Chipotle Mexican Grill (CMG 0.68%) has been one of the more stellar investments in the restaurant space over the past decade. It launched its initial public offering (IPO) 18 years ago at $22 per share, and as it expanded and deepened its footprint in the U.S., it has grown to nearly 3,400 locations across the country.

That impressive expansion has resulted in gains of more than 120-fold for shareholders who bought at the IPO and held. Despite that stunning growth, the restaurant stock will likely continue making its investors richer. Here’s why.

Chipotle’s continuing expansion

As of the end of 2023, Chipotle operated 3,437 locations, though all but 67 of these restaurants are in the U.S. The company added 250 net locations in 2023 — and despite that massive footprint, its North American expansion is not likely to level off anytime soon.

In the fourth quarter of 2023, the company reiterated its goal of 7,000 North American locations as it targets smaller communities. Additionally, it currently operates only 41 restaurants in Canada, meaning it has barely begun to tap the market that is most similar to the U.S.

Moreover, like its fast-food counterpart McDonald’s, it has expanded into Europe. But since that accounts for only 26 locations in the U.K., France, and Germany combined, it has barely scratched the surface of its potential across the pond.

In comparison, McDonald’s operates over 40,000 locations globally. Whether Chipotle intends to build a comparable worldwide footprint is not clear, but the success of McDonald’s indicates it can keep adding stores for a long time to come.

Improving financials

Furthermore, Chipotle made a fortuitous decision when it invested in its digital sales platform and began adding Chipotlanes in 2019. That minimized the negative impact on sales when the U.S. went into lockdowns for much of 2020. Even though customers can dine in again, over 36% of its sales are from its digital platform, indicating it has succeeded in making the ordering process more efficient.

When it comes to overall sales, it reported $9.9 billion in revenue in 2023, a yearly increase of 14%. That includes an 8% surge in comparable restaurant sales, with the rest of the increase coming from its added locations.

Chipotle has also capitalized on its pricing power. It has long served as a low-cost option for natural food. So far, periodic price increases amid rising labor and food costs have not deterred customers. That power may have helped its operating margin climb to 16%, up from 13% in the previous year. That resulted in a net income of $1.2 billion in 2023, a 37% increase year over year.

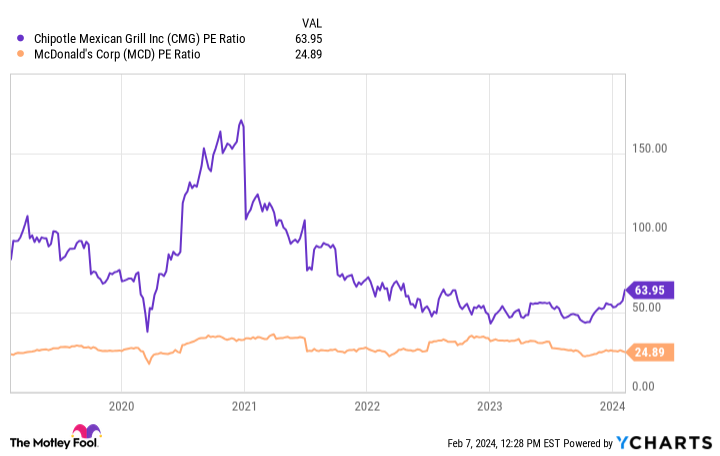

Given these results, it may not surprise investors that the stock is up almost 60% over the last year. And while its price-to-earnings ratio of 64 is well above the McDonald’s earnings multiple of 25, its valuation is well below five-year averages, making further multiple expansion more likely.

CMG PE Ratio data by YCharts

Making sense of Chipotle stock

Despite massive long-term growth and high earnings multiples, the growth in Chipotle stock is unlikely to end anytime soon. Amid a rapid U.S. expansion, it has only completed about half its expected North American buildout. Moreover, rising prices have not deterred revenue and profit growth.

Furthermore, it has begun expanding into Europe, and if it can benefit from success similar to McDonald’s, it could build a massive international presence over the next few decades. As more customers bite into Chipotle’s burritos, the stock should continue to satisfy investor appetites for gains.

Will Healy has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Chipotle Mexican Grill. The Motley Fool has a disclosure policy.

Q2 2024 Earnings Call Transcript")