Anne Czichos/iStock Editorial via Getty Images

Investment Thesis

Chipotle Mexican Grill (NYSE:CMG) has a strong brand identity and a robust growth strategy that is evident in its goal to vastly expand the number of restaurant locations whilst continuing to maximize same store sales growth. These factors highlight the fundamentals of the business. The company’s excellent financial standing, with no debt further emphasizes its efficiency and strategic planning. Chipotle’s success can be attributed to its business model and its appeal to a diverse consumer base who generally have a positive experience at Chipotle’s restaurants. This positions the company well for growth. However, as an investor it is important to consider both business success and financial valuation. The current market price of Chipotle stock is relatively high compared to its estimated value, which reduces the investment appeal. A Discounted Cash Flow (DCF) analysis suggests that there may be overvaluation when evaluating the stock for investment purposes. Despite Chipotle’s strengths in terms of operations, this disparity between market price and intrinsic value leads me to a hold rating for now.

Company Overview

Chipotle is a popular fast-food chain started in 1993 by Steve Ells famous for its Mexican inspired cuisine. The company has grown substantially over the years and now have over 2,500 locations, mostly in the US. What sets Chipotle apart is its dedication to using high quality ingredients and supporting ethical farming practices. Their business model revolves around customizable menu options and an efficient assembly line production system that ensures service while keeping standards high.

Within the fast-food industry, Chipotle are competing against business like Qdoba Mexican Eats, Moe’s Southwest Grill, and Yum Brands (NYSE: YUM). Despite this tough competition, Chipotle leans into their ‘Food with Integrity’ motto, which highlights sustainable ingredients and humanely raised meat. This resonates with people who care about health and the environment. Despite facing challenges such as food safety concerns Chipotle remains at the forefront of the fast casual dining industry thanks to its approach to fast food and unwavering commitment to delivering top notch quality.

Positive Customer Experience Enhances Brand Identity

The fast-food industry is a notoriously competitive industry and is extremely difficult for companies to get ahead and stand out, yet despite this Chipotle Mexican Grill has managed to do so and establish a universally recognizable brand. What initially draws me towards Chipotle is the strong brand identity, which is a cornerstone of its success and appeal, particularly in an era where consumer preferences are increasingly leaning towards health-conscious and environmentally responsible choices. Over the past 30 years, Chipotle has successfully positioned itself by offering unique elements which resonate with customers and enhance the overall experience.

Two such examples of Chipotle’s unique offerings are their “Build Your Own” model and open kitchen concept which collectively enhance the customer experience, aligning well with modern consumer expectations of choice, transparency, and quality. The “Build Your Own” model empowers customers with the ability to personalize their meals, catering to a diverse range of dietary preferences and needs. Simultaneously, the open kitchen layout at Chipotle plays a vital role in underscoring the brand’s commitment to transparency and quality. Customers watching their meals being prepared gain reassurance about the freshness and handling of ingredients. This visibility is crucial in today’s market, where there is a heightened consumer focus on the origins and preparation of food. These offerings are not just a service feature; it creates a personal connection and satisfaction with the food, fostering customer loyalty which translate into reoccurring revenue which the company are leveraging through their Chipotle Rewards program which allows customers to earn points just for ordering and cash them out for a variety of rewards in the Rewards Exchange.

That being said, the company has seen a slight decline in customer satisfaction over the past year according to the American Customer Satisfaction Index, which state the overall consumer satisfaction declined from 78% to 75% which is overall more in-line with its closest competitors. Yet despite this, CMG has able to raise prices 4 times over the past 2 years at a rate which outpaced inflation significantly which I believe is a testament to the company’s brand and highlights its competitive advantage and demonstrates the strength of the overall business.

Market Expansion Continues to Fuel Growth

In my view the expansion of Chipotle’s locations and its consistent growth, particularly in same store sales, are signs that the company has a strong business model and promising future prospects.

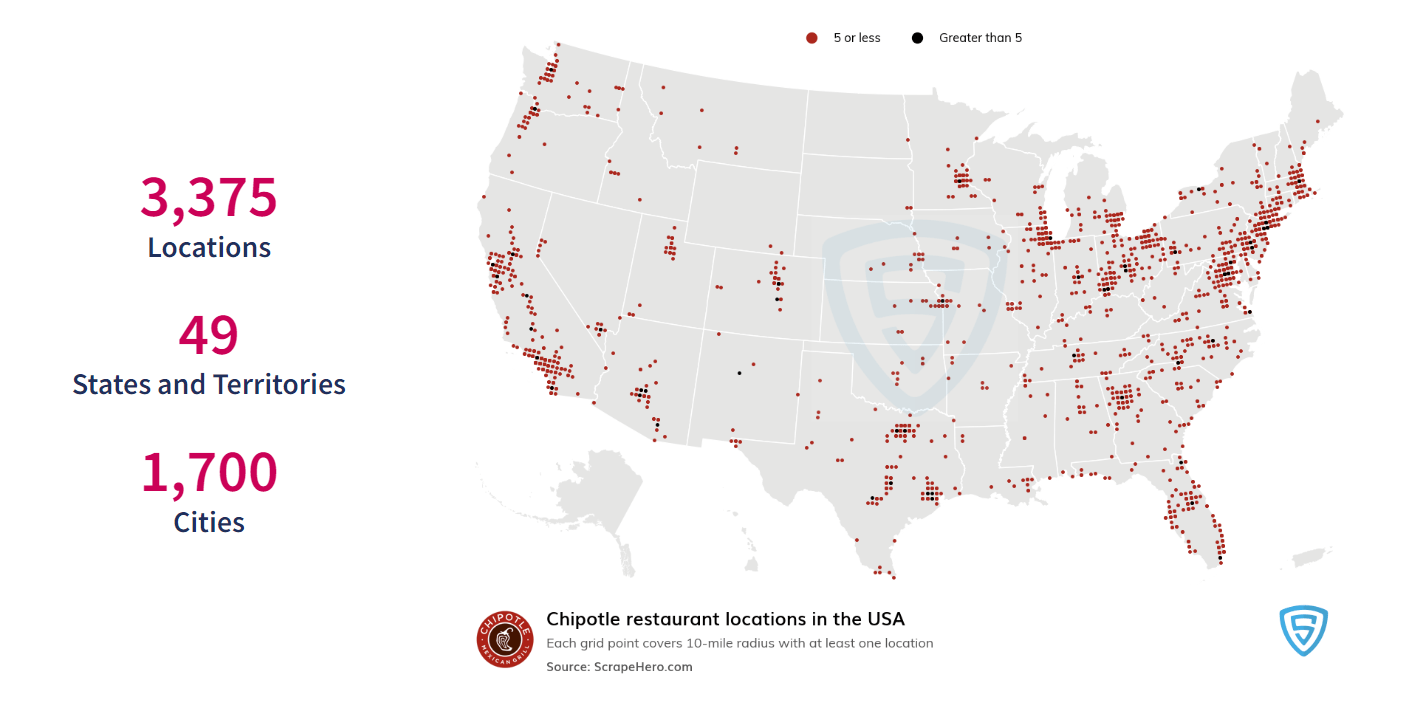

To start with the increasing number of Chipotle restaurants reflects the company’s presence in the market and its effective growth strategy. Expanding into areas both domestically and internationally shows that the brand is becoming more popular and successfully entering markets. This continuous growth in store count is crucial for boosting revenue and market share. For example, it is widely known that Chipotle aims to expand to 7,000 locations in North America as well as expand globally. This indicates their confidence in growth and a clear vision for expanding their business. In Q3 2023 Chipotle opened 62 restaurants, including 54 with Chipotlanes — a drive-thru strategy aimed at attracting more customers. The company also expects to open 285 to 315 restaurants in 2024.

CMG US Locations (ScrapeHero)

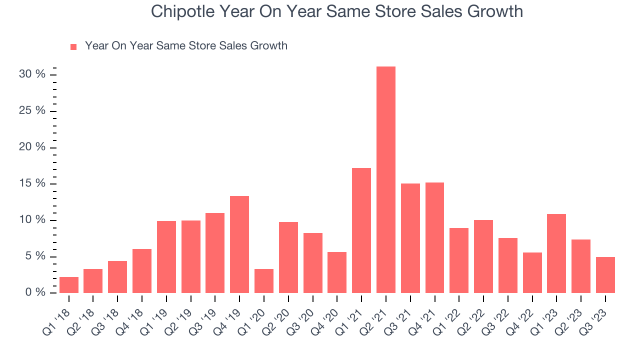

Furthermore, I believe that a restaurant chains overall business performance can be assessed by its same store sales performance. This metric serves as an indicator of a brand’s lasting appeal and operational efficiency. Same store sales, pertain to the revenue generated by the existing outlets of a chain within a specific time frame. This excludes any revenue derived from opened stores. When this metric shows an uptrend it signifies that the existing stores are performing well by attracting customers or experiencing increased spending per customer. Chipotle has consistently witnessed growth in same store sales over the years. This indicates that their business strategies, such as introducing menu items implementing marketing campaigns and enhancing customer service have been resonating positively with their customer base. From my perspective what stands out is the pace at which the company has been able to elevate its same store sales. Since Q1 2018 they have achieved a year, on year growth rate of 8.85% surpassing the historical industry average of 2 to 3% which is a really encouraging sign to me as it demonstrates organic, sustainable growth in the restaurant industry.

CMG Same Store Sales Growth (Yahoo Finance)

Financial Analysis

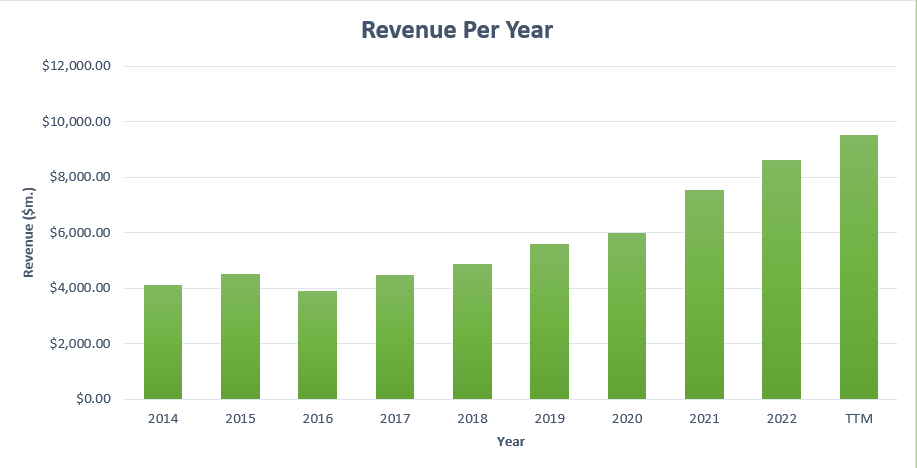

Over the past five years Chipotle has displayed strong financial performance, consistently achieving revenue growth that indicates a strong and steady upward trajectory. From 2018, to the last 12 months (LTM) period their revenue has experienced a compound annual growth rate (CAGR) of 14.4% rising from $4.86 billion to $9.54 billion. This sustained revenue growth showcases Chipotle’s business strategies and their ability to adapt to changing market dynamics and consumer preferences.

CMG Revenue Per Year (Author)

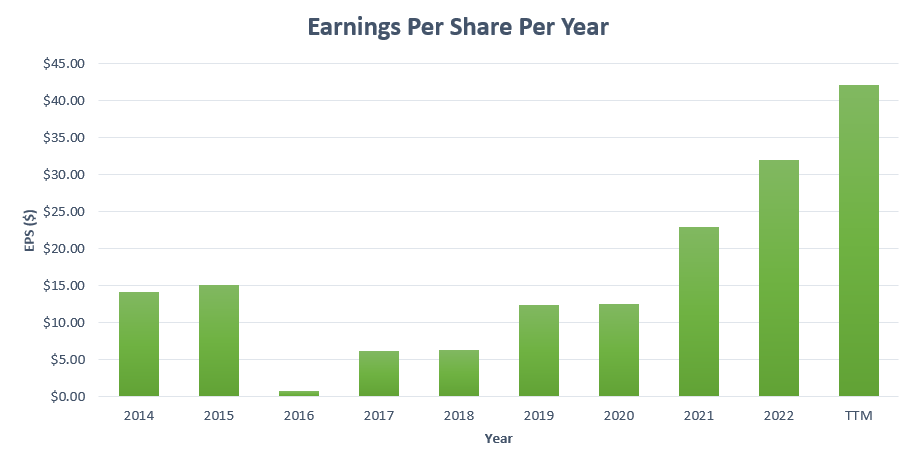

In terms of earnings per share (EPS), Chipotle has also witnessed growth. The EPS increased from $6.31 in 2018 to $42.14 in the LTM reflecting a CAGR of 46.21%. This substantial rise in EPS highlights Chipotles success in implementing growth strategies while efficiently managing expenses and maximizing profitability. Moreover, during this period Chipotle’s free cash flow (FCF) expanded significantly also, growing from $334 million in 2018 to $1.39 billion LTM, a CAGR of 32.9%.

CMG EPS Per Year (Author)

Turning our attention towards Chipotle’s balance sheet, their recent quarterly report reveals an amount of cash and cash equivalents totalling $602 million. Additionally, the company maintains an excellent debt position by keeping their long-term debt at zero, indicating a conservative approach when it comes to utilizing leverage. The fact that Chipotle doesn’t have long term debt is quite impressive in my opinion, especially in the restaurant industry. It shows that Chipotle manages its finances effectively and maintains stability.

Looking ahead to their upcoming results I predict that Chipotle will achieve their goal of opening around 255 to 285 new restaurants for the fiscal year 2023. I expect this expansion to contribute to the company’s revenue and profitability in Q4. Beyond Q4, assuming conditions remain steady, I anticipate that Chipotle will continue with their growth strategy by more opening restaurants both in the US and international markets. They also seem determined to implement Chipotlanes as a way to attract customers, which I believe will greatly benefit the company in the long run.

Valuation

When it comes to evaluating Chipotles worth it’s important to consider both the price we pay (market capitalization). The value we receive ( business factors and future earnings). One effective method for this evaluation is, through a DCF analysis.

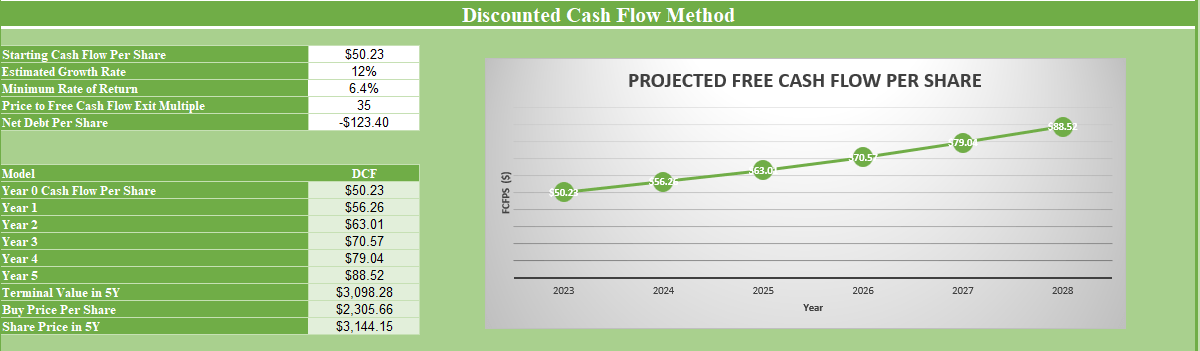

Let’s take a look, at Chipotles FCF per share which’s $50.23 LTM. If we anticipate growth in the number of stores and comparable restaurant sales, I think it’s reasonable to estimate that Chipotles FCF per share could increase by around 12% annually over the five years. Based on this estimation we could expect Chipotle’s FCF per share to reach $88.52 by the end of the five year period.

If we apply an exit multiple of 35 to this earnings estimate, which is lower than the average price to FCF ratio from the past ten years we can infer a potential future price target of approximately $3,144 in 2028.

Considering these projections it seems that investing in Chipotle at its share price might result in an approximate CAGR of 6.4% over the next five years. Based on the estimated return, I believe that Chipotle is currently overvalued and therefore I recommend a hold rating for now.

DCF Analysis of CMG (Author)

Conclusion

To sum it up, Chipotle Mexican Grill stands out in the fast-food industry because of its strong brand identity and unique customer experiences. The company has successfully found its niche by prioritizing service and transparency which aligns well with what consumers expect today. This smart positioning is visible in its business model as evidenced by the growth in both its number of locations and same store sales. Financially speaking Chipotle has shown solid growth whist maintaining a healthy debt status and making strategic expansions that highlight their excellent financial management and business expertise. However, a thorough DCF analysis suggests that, considering its market price, Chipotle might be overvalued. Considering the company’s performance and future growth prospects I believe Chipotle is a hold at current prices. The success story of Chipotle serves as proof of their adaptability focus on quality and innovative business strategies in a challenging market landscape.

Q2 2024 Earnings Call Transcript")