SOPA Images/LightRocket via Getty Images![]()

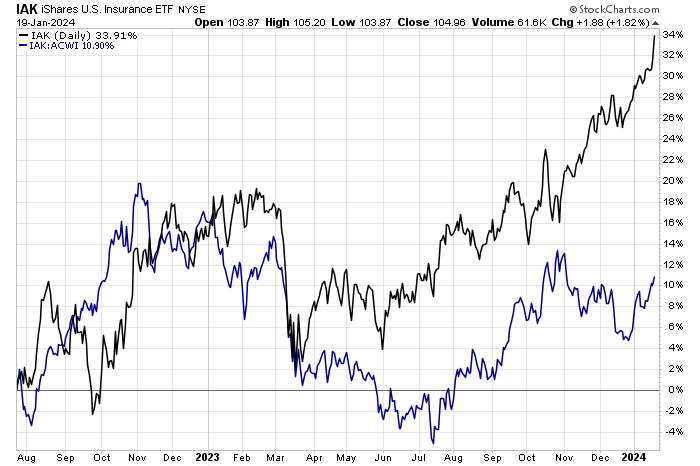

Insurance stocks have been a stealthy outperforming niche in the last several years. Despite volatile interest rates and a slew of costly natural disasters since 2021, the iShares U.S. Insurance ETF (IAK) has outperformed the global stock market. The fund has produced alpha already this year as major insurance companies get set to report Q4 numbers.

I have a buy rating on Chubb Limited (NYSE:CB). I see its valuation as attractive while share-price momentum is very strong with this industry leader.

Insurance Stocks Continue to Work in 2024

Stockcharts.com

According to Bank of America Global Research, Chubb provides diverse insurance/reinsurance to clients globally, focusing on specialty businesses, large accounts, property, and liability-related lines. The business mix is dominated by insurance. International exposure (about 33% of premiums come from outside the US) provides long-term growth potential. Chubb has a major presence in the US, Europe, Asia, and Bermuda. Chubb also writes accident and health and life insurance.

The Swiss-based $97 billion market cap Property and Casualty Insurance industry company within the Financials sector trades at a low 12.2 forward non-GAAP price-to-earnings ratio and pays a near-market 1.5% forward dividend yield as of January 19, 2024. Ahead of earnings due out next week, shares trade with a low 20% implied volatility percentage while short interest on the stock is modest at just 0.7%.

Back in October, Chubb reported a strong set of quarterly results. Q3 non-GAAP EPS of $4.95 topped the Wall Street consensus by $0.53. The profit figure was driven by premium growth trends in the P&C space as well as robust underwriting margins. The firm reported record investment income and solid numbers from its life operating income area. Overall, consolidated net premiums written verified at $13.1 billion, sharply above the $12.0 billion number reported in the same period a year earlier.

Chubb continues to post strong operating cash flow along with improved investment income trends, though risks around just how much higher underwriting margins can get surround the firm given weaker results from some of its peers. To wit, analysts at Goldman Sachs cut Chubb to Neutral from Outperform earlier this month. Still, Chubb remains a prominent S&P 500 Dividend Aristocrat.

Key risks for the company include high international exposure given growth risks overseas as well as the prospect of lower interest rates over the coming quarters. Catastrophe risk is also an ongoing concern which could result in earnings misses.

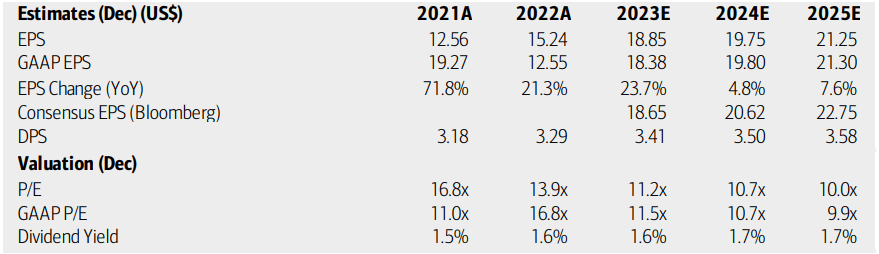

On valuation, analysts at BofA see earnings having climbed by more than 23% last year with a moderation in the bottom-line advance rate this year. Per-share profits are then expected to accelerate to a nearly 8% clip in 2025. The current consensus outlook, per Seeking Alpha, shows more sanguine growth prospects at an EPS growth rate in the low double digits in ’24 and +9% in the out year. Sales growth is also healthy over the next two years. Dividends, meanwhile, are forecast to rise at a slower rate, making Chubb’s yield rather low compared to other companies in the Financials sector.

Chubb: Earnings, Valuation, Dividend Forecasts

BofA Global Research

If we assume earnings of $21.50 over the next twelve months and apply the stock’s 5-year average non-GAAP price-to-earnings ratio of 13.8x, then shares should trade near $295, making this insurance growth name undervalued today. What’s more, CB features a very modest 0.85 forward operating PEG ratio, a steep 38% discount to its long-term average.

Chubb: A Low Forward PEG Ratio

Seeking Alpha

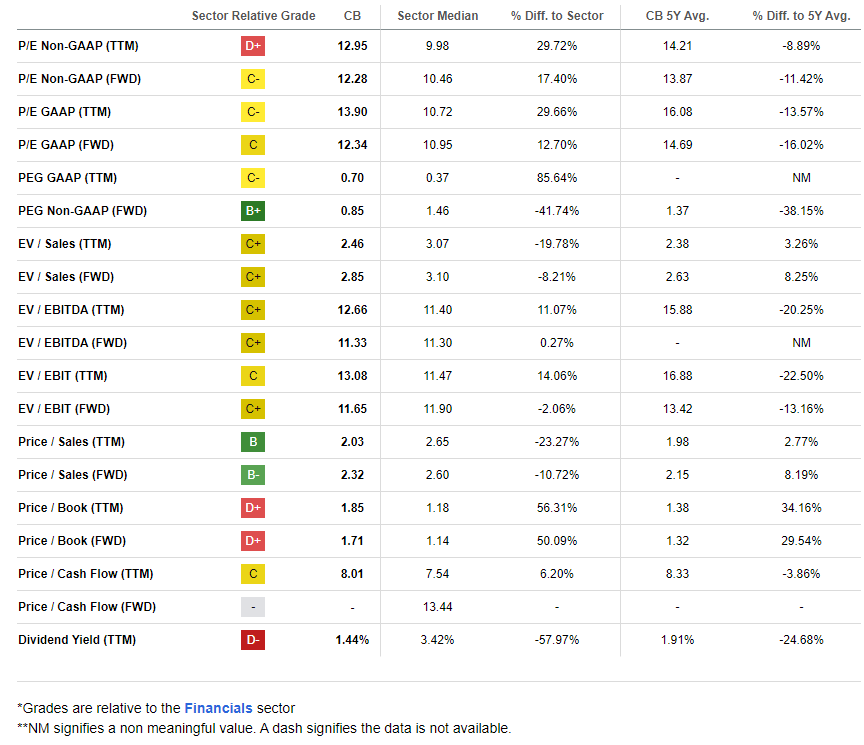

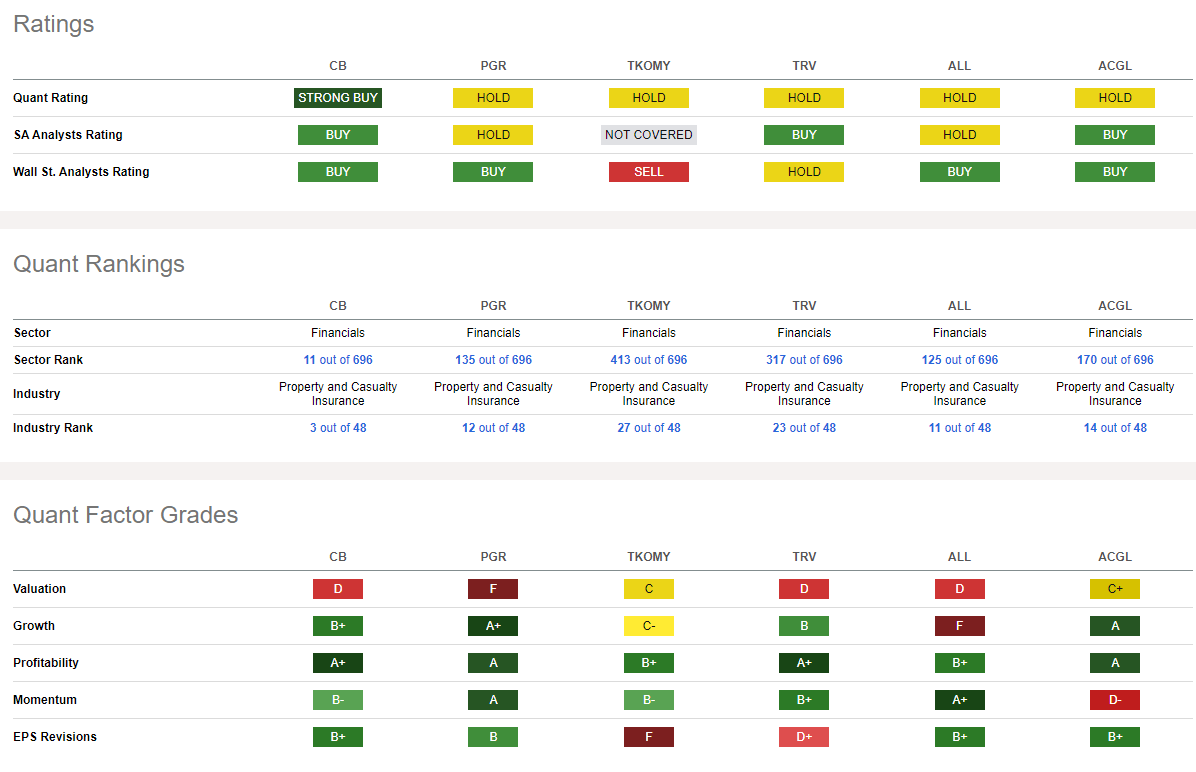

Compared to its peers, Chubb ranks very strong. Currently number 11 out of 696 in the sector, the Swiss company’s valuation grade is weak, but I assert that it has a low earnings-based valuation, particularly given the growth trajectory. Moreover, the firm’s profitability metrics are extremely healthy with robust free cash flow while EPS revisions have been extremely strong lately. Finally, CB’s share-price momentum looks impressive to me, and I will detail a technical breakout later in the article.

Competitor Analysis

Seeking Alpha

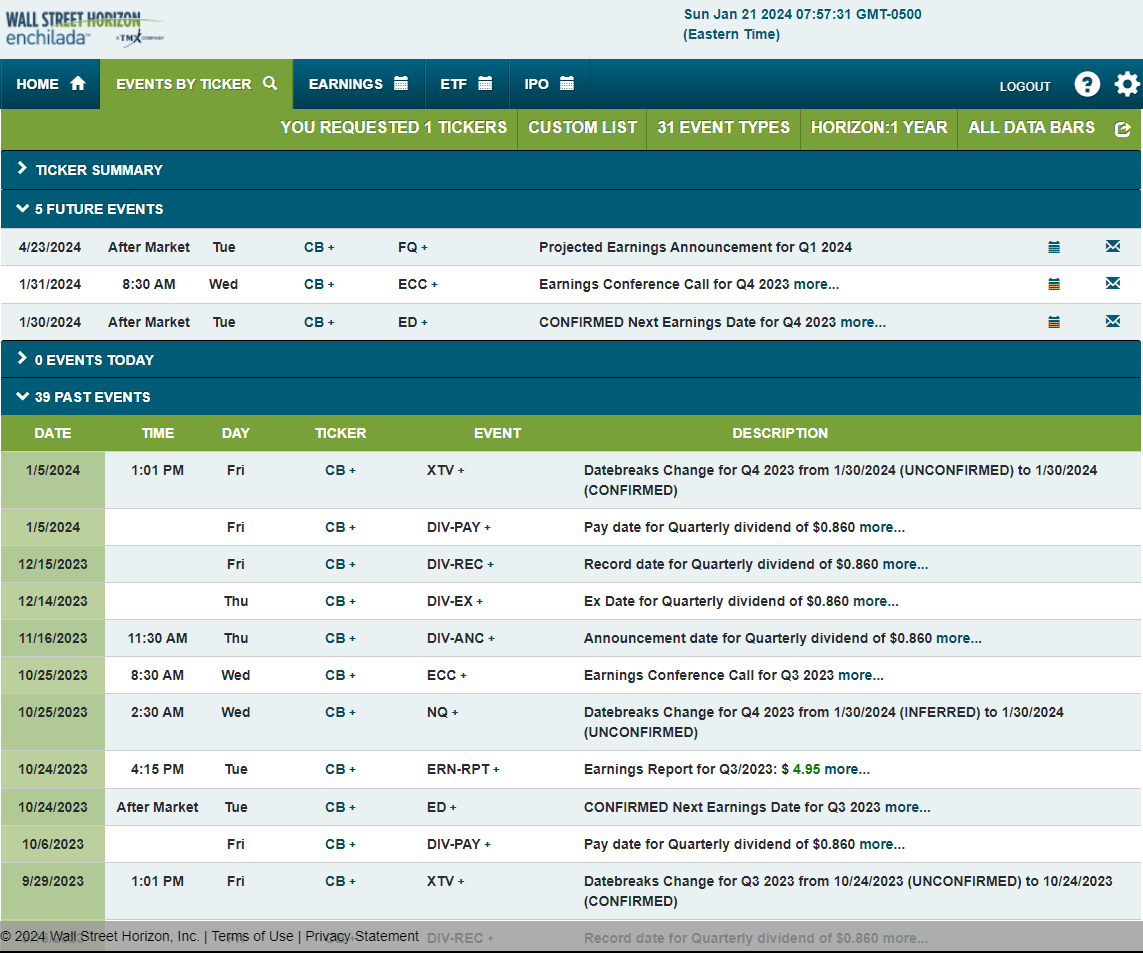

Looking ahead, corporate event data provided by Wall Street Horizon shows a confirmed Q4 2023 earnings date of Tuesday, January 30 AMC with a conference call immediately after the numbers hit the tape. You can listen live here. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

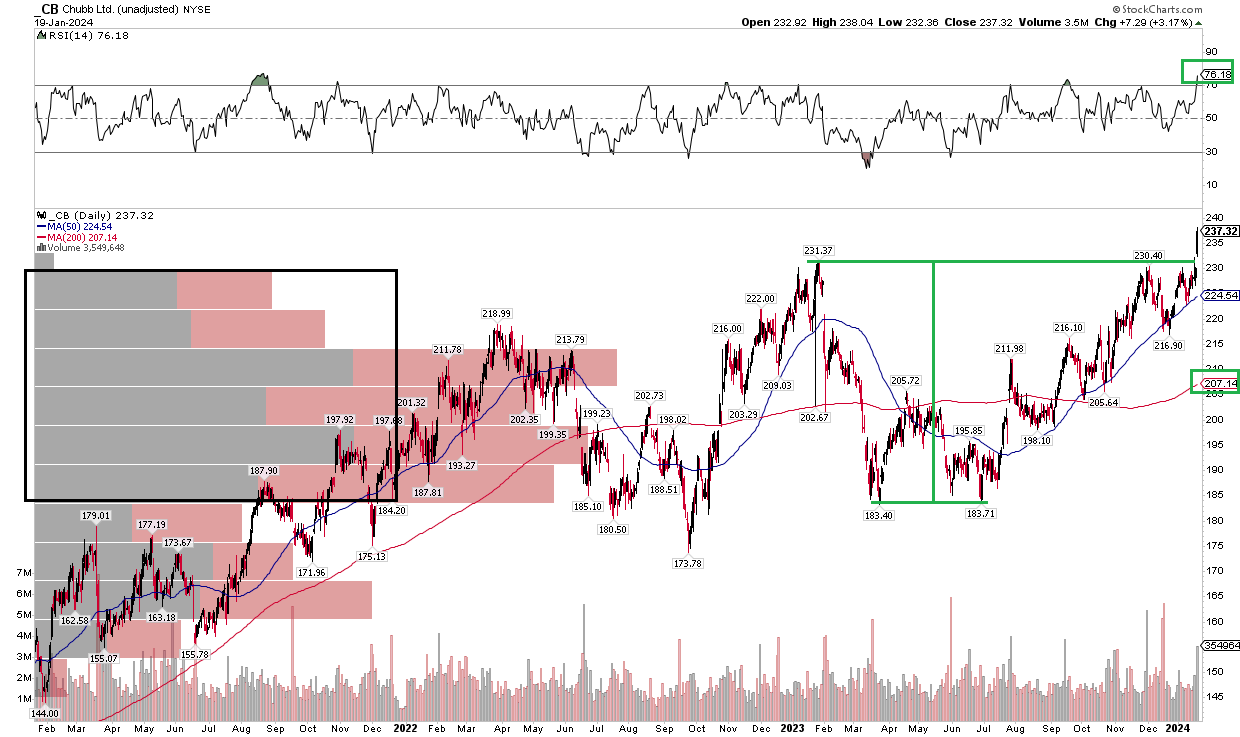

The Technical Take

Inspect the chart below; you might think it’s a high-flying chip name. That is not the case. CB jumped at the end of last week, breaking out to fresh all-time highs above the early 2023 peak of $231. Technicians can calculate an upside-measured move price objective based on the height of the previous pattern. In this case, there was a bullish double-bottom low notched in Q1 and Q3 2023 at $183 to $184. Given the $231 previous resistance, we have a $48 range. Now, tack on that $48 height to the $231 breakout price, and the measure moved price objective is $279, just a few percent below where I see the fundamental value.

Also, take a look at the rising 200-day moving average. Since the shorter-term 50dma and CB’s price are above that trend indicator, it further asserts that the bulls are in charge. Additionally, notice how the RSI momentum gauge at the top of the chart made a fresh high along with the stock price – that’s bullish confirmation, underscoring the power of the breakout. Finally, with a high amount of volume by price in the $184 to $230 zone, there should be plenty of support for pullbacks.

Overall, Chubb’s chart appears healthy for further gains ahead. Support is seen near $216.

CB: Clean Breakout Targets $279

Stockcharts.com

The Bottom Line

I have a buy rating on Chubb. I see its intrinsic value just shy of $300 while the technical situation appears strong.

Q2 2024 Earnings Call Transcript")