Sundry Photography

Introduction & Investment Thesis

Cloudflare (NYSE:NET) is a provider of cloud-based services that secure internet properties. The company produced stellar results in its latest Q4 FY23 earnings report, beating both the top and bottom-line expectations. The company has a terrific track record of driving a 46% compounded annual growth rate (CAGR) in revenue since FY2018 and has recently seen tremendous success in driving market penetration among enterprise customers that contribute at least $100,000 in Annualized Revenue.

At the same time, the management has continued to demonstrate its commitment to improving profitability as it becomes more efficient, driving deeper product adoption, and streamlining its operating expenses.

While the long-term growth thesis of the company is intact given the large TAM with an innovative product portfolio and improving margins, the current valuation of the company suggests that the stock is priced to perfection, leaving little room for execution error for the company’s management. As a result, I will rate the stock a “Hold” at the moment.

About Cloudflare

Cloudflare is a web security and network protection services company whose products are designed to keep internet properties such as websites and internet applications free from cyber attacks and other online threats. The company also provides network security services without the need to purchase any hardware that its competitors, such as Fortinet (FTNT) and Palo Alto Networks (PANW), may require in order to secure networks.

In addition, the company bundles its offerings into a network-as-a-service cloud subscription package, which it sells to its customers. The company operates a combination of a freemium model and direct sales to attract and acquire customers into its sales funnel.

In the past year, the company has also restructured its sales team to target enterprise customers, which has started to boost Cloudflare’s performance, which will be discussed in the next section. The company generates revenue from a combination of periodic subscriptions and usage-based consumption models from its customers.

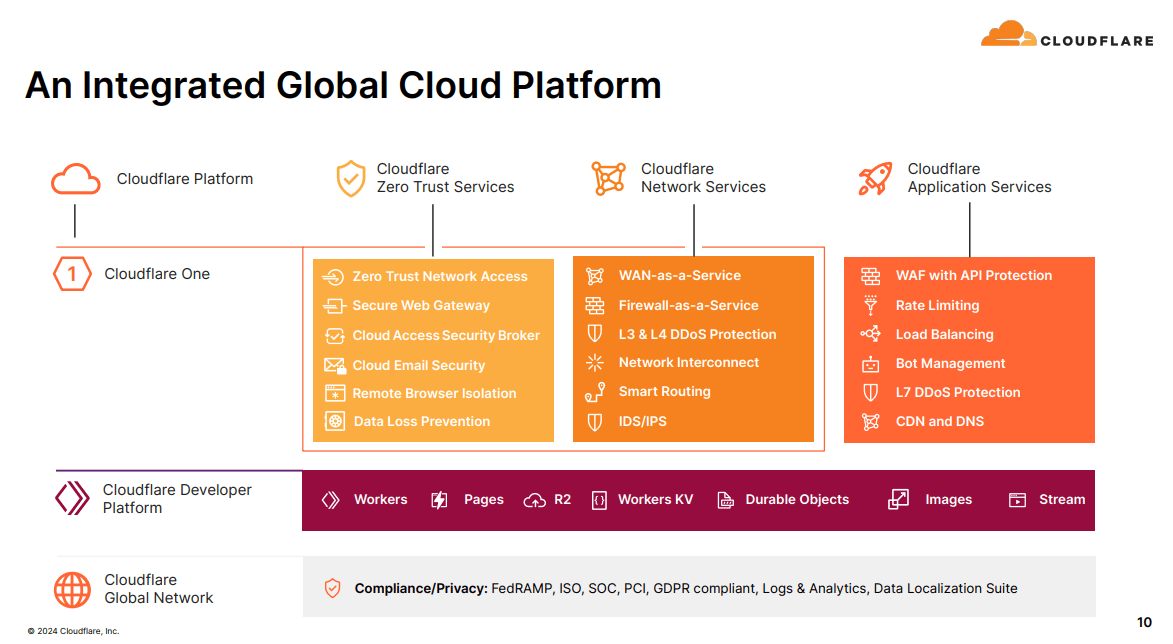

Q4 FY23 Earnings Slides: Cloudflare’s integrated product portfolio of web applications & network security

The Good: Cloudflare Outperformed On All Fronts In Its Q4 Earnings

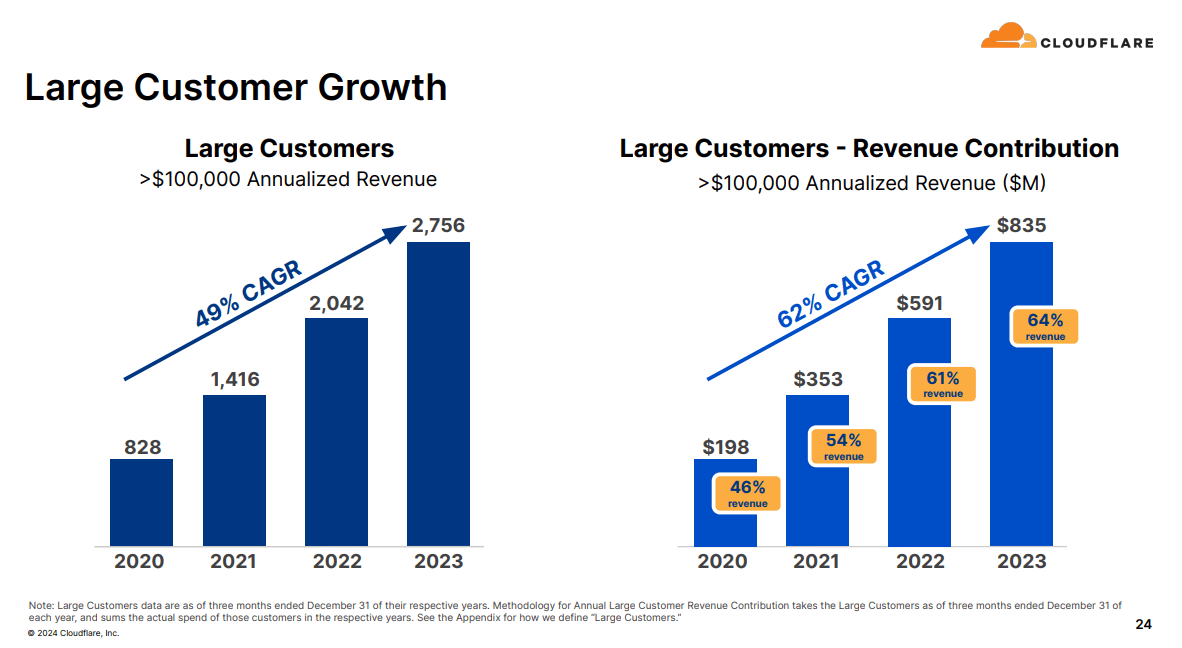

Total revenue for Cloudflare grew by 33% YoY at $1296.7M, beating their own prior forecasts while slightly beating consensus revenue estimates of $1290M. The number of Paying Customers increased by 17% compared to the same period last year. But the strength of Cloudflare’s go-to-market strategy was on full display amongst its Large Customer cohort ($100,000 or more in Annualized Revenue) that grew 35% YoY and contributed 64% to Total Revenue, compared to 61% the year before.

Q4 FY23 Earnings Slides: Cloudflare’s Market Penetration among Enterprise Customers

These were some very strong numbers to show that Cloudflare is having significant success in penetrating the large enterprise market segment as the size of deals is increasing. In addition, management also credited the success of their Zero Trust Architecture (ZTA) cybersecurity products, which gained significant appeal among Cloudflare’s new customers. Moreover, Cloudflare’s Net Retention Rate continues to stabilize at the 115% mark. I believe this confluence of factors is a very encouraging development in Cloudflare’s prospects to consistently outperform in the future, with the management projecting FY24 revenues to grow 27% to $1.65B.

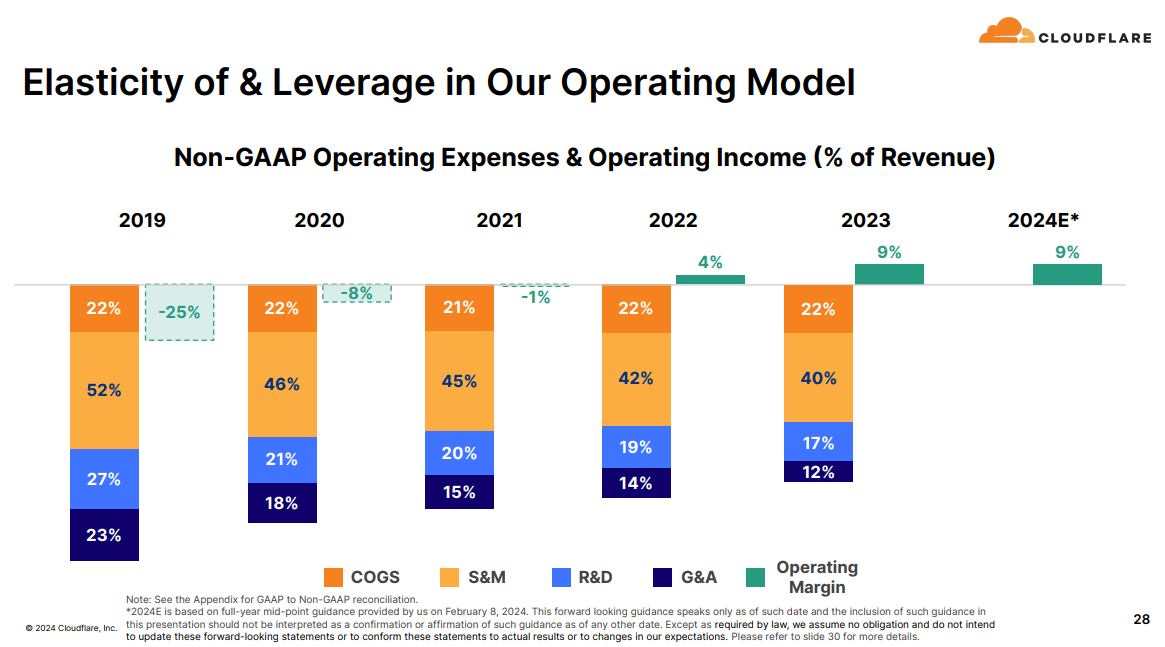

For the full year FY23, Cloudflare’s non-GAAP earnings were 49 cents per diluted share, up 277% from 13 cents per diluted share a year earlier. While full-year gross margins fared slightly better at 78.3%, the company’s non-GAAP operating margins saw some significant expansion, from 3.7% in FY22 to 9.4% in FY23, as the company streamlined its operating expenses on all fronts. The company continues to expect margins to normalize through 2024 and has guided non-GAAP operating margins to be flat on a YoY basis.

Q4 FY23 Earnings Slides: Cloudflare’s margins expanded on a year-on-year basis

The Bad: The Competitive Landscape May Dampen Cloudflare’s Growth Prospects

Although the company outperformed and guided FY24 projections above consensus expectations, management sought to temper optimism by cautioning against a highly uncertain macro environment. Cloudflare had already read the tea leaves earlier and had taken measures early last year to move upmarket by targeting large enterprises in their target market. The approach appears to be paying off, in my view, with the strong growth that Cloudflare saw in the enterprise segment.

In addition, Cloudflare has seen success in demand for its Access ZTA product, which was discussed during the Q4 call. But its past success may not always translate to future achievements, as the ZTA market is an emerging technology within cybersecurity and heavily contested by other industry players. While large hyperscalers such as Google and Amazon provide singular ZTA solutions for their own respective cloud platforms, Cloudflare directly competes with very successful cybersecurity players such as Zscaler (ZS) and Palo Alto Networks. Since ZTA is an emerging technology, Cloudflare may be forced to invest significantly more in their Sales & Marketing spend lines to continue to penetrate the enterprise market for cybersecurity solutions.

Tying It Together: Cloudflare Is Priced To Perfection

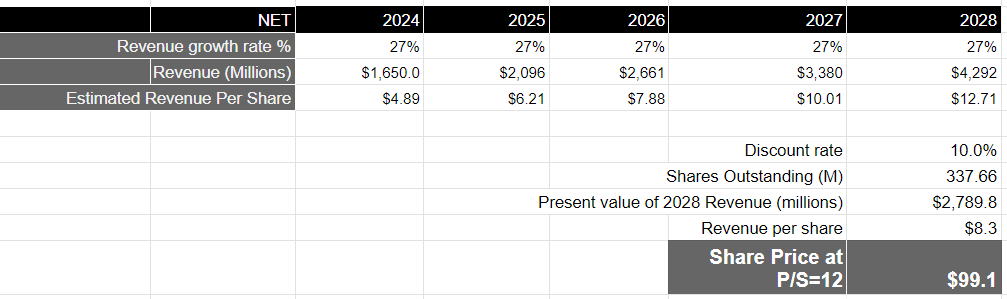

Cloudflare is trading at a forward price-to-sales ratio of 25 based on management’s expectation for FY24 revenue. The management has also provided a long-term operating model where it expects the company to significantly improve its non-GAAP operating margin from 9.5% to 20%. This would mean that we would see Cloudflare’s earnings outpace its revenue growth over the coming years as the company streamlines its Sales & Marketing spending to 28% of total revenue over the course of the coming years. However, since the management has not specifically stated the fiscal year when it realizes such a magnitude of operating leverage, I am going to base my valuation on my revenue growth estimate over a 5-year investment horizon.

In this case, if I assume that Cloudflare grows its revenue in the high-20s range over the next 5 years, as it penetrates deeper into the large enterprise customer cohort coupled with stronger customer adoption of its product portfolio, it should be able to produce approximately $4.3B in revenue by FY28.

This translates to a present value of $2.8B in revenue, when discounted at 10%, or a revenue per share of $8.3. Taking the S&P 500 as a proxy, where its companies have grown their revenues at an average rate of 4.8% with a price-to-sales ratio of 2.19 over a 10-year period, I would assume that Cloudflare should be trading at 5-6x the forward price-to-sales multiple of the S&P 500.

That would mean that the stock should be trading at approximately $99, which would mean that the stock is currently priced to perfection. In my opinion, it does not provide an attractive entry point for long-term investors, given the risk-reward of the company.

Author’s Valuation Model

Conclusion

Cloudflare has thus far executed exceptionally, and this has driven a lot of investor optimism in the stock’s current price. There are undoubtedly a lot of tailwinds that the company has at the moment, given its continuing success in driving new acquisition growth in the enterprise customer segment while deepening adoption among existing ones. The company management also believes that Cloudflare should be able to see robust expansion in operating margins, although the timeframe is unknown. However, competitive forces remain a threat despite the company’s robust product innovation pipeline. Given the above, I believe that the long-term growth prospects of the company are currently baked into the valuation, leaving no room for upside at the moment.

Q2 2024 Earnings Call Transcript")