felixR

Investment thesis

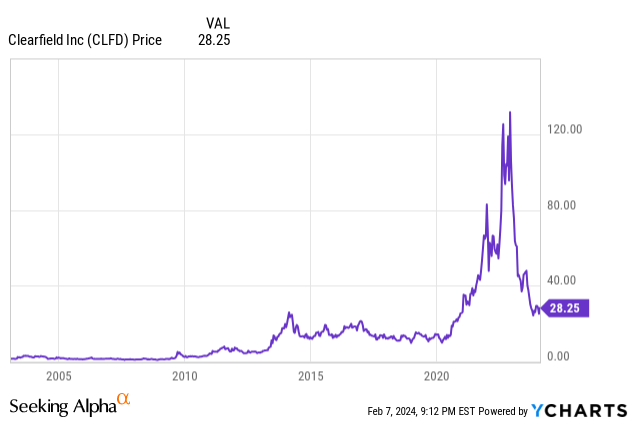

After strong fiscal 2021, 2022, and 2023, Clearfield (NASDAQ:CLFD) is currently suffering a rebound effect as customers have excess inventories and are postponing orders. Net sales fell by 60.17% year over year in Q1 2024 and profit margins have plummeted due to lower volumes, pushing the EBITDA margin well into negative territory. As a consequence, investors are very pessimistic compared to fiscal 2021, 2022, and H1 2023, and the share price already trades 79% below all-time highs reached in November 2022. Still, things are not that bad and, in reality, what the company is currently facing is a stabilization after three years of exceptionally high demand, so it is important to look at the current situation and not consider the recent performance as a trend. That is why, despite the recent fall, the share price is still 51% above the close of 2019 (before the coronavirus pandemic).

Following the strong demand for fiber optic products during the coronavirus pandemic and the subsequent reopening of the global economy, customers increased orders even further to build significant inventories in 2022 and 2023 to prepare for the high demand expected from 2025 when projects under the Broadband Equity Access and Deployment (BEAD) program, which is endowed with $42 billion, begin receiving funding. As a consequence, customers now find themselves with excess inventory. Furthermore, tightening financing conditions have temporarily paused many infrastructure projects, with which Clearfield is suffering a very significant decrease in orders.

The company expects public financing through the BEAD program to reverse this trend in 2025 as customers are expected to increase their activity through 2030. Meanwhile, the company has a very robust balance sheet and very high inventories as it issued shares in Q1 2023 to build working capital, which should allow it to withstand the current scenario and meet the expected increase in demand in the medium term, which is why I consider the recent share price decline to be a good opportunity, for those investors with enough risk tolerance, to start a position and wait for a potential turnaround as potential capital returns are significant at this point.

A brief overview of the company

Clearfield is a North American manufacturer of fiber protection, fiber management, and fiber delivery solutions for the broadband service provider industry. The company was founded in 1979 and its market cap currently stands at $415 million as it employs around 400 full-time workers, with insiders owning 15.68% of the outstanding shares.

Such high insider ownership is positive for investors as the management actively participates as shareholders, so they will also benefit from a potential good share performance. The company is constantly launching new products to adapt to the ever-changing needs of the industry, and it enjoys some geographical diversification as 81% of revenues were provided by operations within the United States in fiscal 2023, whereas the rest took place in international markets, mainly Europe, Canada, Mexico, and Caribbean Markets. Despite this, the current situation is somewhat delicate, which is why the share price has deflated in the last year.

The return to normality after a time that has turned out to be too good to be true has caused a share price decline of 79.06% from all-time highs reached in November 2022 to $28.25. This reflects the recent slowdown in demand as customers are emptying their high inventories while waiting for BEAD to start funding projects. In some way, I believe investors hoped that sales would not decline significantly before the beginning of BEAD even though some stabilization was expected. In this regard, sales are expected to begin increasing in 2025 once customer inventories return to normal levels and demand picks up again, which is why the recent share price is still 50.65% above the $13.94 with which 2019 (the year before the outbreak of the coronavirus pandemic) closed.

Recent acquisitions

Certainly, the company has not been very active in its M&A strategy as it has focused much of its efforts on product launches and the expansion of its manufacturing capacity. Only two acquisitions have taken place in the recent past, and these have been relatively small in size.

In February 2018, the company acquired a portfolio of outdoor-powered cabinet products from Calix (CALX) for $10.35 million, and four and a half years later, in July 2022, it also acquired Nestor Cables, a Finnish manufacturer of fiber optic cable solutions with customers in over 50 countries, for $23 million. This latest acquisition was very important to Clearfield from a strategic perspective as, apart from generating revenues for themselves, Nestor Cables has been a cable provider to Clearfield for its FieldShield product line in North America for over a decade, and the management plans to use its manufacturing capacity to support the growing demand expected in the future in North America, for which it started manufacturing Nestor products in Mexico.

Revenues are taking a break before the beginning of the BEAD project

The company has managed to increase its sales over the years thanks to the expansion of its production capacity, the launch of new products, and acquisitions as the Nestor Cables segment provided 16% of revenues in fiscal 2023. The most significant increases took place in the last 3 years as the coronavirus pandemic brought a significant increase in demand for fiber optic products while customers increased their inventories to prepare for future (expected) increased demand. In this regard, the company reported a 51.23% increase in fiscal 2021, a further 92.45% increase in fiscal 2022, and just a slight 0.80% decline in fiscal 2023.

Clearfield revenue (Seeking Alpha)

Even so, the company reported a 47.72% decline year over year in Q4 2023, and this decline intensified in Q1 2024 as revenues decreased by 60.17% year over year as customers still had excess inventory. Recent interest rate hikes have also played a determining role in the delay in orders as customers and consumers are postponing projects due to the current strict financing environment, and the management doesn’t expect a turnaround until at least fiscal 2025.

Order backlog decreased by 68% year over year in Q1, but this should not be seen as a future revenue indicator as lead times decreased from 6-8 weeks in Q1 2023 to just 4 weeks in Q1 2024. In this regard, the management expects a 54% to 59% decrease in revenues in Q2 2024, and demand is expected to start slowly recovering in H2 2024 as revenues are expected to decrease by 45% in fiscal 2024 (compared to fiscal 2023) but to increase by 36% in fiscal 2025. Globally, the trend plays in favor of Clearfield as the fiber optic cable market is expected to grow at a CAGR of ~9.5% in the 2023-2028 period.

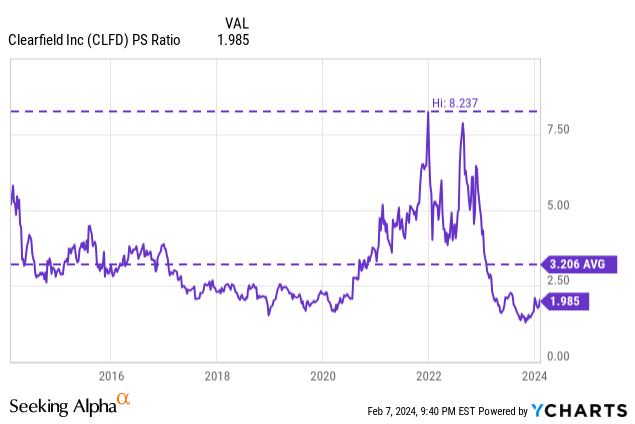

As for now, investors have greatly lowered their expectations while remaining cautious as the impact that BEAD will have on sales between 2025 and 2030 is difficult to predict and measure, which has caused a steep decline in the P/S ratio to 1.985. This means that the company generates $0.50 for each dollar held in shares by investors, each year.

This ratio is 38.08% below the average of the past 10 years and represents a 75.90% decline from the 8.237 peak reached at the end of 2021. Although the average of the last 10 years is strongly influenced by the strong optimism of recent years, the current ratio is in the low range experienced before the coronavirus pandemic as 2025 is expected to close with revenues ~8.4% lower than the current trailing twelve months. Additionally, the recent decline in volumes has caused a huge contraction in profit margins, which is putting significant pressure on operations as the company is temporarily unprofitable.

Margins are temporarily depressed

The company expanded its manufacturing capacity to Mexico in 2014 to lower production costs and has been increasing it since then. The latest upgrade took place in July 2021 when the company announced its expansion through a lease arrangement for a 319,000-square-foot manufacturing and warehouse center, which was put into operation in 2022 to face the growing demand experienced while reducing production costs.

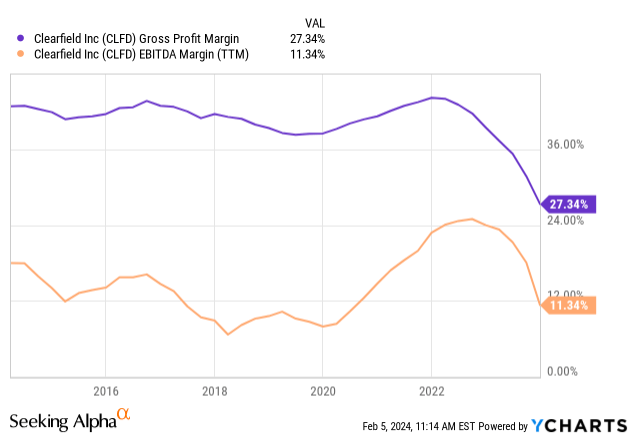

Despite these efforts, lower volumes, which are added to inflationary and wage pressures, are squeezing margins as the trailing twelve months’ gross profit margin currently stands at 27.34% and the EBITDA margin at 11.34%.

But this is not the end of the story as the company reported a gross profit margin of only 13.72% in Q1 2024 while the EBITDA margin entered negative territory at -12.85%. Indeed, this is not surprising as the company has not had material time to adapt its production capacity (i.e. reduce labor) to the current landscape, which changed too quickly. What’s more, higher-than-usual inventories are causing an increase in storage costs.

Now, efforts are focused on reducing storage and product deployment costs, which is setting the roadmap in terms of product innovation. For this purpose, the company launched CraftSmart Fiber Protection Vault in January 2024, which is expected to improve shipping and inventory space by 300%. Meanwhile, it keeps increasing its microduct manufacturing capacity as it delivers higher margins while its demand is expected to increase in the future.

Additionally, the company plans to reduce its workforce to adapt to the new lower-demand environment, which should begin to be noticed in H2 2024 as the management expects demand to start picking up. Also, the company’s H2 is typically stronger compared to H1 due to seasonality, which should relax operations a bit while workforce reductions are carried out and the market (customer inventories) stabilizes.

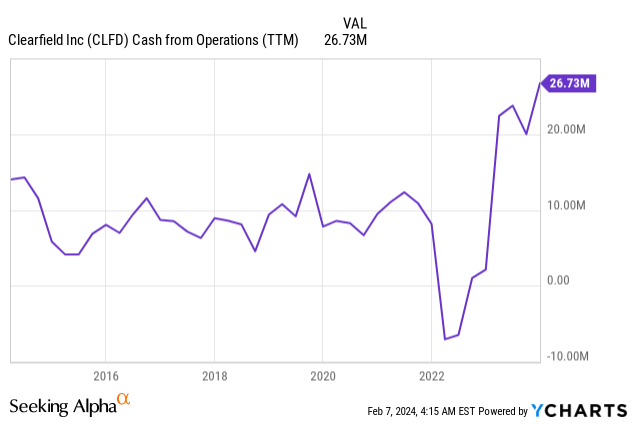

Fortunately, inventories accumulated since 2020 should allow for a significant reduction in the workforce, which should eventually improve profit margins to healthier levels. Furthermore, these inventories should keep the company generating relatively healthy cash from operations for a long time despite the current complex situation of the industry, which greatly reduces short-term risk.

In this regard, the company is currently generating significant cash from its operations, albeit in an unsustainable way. Cash from operations was $7.8 million in Q1 2024 compared to $1.1 million in Q1 2023, which was achieved thanks to a reduction of $3.5 million in inventories and a $11 million reduction in accounts receivable while payables were reduced by only $1.1 million, which essentially means that the company is not currently profitable.

Despite this, the balance sheet remains robust, so the company still has plenty of resources to continue navigating the current situation for a long time.

A very strong balance sheet will sustain operations until headwinds relax

As a consequence of the recent margin squeeze, and despite positive cash from operations, the company is not profitable as it reported a negative net income of -$5.3 million in Q1 2024 (vs. $2.7 million reported in Q4 2023 and a positive $14.3 million in the same quarter of 2023).

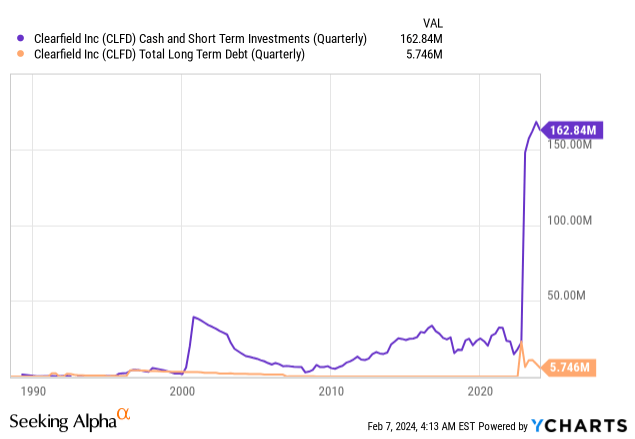

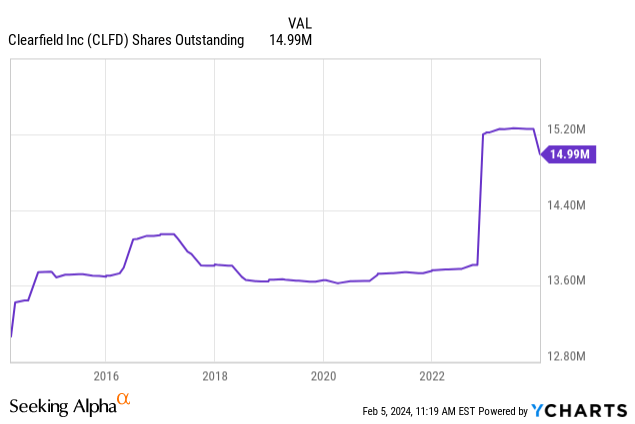

Despite this, the balance sheet is very strong as it holds $162.8 million in cash and short-term investments and virtually zero debt (net debt is currently at -$143.3 million), which has been possible thanks to the share dilution experienced in Q1 2023. For this reason, the management decided to take advantage of the lower share price to buy back $12.4 million worth of shares during the quarter.

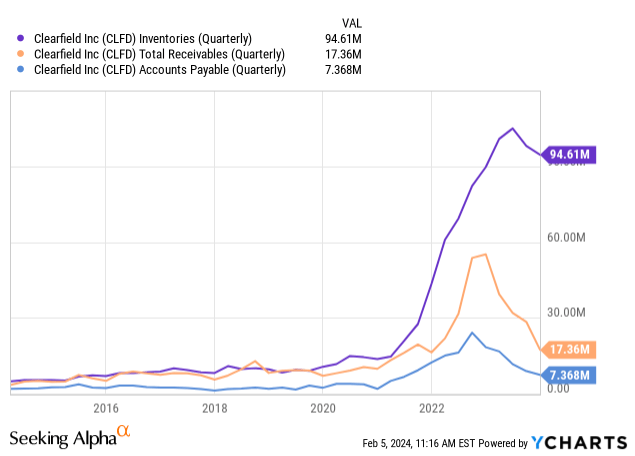

But as I mentioned before, not only are cash and short-term investments high, but inventories are also high as the company has accumulated $105.0 million in recent years, of which it has already used $10.4 million, leaving inventories at $94.6 million. Additionally, accounts receivable of $17.36 million are well above the $7.37 million in accounts payable.

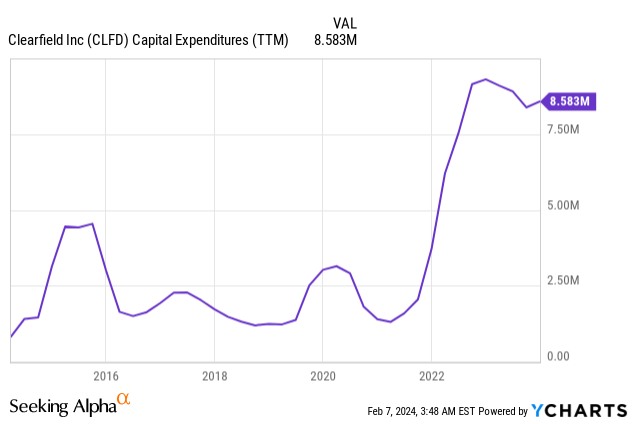

Coinciding with the beginning of capacity expansion efforts in Mexico in 2021, the trailing twelve months’ capital expenditures have increased to $8.58 million as the company has now more equipment to maintain. Still, part of this increase is also due to the strong investments that the company is making in the recently acquired Nestor Cables as the management is upgrading the manufacturing equipment and launching new products with higher profit margins.

Therefore, I consider that the company is prepared to withstand current headwinds for a very long time, and the management has already begun to undo part of the share dilution as the main purpose of share issuance in calendar 2022 was to keep up with increasing demand (in 2021-2023) and build inventories to prepare for a greater-demand environment from 2025 to 2030. In this regard, it now seems a good time to start repurchasing those shares to undo part of the dilution.

Share repurchases

The company issued $131.5 million worth of shares in Q1 2023 to build working capital, which has made the balance sheet so robust today, and the total number of shares outstanding increased by 1.401.184 (or 10.13%) during that quarter. This means that the company received ~$93.85 for each share issued, which is much higher than the price at which the management is currently repurchasing them.

As the share price continued decreasing, the company increased the share repurchase authorization from $22 million to $40 million in November 2023, which left $33 million left at available for repurchases at that time.

Since then, the management repurchased $12.4 million worth of shares in Q1 2024, leaving an additional $21 million authorized, although it seems that it will be expanded soon as suggested in the earnings call conference as the current share price is seen as abnormally low by them. In this sense, it seems that the management has been very careful with the timing of repurchases so far, which reflects a strong knowledge of the business and the industry.

Risks worth mentioning

Before any potential investor decides to purchase Clearfield shares, I would like to remind you that this is a highly speculative investment given the company’s current situation. Next, I would like to highlight those risks that I consider most significant, especially for the short and medium term.

- At this point, the company’s success in the medium term depends on whether the deployment of funds under the BEAD program will translate into a significant increase in revenues from 2025. If this is not the case, the company’s prospects could worsen significantly and the share price would likely decrease further due to an increase in the pessimism among investors.

- Recent interest rate hikes could cause a global recession, which could have a significant impact on sales and hamper the recovery.

- If the company fails to recover a significant portion of the sales lost in recent quarters or if it fails to sufficiently reduce its workforce in the short and medium term, it could have difficulty emptying its inventories, which would likely damage the balance sheet due to negative cash from operations caused by unabsorbed labor and higher expenses derived from storing said inventory.

- 16% of net sales were provided by the company’s largest customer in fiscal 2023, and therefore, a decrease in orders from this customer, as well as the cessation of its relationship with Clearfield, could have a significant impact on the company’s sales.

- The management could pause share buybacks if the situation does not improve in the short and medium term as the balance sheet will keep deteriorating until current headwinds ease, which could limit the opportunity to undo recent share dilution.

Conclusion

The recent drop in sales and the current margin contraction due to lower volumes, although very steep, is not (in my opinion) a cause for concern. Clearfield customers are currently holding very high inventories following accelerated demand in fiscal 2021, 2022, and 2023, so they have decided to postpone new orders until they clear inventories to healthier levels. Furthermore, the macroeconomic situation has also led to the current situation due to much tougher financing conditions compared to previous years and the upcoming financing rounds under the BEAD project that is temporarily leaving the industry on hold.

Hence, I consider that current headwinds are caused by the macroeconomic landscape and not so much by company-specific factors, and the balance sheet is robust enough to continue navigating them for a very long time. The company managed to issue shares at much higher prices than current ones, which allowed the management to start repurchasing them at much lower prices. This movement allowed the company to prepare the balance sheet for the current headwinds, which were already expected as customers were massively building inventory, without causing too much share dilution.

Regarding margins, I understand that the company has not had enough time to reduce its workforce as revenue declines have been very severe and have continued to this day. As the quarters go by, it should start reporting better margins as the expected labor reduction materializes and demand picks up. For this reason, I consider that the recent drop in the share price represents a good opportunity for those investors with sufficient risk tolerance to wait patiently for the company’s prospects to improve and thus the optimism among investors.

Q2 2024 Earnings Call Transcript")