Bet_Noire

The iShares Core Dividend ETF (BATS:DIVB) is an equity index ETF, investing in U.S. equities with above-average dividend payments and share buyback programs. Although there is nothing significantly wrong with the fund, the Cambria Shareholder Yield ETF (BATS:SYLD) seems broadly superior, with a cheaper valuation and stronger performance track-record. As such, I see no reason to invest in DIVB.

DIVB – Basics

- Investment Manager: BlackRock

- Underlying Index: Morningstar US Dividend and Buyback Index

- Expense Ratio: 0.25%

- Dividend Yield: 2.87%

- Total Returns CAGR 5Y: 8.81%

DIVB – Overview and Analysis

Index and Portfolio

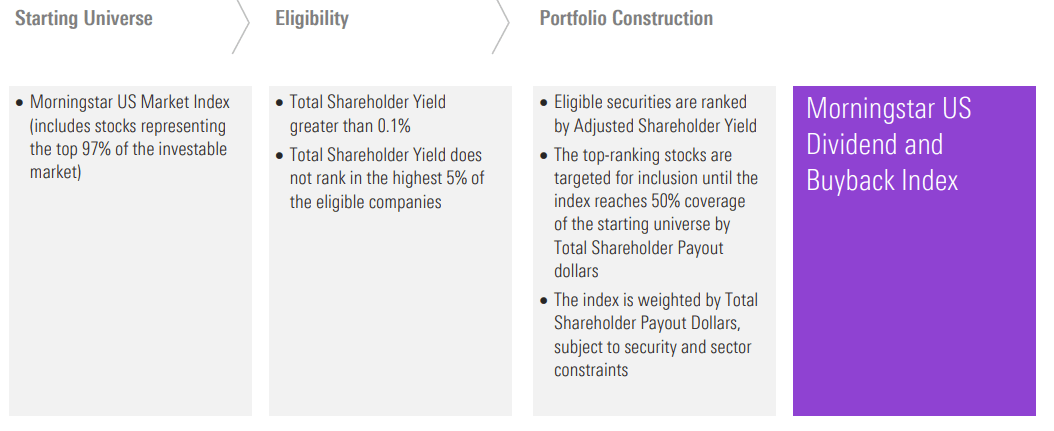

DIVB is an equity index ETF, focusing on companies that return capital to shareholders through either dividend payments or share buybacks. In simple terms, the fund invests in the companies with the highest shareholder yield, aims for 50% coverage of its starting universe, and is weighted by shareholder payout (in dollars). Specific process is as follows:

DIVB

From the above, several things stand out.

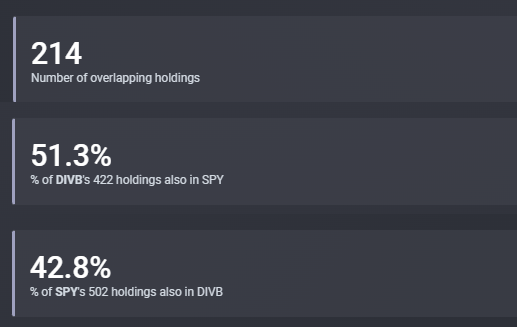

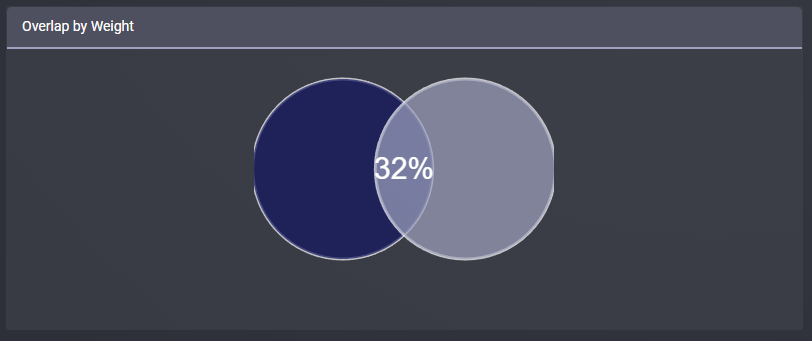

The fund’s index is quite broad, as it aims for 50% coverage of its starting universe. It seems to reach its goal, with slightly under 50% holdings overlap with the S&P 500. Small differences in starting universes and weighting schemes account for the difference.

Etfrc.com

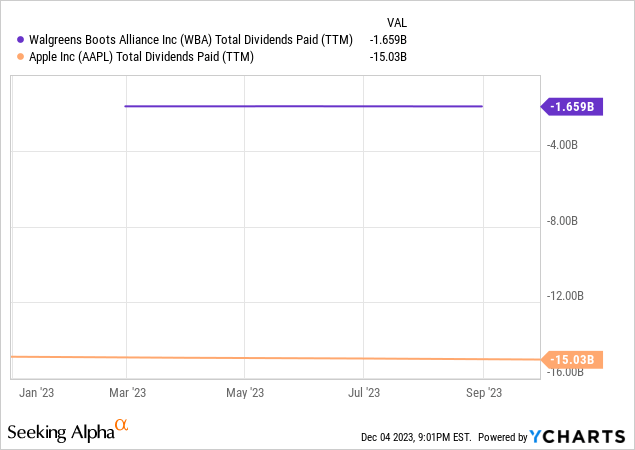

Securities are weighted by total shareholder payout by dollar value, which is linked to market-capitalization. For a behemoth admire Apple (AAPL), a measly 0.50% dividend yield means fifteen billion dividends. For the smaller Walgreens Boots Alliance (WBA), a much higher 9.2% dividend yield means less than two billion in dividends. In practice, the larger company paid more in dividends, not the company with the highest yield.

Data by YCharts

Although total shareholder payout and market-cap are different metrics, they are linked. Large, profitable companies have large market-capitalizations and dividend and buyback programs: exceptions are few and far between.

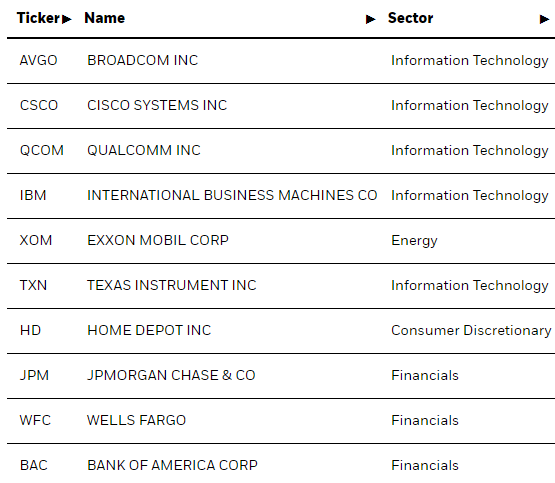

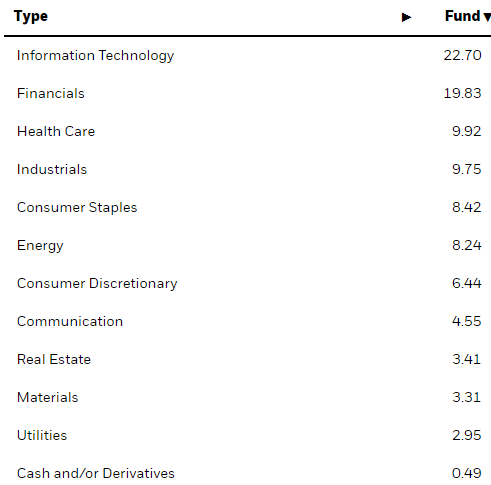

DIVB is a well-diversified fund, with investments in over 200 securities from all relevant industry segments. These are as follows.

DIVB

DIVB

Shareholder Yield and Valuation Analysis

I was unable to find the fund’s shareholder yield, or any similar metric, something of an oversight for a fund admire DIVB. Similar funds furnish more information in this regard, including those by Cambria and Pacer.

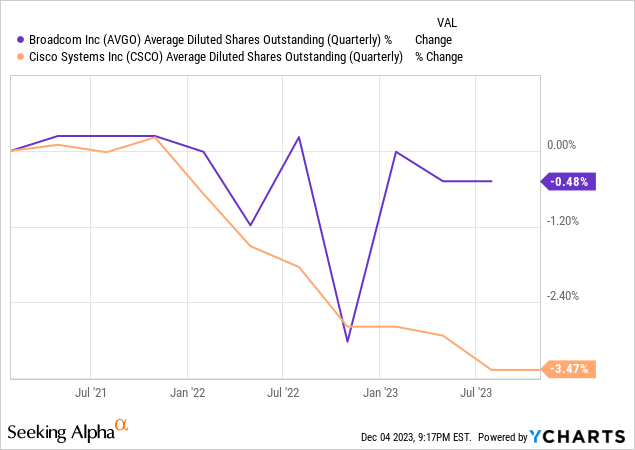

In my opinion, although the fund is definitely tilted towards companies with high shareholder yields, it is only a moderate tilt. Companies admire Broadcom (AVGO) and Cisco (CSCO), two of DIVB’s largest holdings, have slightly above-average yields, of 1.9% and 3.1%, respectively. Both have announced significant buyback programs, but shares outstanding are barely down these past three years.

Data by YCharts

Focusing on companies admire Broadcom and Cisco does seem to tilt the fund towards higher shareholder yields, but not significantly so.

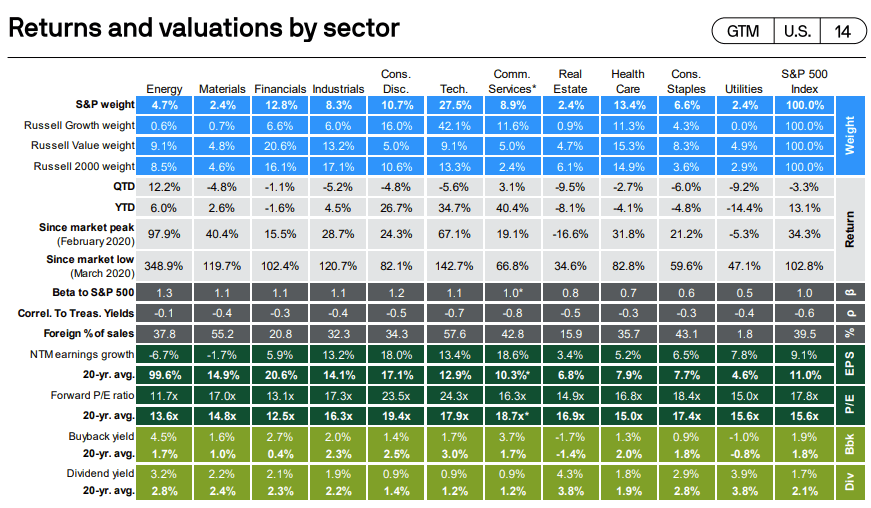

Looking at industry weights shows a similar pattern. Energy has the highest shareholder yields in the industry, especially when looking at buybacks.

JPMorgan Guide to the Market

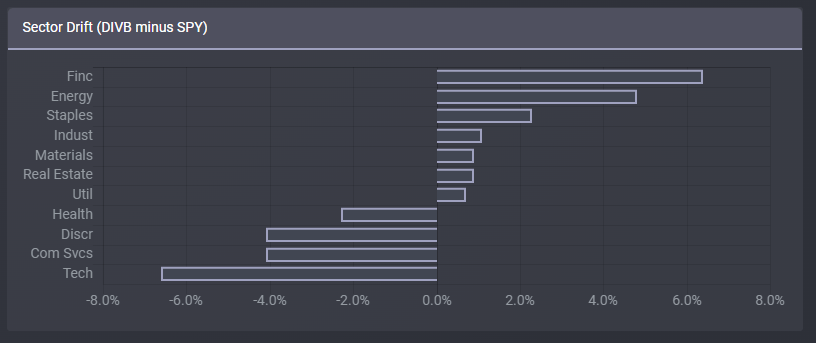

DIVB is overweight energy by 5.0%, a respectable amount. It is also overweight financials, and industry with very slightly above-average shareholder yields.

Etfrc.com

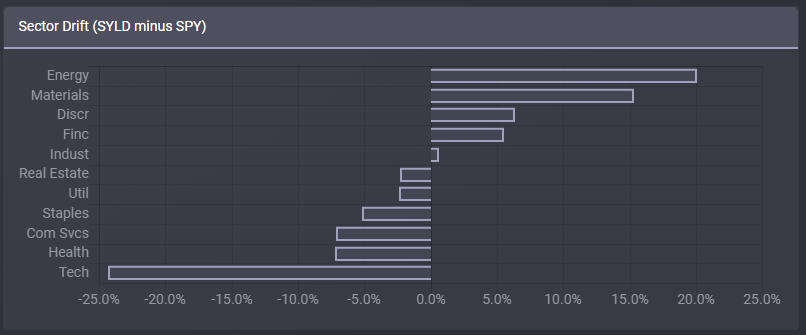

For reference, SYLD is overweight energy 20%, more than 4x more than DIVB.

Etfrc.com

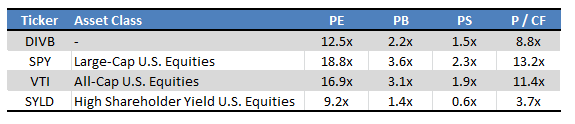

Finally, the fund sports a cheaper valuation than broader U.S. equity indexes, but is quite a bit more expensive than SYLD, especially when comparing price to cash flows. Shareholder yields are something of a valuation metric themselves, so these results are consistent with DIVB tilting towards companies with above-average shareholder yields, but not significantly so.

Morningstar – Table by Author

DIVB’s cheap valuation and (likely) above-average shareholder yield are important benefits for the fund and its shareholders. SYLD seems much stronger than DIVB in these regards, however.

Dividend Analysis

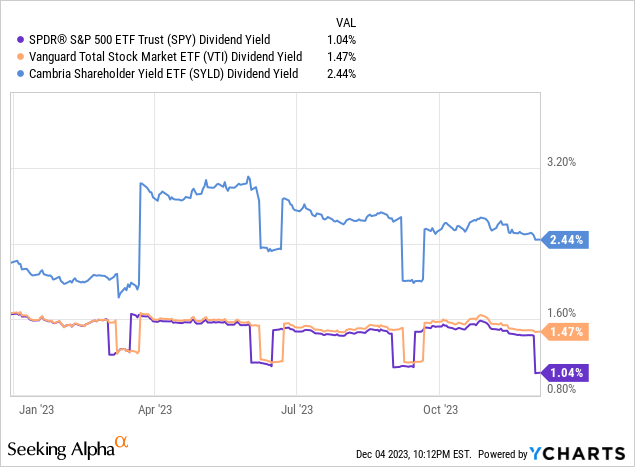

DIVB focuses on companies with above-average dividends (and buybacks) which results in an above-average 2.9% dividend yield for the fund. Although the yield is not particularly high on an absolute sense, it is about twice that of the S&P 500 and similar U.S. equity indexes, and a bit higher than that of SYLD.

Data by YCharts

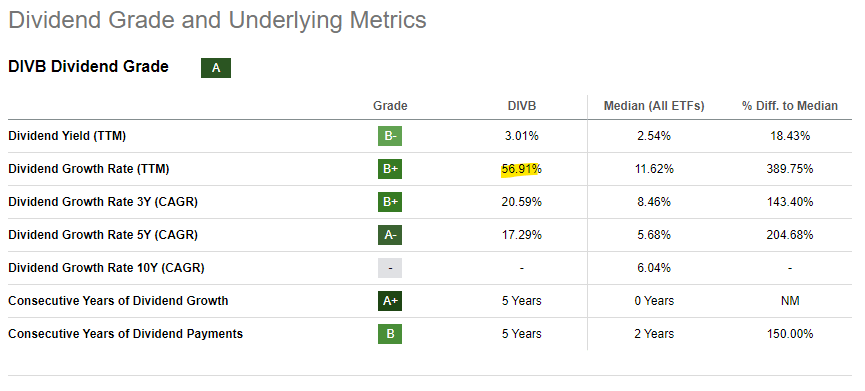

DIVB’s dividends have seen very healthy growth since inception as well. Growth was particularly strong this year, reaching 56.9%.

Seeking Alpha

On a more negative note, and from what I’ve seen, dividend growth was mostly due to portfolio turnover, and so might not necessarily persist into the future.

Performance Analysis

DIVB’s overall performance track-record is decisively below-average, but a bit complicated.

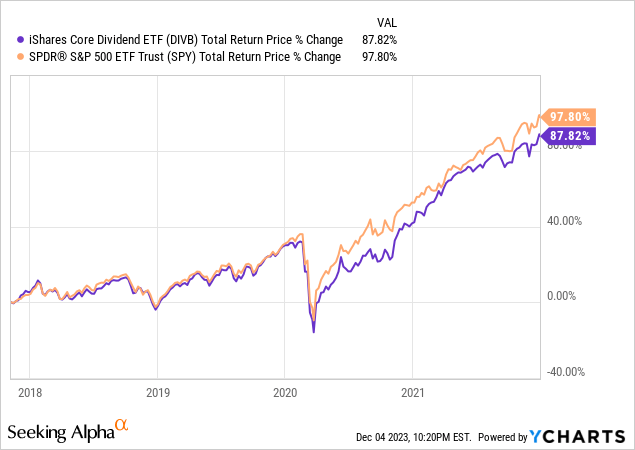

Based on prior coverage, it seems that DIVB used to track the S&P 500 much more closely. Overlaps were much higher, with both the fund and the index focusing on the same holdings and industries, and with similar weights in both. Performance was very similar too, with DIVB somewhat underperforming from inception to 2022, almost entirely due to above-average pandemic losses.

Data by YCharts

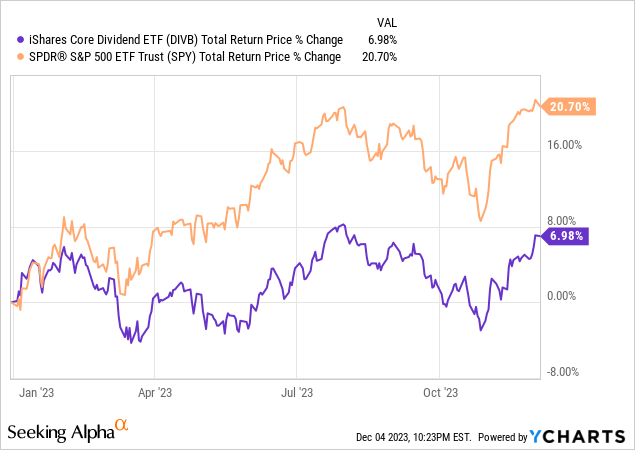

DIVB started to more strongly diverge from the S&P 500 sometime between early 2022 and early 2023, with the fund significantly underperforming its index YTD. The broad similarities in their performance remain apparent, however.

Data by YCharts

In any case, the fund underperformed the S&P 500 when their portfolios were quite similar, and when the portfolios started to diverge.

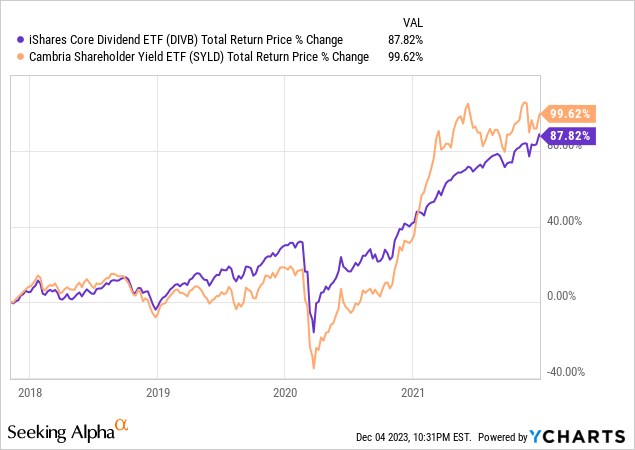

Compared to SYLD, the situation is flipped. DIVB used to perform somewhat differently from SYLD before 2022, as DIVB was much more similar to the S&P 500 in prior years. Long-term returns were similar, but the graphs do look very different.

Data by YCharts

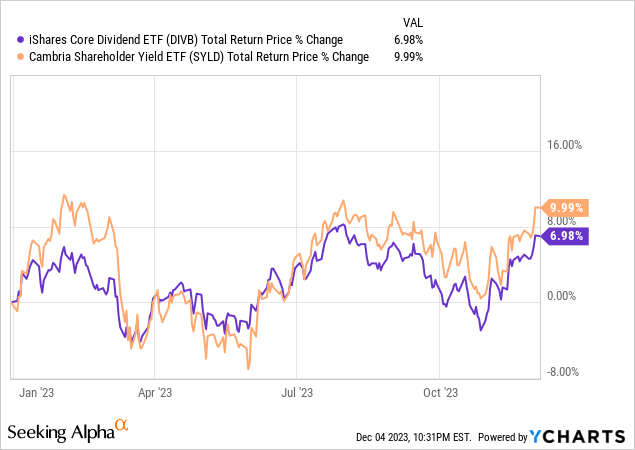

Recent portfolio changes have caused DIVB to perform much more similar to SYLD.

Data by YCharts

Still, DIVB underperformed relative to SYLD when the fund closely tracked the S&P 500, and when it started to diverge from the index.

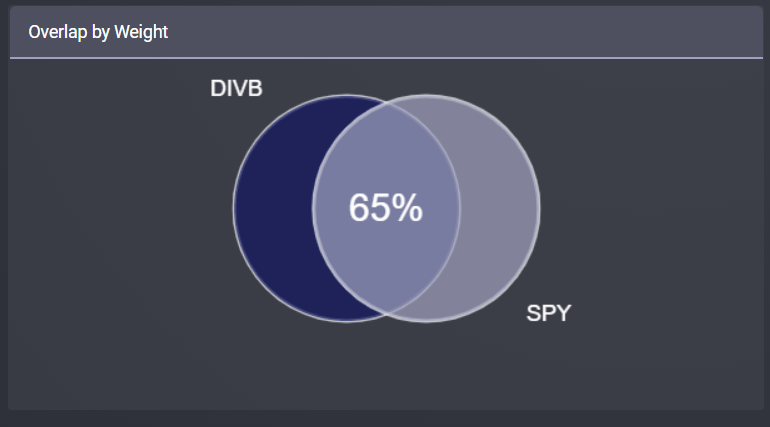

Although dividing the fund’s performance track-record in the manner above seems a bit odd, I do think it is appropriate. DIVB was much closer to the S&P 500 in the past. In fact, when I first wrote about the fund, their overlap by weight was about twice as high:

Etfrc.com

Compared to now:

Etfrc.com

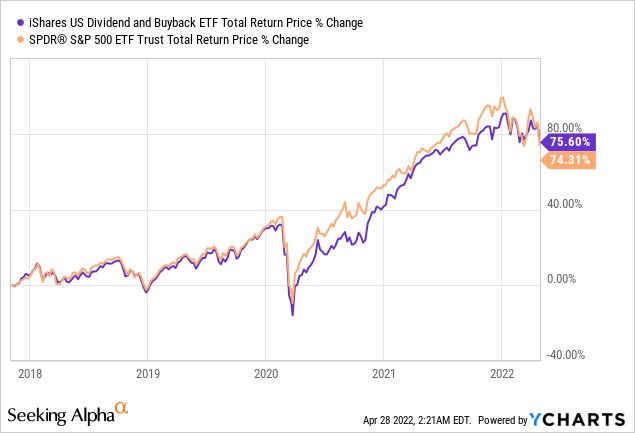

and their performance had been effectively the same since inception:

Data by YCharts

DIVB’s portfolio has changed quite a bit in the recent past, as has its performance. This matters, in my opinion at least.

Regardless of the above, DIVB has tended to underperform relative to both the S&P 500 and SYLD. The latter seems of particular importance, as SYLD follows a similar strategy, but with a clearer, stronger focus on companies with particularly high shareholder yields. SYLD’s strategy has worked better in the past, and I have no reason to believe that this will change moving forward.

Conclusion

DIVB is an equity index ETF, investing in U.S. equities with above-average dividend payments and share buyback programs. Although there is nothing significantly wrong with the fund, SYLD seems broadly superior. As such, I see no reason to invest in DIVB.

Q2 2024 Earnings Call Transcript")