Rawpixel

Back in February, I place a “Buy” rating on CarGurus (NASDAQ:CARG), arguing that its results were being muddied by issues at CarOffer, but that its core business remained strong. The stock is up over 4% since then, trailing the 6% return from the S&P 500. Let’s catch up on the name.

Company Profile

As a refresher, CARG runs an online lead-generation and transaction marketplace for used and new automobiles. All dealers are permitted to put their inventory on its platform free of charge, although dealership info is severely limited and leads capped. It then offers several tiered paid subscriptions that give dealers much more features and exposure. Subscriptions prices vary based on a dealer’s inventory size, region, and expected ROI.

The company also owns a 51% in CarOffer, which runs an instant trade platform that lets dealers automate the wholesale car buying process using rule-based strategies. The company also applied the technology to its Instant Max Cash Offer, allowing dealers to purchase vehicles directly from consumers as well.

CARG also operates owns PistonHeads in the U.K., which is an automotive marketplace, forum, and editorial site geared towards automotive enthusiasts.

Q2 Shows CarOffer Issues Are Being Addressed

At the time of my original write-up, CARG had run into issues with its stake in CarOffer, which had gone from huge growth driver to a huge burden pretty quickly. The issue was that in a used car market that was seeing prices rapidly decline, dealers were starting to reject the vehicles it purchased as not being as described, starting an arbitration process that would see them send vehicles back to the company, which it then had to get rid of at lower prices, taking a loss in the process.

This led CARG’s Digital Wholesale business to go from recording adjusted EBITDA of $19.1 million in Q2 2022 to -$15.6 million in Q3 of 2022 and -$21.1 million in Q4 of 2022.

As a result, CARG had to pull back on and revamp the platform. The results of this work showed up in Q2, with the Digital Wholesale business seeing an -80% decline in revenue to $68.8 million, but with EBITDA turning positive for the first time since Q2 of last year, coming in at $4.2 million. Notably, arbitration and rematch rates declined -71% sequentially. With June and July very poor markets for used car pricing, the company meanwhile was able to pressure test its revamped platform.

Discussing CarOffer and its Digital Wholesale business on its Q2 earnings call, COO Samuel Zales said:

“Quite honestly, over those 3 quarters, we lost some dealer confidence in the platform until we changed our inspection work. We changed our arbitration process. We changed our sale rates. We changed our rematches. Our transportation has gotten tremendously better. Our title time to get titles to dealers buying has been phenomenally better. So we’re now building back that confidence in our customers and doing something more than that, which is building new tools to focus on gaining confidence in a system and instant trade platform that works perfectly in a price rising environment and has more caution in a price declining market for any of these dealers in the market. So we’re building things like the 24-hour with a look capability, which gives dealers the opportunity to be sure before they approve that transaction. … We’re adding a buy now capability, which many auction players use today, which is saying, I’ve got unsold inventory. … We’re adding mobile tooling to allow buyers and sellers to approve transactions more efficiently and effectively. … We now have to fight a macro environment to gain our volume going forward and doing that by building and rebuilding the confidence that dealers have in this platform, almost a CarOffer 2.0 and building that back up to get the volumes we want and play offense and run a growing and profitable business as we go forward.”

CARG’s core Marketplace business, meanwhile, remained solid. Revenue rose 4% to $171.0 million, while U.S. marketplace revenue also increased 4% to $158.4 million.

U.S. average monthly unique users increased 8% to 31.9 million, while international MAUs rose 12% to 7.4 million. U.S. paying dealers fell -1% to 24,220, while international paying dealers rose 3% to 6,877. Quarterly Average Revenue per Subscribing Dealer rose 6% to $6,110, while it increased 5% in international markets to $1,610.

Segment income, however, did fall -13% to $24.6 million, as the company added headcount to expanded its product offerings to build an end-to-end transaction-enabled platform. Companywide product and tech expenses rose 19%, while S&M and G&A expenses both fell around -19%.

Looking ahead, CARG guided for Q3 revenue of between $201-221 million and adjusted EBITDA of $36-44 million. It expects adjusted EPS of between 24-27 cents.

Overall, the big positive out of last quarter was how the company was able to fix the issues at CarOffer and produce positive EBITDA despite much lower revenues. While the environment for CarOffer remains difficult with used car prices continuing to decline, it should be able to go on the offensive once the environment stabilizes.

Meanwhile, its core business remains solid, and the company has solid pricing power, as evidenced by the price dealers are paying rising 6%.

Valuation

CARG trades at 10.5x the 2023 EBITDA consensus of $171 million, and 9.6x the 2024 consensus of $189 million. Analyst estimates are for consolidated EBITDA, and thus includes the full EBITDA of CarOffer, not just the 51% it owns.

Rival Cars.com (CARS) trades at 8.2x 2024 EBITDA, while British firm AutoTrader trades at nearly 16x FY24 (ending in March) estimates.

I’d value the CARG’s core business at around $20-22 per share, about a 12x multiple on its 2024 core EBITDA, at a minimum given the platform’s dominance in the U.S. market place. But I could easily see investors valuing it even higher, as a 15x EBITDA multiple similar to Autotrader, which has a similar dominant position in the U.K., would put the business at around $27. Meanwhile, I think its 51% stake in CarOffer is worth another $1 or $2 as it returns to EBITDA positive. (12x EBITDA of around $20 million).

Conclusion

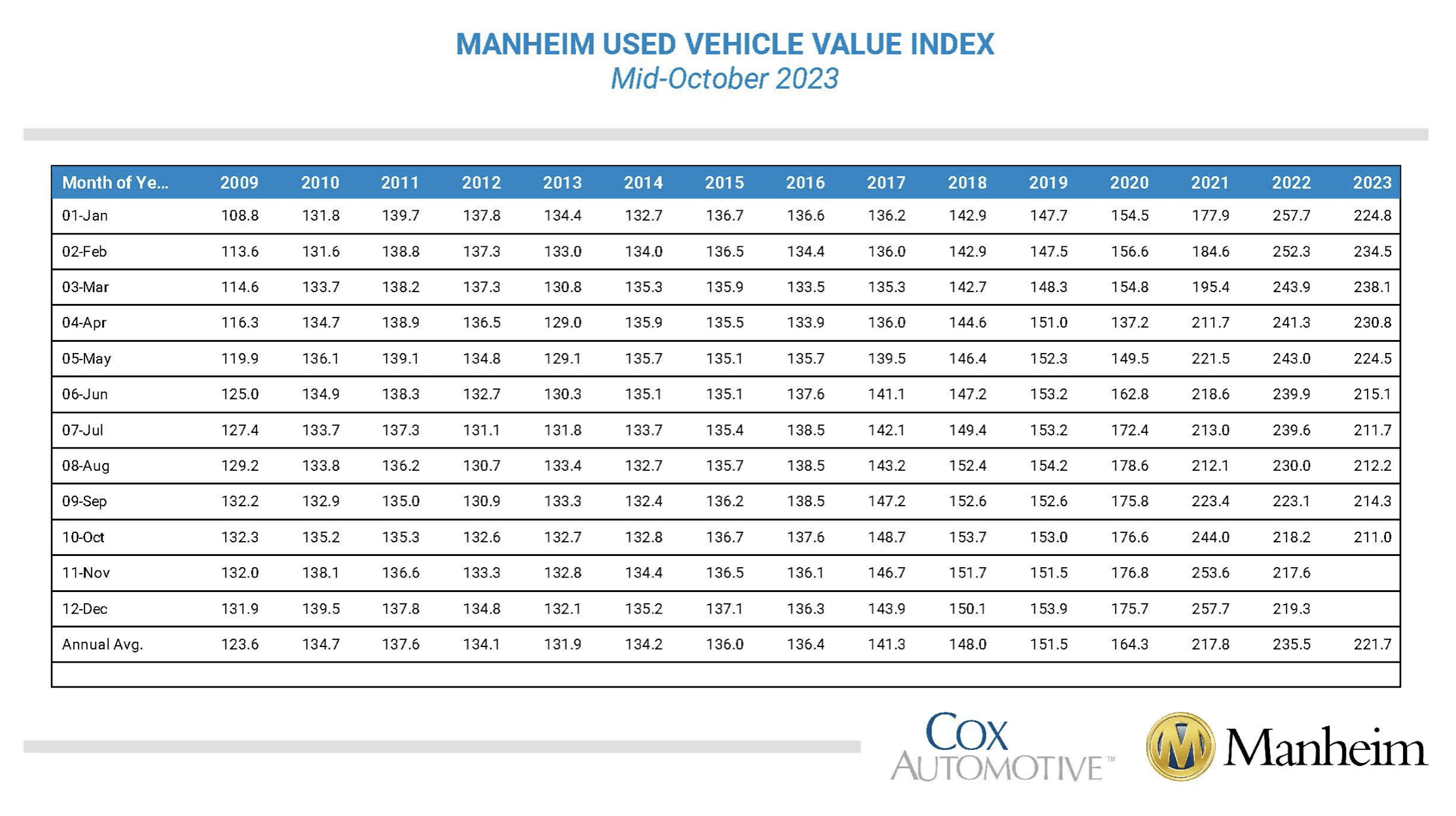

Used car inventory has been low, while wholesale prices have continued to fall, according to the Manheim used vehicle value index. While lower inventory, consumer demand, and falling used car prices wouldn’t seem to be a great environment for CARG’s core business, it actually can help the company. The reason is that dealers don’t want vehicles that are losing value sitting on their lots too long, and thus can get more aggressive marketing them through a service like CARG. Having spoken to dealers in the past, CARG has always been one of their most effective and best priced options to direct their marketing dollars towards and it generally gives them a pretty clear ROI, unlike some other options.

Manheim

The revamps in the Digital Wholesale business, meanwhile, should help protect the company from losses, although revenue will could continue to be under pressure. The auto union strike is another factor to watch, and should prove to be good for used cars sales.

Overall, I continue to like the CARG business model and the ongoing transformation the company is undergoing to make it a one-stop shop for consumers. As such, my “Buy” rating and $22 target remain unchanged.

Th biggest risk to the stock are if CarOffer can’t stand up to a continued declining price used car market, any algorithm change from Google (GOOGL) that impacts CARG’s traffic, and a general decline in the sales of vehicles, especially used ones.

Q2 2024 Earnings Call Transcript")