A_Melnyk

Chicago Atlantic Real Estate Finance, Inc. (NASDAQ:REFI), founded in 2021 and headquartered in Chicago, Illinois, is an mREIT that primarily originates, structures, and invests in senior secured loans to state-licensed cannabis operators.

The industry it serves is expanding along with its business and its leverage is exceptionally low for an mREIT. Regardless, I think that investors should only add it to a watchlist for now as the stock seems to be fairly valued.

Business

Operated externally by Chicago Atlantic REIT Manager, LLC, the company specializes in originating mortgage loans ranging from $5 million to $200 million each. Typically structured with terms spanning one to five years, with amortization applied for terms exceeding three years, these loans are often co-lent, with the company holding a portion (up to $50 million) of the aggregate loan amount. That approach can allow the mREIT to diversify more while still being exposed to well-established borrowers, have access to more deals, and share the risks with other experienced lenders.

The company’s portfolio primarily consists of first mortgages extended to established multi-state or single-state cannabis operators and property owners. These loans are secured by real estate assets, as well as licenses, equipment, and receivables, supplemented by personal or corporate guarantees. As of September 30, 2023, and December 31, 2022, personal or corporate guarantees backed 26.3% and 13.6%, respectively, of the principal amount of the loan portfolio.

REFI basically capitalizes on the limited access that cannabis operators have to tailored financing solutions that more traditional institutions are unable to provide due to regulatory constraints. In addition, the ongoing legalization of cannabis at the state level naturally increases loan demand from the industry players and property owners leasing to cannabis tenants. With cannabis being legal in 38 states for medical use and 24 states for recreational purposes, the market has become very wide. According to Statista, industry revenue in the U.S. is forecast to reach $39.85 billion in 2024 and the market is expected to compound at a CAGR of 13.93% up to 2028. So while it’s true that the borrowers constitute a more niche customer base than others on which mREITs usually focus, the industry, although heavily regulated, is not as risky as it once may have been.

Profitability

Being externally managed is expensive though. Consider that the company paid the manager $9,699,948 in management fees and expense reimbursement during 2022. For context, revenue was $51,471,766 during the year.

That being said, REFI is becoming very profitable very fast. In the third quarter of 2023, its performance reflected a lot of growth. Total revenue experienced a YoY growth of 90.8% and net interest income increased by 6.8% compared to the same period the previous year. Moreover, net income for the quarter rose by 2.1% from the same quarter the previous year, reaching $9,976,998. Last, EPS remained at $0.55.

Solvency

As of the end of the third quarter of last year, the company has a revolving facility of $63 million bearing an 8.5% interest rate. The loan matures on December 16, 2024, but REFI has a one-year extension option.

One of the covenants of the facility requires the company’s debt service coverage ratio to be higher than 1.35; as of the last reported quarter, the ratio was 7.8. Another requires a leverage ratio below 1.5; it was approximately 0.17 per the last report and it’s worth noting that this is remarkably low for an mREIT as well. Last, there is a covenant limiting the company’s capital expenditures below $150K which the company was also in compliance with.

Now, 96.16% of the company’s asset base is comprised of the loan portfolio, so we should briefly assess its quality to see how sustainable the above leverage and liquidity levels are. First, it’s nice to know that the credit loss reserve amount reported lately only represented 1.6% of the loan portfolio. Moreover, about 74.3% of the portfolio was fully covered by the real estate collateral pledged, with the rest being partially covered; although note that there might be additional collateral present here, such as equipment, receivables, and licenses. In any case, the average collateral coverage was 1.5x as of the end of the third quarter of 2023, which provides a significant margin of safety here. The margin of safety is also reflected in the loan/EV ratio of 42.5%.

Further, the company assigns a credit score to each loan on a scale of 1 to 5, with 1 and 2 representing very low and low risk, respectively, 3 and 4 representing moderate to high risk, respectively, and 5 representing an impaired state/likely loss. As of September 30, 2023, the weighted average score of the portfolio was 2.32 and no portion had one of 5, reflecting a generally low risk.

Last, the 28 loans in the portfolio seem to be well diversified with the largest one contributing 11.3% to the total value. And while 19% of the loans (largest exposure) concern corporations operating in one state, Maryland, the portfolio is exposed to 14 states in total, which is promising in the context of such a new business.

Dividend and Valuation

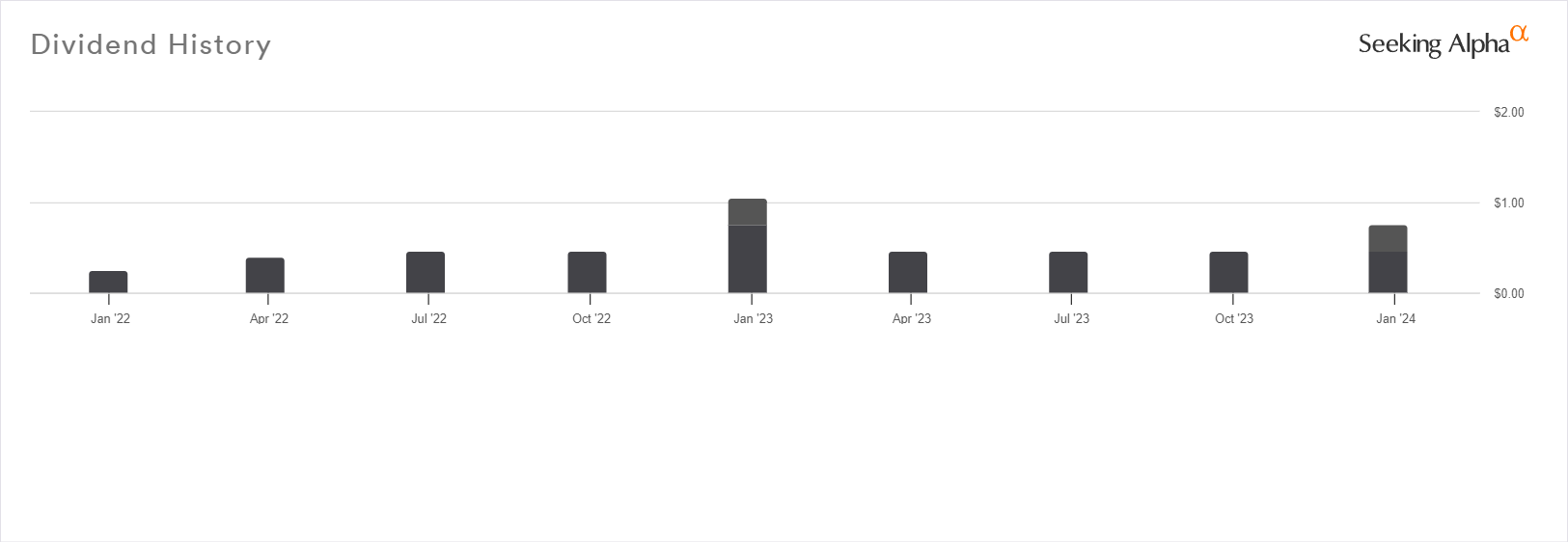

The company currently pays a quarterly dividend of $0.47 per share, which results in a forward dividend yield of 11.64%. Maybe it’s too early to assess the safety of the dividend with adequate certainty considering the payment record:

Seeking Alpha

However, the payout ratio based on the latest EPS annualized is 87%, which is quite high. But it’s difficult to judge this too when the business is in the early stages of expansion; a potential further EPS growth can tell a different story in the short term.

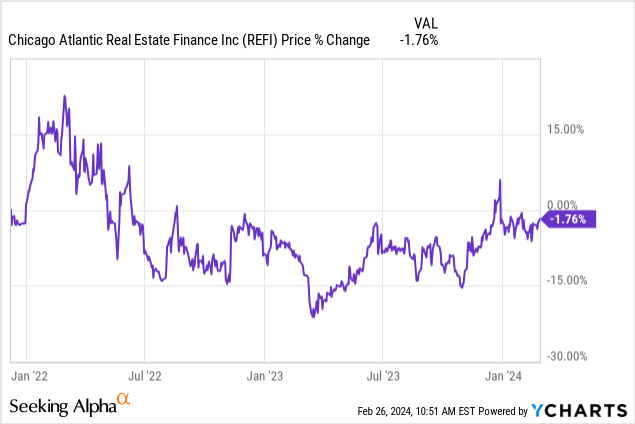

Now, a price reversal seems to have taken place in 2023 for REFI, bringing it back to IPO levels:

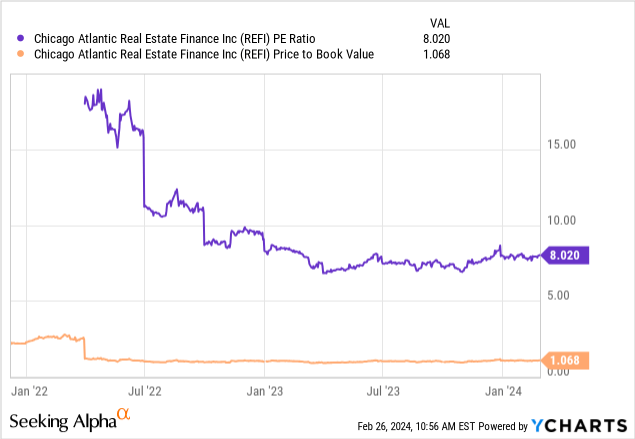

Is the price now a good offer by the market considering the more mature business? This is where it gets personal. It’s fair, but that’s not good enough for me as I prefer to buy below book value.

And considering that this business is so new, I wouldn’t feel comfortable holding fairly valued stock in it.

Risks

Some risks you should also consider are the following:

-

Interest Rate Risk: Share prices of mREITs are highly sensitive to changes in interest rates. Even though interest rates are unlikely to climb higher, the volatility driven by speculation on the matter of interest rates may be uncomfortable and result in the realization of losses if you’re not mentally prepared.

-

Prepayment Risk: REFI’s profitability can be affected by a materially increased number of loan prepayments since the company relies on the interest to generate revenue.

-

Credit Risk: Profitability can also suffer from defaults on REFI’s loans; remember that one-fourth of its loans are not fully covered by the real estate collateral.

-

Market Risk: The cannabis industry is fairly new and though it’s growing rapidly, it’s also likely that it will continue to change due to tweaks in regulations which may adversely affect REFI’s borrowers.

- Dividend cut risk: REFI’s dividend could prove to be unsustainable; a cut is not unlikely and that would not only affect your income power but probably also the price of the shares.

Verdict

All in all, I wouldn’t mind holding REFI considering its potential for growth, conservative use of leverage, and portfolio. But its price, although fair, lacks the margin of safety that I prefer to observe when it comes to mREITs. For this reason, I am rating it a hold for now and adding it to a watchlist. I’ll reconsider it if shares reach anywhere near $12 as that level would imply a significant discount.

What’s your opinion? Do you own the stock? What’s your cost basis, allocation size, and exit plan? You’re welcome to leave a comment below! Thank you for reading.

Q2 2024 Earnings Call Transcript")