Alexander Farnsworth/iStock via Getty Images

In November 2023, I wrote about Caribou Biosciences (NASDAQ:CRBU), rating it a buy based on the data with its off the shelf CAR-T therapeutic CB-010, from which I expected more positive data in 2024, its pipeline and plentiful cash. CRBU is up just 9% since then, despite positive updates and the larger rally in biotech. This article looks at those updates, and reconsiders the buy rating I originally gave CRBU.

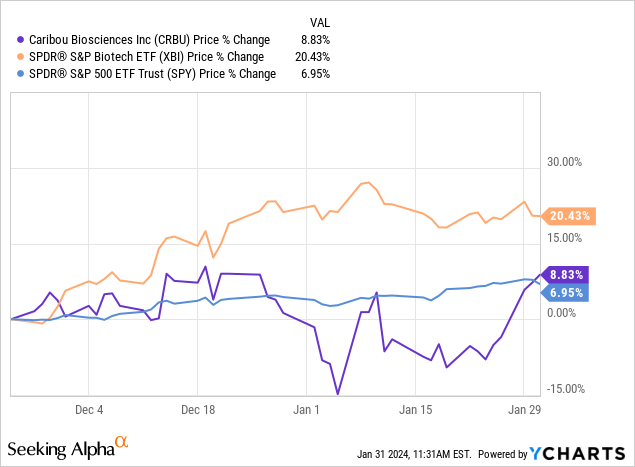

Figure: CRBU trading since my November 2023 article, versus key indices.

An important regulatory update

In my previous article, I noted a major risk with any long position in CRBU related to interactions with the US Food and Drug Administration (FDA).

The most obvious risk I see to CRBU near-term would be an update on FDA discussions regarding a pivotal trial of CB-010 in second-line LBCL [Large B Cell Lymphoma] patients.

Biotech Beast, November 2023.

On December 12, 2023, CRBU provided a regulatory update noting the FDA found CRBU’s proposed comparator arm, for a pivotal study of CB-010 in second-line relapsed/refractory large B cell lymphoma (r/r LBCL), to be acceptable. That comparator arm is immunochemotherapy then high dose chemotherapy with autologous stem cell transplantation. While CRBU is still collecting more data from the dose expansion portion of its ANTLER phase 1 study of CB-010, it plans to start the pivotal study by year-end 2024.

Clarity on timing of 2024 catalysts

In the near-term then, the key catalyst is additional data from the ANTLER trial, from which we have clarity on timing. The December 12 update came with news that initial data from the dose expansion of antler was expected in Q2’24. I had previously speculated that a readout in Q1’24 was possible, since CRBU had only guided for H1’24 but the update has made clear that won’t be the case. Nonetheless, the stock traded up not down with the December 12 update, so clarity that the catalyst would come in Q2’24 wasn’t received poorly.

Regarding CB-011, a January 7, 2024, press release confirmed that CaMMouflage, a phase 1 trial of it CAR-T therapeutic CB-011, would produce initial data by year-end 2024.

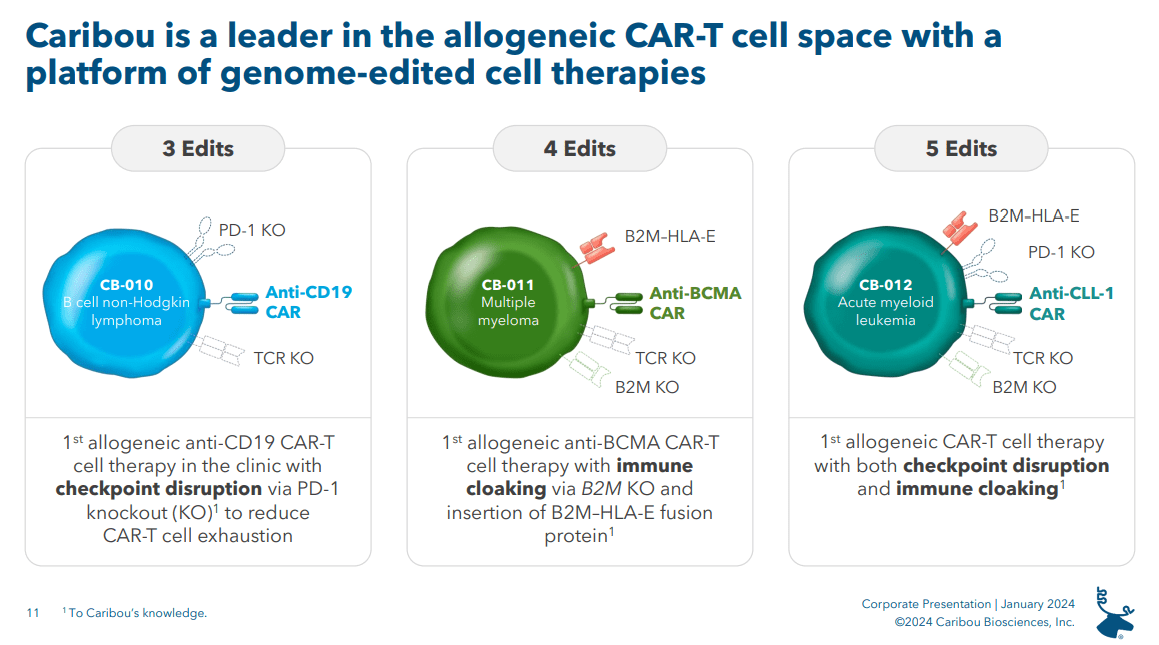

Figure: Overview of CRBU’s three CAR-T therapeutics. Note that CRBU also has a CAR-NK cell therapeutic in its pipeline, albeit at the preclinical stage. CB-011 (central panel) is in a phase 1 trial called CaMMouflage in multiple myeloma patients. (CRBU Corporate Presentation, January 2024.)

Notably, CRBU also updated that it had completed dosing at the second dose level (150M cells) in CaMMouflage, and had moved on to the third dose level (450M cells). While this is a minor update it means there wasn’t excessive toxicity at 150M cells. These dosage ranges are similar to what has been used in the development of other anti-BCMA CAR-T’s (see table 2 for several examples). For example, Bristol-Myers Squibb’s (BMY) Abecma has a recommended dose of 300M to 460M CAR-T cells. As such the current dosages aren’t leagues below where we might expect to see efficacy, if CB-011 is effective, and so the lack of excessive toxicity so far is encouraging.

It’s also worth commenting on the comparison between the doses of CB-011 being trialed in multiple myeloma compared to the doses of CB-010 which was dosed at levels of 40M, 80M, 120M cells in the phase 1 ANTLER study (in B-cell Non-Hodgkin lymphoma patients). CRBU’s CEO noted at the recent JPMorgan Healthcare Conference in a presentation on January 11 that the PD-1 knockout in CB-010 theoretically increases the therapeutic index of CB-010, allowing it to be dosed at lower levels than the average CAR-T therapy. For example, note in the figure above that PD-1 knockout is designed to reduce CAR-T cell exhaustion. With less CAR-T cell exhaustion, a lower dose of CAR-T cells can be used and it seems that was indeed the cases with CRBU seeing responses with just 40M cells of CB-010.

Previously, attempts have been made using other CAR-T therapies (that don’t have PD-1 knocked out), combined with antibodies known to interfere with PD-1-PDL1/L2 interactions (nivolumab, pembrolizumab) to reduce CAR-T exhaustion. Of course CRBU’s CB-010 takes away the need for that by just knocking out PD-1 in the first place.

Beyond CB-010 and CB-011, the third CAR-T therapeutic, CB-012 is also ready for clinical study. The AMpLify study of CB-012 in relapsed/refractory Acute Myeloid Leukemia (AML) is expected to start in H1’24, with some clinical sites already active.

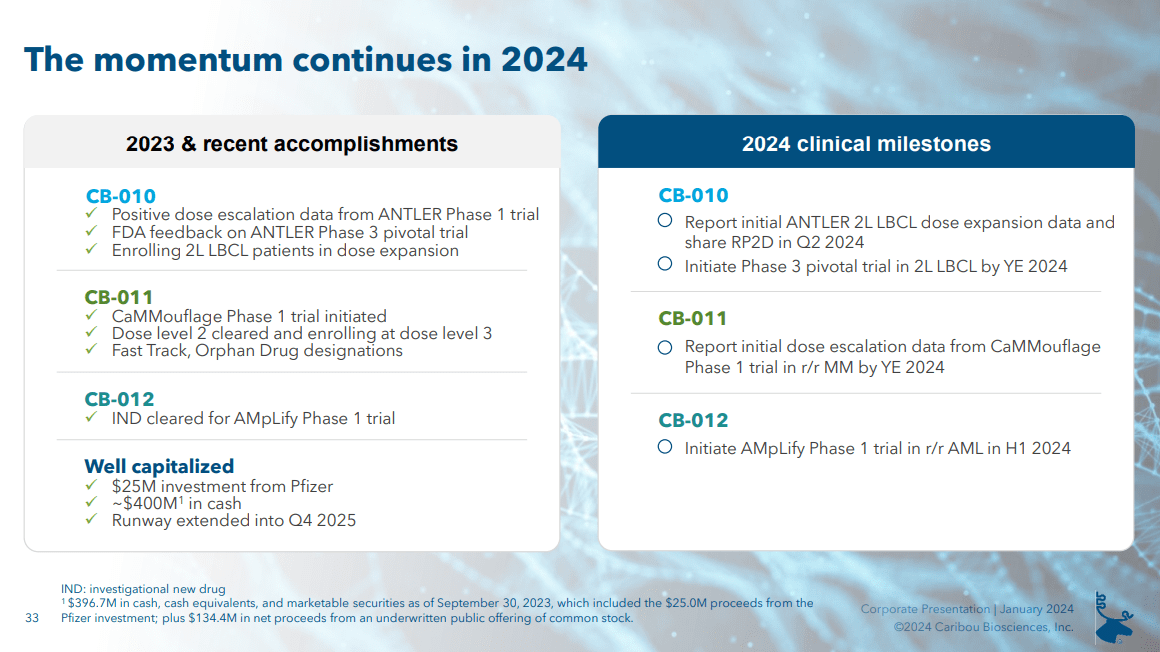

Figure: Outline of CRBU’s achievements and upcoming milestones. (CRBU Corporate Presentation, January 2024.)

Financials, conclusions and risks

There hasn’t been another financial update since my previous article, but I expect CRBU to report Q4’23 and full year 2023 earnings around early March as it did in 2023. CRBU had cash, cash equivalents and marketable securities of $396.7M at the end of Q3’23 and net cash used in operating activities was $71.9M in the first 9 months of 2023. I’m not expecting year-end cash to be much below $370M.

Further, CRBU has a market cap of $543.85 at the time of writing ($6.15 per share), giving it an enterprise value under $200M. This is despite being perhaps just two months away from updated data from the ANTLER study. I expect those results to be positive, as the results from the first cohort patients in ANTLER were. Those results showed CB-010 could offer the efficacy of existing CAR-T’s like Gilead’s (GILD) Yescarta, which brought in $391M in Q3’23 alone, but in an off the shelf format (allogeneic) and potentially with less side effects. Further, if CRBU does see positive results from the updated dose expansion portion of ANTLER, it is ready to start the pivotal study by year-end 2024 and has alignment with the FDA on the comparator arm.

Beyond CB-010, CB-011 should produce initial data in 2024, adding another clinical catalyst to the calendar and doesn’t seem to be having overt toxicity issues at the two doses tested so far. Taking these positives updates, and coupling them with the fact CRBU hasn’t run up to the same extent as the rest of the biotech market, makes CRBU an even better buying long than it was a few months ago. As such, I rate CRBU a strong buy.

A major risk now that the regulatory update is out of the way and has been positive is that the updated ANTLER data could underwhelm. Initial data did set a high bar and was from only 16 patients.

Beyond the risk of ANTLER underwhelming, although there probably isn’t much expectation on CB-011, underwhelming results could make it clear that not all CRBU’s pipeline members are necessarily going to be a hit.

Lastly, CB-012 entering the clinic is another opportunity for a toxicity to arise that causes a halt. While I have no particular reason to believe this is the case, every new therapeutic in the clinic carries this risk, so it is a possibility that a halt could weigh on the stock.

Q2 2024 Earnings Call Transcript")