Justin Sullivan

In late December 2023, I upgraded Charles Schwab (NYSE:SCHW) stock from Sell to Hold, arguing that the U.S. brokerage firm is likely a key beneficiary of the 2024 expected rate cuts. Today I give SCHW shares another upgrade, as my latest view on the brokerage market suggests strong earnings upside thanks to the emerging bull market in equities, crypto and other tradeable asset classes. In fact, I argue that vibrant markets will inevitably lead to higher margin balances and trade volumes, which will compound the NIM-implied earnings tailwind from still-elevated rates over the next 12-24 months. This overall positive view on Charles Schwab is supported by robust February metrics, pointing to healthy, and accelerating commercial activity for the brokerage firm. Against the backdrop of positive and increasing commercial dynamics for Charles Schwab, I have revised my earnings per share forecasts for the company up to the year 2026; consequently, I now calculate a fair implied share price equal to $75.

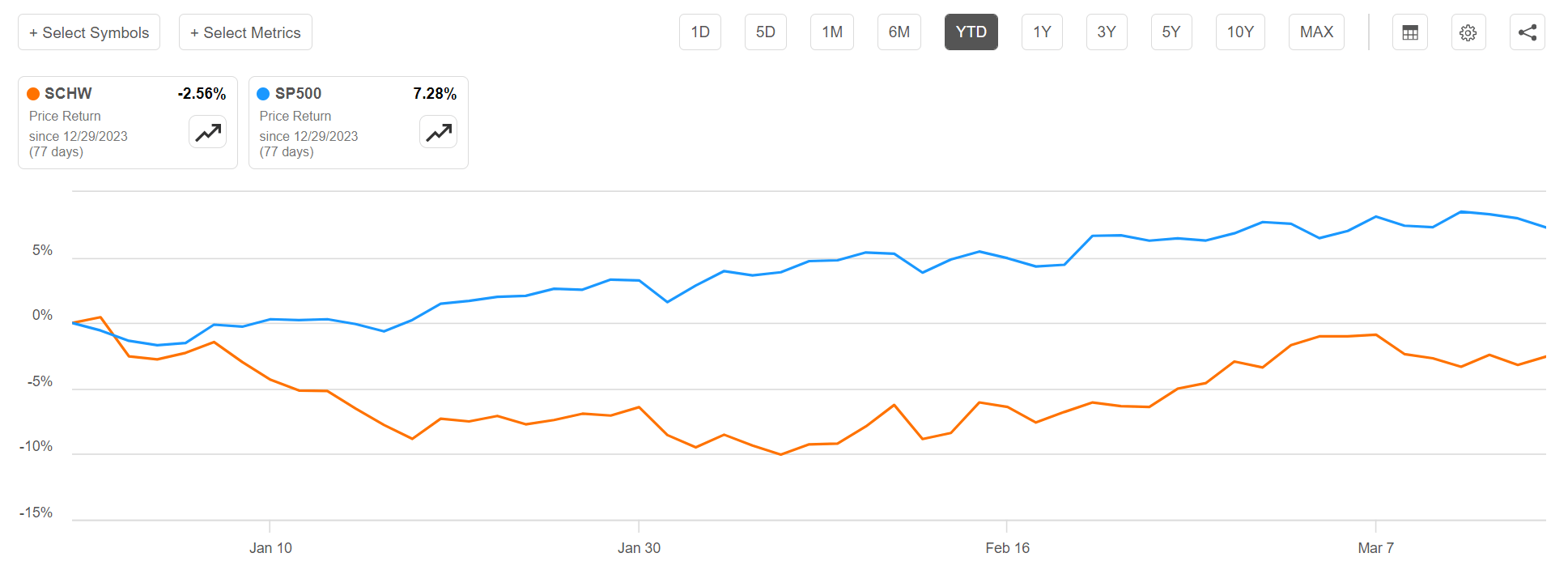

For context, Charles Schwab’s stock performance has underperformed the broader U.S. equities market year-to-date. Since the start of the year, SCHW shares are down almost 3%, compared to a gain of about 7% for the S&P 500 (SP500).

Seeking Alpha

Charles Schwab Closes A Strong FY 2023

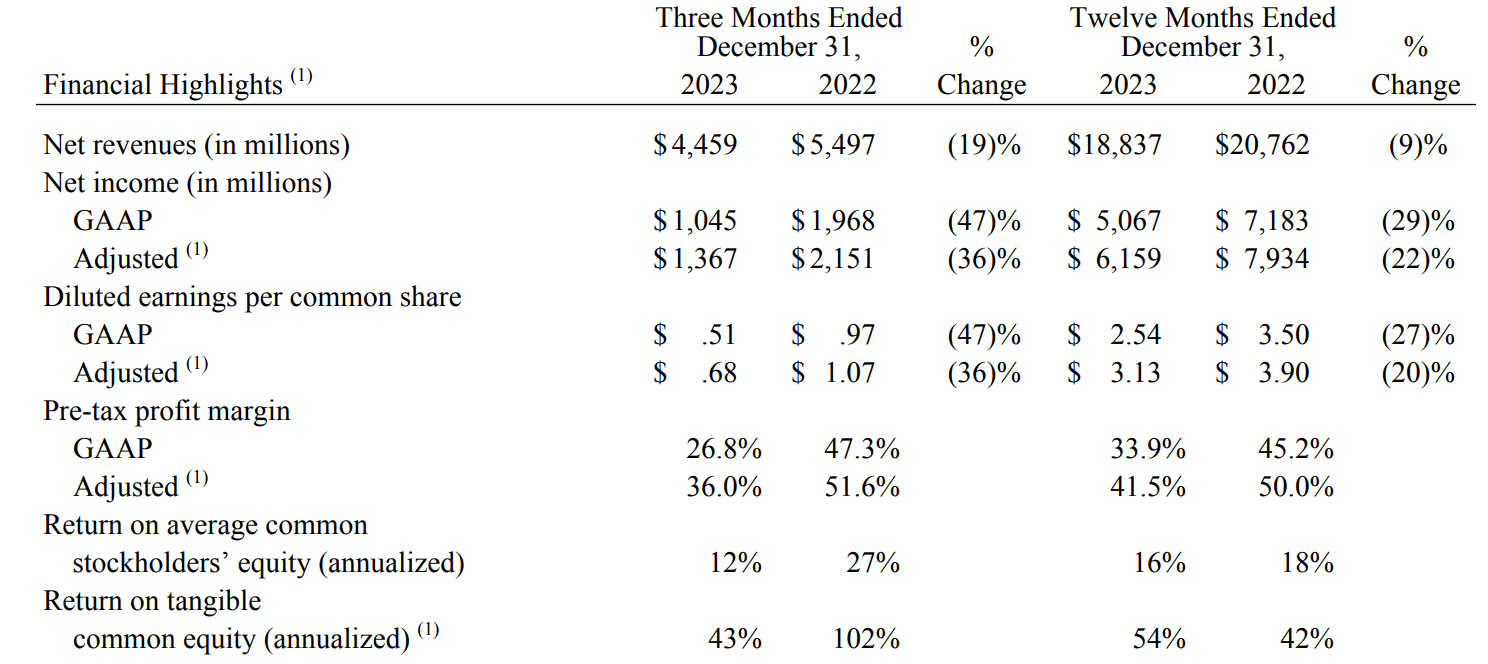

In mid-January, Charles Schwab opened its books for Q4 as well as FY 2023 and reported an overall strong set of results, despite headwinds relating to the Federal Reserve’s hawkish rate stance and the subsequent impact arising from the regional banking crisis in March: During the period from January to end of December, the brokerage company generated total revenues of $18.8 billion, down about 9% YoY compared to the $20.8 billion recorded in FY 2022. Investors should note, however, that the drop in revenue was primarily influenced by lower net interest income, as interest expenses surged from $1.5 billion in FY 2022 to $6.7 billion in FY 2023. As funding pressures are expected to fade through 2024, NIM growth should rebound. Meanwhile, Schwab’s revenue from capital markets activity posted a slight growth, led by strong asset management fee income: growing from $7.9 billion in FY 2022, to $8.0 billion in FY 2023.

On the profit side, after deducting $11.6 billion in operating expenses (up from about $11.0 billion in the previous year), Charles Schwab achieved a net income of $5.1 billion (down 29% YoY vs. $7.2 billion in FY 2022), and a return on average common equity of 16% (down 200 basis points YoY vs. 18% in FY 2022).

Throughout the year, Charles Schwab captured $306 billion in core net new assets, bringing total client assets to a record $8.52 trillion. In addition, Schwab welcomed 977 thousand new retail households and onboarded 315 transitioning advisors. Overall, the company registered 3.8 million new brokerage accounts, bringing total client account count to 34.8 million.

Charles Schwab Q4 2023 reporting

Early Insights In 2024 Look Bullish

The strongest argument about why Charles Schwab stock should deserve a Buy is, in my opinion, found in the emerging bull market for tradeable assets. This environment can be a major driver for commercial momentum for a brokerage firm for several reasons. Firstly, investors should consider that vibrant markets inevitably come with increased trading volumes for brokerage firms, boost high-margin revenue from transaction fees and commissions. For FY 2024 vs. 2023 I model about $500 million to $1 billion in revenue upside for Schwab, referencing that Schwab’s income from trading was about $4.2 billion in FY 2021, a bull market year, compared to only $3.2 billion in FY 2023. Secondly, I point out that Schwab is poised to benefit from higher asset values, because Schwab partially charges fees based on the percentage of AUM. Thirdly, I highlight that a bull markets is poised to attract new investors looking to capitalize on market gains. This leads to an increase in new account openings for brokerage firms, expanding the client base and potential revenue sources for brokerage firms. Lastly, I am bullish on Schwab’s outlook for increased margin lending, as bull markets are often accompanied by a significant uptick in leverage to purchase additional securities. This not only generates interest income, pointing to rates of up to 13.6%, but also increases the firms’ transaction volumes.

Considering the above points, I argue there is more room for Charles Schwab to surprise to the upside in 2024, a thesis that is broadly supported by encouraging monthly metrics YTD. Zooming in on the February release, I highlight that core net new assets increased significantly, by $33.4 billion. Moreover, client engagement showed strength, with daily trades rising to 6.121 million from 5.856 million in January. Lastly, average margin loan balances closed at about $63.6 billion, up 5% YoY.

Valuation Update: Raise Target Price To $75

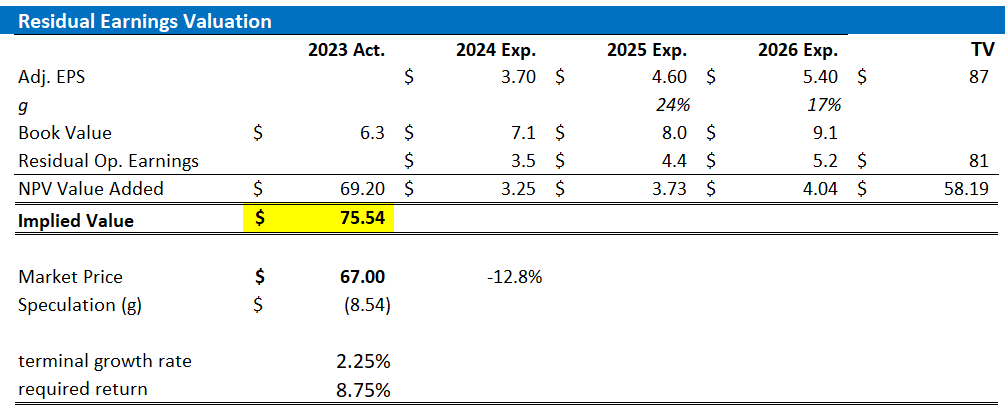

Motivated by a robust financial year 2023 and optimistic preliminary supportive metrics in the first quarter, I am updating my residual earnings forecast for Charles Schwab stock. I now project that Charles Schwab’s earnings will range from $3.6 to $3.8 (non-GAAP) for the fiscal year 2024. For the fiscal years 2025 and 2026, I expect earnings to be $4.6 and $5.4, respectively, with a subsequent average annual growth rate in earnings of 2.25% after fiscal year 2026. For the 2024-2025 growth expectation, I base my starting value for EPS on consensus estimates as collected by Refinitv. On top of this, I model a 10-15% uplift on earnings, as I believe analyst consensus is lagging to incorporate the strong trading/ margin momentum that Schwab is seeing and disclosed in the latest monthly metric reports. Additionally, I maintain my equity cost assumption at 8.75%. My cost of equity assumption is mostly a function of the CAPM framework, assuming a 1.1 adjusted beta to the S&P 500, as well as a 2.0 – 2.5% long-term risk-free rate, as guided by the Fed.

Based on these revised assumptions, I now estimate Charles Schwab’s fair stock price to be $75.54, a notable increase from ,y previous estimate of $59.

Refinitiv; Company Financials; Author’s Calculations

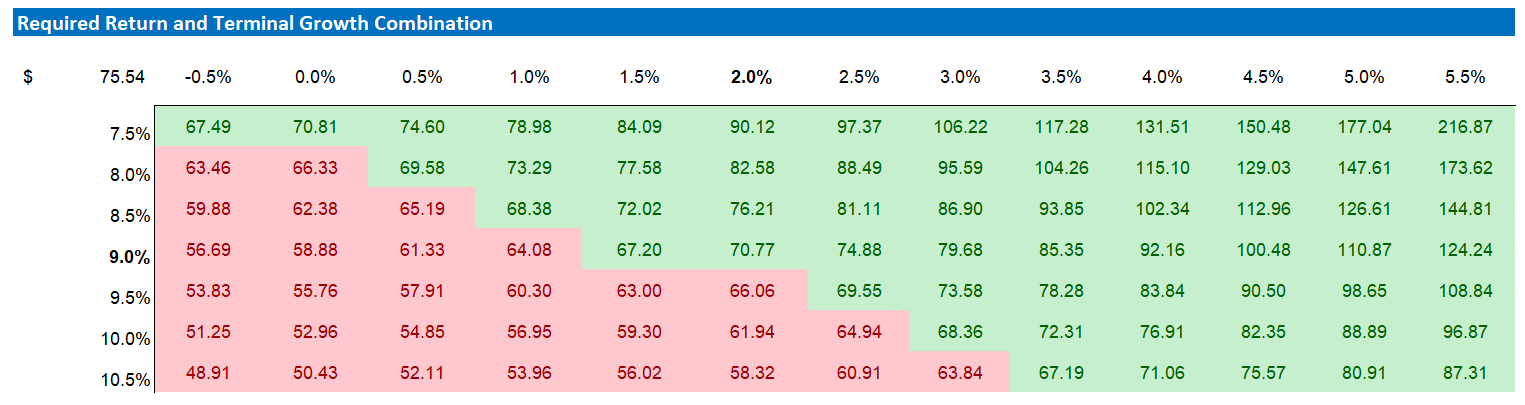

Below is also the updated sensitivity table.

Refinitiv; Company Financials; Author’s Calculations

A Note On Risks

In summary, I regard Charles Schwab as one of the strongest brokerage firm globally. The firm’s ongoing momentum with both new and existing clients diminishes my concern regarding competitive threats. Additionally, with Charles Schwab’s steadfast commitment to a digital-first strategy, I foresee minimal risk of significant disruptions to its business model. From my perspective, the primary risk to Charles Schwab’s growth and earnings trajectory stems from macroeconomic factors. Specifically, investors should note that the positive outlook for Charles Schwab stock is predicated on the expectation of increased margin financing and trading volumes, which are largely contingent on the continuation of the current bull market. Should there be a significant downturn in the stock market during the forecasted period, there could be a notable decrease in demand for Charles Schwab’s offerings.

Investor Takeaway

In late December 2023, I upgraded Charles Schwab stock from Sell to Hold due to expected benefits from 2024’s rate cuts. I am now further upgrading SCHW shares, anticipating strong earnings from the growing bull market in equities and other assets. This outlook, backed by February’s strong metrics, suggests increased trading volumes and margin balances, likely boosting earnings over the next few quarters. Given these factors and improved commercial dynamics, I am also updating my valuation model anchored on earnings through 2026, setting a new fair share price at $75.

Q2 2024 Earnings Call Transcript")