SOPA Images/LightRocket via Getty Images![]()

Dear readers/followers,

I’ve covered Chubb (NYSE:CB) a few times in the past. My last coverage was all the way back in 2022, and the company since that time, and my position, have seen some attractive RoR. However, it has failed to generate enough return to beat the S&P500, and as such it’s questionable whether this was a solid investment at the time in the short term. I expected limited further premiumization of this company, and that’s why my investments during the months actually were focused on different financial and insurance companies, often with far higher yields than Chubb offers.

Nevertheless, Chubb’s appeal has not been its yield, but rather the operational safety offered by an above-average insurer. This is what Chubb is, and what it offers. I’ve been covering Chubb for almost 2 years at this point, and I’m familiar with the company’s ups and downs.

Insurance is a tricky segment when it becomes overvalued. While Chubb is a good company, my thesis going into this specific article is that Chubb, relative to market and peers, is still not at an overvalued state, even if it’s at a premiumized one

You can find my last article here – and I will explain my issues with Chubb in this one, but why I ultimately come down at a “BUY” here at this time.

Chubb – Impressive insurance operations at a firm premium to peers

If you follow my work, you know that I invest quite a bit into insurance. You also know that many of those insurance investments are made at discounts, often 5-7x P/E – because insurance operations, first of all, are not valued well using traditional profitability metrics, but also because they tend to be valued at KPIs much lower than other companies. Seeing 4-8x P/E is not difficult or strange in this sector.

That’s why when you buy a company in insurance at over 10-12x, you should be very aware of just what you’re getting into and make sure the company can realize your stated investment goals.

To those investing in Chubb, we’re talking about an insurance company in the P&C sector with a credit rating of A.

If you enter an insurance investment, you should be very aware of how these companies work and how they make money. The companies offer policies where customers pay premiums over a period of time – in P&C, such premiums are typically at a far shorter time period than in life insurance. It’s not strange in this sector to see 1-5-year policies, whereas in life, you’re typically talking decades. The companies in the segment, then take these premiums, and from these collected premiums payout where policies require them to do so – whatever remains is then the company’s profit – oversimplified to a great degree of course. These companies also take those profits and invest them in the market, resulting in an additional NII (net interest income) and other investment income, typically in very safe bonds and similar investments. Life & Health tend to have far longer-dated portfolios than P&C due to the nature of their operations – but their M.O. is similar in this at least.

Chubb does this extremely well. The company, headquartered in Switzerland, has nearly $100B in market cap. The company’s margins and combined ratios are all very attractive, and Chubb mostly lacks the cyclicality that makes up these companies, generating nearly 12% annualized EPS over the past 20 years.

However, I want to make it clear to you, that the trend for Chub to trade above 10x, is relatively new. Between 2006 and 2015, it was more common for Chubb, like other insurers, to trade below 10x. What changed in early 2017 and beyond 2020, is that Chubb suddenly started to estimate an outsized pace of growth, both organically and inorganically. This started with a 72% adjusted EPS growth in 2021 and continued with double-digit 20%+ EPS growth in 2022 and is now slated for 2023 as well.

If this trend were to continue, there’s no argument from me that Chubb is obviously worth more than 5-9x P/E. But we’re, also equally obviously, moving into more uncertain areas here when we start estimating double-digit growth as some sort of “trend”.

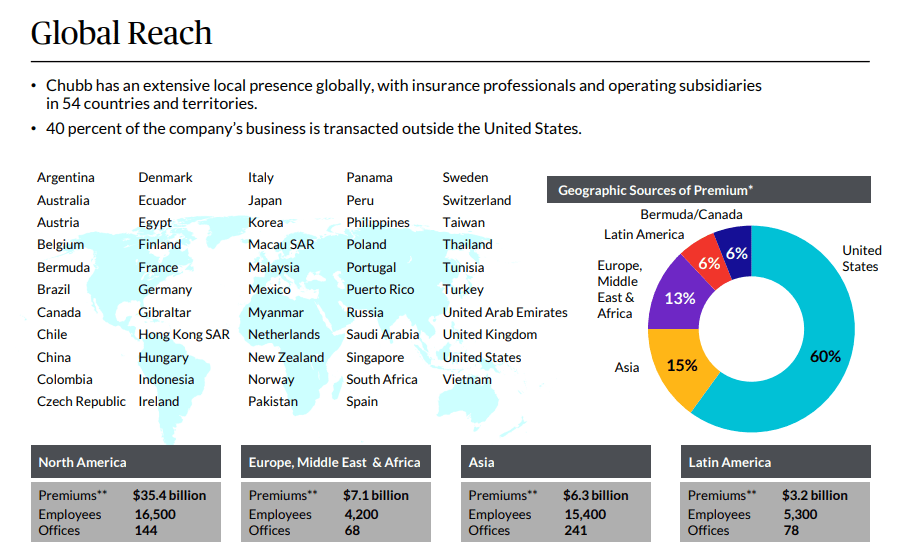

However, if anyone would be able to pull it off, it’s Chubb. It’s the world leader in public P&C with operations in 54 countries and territories. It’s not focused or diversified on other things, but it has a good product and consumer mix, with a leadership in commercial line insurance.

Chubb IR (Chubb IR)

Global reach with a US focus and a growing APAC – that’s Chubb, but with a superb product mix, with no sub-segment more than 24% of the total premium distribution, this being small commercial/middle market P&C.

Whenever I look at an insurer, I want to see sector-average underwriting expertise. Many misconceptions exist about what underwriting is, but it’s essentially evaluating risk or risk analysis. The better a company is at evaluating client risk, the better an insurer it can be, if acting on this expertise. The KPI to look at this is the combined ratio, and Chubb is a serial combined ratio outperformer on a global scale. The company has a 10-year combined ratio (which specifies the sum of incurred losses/expenses divided by the earned premium) of below 90.5%, at 90.1%. Why is this so significant? Because the global peer average, with 10 years including COVID and other things, is 97.4%. And this includes some world giants that I invest in like AXA (OTCQX:AXAHY) and Allianz (OTCPK:ALIZY). Chubb is, simply put, one of the best insurance companies out here, and there is hard data to prove exactly that. (Source: Chubb).

The 3Q23, the latest results we have, give us no reasons to really expect this to change. Net income was up 157% YoY, and net premiums written were up 8.4%. Global P&C excluding Agri was up 12.3%, and consumer insurance grew 17.6%.

In short, the double-digit aforementioned growth is actually fairly visible here. The one drawback or negative was Agriculture insurance, which saw a premium decline of 11.7%, though this was primarily due to the timing of premium recognition (another core concept in insurance – if you write a 12-year policy with a normalized fiscal in late October, you can only recognize two months’ worth for that fiscal). We also saw an increase in the Agricultural combined ratio to 93.2%, which is the highest for Chubb – and this reflects the company’s expectations for P&Ls for the current crop year. While this may seem like something to really dig deep into, this segment is less than 8% of the company’s total premium distribution, so not something I would consider a big deal.

It was also easy to expect a decline and unrealized losses in the company’s book value due to investment portfolio tendencies, namely the mark-to-market of rising interest in the fixed-income portion of Chubb’s portfolio. Every insurance company has been seeing this. There were also some goodwill impacts though, which meant that Tangible BV excluding AOCI (accumulated other comprehensive income), declined 4.2% YoY.

None of this takes away though what was, in my view, a superb quarter and a catalyst for the upward trajectory of the stock. The company’s price increases and rates remained strong, and demand for products and services has seen no material adverse impact. Chubb has been able to stay well ahead of cost inflation, and I see no reason to doubt management in the near term, in that they will deliver 20%+ EPS growth year-over-year, or at the very least something close to this.

Some of you might have thought that the time has come to go negative on this stock, or go “HOLD”. We’ve seen a material uptick after all – but this is not the case, as I see it (and clarifying this is one of the reasons for the update).

Let’s look at the risks and upsides for this company.

Risks & Upside with Chubb

Chubb is, at its current state, seeing a distinct advantage from a combination of a challenging market and its market-leading position. In times like these, the scale of these larger companies and the expertise they offer, and can offer at a lower price point, make the difference.

What risks exist for this company here? Mainly macro. If one of the large players decides to go into some sort of premium pricing war, this could impact potential company returns. It’s also not strange that this growth we’re seeing in P&C and L&H often is at the same time with increased political and personal uncertainty. This is the case now as well. And if one of those uncertainties were to turn material – well, we know what happens to a P&C company when something truly catastrophic actually does happen. I’ve also not mentioned in any material way the company’s L&H insurance. For many companies, I’m favorable in terms of a multi-line/multi-segment insurance approach, mixing L&H with P&C. For Chubb, I think the better idea would be to abandon L&H; its expertise is in P&C, and I view L&C as dragging the company down.

Despite both being “insurance”, I don’t see any strategic rationale for keeping this in-house.

But the upsides speak for themselves. Scale, global footprint, history and international appeal. The company is one of the very few companies that can manage to “beat” things here, and that’s worth something.

Valuation for Chubb

As I wrote in my last article, I believe that Chubb has mostly everything that an insurance investor should want, with the exception of yield. Chubb’s current yield is less than 1.5%, which makes it the lowest-yielding financial position I have in my portfolio. Not a positive. I also don’t see this yield materially improving above 2% in the near term.

Much of the upside here will come from continued premium and earnings growth.

I will also say that if you take a long-term view, you can make a very solid case for why the company is getting too expensive here. If I forecast the company at 20-year averages, this comes to a P/E of 12.3x, which means that the annualized upside even with 12% EPS growth per year until 2026E only comes to 13.76% per year. This is still solid but below my 15% target.

However, forecasting at 20 years also implies that I’m considering the likelihood of another GFC. I don’t think that’s the case.

Over 10-years, excluding the GFC, we have a 14x P/E average, and the upside to that is 18.8% per year. I consider this more likely. Chubb is not cheap, but nor is it what I would consider prohibitively expensive.

However, I will go on record and say the following; in order to be significantly positive on the company here, you have to accept that the company is worth more in BV and tangibles than historically and that the growth continues – because if it doesn’t continue, if there is some large event that triggers policy payouts larger than the company’s underwriting has estimated, we could see a downturn.

The current average analyst target is close to the share price. 23 analysts give the company a target from $210 to $275 with an average of $246. We’re at $237/share. In fact, my last price target was $235, and it’s only thanks to a raise to $242 that I can still see an upside and a “BUY” here, owing to very impressive and above-expectation results for 2023.

13 out of 23 analysts still consider the company good enough to “BUY” or for it to outperform.

However, we are edging to very high levels here – and given the book value component of the valuation, which is currently at the higher end of the 5-year average, my price target of $242 has perhaps one of the highest allowances for premiumization in the insurance sector. It’s suitable that the target is Chubb, given its quality and fundamentals. Other analysts have already considered the company overvalued here. The only company that on a peer average has the sales multiple allowance for premiums such as Chubb, is Berkshire (BRK.A) (BRK.B). The 2x sales multiple is, more typically at peers like AIG, at around 0.95-1x. Realize therefore that you need to allow a substantial premium and outperformance expectation for Chubb.

Currently, I consider this valid and give the company the following thesis.

Thesis

- Chubb is among the class leaders in P&C and other insurance lines, such a personal ones. The company has a history of solid outperformance over time, comes with superb fundamentals, and has an upside in the double digits over the coming few years. It combines attractive fundamentals with a market-beating upside, and this is very rare in any sector.

- Chubb is an easy “BUY” at any sort of attractive valuation – and that’s what we have here if one that’s very close to no longer being attractive.

- I adjust my PT for Chubb to $242/share for the near and medium term, and give the company a “BUY” here, for 2024E.

Remember, I’m all about:

- Buying undervalued – even if that undervaluation is slight and not mind-numbingly massive – companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn’t go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

I only call companies with a 15% upside to my conservative PT cheap, but other than that, this company has “everything” you might want – except a higher dividend.

Q2 2024 Earnings Call Transcript")