Kirk Fisher/iStock Editorial via Getty Images

Caterpillar Stock Heading Into Earnings

Caterpillar’s stock (NYSE:CAT) soars and soars, hitting almost quarterly new all-time highs. And, yet, compared to many other successful stocks in today’s market, Caterpillar shares keep on trading at a rather cheap valuation, with a fwd PE of 14.6 which is below the current S&P 500 PE ratio of 26.6.

Caterpillar is a global leader as a manufacturer of construction and mining equipment and operates in three primary segments: Construction Industries, Resource Industries, and Energy & Transportation. All of these segments are supported by the Financial Products segment. While all of these segments achieve great success, Caterpillar’s service business is the golden goose because it generates high-quality revenue thanks to its higher margins and recurring nature.

While the stock just recently breached the $300 per share threshold, investors are wondering whether Caterpillar is a good investment right now. Fear of missing out (FOMO) may also be felt. Therefore, we will look at the company as its Q4 23 earnings report draws near and assess it to see if there is an opportunity for us or not.

Caterpillar Benefits From Secular Tailwinds

Before we move to the earnings forecast, we can’t overlook some strong macro-trends that benefit Caterpillar. In particular, I will highlight three of them:

- The Infrastructure Investment and Jobs Act approved in late 2021 is pumping money into construction equipment use and demand.

- Revitalization of American manufacturing is now a political priority for the U.S.

- The role of critical minerals in the transition to clean energy has galvanized mining activity, increasing the need for highly technological and competitive equipment.

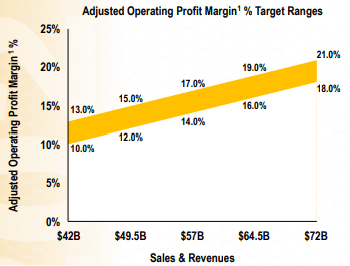

We need to be aware of these trends not only because they are in favor of Caterpillar’s top-line growth, but also because, as Caterpillar grows in size, its scale can lead to higher margins, as we can see from the graph below.

CAT Q3 2023 Earnings Presentation

This means that every additional dollar in revenue will generate more profits for the leader of the industry.

Caterpillar’s Sales Mix By Segment And Region

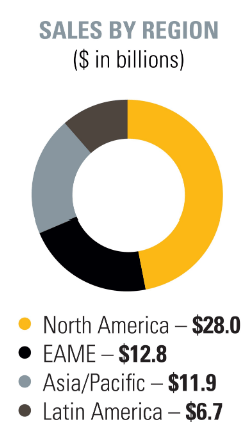

While we wait for Caterpillar to release its FY23 results, we can look at the last annual report available to see how the company’s sales were split by region and by segment.

North America alone makes up around 45.6% of total revenues, with EAME and Asia Pacific accounting for a rough 20% each.

CAT Investor Relation Webpage

If we break down Caterpillar’s sales by segment, we see that Construction Industries brought in around $25.3 billion in revenue, Resource accounted for $12.3 billion while Energy & Transportation performed quite well reaching $23.8 billion in revenue. This means Construction makes up 41.2% of total revenues, Resource accounts for 20% and E&T brings in almost 38.7%.

Why is this important? Because, to assess Caterpillar, we need to know how North America is doing and how Construction, together with Energy, is performing.

Caterpillar’s Financials

Some investors might be surprised by what I want to show as a particularly interesting metric. Considering it is an industrial, its capex is extremely low and well under control. Caterpillar’s TTM revenues are $66.6 billion, while its TTM capex is $2.9 billion, which is 4.4% of total revenues. Deere’s (DE) TTM capex, for example, is $4.3 billion compared to total revenues of $61.2 billion (7%).

Moreover, depreciation & amortization is decreasing over time and now stands at $1.83 billion. What does this mean? Caterpillar seems to be trying to become as capital-light as possible. On its balance sheet, its net property, plant & equipment item is also decreasing. Ten years ago it was $13 billion, the most recent report showed only $8.2 billion.

This goes along with what United Rentals is reporting: companies are shifting more and more toward rentals because it makes their balance sheets leaner.

Caterpillar’s capex in Q3 was around $400 million. This makes me expect the company will close its fiscal year with a capex of around $1.5 billion. The balance sheet therefore will be even stronger, holding ample liquidity of $6.5 billion, supported by an additional $4.3 billion Caterpillar holds in longer-dated liquid marketable securities to improve yields on that cash. Its total debt is $37.2 billion, but this takes into account the debt from the financial services branch. I haven’t been able to find a breakdown to understand what Caterpillar’s industrial debt is, but I am inclined to think it is very low, if not zero.

Caterpillar’s Peers Hint At What Its Report May Look Like

In this earnings season, several companies correlated with Caterpillar have reported. On one side, most of the Class 1 railroads reported increasing rail traffic. This is a good sign that manufacturing activity is picking up speed once again. But what matters even more for the needs of this article can be found in the reports of two other companies: United Rentals (URI) and The Volvo Group (OTCPK:VLVLY).

United Rentals reported better-than-expected results, highlighting during the earnings call that in its construction segment, both infrastructure and non-residential continued to do great. Geographically, United Rentals reported strength across its whole business. Since United Rentals rents equipment, it offers the pulse of the economy, in particular, it can tell us if people across the country are involved in construction projects, thus increasing the overall demand for the right equipment.

The Volvo Group is another interesting company to look at to gauge what to expect from Caterpillar. The Swedish truck manufacturer doesn’t only produce trucks, nor does it operate only in Europe. It has a construction segment that makes up around 20% of the company’s revenues.

Now, The Volvo Group reported weak performance in construction. However, it was mainly due to Asia and Europe, with deliveries down 40% and 4% and orders down by 39% and 9% respectively. So, while for the Volvo Group Europe is the main market, for Caterpillar it isn’t. Moreover, The Volvo Group actually reported strong performance in construction in North America, with deliveries flat YoY but orders up a staggering 173%.

Caterpillar Is Likely To Beat Estimates

From what we have just seen, Caterpillar is surely seeing a favorable environment in North America. It would not be surprising to see this core region jump up to around 50% of total sales, given on one side its strong performance and, on the other, the weakening outlook for other key regions such as Europe and China. During the last earnings call, Caterpillar’s management did talk about “positive momentum […] in non-residential construction in North America due to the impact of government-related infrastructure investments”.

Moreover, Caterpillar ended Q3 with a backlog of $28.1 billion, which is equal to almost 50% of FY22 revenues. Caterpillar’s backlog extends well into 2024, making the company comfortable in expecting another good year. In fact, Caterpillar’s management disclosed the backlog as a percentage of TTM monthly revenues for the past few years. In 2017, it was 37%, in 2018, it was 32%. Currently, it’s around 44%. This leaves Caterpillar with room to see its backlog go down without creating particular issues.

In Q4, the company’s guidance indicates slightly higher sales YoY with pricing still favorable. However, we should not see a big top-line jump because, by now, we have overlapped the big price hikes the company applied in 2022.

Among the three business segments, according to the guidance given by Caterpillar at the end of Q3, we should see the Energy & Transportation segment as the best performer due to higher solar turbines and rail deliveries.

As a result, I expect Construction Industries to report total sales of around $6.8 billion (flat YoY). However, I believe its order book has grown in the past quarter, due to the results other companies reported. Resource Industries should be down a bit to $3.3 billion (-3%). Energy & Transportation will likely be up 8% to 10%, so I expect a quarterly revenue of $7.5 billion, making it the top segment in Q4.

This leads me to a total revenue estimate of $17.6 billion, which is a 6% increase YoY and a 2.7% surprise compared to the current revenue estimate for Caterpillar.

As we can see from the graph below, Caterpillar has usually beat analysts’ estimates by 2-4% in the past 12 quarters. So, I think we should see something similar this time, too.

Seeking Alpha

Considering Caterpillar’s profitability reports a net income margin of 13.7%, we can expect a quarterly net income of $2.4 billion. Dividing by the number of shares outstanding (509 million at the end of Q3), I reach an EPS estimate for Q4 of at least $4.72, not counting the effect of buybacks during Q4. This leads to a FY23 EPS of $20.70 which makes Caterpillar trade at a TTM PE of 14.9. Even more compelling, CAT shares trade at a free cash flow yield of 6.2%. True, Caterpillar is a bit cyclical, and at the end of the cycle, it usually generates more free cash flow than usual.

Conclusion

Caterpillar’s valuation is still not as demanding as that of many other stocks in today’s market. However, looking at the company’s trading range, I still don’t see a particular discount that can make me jump in and buy some shares. For now, I rate the stock as a hold. For sure, those who are invested in it are doing great. But those, like me, who haven’t been able to initiate a position, should wait for a pullback to enjoy a larger margin of safety.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")