Marvin Samuel Tolentino Pineda/iStock Editorial via Getty Images

Introduction

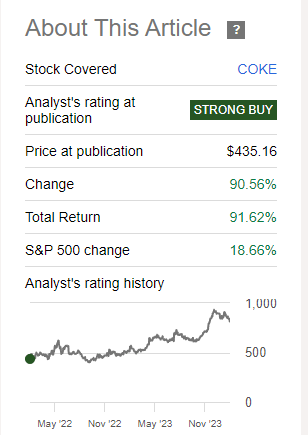

Sometimes the best investments are the ones that don’t need a lot of attention. I last discussed Coca-Cola Consolidated (NASDAQ:COKE) in February 2022 and rated it a ‘strong buy’. The share price has performed really well in the past two years as the stock is up by in excess of 90% compared to a total performance of the S&P 500 of less than 20%.

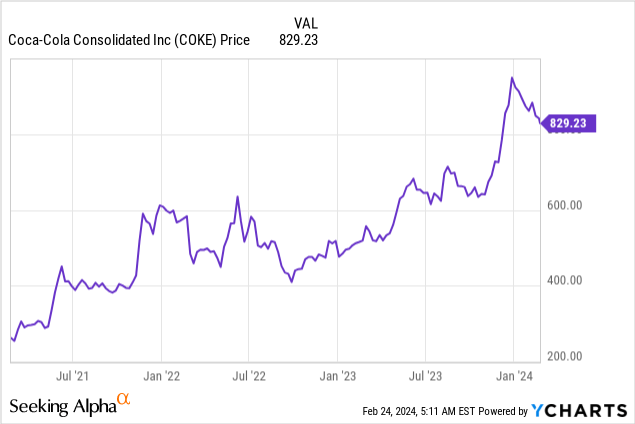

Seeking Alpha

As I am looking to cash up my portfolio, I wanted to check if I need to take any action on this position.

As a reminder, Coca-Cola Consolidated is a marketer, producer and distributor of Coca-Cola (KO) products in certain areas of the United States, serving approximately 60 million customers with products from 10 manufacturing plants and 60 distribution centers.

The cash flow remains strong

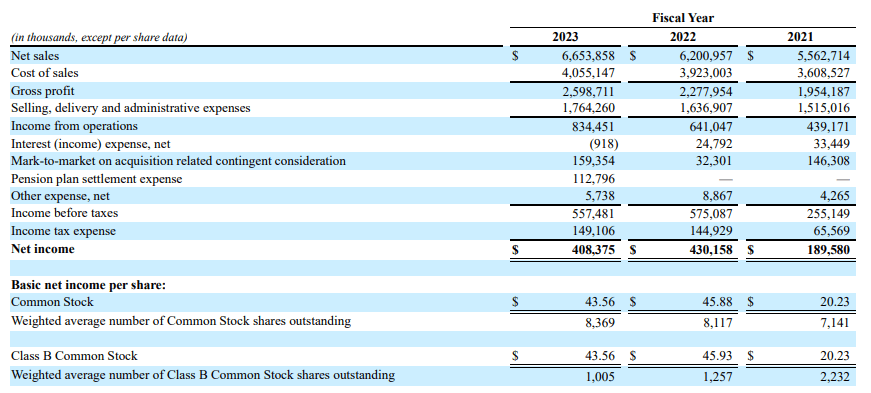

In 2023, COKE reported a total revenue of $6.65B, which represents an increase of just over 7% compared to the $6.2B it generated in 2022. The gross profit increased by approximately 14% to just under $2.6B and although the selling, delivery and administrative expenses also increased, the operating income increased by approximately 30% to $834M.

COKE Investor Relations

That’s a very impressive performance, as the company has now almost doubled its operating income in the past two years.

Unfortunately, this didn’t mean the company reported a profit explosion. As you can see in the income statement, it recorded a $159M cost related to a previous acquisition, while there also was a $113M expense related to the settlement of the pension plan. The $113M settlement covered the actuarial losses, which means there no longer is any unfunded liability related to the plan.

That weighed on the results, and the pre-tax income as well as the net income actually came in lower than the previous year. The EPS of $43.56 was certainly disappointing, but it is clear it was impacted by non-recurring items.

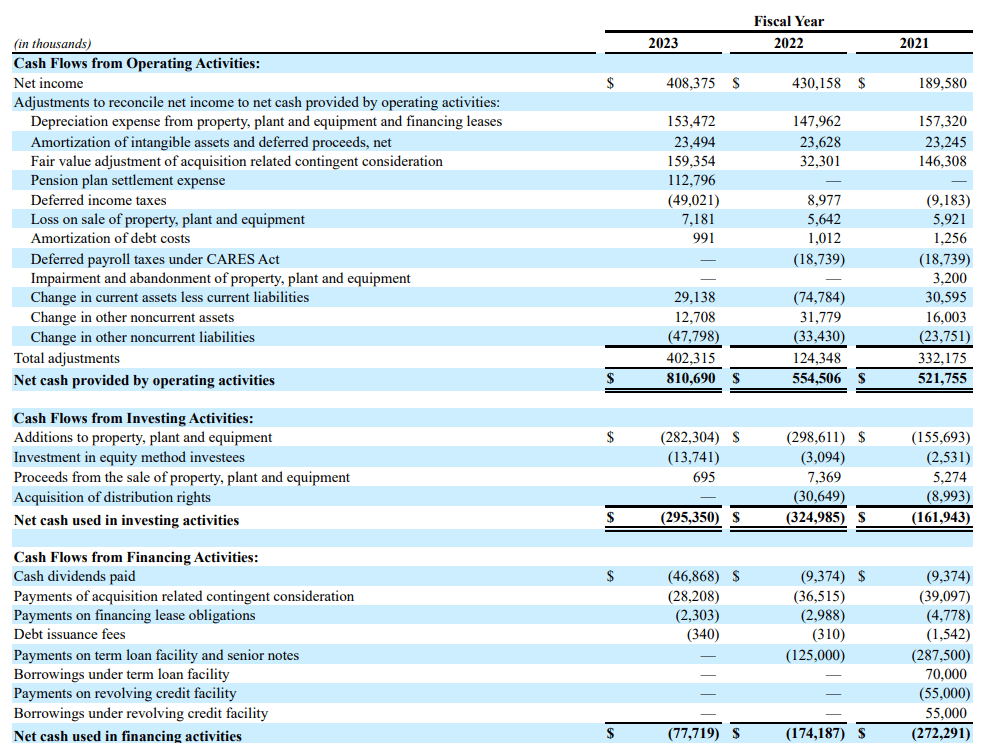

In the previous articles I mainly focused on the cash flow performance of the company as that ultimately drives COKE’s ability to continue to invest. The cash flow statement below indicates the operating cash flow was just over $810M, but there also was a $35M investment in the working capital position, while we also should deduct the $2.3M in lease payments. This means that on an adjusted basis, the operating cash flow was $843M. Keep in mind this also includes the payment of $49M in deferred taxes, while the $149M tax payment in 2023 was already relatively high as some elements were non-deductible. So on a normalized underlying basis, I’d argue the operating cash flow was actually closer to $900M.

COKE Investor Relations

The total capex was $282M, and this means the underlying free cash flow was approximately $610M. And divided over the current share count of 9.4M shares (a combination of common shares and Class B shares), this means the free cash flow came in at approximately $65/share. Which means that at the current share price of $829/share, the free cash flow yield is still a very respectable 7.8%.

The strong cash flows obviously also helped the balance sheet. At the end of December, COKE had in excess of $630M in cash on the balance sheet, while the total amount of long-term debt was just $599M. This means Coca-Cola Consolidated ended 2023 with a net cash position, and that is an enviable position to be in. The next debt maturity date is in November 2025 when the 3.80% senior bonds mature. The total issue size was $350M and if Coca-Cola Consolidated would just repay these bonds rather than refinancing them, it would save approximately $13.3M in interest expenses and add in excess of $1 to its free cash flow result per share on an after-tax basis. But thanks to the high cash position and the fixed coupons on the debt, COKE actually reported a positive net interest income during 2023.

Investment thesis

With an EBITDA of approximately $1.01B (defined as income from operations plus the depreciation and amortization expenses added back to the equation), the company is still trading at less than 8 times its EBITDA. This, in combination with the strong free cash flows and attractive free cash flow yield of almost 8% still makes COKE a buy. The special dividend of $16/share was a nice touch, but still represents a very small part of the net income and free cash flow for the year.

That being said, I may sell a portion of my position. Not because the company is unattractive, but because of my personal portfolio management style. I am looking to increase my cash position, and selling a portion of a stock that has almost doubled also helps to lock in a nice win.

Q2 2024 Earnings Call Transcript")