Bonds issued by Chesapeake Energy Corp. and Southwestern Energy Co. were rallying on Thursday after the companies sealed their expected $7.4 billion all-stock merger.

The news was welcomed by Fitch Ratings, which placed both companies’ BB-plus long-term issuer default ratings on Rating Watch Positive, meaning it could upgrade them in the medium term.

The BB-plus rating is a single notch into speculative-grade or junk status, so an upgrade would push the credits back into investment grade. Investment-grade issuers pay lower interest rates than issuers who are deemed to be less creditworthy, whose investors demand greater compensation for risk.

“The scale of the combined entity is commensurate with an investment-grade rating,” Fitch said in a statement. “Combined reserves will approach 32 trillion feet of natural gas equivalent (Tcfe) and production will approach 7.9 billion cubic feet of natural gas equivalent a day (bcfe/d), making it the third-largest public global natural gas producer.”

Moody’s later followed suit by revising the outlook on its junk rating of Ba1 on each issuer to positive.

“The positive outlook points to the potential for an upgrade to Baa3 if the company can progress toward delivering on its debt reduction target and achieving synergies following the combination, and reduce its reserve replacement costs to generate more competitive returns on investment at mid-cycle natural gas prices,” Moody’s Senior Credit Officer Amol Joshi said in a statement.

Chesapeake

CHK,

will have 650,000 net acres in the Haynesville Shale and 1.2 million net acres in Appalachia, equal to 15 years of drilling inventory at the expected production levels.

Chesapeake will assume Southwestern’s

SWN,

debt after closing the transaction. Fitch expects the combined entity to maintain a sub 1.5x Ebitda (earnings before interest, taxes, depreciation and amortization) leverage after closing, strong liquidity and a back-end maturity profile.

The ratings agency is expecting to resolve the rating watch once the deal closes, which may take longer than six months, it added.

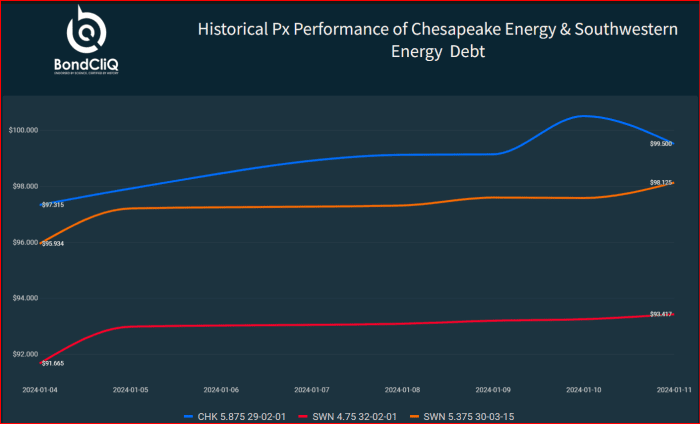

The companies’ outstanding bonds have been rallying for at least the last week, as the following chart from data-solutions provider BondCliQ Media Services shows. The Wall Street Journal reported on Jan. 5 that a merger was imminent.

Historical price performance of Chesapeake Energy and Southwestern Energy debt.

BondCliQ Media Services

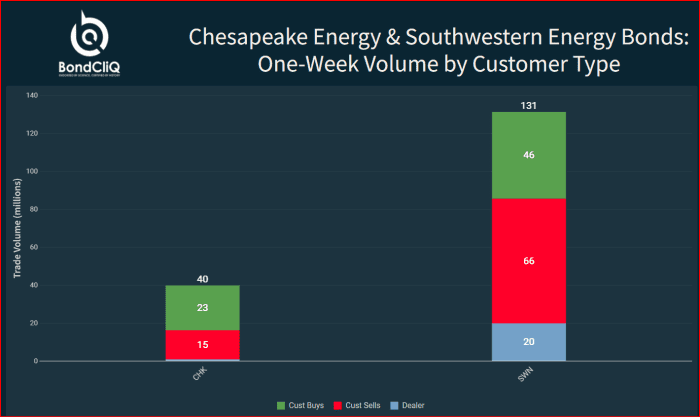

The companies have also seen net buying over the period, as the following chart shows, along with the volume breakdown by customer type.

Chesapeake Energy and Southwestern Energy bonds: one-week volume by customer type.

BondCliQ Media Services

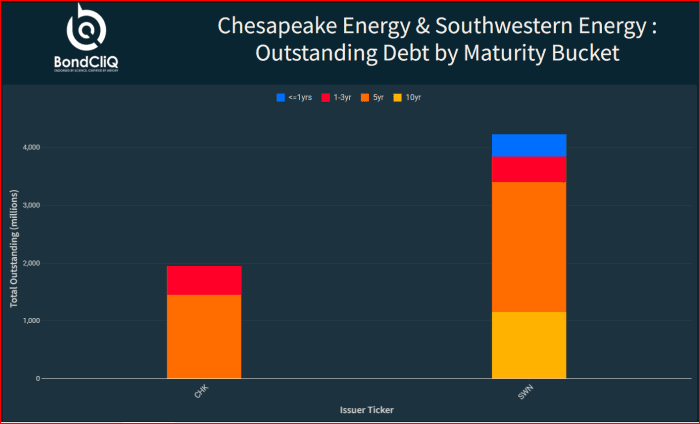

The next chart shows the debt by maturity bucket, with the bulk of the bonds issued by both companies in the five-year range.

Chesapeake Energy and Southwestern Energy: outstanding debt by maturity bucket.

BondCliQ Media Services

The deal announcement comes three years after Oklahoma-based Chesapeake emerged from bankruptcy on Feb. 9, 2021. The storied company, which was at the center of the fracking boom, had filed for chapter 11 protection in June 2020, as the COVID pandemic made Chesapeake’s debt load unbearable amid falling natural-gas prices.

It also comes during a wave of consolidation in the energy sector.

In the past month, Occidental Petroleum Corp.

OXY,

announced a $12 billion purchase of CrownRock LP, and APA Corp.

APA,

entered a deal to buy Callon Petroleum Co.

CPE,

valued at $4.5 billion.

The companies’ stocks, meanwhile, were mixed, with Chesapeake last up 4.8% and Southwestern down 0.6%.

Q2 2024 Earnings Call Transcript")