Editor’s note: Seeking Alpha is proud to welcome GP Sigma Analytics as a new contributor. It’s easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

YvanDube

Thesis

After conducting a thorough analysis, I firmly believe Costco Wholesale Corporation (NASDAQ:COST), a well-known membership-only warehouse retailer, presents an attractive investment opportunity. What catches my attention is the company’s superior financial metrics, profitability ratios, and robust top-line growth prospect, driven by its unique membership only model, outperforming its rivals like Walmart (WMT) and Target (TGT). Even though the stock has risen sharply over the past year, in my analysis it stands out as a buy recommendation.

Company Overview

Costco Wholesale Corporation is an Issaquah, Washington, USA headquartered giant retailer founded by James Sinegal and Jeffrey Brotman in 1976. Over the years it has grown to operate 874 warehouse and online platforms worldwide. Their mantra for success? A low-margin, high-volume business approach, which may seem counterintuitive to some, I believe is a key differentiator that delivers value consistently to members and fosters customer loyalty and drives sustainable growth.

Membership Model and Customer Loyalty

In my opinion, Costco’s membership-only model is the key to their incredible performance. With 73.4 million paid members and 132 million cardholders worldwide, Costco’s loyal community drives its profitability, with membership fees totaling $4.6 billion in fiscal 2023 alone. While some investors may only see this as a number, I consider Costco’s membership model to be a significant competitive advantage.

The company’s focus on providing value proposition for its members through quality products at discount, and retention strategies such as discounted hot dogs, and added services on its tyre have helped it to maintain a loyal customer base and generate long-term revenue streams. As such, its renewable rates have reached 92.9% in the US and Canada, and 90.5% worldwide. My perspective on these high renewable rates is that they indicate strong customer loyalty towards the Costco brand. Furthermore, as trends indicate continued market saturation and growth, Costco’s membership model is in my view not just a barrier to entry but also a symbol of loyalty, ensuring their dominance over the retail industry.

However, a potential membership fee hike has been overdue, based on its historical average gap between hikes. This is making many investors uneasy as I expect it to hike its membership fee by around 10%, in line with its competitor Walmart’s recent 11% increase. This potential hike could significantly increase the company’s net earnings, but, with inflation still above fed’s tolerance rate, and recent leadership changes, notably the appointment of Ron Vachris as CEO, and Gary Millerchip as CFO, I highly doubt the new CFO would take such a big decision so early that might negatively impact the performance of the company.

Crafting Value And Simplifying Choice

In terms of the company’s retail strategy, Costco displays a rather limited but affordable products mix ranging from groceries to fancy delicacies to state-of-the-art electronics. Each item is carefully selected, with only around 4,000 active stock keeping units (SKUs) per warehouse compared to Walmart’s 100,000+. My perspective is that a deliberate selection process ensures accuracy, as well as optimizes its inventory management and provides negotiating power with suppliers to provide competitive pricing to its members. At the core of Costco’s retail concept lies its private label brand, Kirkland Signature, which contributes around one third of Costco’s total revenue, aims to offer high quality products at affordable price compared to name-brand products. Whether it is household staples or fancy delights, every Kirkland Signature product comes with Costco’s return policy and affordability. In my opinion, through its exclusive brands like Kirkland, Costco enhances its members’ shopping experience and differentiates itself from other retail peers.

Financial performance and Outlook

Costco has demonstrated amazing strength by consistently driving higher revenue growth over the years, primarily due to expansion efforts, robust membership fees, and strong sales volume. Although Costco missed revenue estimates in Q2 2024, I am not overly concerned as I believe the underlying demand and membership growth remained strong, and cost controls further strengthening its position. The company reported total revenue and net sales of $58.44 billion and $57.33 billion respectively, an increase of 5.7% Y/Y, reflecting strong customer demand and higher sales in e-commerce, but lower than the analysts estimate because of the negative impacts from low gasoline price, and slower revenue growth in its traditional warehouse business.

Membership fees, which is a significant contributor to the overall profitability of the company, were $1.11 billion in Q2 ’24, an increase of 8.2% from the same quarter prior year. This strength in membership fees is due to Costco’s strong business model and various strategic initiatives. Additionally, Costco demonstrates proactive approach to expense management and budgeting, as its SG&A expense as a % of net sales has improved to reach 9.14% in the latest quarter compared to 10.10% in fiscal 2019.

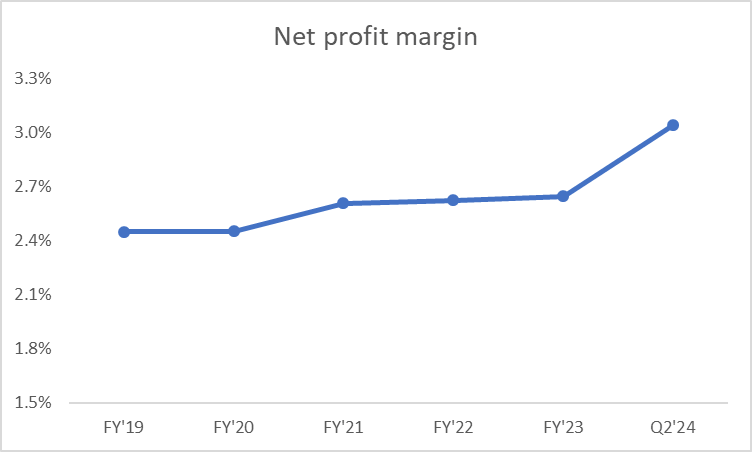

Costco’s diluted earnings per share (EPS) of $3.92 for the second quarter beat consensus estimates by $0.31. The increase in EPS was because of $94 million in tax benefits due to deductibility of special dividends, and higher growth in membership fees. Its NPM in the second quarter reached 3% from 2.4% in fiscal 2019, showcasing operational efficiency and favorable membership trends over the years. While fluctuations in gas prices have negatively impacted Costco’s profitability lately, the company has several possible mitigation strategies. These include underscoring growth opportunities in the big ticket discretionary category and maintaining a diligent expense management programme. These measures signal the company’s underlying financial strength to me.

Company Data, Author’s Compilation

Strategic Initiatives and Growth Prospects

Looking ahead, Costco continues to strategically pursue expansion opportunities both domestically and globally to drive its future growth. With a network of 874 membership warehouses across various countries, Costco continues to explore new ways to increase store count. In Q2, Costco opened 4 net new warehouses, including one in China, and for the fiscal 2024 it plans to open 30 units in total, mostly in the US. Regarding expansion in the US, CFO Richard Galanti during the Q2’24 earnings call said:

our view is over the next 10 years that we could easily add another 150 and that’s on top of however many business centers, call it, but just in the U.S. So – and that number keeps changing … .So, we’re finding more opportunities here and it’s evidenced by just the sheer volumes of the units – that our units are doing today versus three or four years ago. It’s much higher than we would have expected three or four years ago. So we think that there is still a lot of runway in that regard.

I am particularly impressed with Costco’s strategic initiatives like Costco Next, Costco Logistic, and its E-commerce push. The successful implementation of Costco Next which comprised of remodeling and relocation of stores, has significantly strengthened sales growth, with the company reporting a 5.6% increase in same-store sales during Q2 2024. Meanwhile with Costco Logistics, the company is working to improve its supply chain and logistics by building new distribution centers and expansion of its transportation network.

The E-commerce and digital initiatives have been of great help in revenue growth for the company. Its online business grew by 18.4% Y/Y last quarter, which primarily drove their overall revenue growth. I notice that these efforts not only enhance revenue of the company, but also set it for the future by improving operational excellence and supply chain. However, there are some risks and challenges associated with it, like increased infrastructure costs, increased competition from other retailers like Amazon (AMZN), Walmart and Target, and difficulties in the process of attracting & retaining customers in the rapidly evolving digital landscape.

In my opinion, Its strength was demonstrated last year with the quick sell-out of gold bars upon their introduction. Likewise, the expansion of Kirkland Signature brand and improvement of its omnichannel capabilities position Costco to further drive revenue growth and market share gains.

Valuation

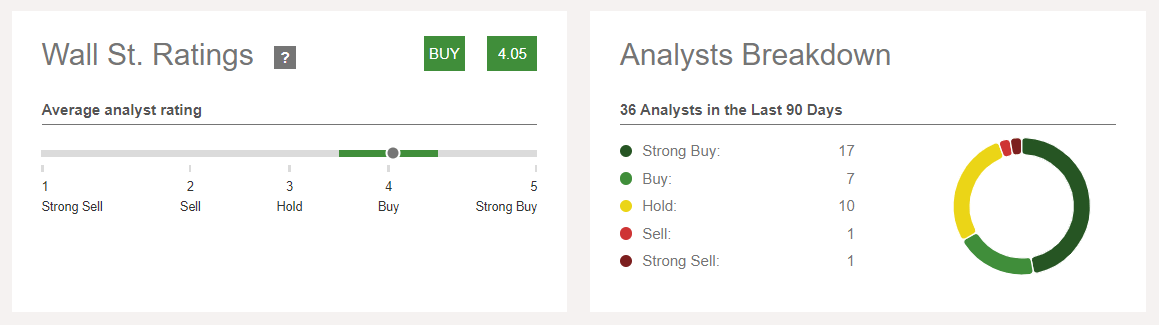

While it is true that the company’s share price has risen by ~45% over the past year, which some investors may see as a warning sign about valuation, I believe the recent correction of over 10.33% presents an attractive entry point for long-term investors like myself. In addition, Cash dividends of Costco make it an attractive investment choice for income oriented investors. Costco’s current stock price of $705.69 reflects an upside of 8.63% from Wall Street analysts average price target of $758.77. So, I am not alone here, 24 out of 36 analysts have either a strong buy or buy rating on the stock with average score of 4.05 out of 5.

Seeking Alpha

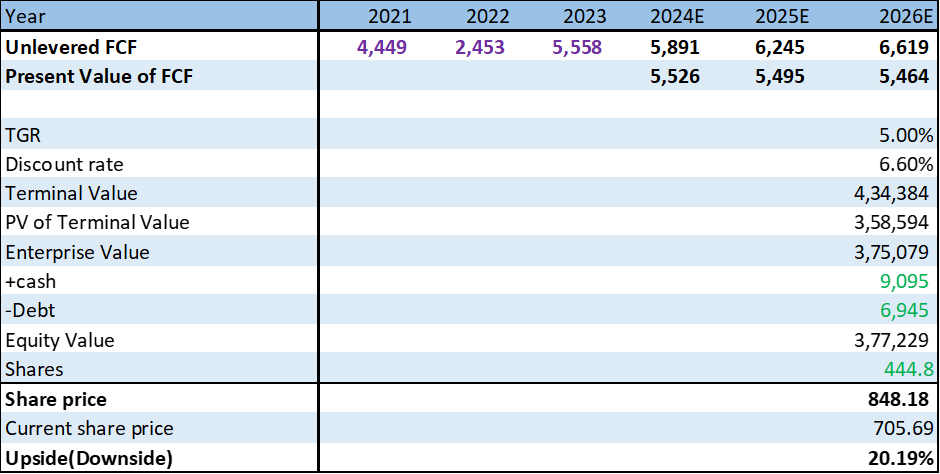

For my DCF analysis, I am discounting unlevered annual free cash flow (FCF) to arrive at the fair value. FCF represents the cash available to the company after accounting for CapEx and changes in working capital, making it a more accurate representation of the company’s ability to generate cash flows for its stakeholders. As I expect the company should continue to grow its FCF for fiscal FY’24 to FY’26 near its historical 5-yr average FCF growth rate of ~6.18%, I am keeping it at 6% and further I expect it should be able to grow perpetually at the rate of 5% as the company is already in its mature stage. This growth rate also accounts for its strong membership model and potential fee hikes. I am assuming a discount rate of 6.6%, which is obtained by adjusting 10-year US government bonds’ yield of 4.30%. I have added a risk premium to the risk-free rate to capture the inherent risks associated with Costco’s business. As you can see in DCF output, we arrived at a fair value of $848.18 for the stock, representing a potential upside of over 20.19%.

Costco’s DCF (Company Data, Author’s Compilation)

For the worse case, if we assume that its FCF grows indefinitely at only 4.50%, which is well below its historical 5-year growth rate of 6.18%, and discounted at 7.00%, target price comes out to be $549.72, which is 22.10% lower than the current price. Now for the best case, let’s say its FCF grows indefinitely at 5.5% and discounted at 6.50%, the target price comes out to be $1341.74, which is 90.13% higher than the current price. Under both these extreme case scenarios the probability of upside potential is higher. Therefore, I think the stock appears to be undervalued with strong potential return under the base case fair value of $848.18.

Risks

Costco operates in a very competitive retail landscape, facing pressure from traditional retailers like Walmart and Target which have also introduced membership programs in response to Costco’s success, and online retailers like Amazon, which has a significant online presence, successful membership base and has been expanding its physical stores. However, neither Walmart nor Target has been as successful as Costco with its membership model or Amazon with its physical stores expansion.

Also, the company has gone through leadership changes recently, they now face the risk of a strategic shift from its long standing principles, which could disappoint its loyal members who believe in the value it provides, resulting in disappointed investors who value the company at a premium compared to its peers. However, in my view, Costco’s member loyalty should help mitigate this risk, but still I believe investors should be mindful of these risks to make informed decisions.

Conclusion

In conclusion, the financial performance of Costco continues to be on a rise, driven by operational excellence, strategic initiatives, and aided by its membership model. With the purpose of boosting revenue, expanding profitability, and seizing the expansion opportunities, Costco is well positioned in the retail industry to generate long-term value for its shareholders. Based on my analysis of Costco, I have assigned a buy rating on the COST stock with a price target of $848.18.

Q2 2024 Earnings Call Transcript")