Mario Tama

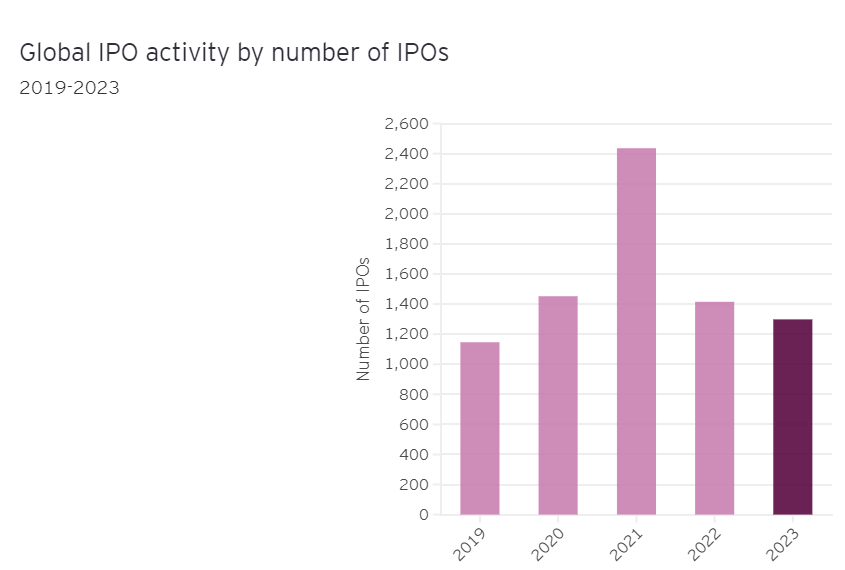

2023 was a less than stellar year for initial public offerings as the below graphic from Ernst & Young illustrates:

E&Y

The number of IPOs in 2023 was lower than 2022 and considerably lower than 2021. Still there were a few notable IPOs from the prior year.

Today, I’d like to discuss a founder-led company that debuted in 2023 that has caught the eye of numerous investors.

That company is CAVA Group, Inc. (NYSE:CAVA) Let’s dig into the details to see how this company has performed since going public and if this company is worth adding to your portfolio.

The Company

CAVA Group, Inc. is a Mediterranean restaurant company. The company was founded in Rockville, Maryland, in 2006 when three Greek Americans, Ike Grigoropoulos, Dimitri Moshovitis and Ted Xenohristos opened the first restaurant. Brett Schulman joined them in 2009 and became the company’s CEO. The company’s mission is to “Bring heart, health, and humanity to food.”

In fall 2018, the company acquired all of Zoes Kitchen, Inc. as part of their expansion strategy. CAVA went public in June 2023.

CAVA also has a line of dips, spreads and dressings which are sold in grocery stores across the nation, including Whole Foods.

As my readers will know, I am a fan of founder-led companies and it’s great to see several of CAVA’s founders are still with the organization. Brett Schulman is still the company’s CEO and Ted Xenohristos is CAVA’s Chief Concept Officer.

Moat and Opportunity

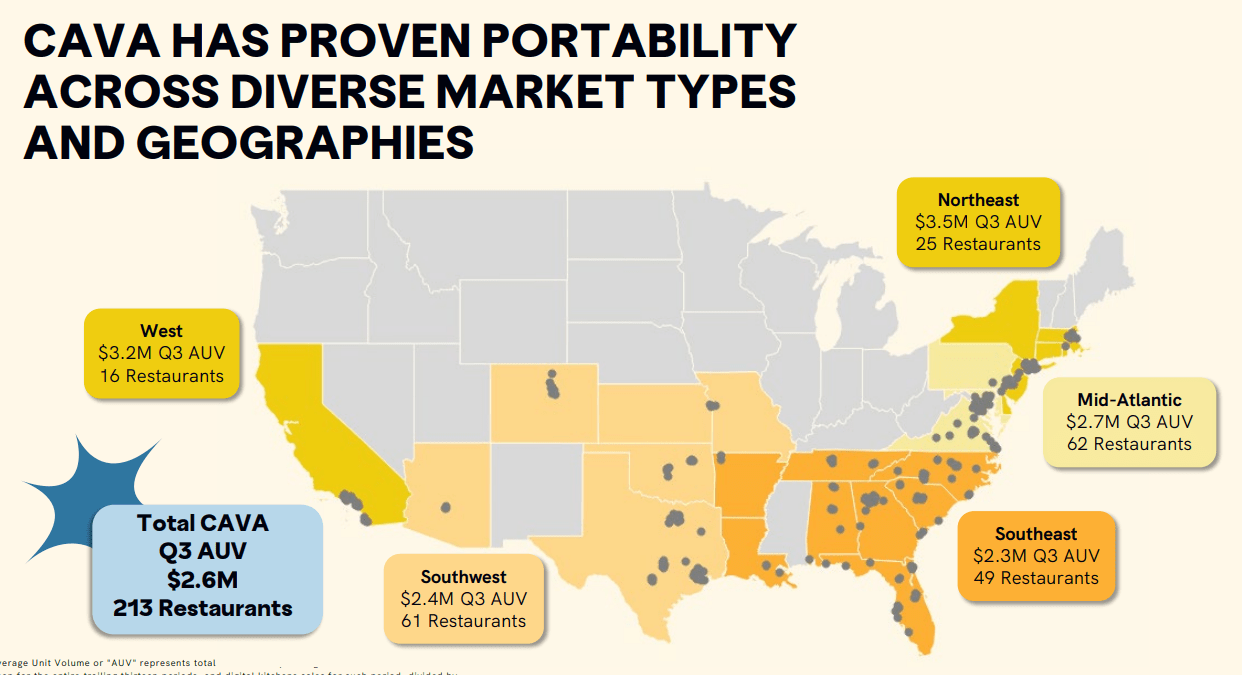

CAVA has a goal to grow the number of new units by at least 15% as stated on the company’s latest earnings release. In 2024, the plan is to add somewhere between 47 and 50 new stores. As you see from the below graphic, there are still a lot of opportunities for CAVA to grow, especially out West:

Investor Presentation

CAVA’s management team noted three strategic pillars for the organization moving forward. The first is solidifying the Mediterranean brand. To me, I think this really focuses on continuing to grow the number of units while ensuring their Mediterranean food is deliciously alluring to consumers.

The second strategic pillar is to develop a modern, best in class organization. This pillar really focuses on maintaining and developing talent. The company’s CEO Schulman noted the progress being made on this front as CAVA had a conference last September to bring all the restaurant general managers together to celebrate successes and share knowledge.

Additionally, on the Q3 earnings call, Schulman stated, “To support sustainable growth, we’re building a pipeline of qualified, highly engaged leaders with the skills to run great operations and provide fantastic guest experiences. In 2023, our target is to internally place 75% of our new restaurant GMs, and we remain on track to achieve that goal. Our Academy GM network supports this pipeline and serves as a farm system for future leaders. At the end of Q3, we had 45 Academy GMs, including 7 recently promoted to the multi-unit leader position. We plan to have 50 by the end of the year, enabling localized training in existing markets across the country.”

I think this pillar is vital to CAVA’s ongoing success and I applaud the organization for trying to create a positive culture for employees. The management team also noted CAVA is going to make sure employees are compensated competitively within the industry. Not all restaurant companies are taking such an approach. Sweetgreen (SG) appears to be de-emphasizing employees as the firm focuses on automation with their Infinite Kitchens. I’m much more in favor of CAVA’s approach as focusing on employees, cultivating and maintaining internal talent will lead to higher retention levels, getting CAVA closer to that goal of becoming a best in class, modern restaurant company.

The company’s last strategic pillar is to build the infrastructure to scale the business. On the Q3 earnings call, management mentioned a loyalty program was in the works and should be rolled out nationwide in late 2024. Many restaurant chains already have loyalty programs in place, and I’d view this program as a necessity for CAVA so they can keep customers coming back.

I’m not sure I would say CAVA has a moat. The company has many competitors in the fast casual restaurant space such as Chipotle (CMG), Panera, and Sweetgreen just to name a few. However, I do think CAVA is uniquely positioned. Compared to restaurants such as McDonald’s (MCD), Wendy’s (WEN) or Taco Bell (YUM), CAVA has healthier options and CAVA’s Mediterranean menu offers options such as their crispy falafel and spicy lamb meatball pita wraps can’t really be found elsewhere within the fast casual space. However, the company faces competition locally from other Mediterranean restaurants.

Management

Brett Schulman is the current CEO of CAVA and, as noted above, is one of the company’s co-founders.

Tricia Tolivar is the company’s Chief Financial Officer. Tolivar joined CAVA is 2020. Tolivar previously was the CFO at GNC and has held numerous leadership positions at Ernest & Young.

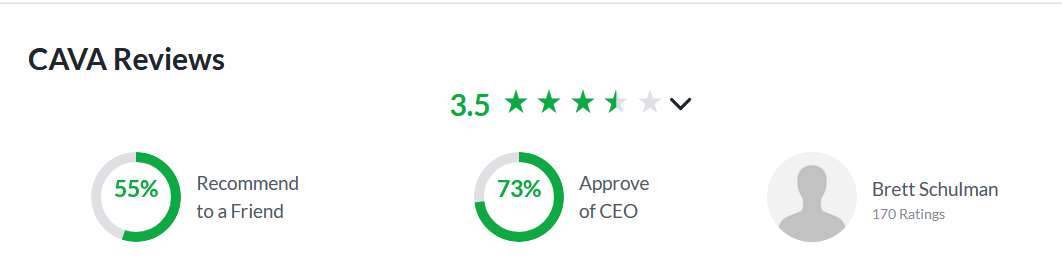

As you can see from these Glassdoor ratings, CAVA is viewed as a decent place to work and employees at the company approve of Schulman:

Glassdoor

Now 55% likely won’t be viewed as “great” by many readers but this is essentially a fast-food company (or fast casual). Also, both CAVA’s percentages (recommend to a Friend and Approve of CEO) are higher than Chipotle and much higher than Sweetgreen. Given the organization’s emphasize on employees and creating a first-class restaurant organization, I’d say CAVA is on its way to becoming a leader in the space.

Financials

Given CAVA has only been a public company for a short duration, there is limited financial data for the company. Nonetheless, the data available shows a compelling story as the company’s Q3 2023 results were impressive.

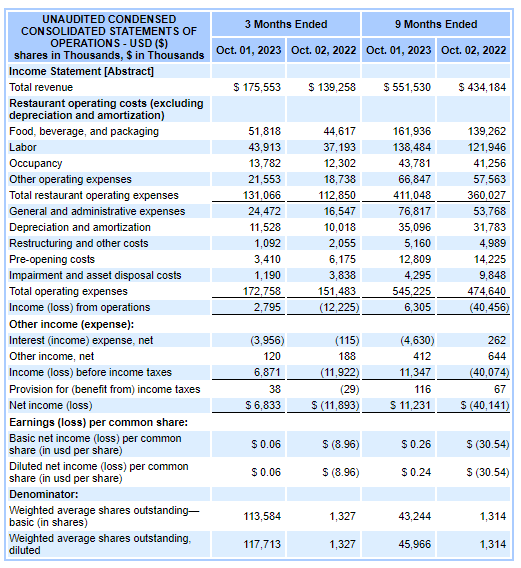

In the third quarter of 2023, CAVA delivered revenues of roughly $174 million, which is nearly a 50% increase compared to Q3 2022. Same store sales grew by 14% and management notes traffic increased by over 7% as well. CAVA also opened 11 net new restaurants for the quarter, bringing the total number of stores up to 290.

The company was profitable this quarter as well, as net income was roughly $6.8 million. Far better than the $11.9 million loss in the prior year quarter as you can see below:

SEC.gov

This turn to profitability in such a short time frame is impressive. For comparison, Sweetgreen, another newer restaurant company (which I reviewed here), still has yet to turn profitable and on their last 10-K Sweetgreen noted, “our net losses may increase while we continue our planned expansion.”

In today’s economy with higher interest rates and a more price sensitive consumer, companies must focus on profitability. I don’t believe the growth-at-all-cost playbook which occurred several years back will work in the years to come.

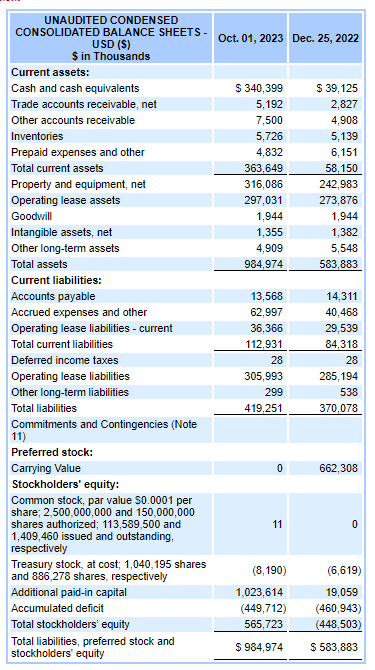

CAVA has a decent balance sheet as you can see below:

SEC.gov

The company’s cash balance has grown considerable since December 25, 2022, and now the current assets can more than cover the firm’s current liabilities. That wasn’t the case in December 2022.

Risks

CAVA faces numerous risks, but today I’m going to discuss the two main concerns I have about the company.

First, food safety is a clear risk. Various restaurant companies such as Chipotle have had food safety issues in the past. This really goes hand-in-hand with brand image. If the organization has a food safety issue, this would certainly impact CAVA’s brand and would hurt the company in their expansion efforts.

Secondly, as CAVA just went public, there is only limited data available to investors. Generally, I don’t like buying IPO companies within the first year. I find most of these companies are overvalued (which I’ll discuss below), have limited information, and management can’t be entirely trusted yet. Thus far, Schuman and team appear to be doing a great job yet with only a few quarters in as a public company I don’t think you can completely reply on the word of management as you need a few quarters to see if management hits the targets they set and make strides towards company’s objectives.

Valuation

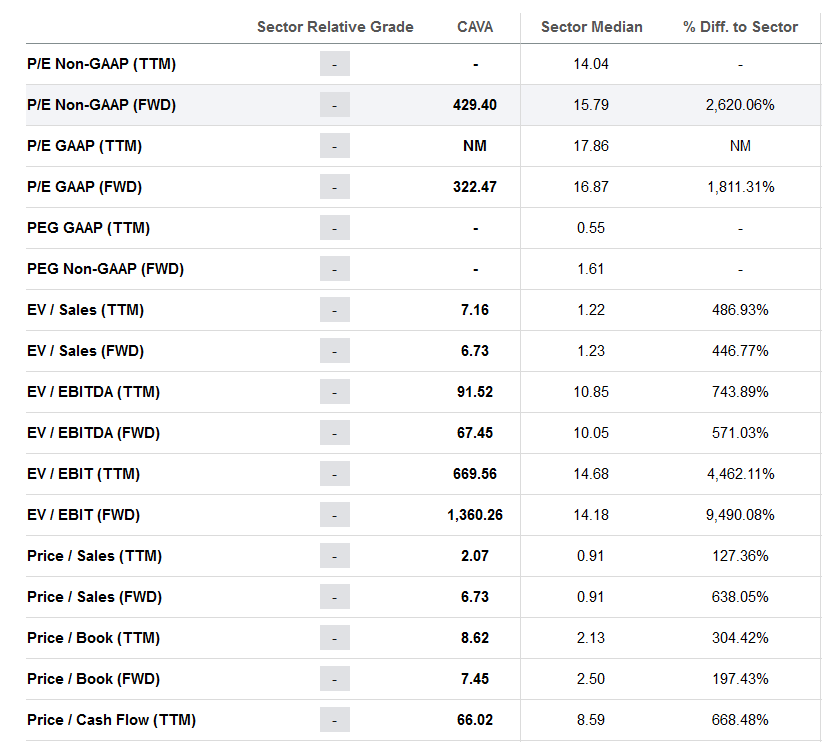

Seeking Alpha doesn’t have a quant value grade for CAVA yet, although it does have several metrics listed:

Seeking Alpha

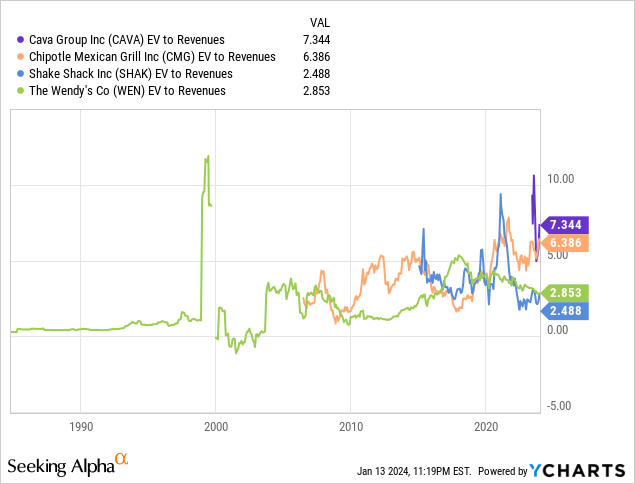

At this stage, I think EV/Sales or Price to Sales are the more appropriate measures to value CAVA. As you can see from the below, in comparing the EV to Revenues of CAVA to Shake Shack (SHAK), Chipotle and Wendy’s, CAVA exceeds all of those companies. Also, as noted, CAVA is far above the sector median which is 1.22.

CAVA does have significant growth potential, yet given this current valuation, I’d prefer to buy CAVA once it gets closer to the sector median or at minimum closer to Chipotle’s 6.3 EV/Sales.

Conclusion

I’m impressed with CAVA thus far despite only being a public company for a short duration. The revenue growth and turn to profitability is impressive.

I like that CAVA’s founders are still with the company, and I believe the company is making excellent strategic decisions such as continuing to add new stores, train and educate employees while compensating them appropriately, and establishing a loyalty program.

However, the company is priced at a premium even with the CAVA’s growth prospects.

While I like what I see thus far, I’m going to hold off for now. I want to continue to see the company’s management team execute for a few more quarters before I think about buying shares.

Q2 2024 Earnings Call Transcript")