AdShooter/E+ via Getty Images

The Cornerstone funds, CLM and CRF, are some of the oldest CEFs that trade on the stock market. The original Cornerstone Total Return Fund (NYSE:CRF) began trading on the NYSE in May 1973. Although the fund’s stated investment objective is capital appreciation with a secondary goal of current income, many investors (including me) rely on CRF for a steady, dependable high-yield distribution that is paid monthly. The fund’s adviser uses a “balanced approach” of value and growth investing seeking out companies that are trading at reasonable prices and offer long-term growth characteristics.

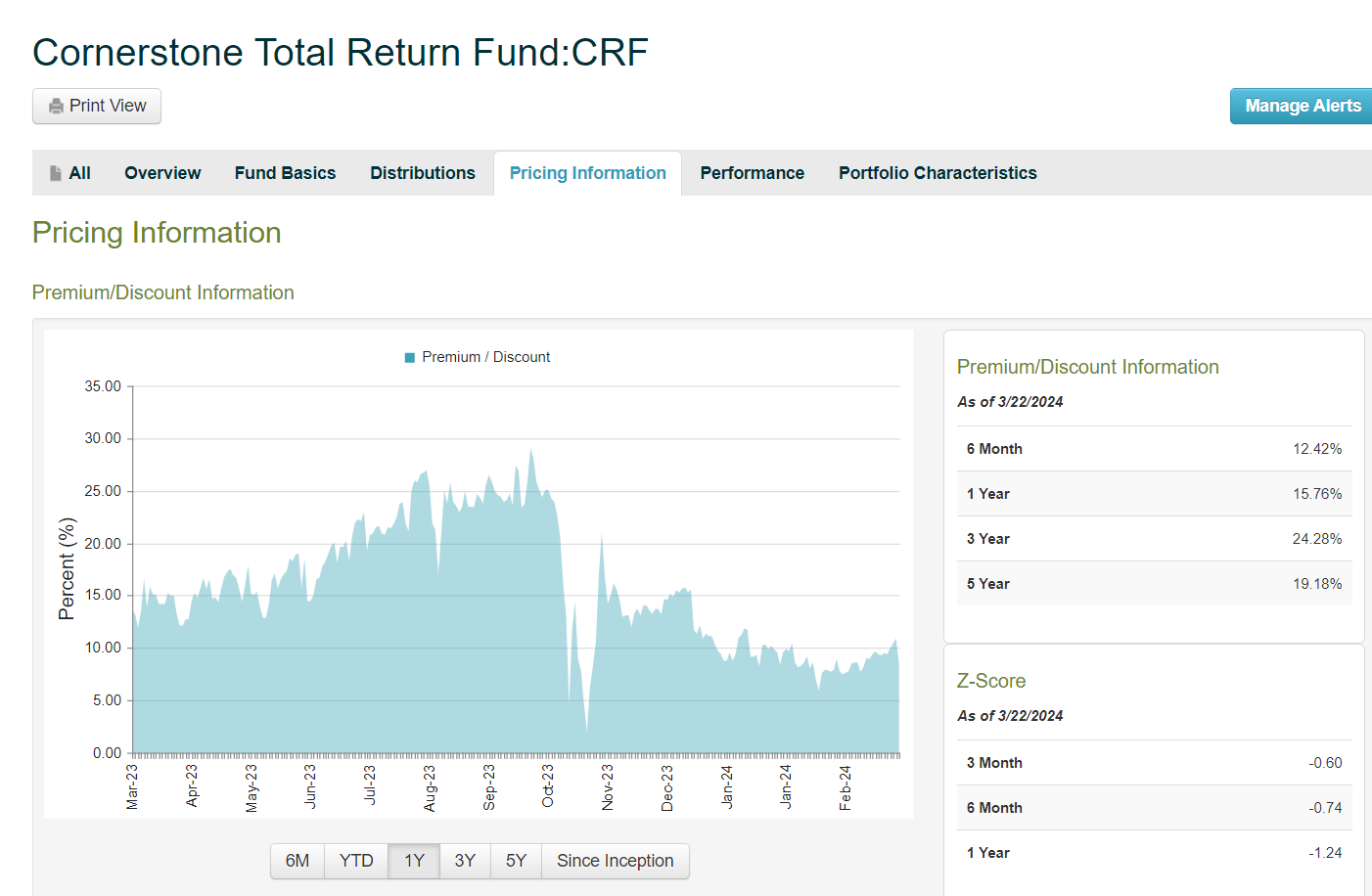

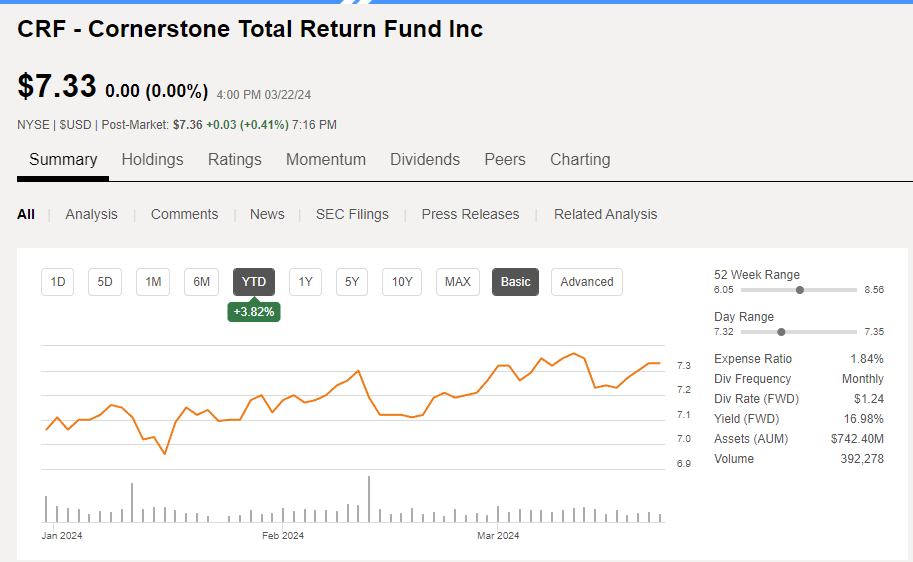

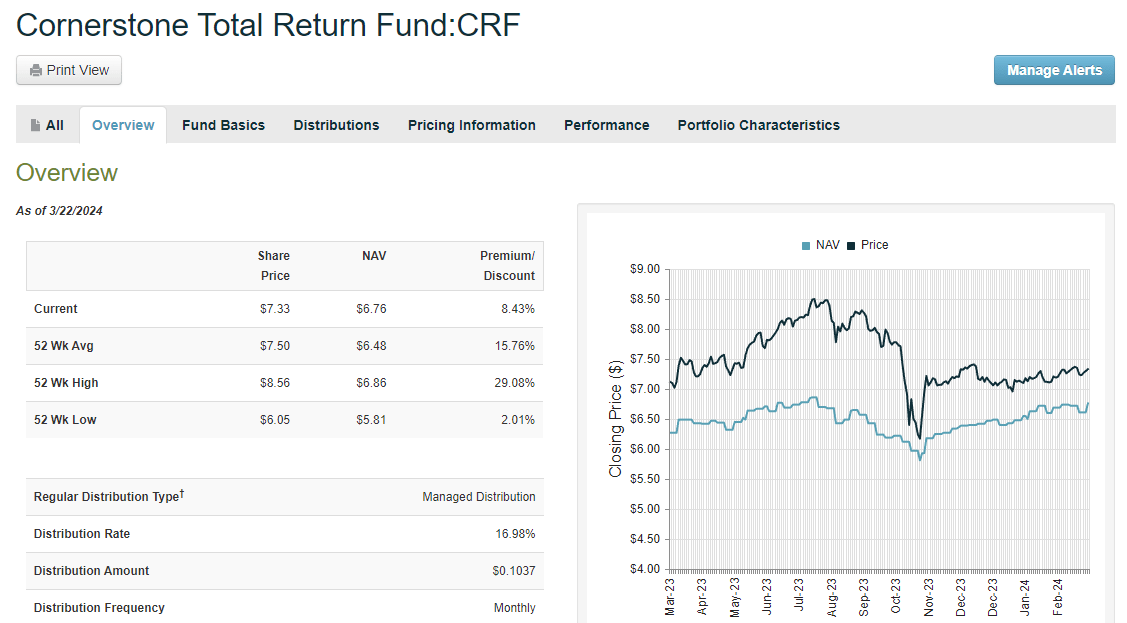

Also, being a closed-end fund, the market price frequently trades at a premium or at times, a discount to NAV. Historically, over the past 5 years at least, the market price of CRF traded at a premium which offers another substantial benefit to investors who reinvest the monthly dividend. Because of the generous DRIP policy, investors in both Cornerstone funds can reinvest shares automatically at NAV, which offers an immediate discount over the market price. Currently, CRF trades at a relatively low premium of about 8%, which is well below the 1-year average of 15.76% as shown on the CEFConnect website. As a result, investors who DRIP their monthly shares receive an -8% discount compared to buying shares on the open market.

CEFConnect

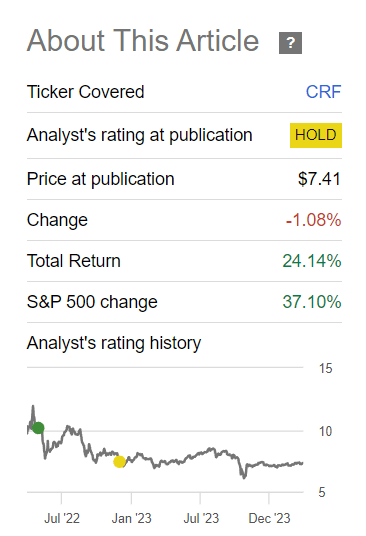

The last time I wrote about CRF was in December 2022 where I explained the preferred methodology for collecting a strong total return from the fund by buying, reinvesting, and then over-subscribing when the fund does a “rights offering” or RO. Although both funds typically do a RO every year to increase the share count of the funds, last year was an exception due to the uncertainty in the economy with continued expectations of recession and rising inflation. Nevertheless, CRF delivered a total return of more than 24% since December 2022 simply based on the standard total return calculation (with dividends reinvested at market price) provided by Seeking Alpha. Because I rated it a Hold at the time, that seems like a pretty decent return when you do not even consider the added discount available from DRIPing shares at a discount.

Seeking Alpha

Comparison To S&P 500 Returns

In some previous articles discussing CRF and CLM, I have read comments from some that say, why not just invest in the SPY? After all, the holdings in CRF mimic to some extent the holdings in the S&P 500 and if an index fund can return 37% while CRF only returns 24% why invest in CRF? My immediate response is that those two investments have very different objectives – growth versus income. As a now-retired income investor, I am far less concerned with growing my portfolio value than I am with increasing the income generated from my portfolio holdings. If the value of those holdings also increases, that is great, but it is not my primary objective.

This can be a difficult concept to grasp and is also dependent on what the overall market is doing. In bull markets like we are experiencing now, it is easy to find growth opportunities in individual stocks like Nvidia, Super Micro (SMCI), and AMD. But at some point, that growth will slow or stagnate, and the stock prices of those holdings will languish. On the other hand, CRF can adjust its portfolio holdings to take advantage of that price growth to capture capital gains that will help to support the high-yield distribution that the fund offers. Even if the prices drop, the fund will continue to pay the same level of distribution for the entire calendar year, according to the fund’s mandate as explained in the Annual Report:

The policy of maintaining regular monthly distributions is designed to enhance stockholder value by increasing liquidity for individual investors and providing greater flexibility to manage their investment in the Fund. As always, stockholders can take their distributions in cash or reinvest them in shares of the Fund pursuant to the Fund’s reinvestment plan.

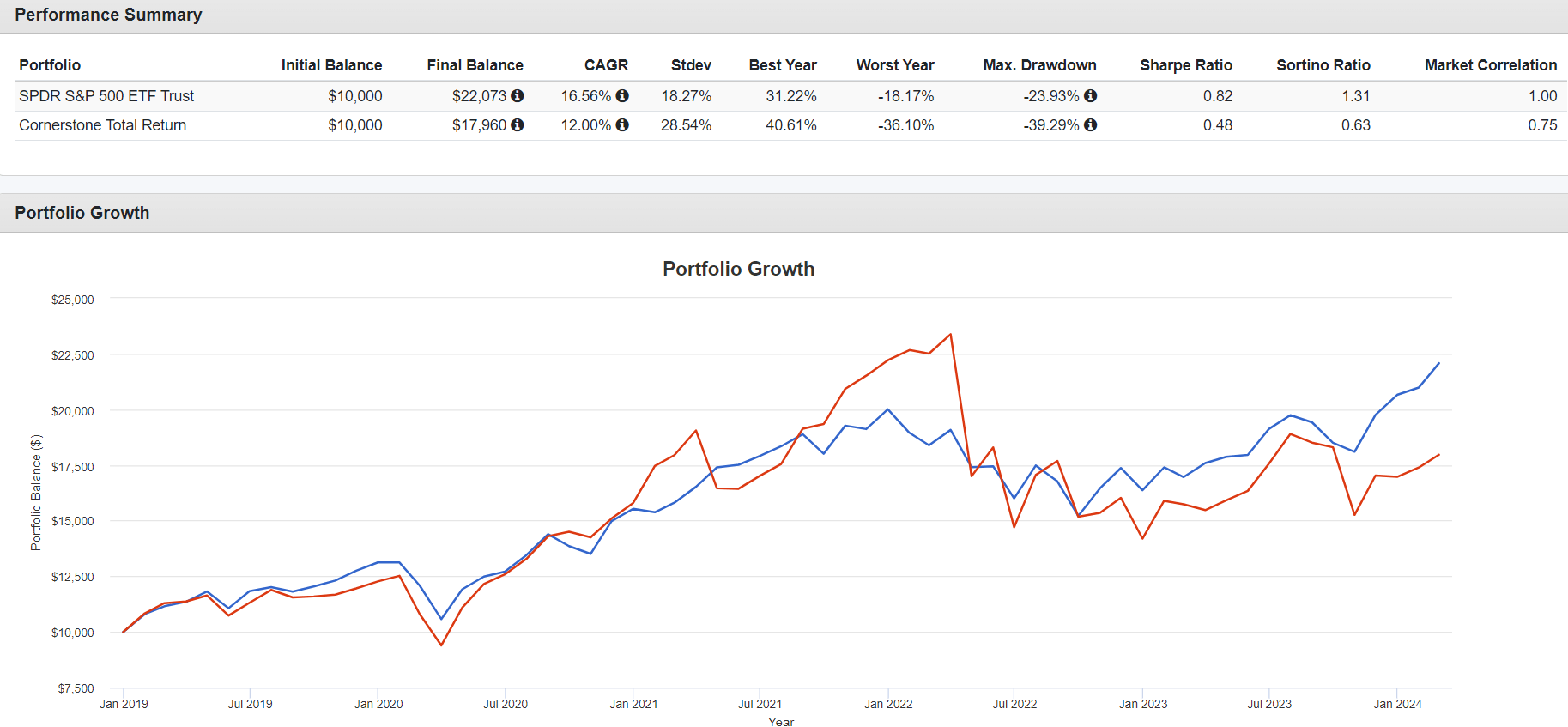

One way to help explain this concept is by showing the results from Portfolio Visualizer comparing 5-year returns from SPY versus CRF with dividends reinvested (again, not taking the additional discount for reinvesting into account). The parameters I used include $10,000 invested in January 2019 through February 2024. The investment in SPY would result in a final balance of $22,073 while the CRF portfolio balance would be $17,960, and that is mainly due to the recent jump in the SPY in the past couple of months.

Portfolio Visualizer

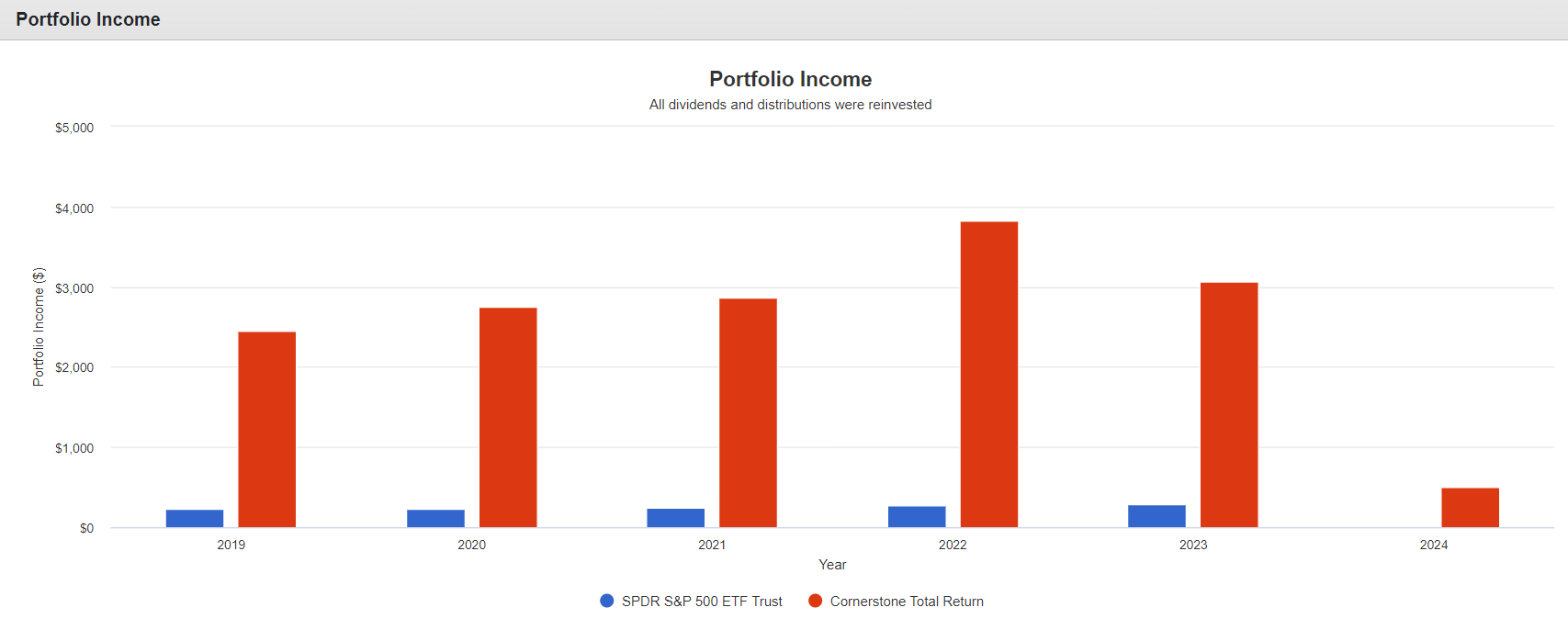

Meanwhile, the income generated from CRF would be considerably higher with nearly $4,000 in income in 2022 and about $3,000 in 2023. By the end of this year, the amount of income generated would likely be close to $3,000 given that about $500 was paid in the first two months, even though the monthly distribution was reduced slightly in January. That is because the reinvested dividends buy more shares at lower prices resulting in higher future income. That is the benefit of an income-compounding approach. It also explains why so much more income was generated in 2022 when the stock market had one of the worst years in decades.

Portfolio Visualizer

CRF Portfolio Holdings

As explained in the Annual Report as of 12/31/23, the fund portfolio holds mostly large cap, domestic stocks such as Apple, Microsoft, Amazon, and Alphabet. In fact, those were the top 4 holdings at that time (they may have shifted some since then). Further explanation of the fund holdings is described in the Letter to Stockholders section of the report:

The majority of the Fund’s portfolio is comprised of domestic large-cap stocks, which generally performed well through the year. Toward the end of the third quarter and into the beginning of the fourth quarter, the S&P 500 index saw significant declines. However, only the third quarter saw negative returns for the S&P 500 index, but technology stocks continued to perform well through the end of the year. Our investing approach considers overall sector weighting and individual positions within each sector to balance the best potential for positive performance while taking advantage of occasional inefficiencies when prudent. We believe this approach adds objectivity through sector discipline, reduces volatility, and provides a conservative path to consistent long-term returns. In 2023, the strength of the Fund’s positions in Nvidia, Alphabet, and Amazon boosted overall returns. In contrast, the Fund’s holdings in Visa and UnitedHealthcare underperformed. The Fund benefitted from volatility in securities in the closed-end fund category during the year. Closed-end funds have an elastic effect on the Fund’s performance, sometimes benefiting performance and sometimes lagging depending on the broader market.

Fund Distributions

Each year in November the fund resets the level distribution for the upcoming calendar year based on a formula that typically is set to 21% of the NAV as of the end of October. Last year, the market bottomed out at the end of October, so the fund NAV was at about its lowest point of the year, which resulted in a decline in the monthly distribution amount from $.1173 to $.1037 per share for 2024. While that may have been disappointing to some who are new to the fund, it was to be expected based on the fund’s history and well-known distribution policy. Furthermore, as investors take advantage of the fund’s DRIP policy, the total return will likely improve in 2024 as the market continues its bull run in the first 3 months.

The Fund’s distribution reinvestment plan may at times provide significant benefits to plan participants; therefore, stockholders should evaluate the advantages of reinvesting their distribution payments through the plan. Under the plan, the method for determining the number of newly issued shares received when distributions are reinvested is determined by dividing the amount of the distribution either by the Fund’s last reported NAV or by a price equal to the average closing price of the Fund over the five trading days preceding the payment date of the distribution, whichever is lower. When the Fund trades at a premium to its NAV, as it has in recent history, stockholders may find that reinvestments through the plan provide potential advantages worth considering.

While the price of the fund dropped after the new distribution was announced, it was mostly the result of the premium shrinking and not the NAV of the fund. In the last 6 months, CRF has declined in price by about -8% but YTD the fund price is up nearly 4%, which mostly reflects the rising NAV.

Seeking Alpha

While the best time to buy would have been back in late October when the price plummeted to nearly a discount, the current price is still what I would consider Buy territory at a premium under 10%. If one wanted to wait until the premium rises higher there may be another RO this year. That is often a good time to buy also because the share price typically drops after the RO terminates due to some dilution to NAV that typically results from issuing new shares. Again, using CEFConnect to display the relationship between NAV and price it is apparent that NAV is on the rise in 2024 while the premium remains narrower than average.

CEFConnect

Recommendation And Summary

With a current distribution yield of about 17% and a level monthly distribution that is unlikely to change until next January, I rate CRF a Buy. The top holdings are all performing well, and NAV is rising while the premium is below the historical average. For those investors who wish to secure a strong source of current income with some potential capital appreciation in 2024, I suggest taking a closer look at CRF and its sibling fund, CLM, which is trading at an even smaller premium.

The CLM fund is newer and about twice the size based on net assets. It generally has a NAV that is a few cents more than CRF but currently is about $.30 more ($7.06 for CLM compared to $6.76 for CRF). The price of CLM is trading at a premium of less than 5% so if I had to choose between the two, I would probably go with CLM right now. The fund holdings are very similar and the distribution policy with the DRIP discount is the same. The current yield at market price for CLM is nearly 18%.

Please chime in with your thoughts in the comments section below if you have anything constructive to add or wish to share your experience with others. I have done well with both CRF and CLM in my Income Compounder portfolio held in my Fidelity IRA and have substantial holdings (for me) in both funds currently.

Q2 2024 Earnings Call Transcript")