ymgerman

Introduction

From what I can tell, Citigroup has only three listed “preferreds” still outstanding after calling many of the others since 2000. One is a standard Preferred Stock, the Citigroup Inc. DEP SHS 1/1000 J (C.PR.J). The other is a debenture known as Trust Preferred stock: Citigroup Capital XIII – FXDFR PFS REDEEM 30/10/2040 USD 25 (CPRN). After a brief overview of Citigroup itself, I will compare the two Citigroup listed issues and render my verdict as to the better investment at this point. There is also a legacy Travelers TruPS but only 200k shares exist. Their website also shows several non-listed preferred stocks.

Years ago I owned several assets known as Trust Preferreds. Here is how those assets are defined:

Trust preferred securities (TruPS) were hybrid securities issued by large banks and bank holding companies (BHCs) included in regulatory tier 1 capital and whose dividend payments were tax deductible for the issuer.

The bank would open a trust funded with debt; then, the bank would carve up shares of the trust and sell them to investors in the form of preferred stock. The resulting stock was called a trust preferred security or TruPS.

First issued in 1996, TruPS became the subject of increased regulatory scrutiny following the 2008-09 financial crisis. As a result of the Dodd-Frank reforms and the Volcker Rule, most of these were phased out at year-end 2015.

Source: investopedia.com/terms

Screening Quantumonline.com, I found 18 Trust preferreds, though many of those are in default currently. One, brought to my attention by a reader, is the CPRN covered here. Bank of America was the only other bank showing an outstanding TruPS, and BOA told me it was an institutional-only issue.

Citigroup review

Seeking Alpha describes this bank as:

Citigroup Inc., a diversified financial services holding company, provides various financial products and services to consumers, corporations, governments, and institutions in North America, Latin America, Asia, Europe, the Middle East, and Africa. It operates through three segments: Institutional Clients Group (“ICG”), Personal Banking and Wealth Management (“PBWM”), and Legacy Franchises. The ICG segment offers wholesale banking products and services, including fixed income and equity sales and trading, foreign exchange, prime brokerage, derivative, equity and fixed income research, corporate lending, investment banking and advisory, private banking, cash management, trade finance, and securities services to corporate, institutional, and public sector clients. The bank traces its lineage back to 1812.

Source: seekingalpha.com C

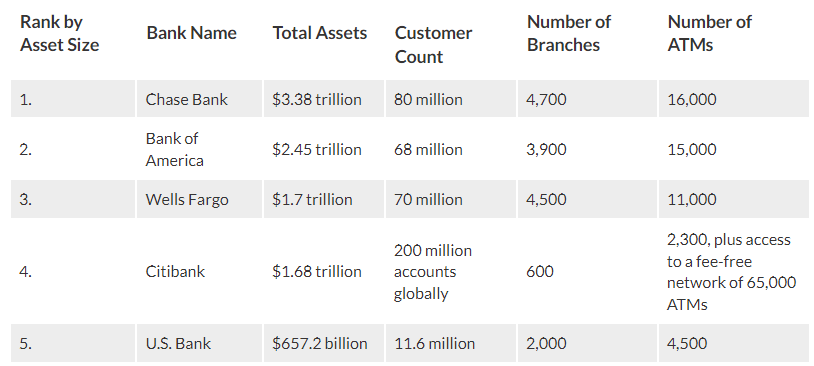

Currently, Citibank is the fourth-largest bank in the US based on Total Assets, slightly behind #3 Wells Fargo, way ahead of #5, US Bank.

marketwatch.com/guides/banking/largest-banks-in-the-us

Based on the number of branches and ATMs, Citibank appears to have a different consumer strategy than its larger competitors. Looking at the Citigroup 2022 Annual Report shows Institutional Clients provided 3X the income that Personal Banking did.

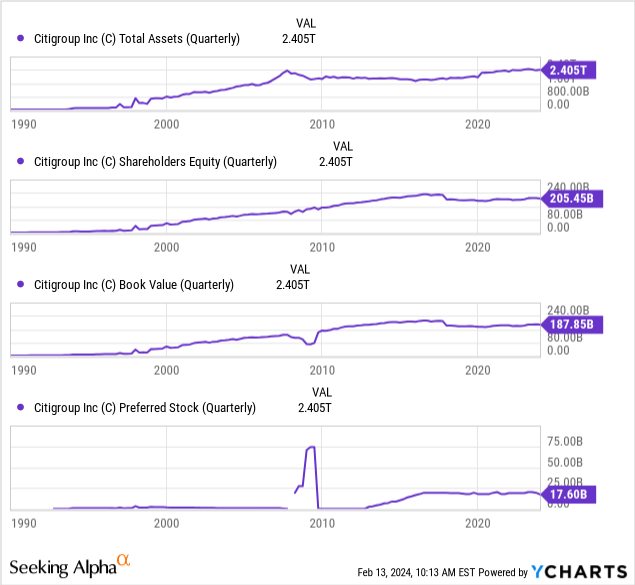

The next set of charts shows important balance sheet items for Citigroup.

While Total Assets continued to grow, both Shareholders Equity and Book Value have shown little movement over the last few years. Citigroup issued tons of preferred stocks during the 2008-09 GFC, much of which apparently was Called shortly thereafter, leaving just a few remaining. Important to the preferred stock owners is the fact the Shareholders’ Equity is over 11X what they are owed.

Trust preferred review: CPRN

seekingalpha.com CPRN homepage quantumonline.com C-N

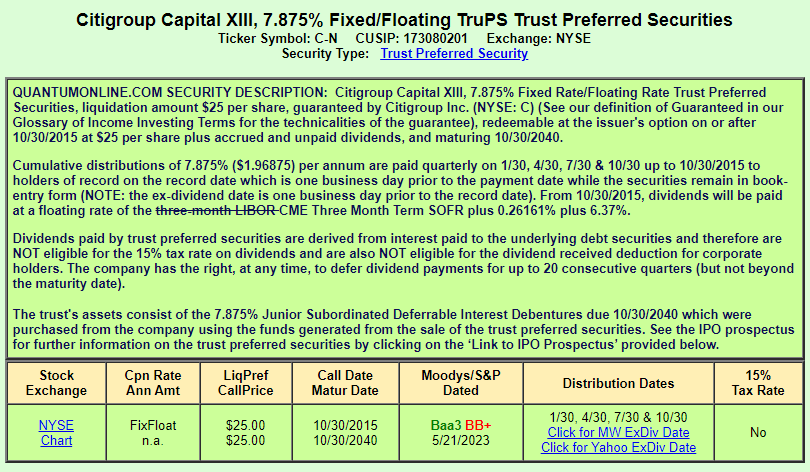

This TruPS holds the 7.875% Junior Subordinated Deferrable Interest Debentures due 10/30/2040. When the bonds mature, CPRN matures with it. Notice the payments are not eligible for the 15% tax rate and Citigroup can defer dividend payments for up to five years, but not past the maturity date. According to the SEC Registration document (pg 8), any deferment freezes dividends on the common stock, and interest payments on equal or lessor-ranked debt.

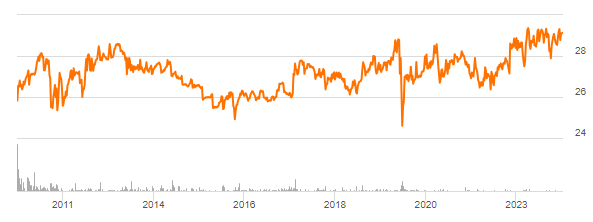

Current payments were switched over to the 3-mo SOFR + 26.161 bps risk adjustment, plus the original fixed component of 6.37%. Fidelity lists the current coupon at 12.28%, but the yield is only 10.25% as CPRN’s latest price is over $29. Unlike a true preferred stock, payments are tax-deductible to Citigroup, which does lower the cost to the bank. That said, there must be a reason the bank has not redeemed a 12+% coupon. The above description does not mention this TruPS being part of Tier 1 capital, but the Prospectus does, subject to regulation changes.

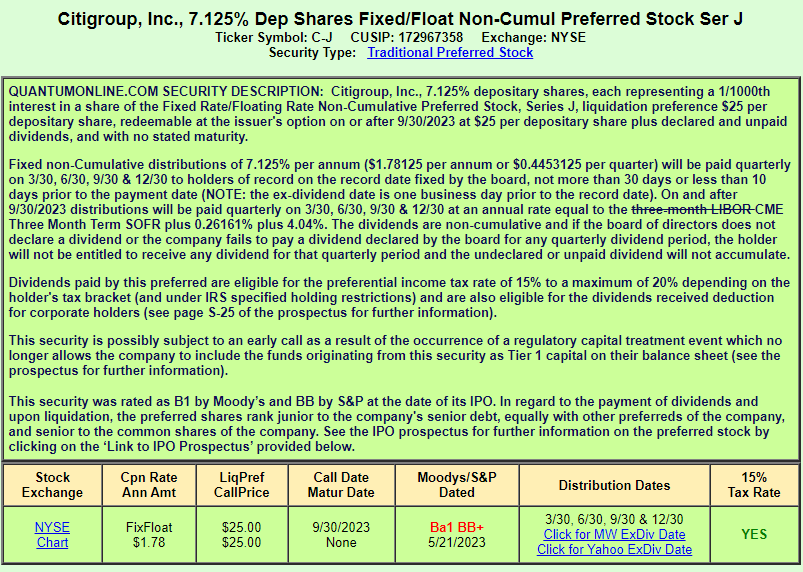

Traditional preferred review: C-J

seekingalpha.com C-J homepage quantumonline.com C-J

This preferred stock became Call-eligible at the end of September and its coupon was reset based on the 3-mo SOFR + 26.161bps risk adjustment factor + 404bps that was part of the original formula. That makes the current payment $.6098, making the forward yield 9.3% but that rate resets quarterly. While payments here are subject to the lower tax rate, they are not cumulative. Based on this Citigroup redemption announcement, about 40% of this issue was Called at the end of 2023.

Citigroup Inc. is redeeming 16,000 shares out of 38,000 shares outstanding of its 7.125% Fixed Rate / Floating Rate Noncumulative Preferred Stock, Series J (ticker “C Pr J”) (the “Preferred Stock”), equivalent to $400 million out of an outstanding total of $950 million aggregate liquidation preference of Series J Depositary Shares representing interests in its Preferred Stock.

The redemption date for the Preferred Stock and related Depositary Shares is December 29, 2023 (the “Redemption Date”). The cash redemption price, payable on the Redemption Date for each Depositary Share, will equal $25. Holders of record on December 18, 2023, will receive the previously declared regular quarterly dividend of $0.606026875 per Depositary Share payable on the Redemption Date. The Depositary Shares to be redeemed will be selected in accordance with the applicable procedures of The Depository Trust Company.

Comparing the issues

| Factor | CPRN | C-J |

| Issue size | $2.25b | $450m post Call |

| Issue type | TruPS | Traditional Pfd |

| Assets held | 7.875% Jr Sub Deferrable Interest Debentures due 10/30/2040 | itself |

| Coupon formula | 3-mo SOFR + 26.161 bps + 637bps | 3-mo SOFR + 26.161bps + 404bps |

| Payments | Deferrable up to 5 years | Noncumulative |

| 15% taxable | No | Yes |

| Price | $29.13 | $26.09 |

| Yield | 10.2% | 9.3% |

Portfolio strategy

To show you how expectations about FOMC actions are important, the latest CPI report came in hotter than expected and the DJIA was down over 700 points at one point, closing down 524 points. Higher than expected inflation could mean “higher for longer” is back on the FOMC’s option list, which is not good for interest-bearing securities. That said, the two Citigroup only moved pennies whereas Citigroup dropped over 2%!

At a price over $29, that is a big hit if Citigroup does decide to Call CPRN, though that requires approval if indeed it is part of their Tier 1 capital. That said, a 10+% yield on “debt” issued by a “too big to fail” bank could be worth the risk. Citigroup has Called all but one of the other (I counted about 12) of their TruPS issues, some as far back as 2003.

Conclusion

Until I came across the news release about Citigroup calling 40+% of the J preferred, I would have given it a Buy rating even with its lower yield because it also had the lower coupon. Under the assumption that Citigroup will retire the rest before touching CPRN, I change to giving the TruPS the Buy rating with the warning to watch for the rest of the J preferred to be Called, at which time if CPRN is above Par, my rating switches to a Strong Sell to avoid the capital loss the J holders just incurred.

Q2 2024 Earnings Call Transcript")