Nastco

Welcome to another installment of our CEF Market Weekly Review, where we discuss closed-end fund (CEF) market activity from both the bottom-up – highlighting individual fund news and events – as well as the top-down – providing an overview of the broader market. We also try to provide some historical context as well as the relevant themes that look to be driving markets or that investors ought to be mindful of.

This update covers the period through the second week of March. Be sure to check out our other weekly updates covering the business development company (BDC) as well as the preferreds/baby bond markets for perspectives across the broader income space.

Market Action

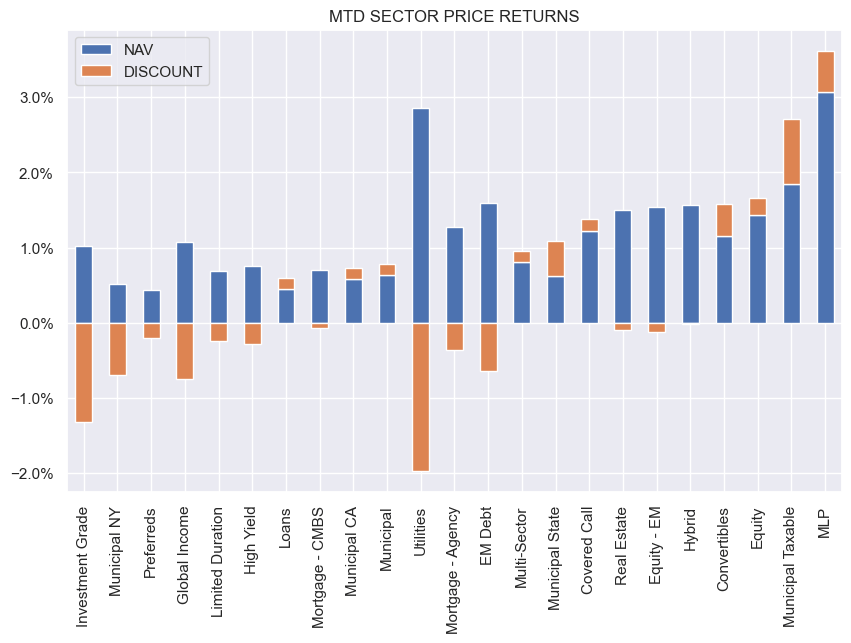

It was a good week for CEFs with all sectors enjoying a rise in NAVs, however discounts were mixed. Mostly equity-linked sectors finished in the lead.

Systematic Income

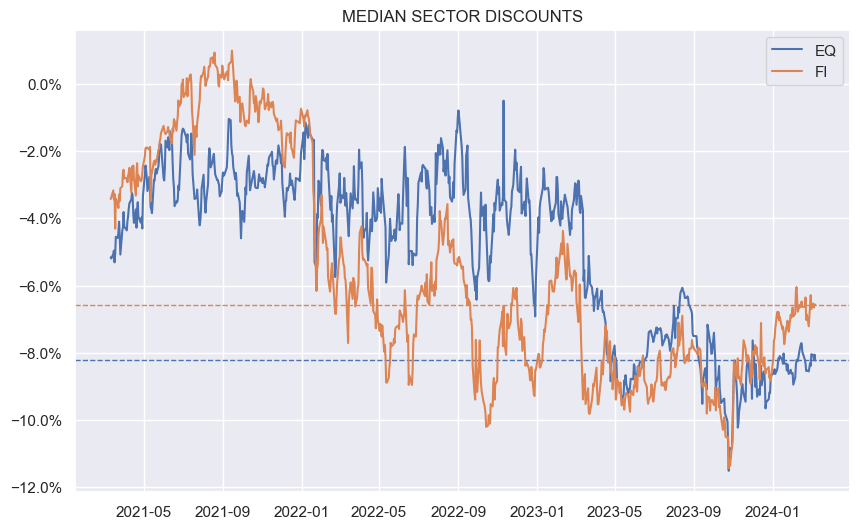

The gap between fixed-income and equity CEF sector discounts remains. The aggregate CEF discount remains wider of its longer-term average; however, this is largely due to a handful of sectors such as Munis and Covered Calls with the rest of the CEF space now trading around their longer-term averages.

Systematic Income

Market Themes

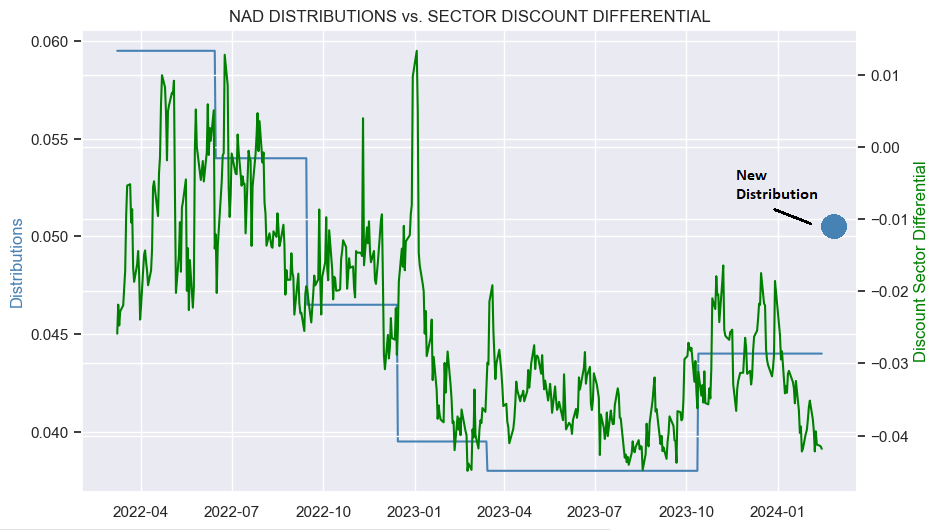

If at first you don’t succeed… Nuveen is having another go at boosting the discounts of their Muni CEFs by hiking distributions. The reasoning in the press release was the same – to improve market liquidity and to tighten discounts. The former is a catch-all generic reason that managers use for anything they do. And on the latter, recall that the previous sizable hikes didn’t make much of a dent in the discounts. If anything, it has been the recently broad-based market rally which has tightened Muni CEF discounts somewhat.

The chart below shows that while the distribution has grown for NAD (blue line / dot), its relative discount has actually widened – NAD trades at a discount 4% wider than the sector average which is the widest level over the past year. In other words, Nuveen’s move has failed so far for NAD and many others of its funds.

Systematic Income

Realistically, we may have to wait for leverage costs to fall before Muni CEF discounts tighten convincingly. The hike in distributions in the absence of net income gains has not convinced the market.

Market Commentary

The Virtus Convertible & Income 2024 Target Term Fund (CBH) sharply reduced its distribution. CBH is a target term CEF with a termination date in 2024. The press release mentioned the fund has rotated into short-term securities in anticipation of its termination. As is fairly common knowledge, term CEFs don’t always terminate. And a manager like Virtus which has been busy acquiring existing CEFs from smaller shops (e.g. Allianz, Voya), may not be particularly keen in losing assets and fees.

However, a target term CEF structure (as opposed to a plain term structure) is a bit more difficult to turn into a perpetual fund as it would require a nearly total turnover of the portfolio as well as a shift in strategy. If the fund actually terminates, it’s likely this feature which is responsible. In this sense, target term CEFs are more likely to terminate than plain term CEFs.

The PIMCO Dynamic Income Strategy Fund (PDX) made a bunch of changes in its distribution. First, it hiked the distribution by over 18% from $0.22 to $0.26. Then it switched over from a quarterly to a monthly distribution. And finally, that monthly distribution was hiked as well – from $0.0867 (the new $0.26 quarterly distribution / 3) to $0.1133 – by over 30%.

Net net the distribution was hiked by 55% and changed to a monthly profile. These changes were expected and discussed in our last update. Although the size of the hike looks large, we are starting from a very low base of just a 3.8% distribution yield on NAV which brings us up to only 5.84% – a bit more than half of what the company’s other taxable CEFs distribute. Although the distribution should keep rising, we shouldn’t expect it to match the other taxable funds given the higher Energy sector profile of the fund (leaving net income lower than the more pure-play credit funds) and its higher management fee.

Stance and Takeaways

Muni CEF discounts remain very wide in both absolute and relative terms. Managers of these funds have tried to tighten them by hiking distributions. As we discussed recently, part of this is due to potential activist pressure with Karpus, in particular, sniffing around many funds. Ultimately, we believe Muni CEF discounts will tighten; however, investors may need to wait for the Fed to start to cut the policy rate first.

Check out Systematic Income and explore our Income Portfolios, engineered with both yield and risk management considerations.

Use our powerful Interactive Investor Tools to navigate the BDC, CEF, OEF, preferred and baby bond markets.

Read our Investor Guides: to CEFs, Preferreds and PIMCO CEFs.

Check us out on a no-risk basis – sign up for a 2-week free trial!

Q2 2024 Earnings Call Transcript")