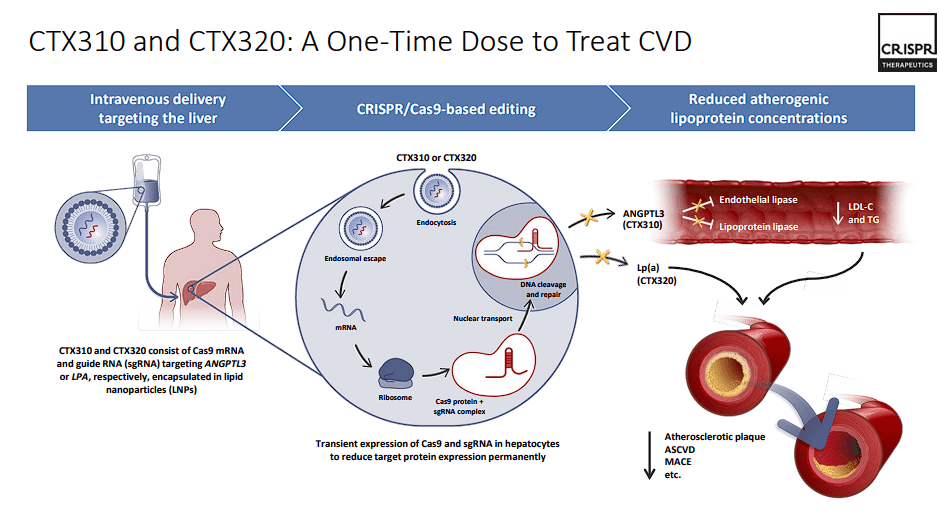

CTX310 and CTX320

CRISPR is also developing their in vivo gene editing programs, which utilize lipid nanoparticle (LNP) delivery of Cas9 mRNA and guide RNA ((gRNA)). Leading this effort are two innovative programs, CTX310 and CTX320, each tailored to tackle distinct aspects of cardiovascular disease. CTX310 is in Phase I trials, focusing on reducing angiopoietin-like 3 protein (ANGPTL3), which is expected to lower cardiovascular risk for people with mixed dyslipidemias, homozygous familial hypercholesterolemia, heterozygous familial hypercholesterolemia, and severe hypertriglyceridemia. Concurrently, CTX320 is working with lipoprotein(a) (Lp(a)), a significant biomarker associated with atherosclerosis and cardiovascular disease. Phase I trials for CTX320 are also in progress. CRISPR expects to complete dose escalation in this.

CRISPR Therapeutics CVD Programs (CRISPR Therapeutics)

If the data from these candidates is promising, CRISPR could unlock the potential of in vivo gene editing as a groundbreaking approach of a one-time cardiovascular therapy.

Undisclosed Targets

Another catalyst to consider is the company’s expected announcement of multiple new targets in 2024 to expand its pipeline and explore novel therapeutic avenues. These undisclosed targets may be significant market opportunities for addressing diverse disease areas and help solidify the company’s position as a leader in gene editing.

Validating The Thesis

CRISPR Therapeutics is loaded with multiple catalysts expected to drive clinical progress and value creation. From advancing novel CAR T cell therapies to addressing autoimmune disorders, cancer, cardiovascular diseases, and diabetes, the company’s diverse pipeline reflects its unwavering commitment to transforming patient care through innovative gene-based therapies. As these upcoming catalysts approach, patients, providers, and payers alike fervently anticipate the impact of CRISPR technology on the healthcare industry.

For me, these catalysts could validate my thesis that CRISPR will be considered a lead candidate for having the best-in-class CRISPR technology and that their technology can be applied to a variety of diseases and conditions. So, far CRIPSR has achieved historic milestones to validate this technology, including the approval of CASGEVY for hemoglobinopathies. Moreover, the company’s efforts to advance next-generation therapies, such as gene-edited allogeneic CAR T candidates and stem cell-derived beta cells candidates, underscore their determination to quickly achieve leadership.

The “Pie-In-The-Sky” potential here is that CRISPR Therapeutics could have therapy for nearly every type of disease or condition. CRISPR is not at that stage with their pipeline, but you can see the seeds of rapid expansion upon the success of their programs. Some of the worst diseases are cardiovascular, metabolic, cancer, and autoimmune… all of which currently have blockbuster drugs. Positive data readouts from these programs would not only improve the outlook for the candidates but could insinuate that future candidates would have similar success in these areas of healthcare.

Indeed, these programs are still early in their development, however, I will point out that the FDA and other regulatory agencies have approved gene therapies without a big Phase III trial. It is possible that one of CRISPR’s Phase I or Phase II trials could reveal the likelihood of approval more than other drugs or therapies. Therefore, my bull thesis might not only be validated by these upcoming catalysts, but it could also be confirmed at a much shorter timeline than originally projected.

Another point to add, CRISPR’s robust balance sheet, with roughly $2.1B in pro forma cash, provides them with the fuel needed to advance their pipeline and firm foundation for future growth. It is hard to forecast how long that cash position will last with the company’s extensive pipeline, but it should last long enough to see most of these active programs get to their next readout or milestone. By leveraging its resources effectively, CRISPR Therapeutics can accelerate the development and commercialization of its transformative therapies, bringing them to patients in need expeditiously.

Binary Risks

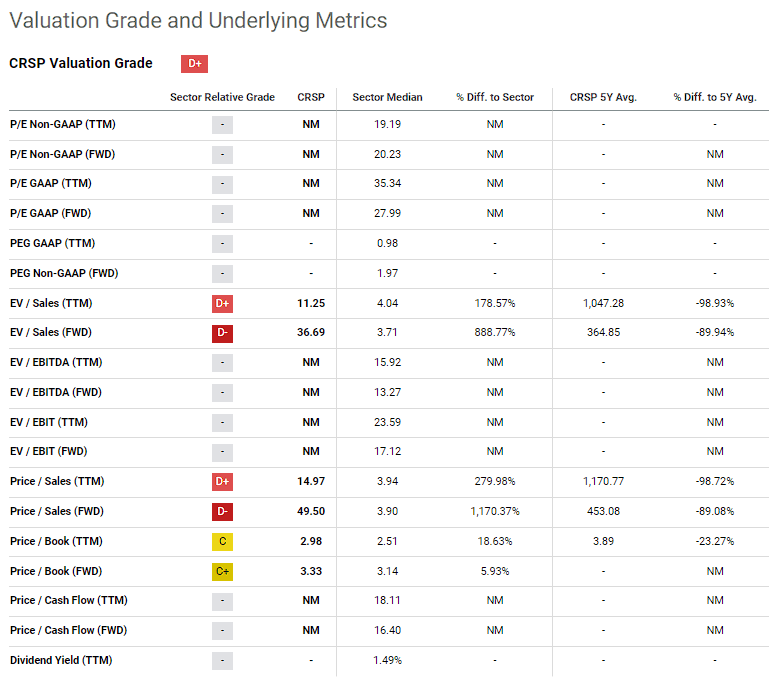

The downside to most of these catalysts is that they are binary events… meaning, if the data is positive, it should be a positive event for the company and the ticker. If the data is disappointing or the therapy fails to hit its endpoint… well, you should expect a negative reaction from the market. At the moment, CRSP’s market cap is around $5.63B, which is a rich premium for its current performance and financials.

CRSP Valuation Grades and Metrics (Seeking Alpha)

Although CASGEVY’s launch should improve those metrics, I still believe CRSP is still a bit overvalued for that product alone. In fact, estimates have CASGEVY hitting $1B in sales in 2027 and reaching a peak of $2.2B in 2030. So, it is likely that some of the ticker’s premium is linked to their current and future pipeline programs will be a success. Consequently, a clinical or regulatory failure could quickly remove that premium and hype around CRSP.

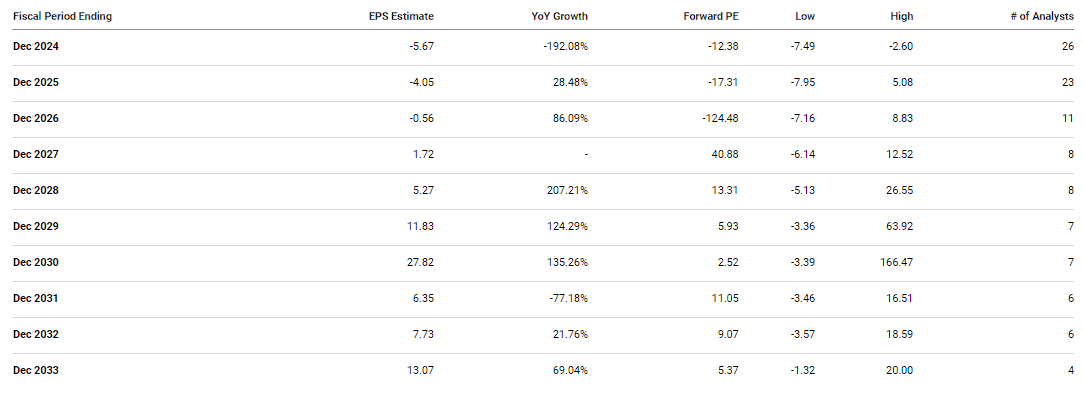

In addition, any clinical or regulatory setbacks will most likely prolong the company’s cash burn and force analysts to consider the likelihood of additional dilution. At the moment, analysts are not expecting CRISPR to report a positive EPS until 2027, so investors need to be prepared for continued cash burn.

CRISPR EPS Estimates (Seeking Alpha)

A failure might move those positive EPS estimates back a year or more and place a cloud over the ticker for an extended period of time.

Lingering Concern

I still perceive the primary challenge facing CRISPR emanates from the tough competition posed by numerous gene therapy companies and research institutions. Among these, notable contenders utilizing CRISPR-Cas9 technology consist of Intellia Therapeutics (NTLA) and, prominently, Editas Medicine (EDIT). Furthermore, there are other gene therapy firms like bluebird bio (BLUE), Sangamo Therapeutics (SGMO), Cellectis (CLLS), Precision BioSciences (DTIL), and Allogene Therapeutics (ALLO), are employing alternative gene-editing platforms. While several gene therapy firms exist beyond those stated, the principle of the argument remains clear.

Although certain competitors may not presently match CRISPR’s stature, I contend that their most significant threat lies in nascent or unanticipated developments. As gene therapy products enter the market and begin displacing established therapies, it’s foreseeable that major pharmaceutical companies will allocate a larger portion of their research and development resources toward gene therapies. Consequently, more academic and research institutions may innovate novel CRISPR technologies or advance gene-editing capabilities to surpass CRISPR as the pinnacle technology in the field.

My Plan

At the moment, my Buy Targets and Sell Targets for CRSP will remain the same. However, the company mentioned that they expect to provide some updates on the timing of readouts and trial starts around mid-year for some of these programs. Once we have some clarity on readout timelines, we can begin to forecast other regulatory milestones and match that with estimated cash burn to help reset some Buy and Sell levels using a combination of technical analysis and several valuation models.

Long-term, I plan on being involved in CRSP for the next 5 years in anticipation the ticker will provide plenty of trading opportunities to book profits, all while amassing a “House Money” core position to hold for a long-term investment.

Q2 2024 Earnings Call Transcript")