baona

On 10th Aug 2023, Tapestry, Inc. (TPR) and Capri Holdings Limited (NYSE:CPRI) announced that they had reached a definitive agreement under which Tapestry would acquire Capri, providing Capri shareholders with $57 per share, a 65% premium to the prior closing at the time, and valuing the company at $8.5bn on an enterprise value basis.

The transaction, although not subject to financing conditions, is subject to customary closing conditions, including the receipt of antitrust approvals from the Federal Trade Commission (FTC) in the US and the EU Commission (EC) in Europe.

At the time of writing, the FTC has issued a second request in the US, and the EC has admitted a request for approval of the merger.

In this note we focus on merger control in Europe and provide information on the probability of this transaction being blocked or approved in this particular market.

Relevant Authority in Europe: EC or Member States?

The Council Regulation (“EC”) Nº 139/2004, commonly referred to as the EUMR for European Union Merger Regulation, establishes that a concentration with Community dimension, that is, a merger or concentration where the aggregate turnover of the undertakings concerned exceeds certain threshold, could be investigated either by the EU centralized authority or by individual competition agencies in certain Member States.

The identification of Member States that could initiate an investigation following a merger notification to the EC is warranted in cases where the EU turnover of the merging undertakings is highly concentrated in specific Member States.

The EC could also refer a notified concentration to a Member State if it is made to believe, or otherwise determines, that “the concentration may significantly affect competition in a market within a Member State which presents all the characteristics or a distinct market and should therefore be examined […] by that Member State”, according to article 4(4) of the EUMR.

With respect to the proposed acquisition of Capri by Tapestry, the concentration was notified to the EC on 6 Mar 2024. At the time the Commission reserved initial judgment on whether this concentration falls within the scope of the EUMR, and hence whether it would apply itself to examining it or would refer it to the competition authority of any Member State.

Given that the EC has 25 working days from receipt of notification to decide, we expect a press release on 15 Apr 2024, in which the EC would indicate that (i) the concentration doesn’t fall within the scope of the EUMR (it could fall within the scope of one or several Member States’ competition laws), or (ii) the concentration falls within the scope of the EUMR but doesn’t raise serious doubts as to its compatibility with the common market in the EU, or (iii) the EC will initiate phase II proceedings as a result of ruling that the concentration, falling within the scope of the EUMR, raises serious doubts as to its compatibility with the common market.

Referrals from the EC to Member States are not common. From the 7,897 concentrations notified to the EC in 2000-2023, only 202 were referred to local competition authorities in Member States, that is 2.5% of all notified mergers in 23 years, according to EC statistics on merger cases. This ratio is consistent even if we take into consideration only the post-pandemic years from 2021, showing a referral ratio of 2.6% for the 1,132 concentrations presented to the EC in the period.

Market compatibility, however, shows a clearly positive picture: 91% of all concentrations notified to the EC in 2000-2023 were considered compatible with the common market and approved within the 25 working days timeline. More importantly, when computed over quinquennial periods ending in 2023, there is a positive trend in the proportion of concentrations swiftly approved by the EC, which may suggest a learning curve in the market such that fewer mergers are being found to be incompatible with the market by the EC, that is, fewer mergers that are preliminarily thought to be incompatible with the common market are being notified to the EC.

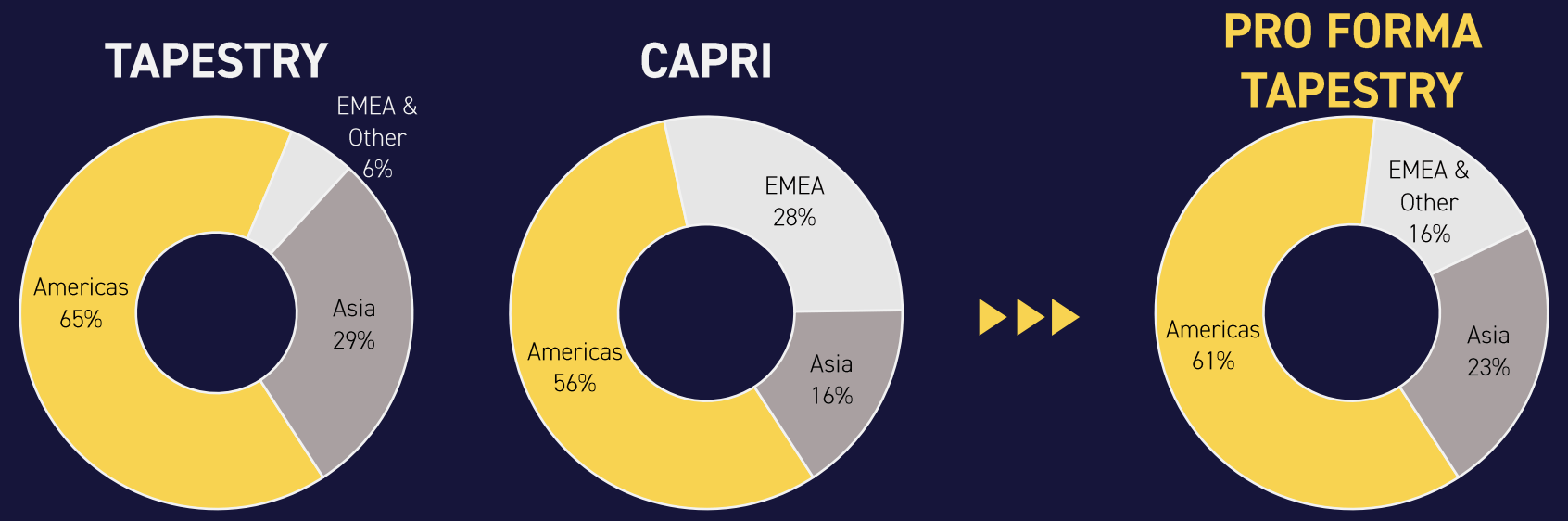

Specific to this proposed merger, neither Capri nor Tapestry disaggregates their European sales, but we have been able to identify the localized online presence, fulfilment centers and subsidiaries in the UK, Italy, France, Germany, Spain, Switzerland, the Netherlands, Austria, Belgium, Ireland and Portugal. Since the UK and Switzerland are excluded from the EUMR scope, we note that the main overlapping markets are Italy, France and Germany, which is consistent with the characterization of the European market for leather bags, as identified by the Dutch CBI.

We see why both Capri and Tapestry would choose to establish and maintain a significant presence in these markets, as they house unparalleled craftsmanship, innovative design and, at the same time, have both high-income local buyers and attractive touristic appeal to American and Asian holidaymakers.

In determining the relevant geographic market for an EU antitrust filing, we would add Spain and the Netherlands to Italy, France and Germany, so we have a more complete market picture that comprises not only consumers but also European suppliers.

Pro-Forma Geographic Footprint (Tapestry Merger Presentation)

Based on the geographic identification above, the pro-forma EU penetration, and the legal definition of Community dimension under EUMR, we believe that this transaction will remain within the scope of the EC and not be referred to any Member State. This is not to say that Member States, in particular Italy and France, will not have a participation in the scrutiny, but rather would provide valuable data to the EC as part of a Phase I investigation.

Will the Transaction Require Phase II Proceedings?

Historically, Phase II proceedings have been initiated in 2.9% of the concentrations notified to the EC in 2000-2023, and the trend shows a clear downward drift, with the Phase II ratio in 2023 at the historic low of 1.4%. This could suggest that the EC is concentrating its efforts on scrutinizing market-shifting transactions, which lately have been associated with those with a technological edge or where a dominant position exists or could be created as a consequence of the merger.

Our analysis indicates that the main overlapping market for Capri and Tapestry in Europe is luxury women’s footwear in France, Italy, Germany, and Spain, where Jimmy Choo and Stuart Weitzman seem to compete in a market that targets stylish professional women. Although Coach and Kate Spade also compete in the footwear segment for both men and women, these brands do not compete with Jimmy Choo, as they would likely appeal to a younger, less affluent demographic (of women in the particular case of Kate Spade).

We believe that, even though there is a geographic overlap between the merging entities, no Tapestry brand could be deemed a direct competitor to Versace, based on target audience and price point. To be precise, we believe that the Versace luxury footwear line could be somehow lined up against Stuart Weitzman´s, however, the competition authority could not look through any meaningful comparison here due to the relatively small footprint of these two categories, and the presumption that merging the two companies wouldn’t change the brand and identity of these product lines since brand recognition is such a valuable asset in the luxury market.

This would then lead to the merged entity likely keeping and growing these separate lines, while they decide which course of action to follow for the Stuart Weitzman business, which generates only about 4% of Tapestry’s global revenue, and would be diluted to 2.3% of the enlarged Tapestry.

Moreover, we believe that the EC could, in the case of luxury footwear, determine that the transaction is not likely to lead to adverse effects for consumers, in terms of increased prices or decreased quality of products and services, because there is no dominant position that would be created as a consequence of this transaction, and even more, demand elasticity in the high-end luxury footwear segment makes this consumer less concerned with price changes than the more price-sensitive customers of the Coach and Kate Spade brands. This is mainly an income effect due to consumers in these two segments exhibiting different levels of disposable income.

In our view, the luxury footwear market could be seen as partially self-regulating in the sense that high-end consumers are not constrained by price or choice, due to their ability to access local and global brands up and down the price scale and value chain, consistent with a market with low or no switching costs. To a lesser extent this same logic could apply to the market for handbags and small leather goods served by Michael Kors, Coach and Kate Spade, however, we are conscious that the typical market for these brands would fall onto the so-called accessible luxury, affordable luxury, or essential luxury; categories that rank below true stylish luxury in terms of craftsmanship, materials, design and brand positioning in the market.

The political contour of merger control in Europe is also relevant for this transaction. Given the current European political environment, we believe that the EC would be hard-pressed to justify using public resources to protect consumers that could arguably enter and leave the market at will due to their significant disposable income, particularly when the underlying product is clearly a component of discretionary spending.

Furthermore, with EU elections scheduled for June this year, we believe that Commissioner Margrethe Vestager would try to avoid a repeat of the 2019 political setback when, following European parliamentary elections, she was proposed as President of the European Commission, but was fiercely opposed by French President Emmanuel Macron, due to her decision to veto the merger between Siemens and Alstom. These events cleared the way for Ursula von der Leyen to become President of the European Commission, leaving the role of first Vice President for Vestager.

We’re inclined to believe that, from a consumer protection standpoint, the EC could indicate later this month that the proposed merger doesn’t raise serious competition concerns in the women’s luxury footwear market, as no dominant position is created or strengthened, and consumers surplus could potentially be relatively unaffected by the transaction.

On the other hand, since the EC must only prove that the merger is likely to result in a significant impediment of effective competition in the internal market to initiate Phase II proceedings, there’s a non-trivial probability of an extended inquiry in the affordable luxury market, specifically concerning handbags and small leather goods manufactured by Coach, Kate Spade, and Michael Kors.

We estimate that Capri and Tapestry generate about $1bn from this market in Europe, which, together with closeness of competition between Coach, Kate Spade and Michael Kors, could give the EC grounds to assess competition effects and request the introduction of remedies in order to satisfy antitrust concerns.

This would have been considered by advisors involved in the transaction, so we believe that this could, in the worst-case scenario, delay approval of the transaction, from Phase I to Phase II with remedies, but wouldn’t cause the transaction to collapse due to competition obstacles.

Nonetheless, we don’t dismiss the possibility of this transaction being approved under Phase I in April because the co-existence of Coach and Kate Spade brands within the Tapestry portfolio gives an indication of the group’s brand philosophy, that is, Tapestry seems to be comfortable with marketing globally substitutable products with similar brand identities. This would be a strong point in proving to the EC that the company has no intention to diminish Michael Kors’ presence in Europe in favour of Coach and Kate Spade. In fact, we believe that the enlarged group could be looking into diversifying the Michael Kors geographic footprint, which is currently two-thirds concentrated in the Americas.

Examining Reduced Competition and Choice in Suppliers Market

In our view, the EC angle would not be linked to protecting high-income luxury products consumers but to ensuring that EU suppliers are not unfairly treated as a consequence of the merger, as well as customers that fall within the affordable luxury category.

Capri has a large network of extremely valuable suppliers and distribution partners in Italy and the Netherlands. In fact, it could be said that the Versace production system is almost entirely done in Italy, which adds to the glamour and style that characterize the brand and its products.

Moreover, Jimmy Choo is also dependent on Italian craftsmanship for the production of footwear, whereas Stuart Weitzman relies on Spanish value chains for manufacturing and distribution.

Kate Spade, Michael Kors, and Coach products are made in Asian countries, including Vietnam, Cambodia, the Philippines and China, which somehow undermines their ranking in the high-end luxury market, and keeps them out of scope for any EU upstream market.

In Europe, we believe that the EC would be mindful of the potential effect that this merger could have on companies like Safilo SpA, EssilorLuxottica SpA, Swinger SA, Euroitalia SRL in Italy, Interparfums SA in France, and fulfillment centers in the Netherlands, not to mention Spain, where Tapestry owns 50% of a factory in the province of Alicante.

Italian Safilo, for instance, makes eyewear for Kate Spade, Jimmy Choo and Stuart Weitzman, among other global brands, including Boss, Carolina Herrera, Under Armor and Moschino. The EC could be interested in avoiding a significant shift in service terms in favor of the enlarged entity at the expense of European companies. The situation to avoid would be such that the enlarged Tapestry would use its increased negotiation power after the merger to obtain better terms than otherwise would have obtained, causing European suppliers to reduce profit margins, employment, and investment, and/or ultimately delaying innovation in their respective sectors.

Despite being a hypothetical scenario (competition authorities operate in this realm with balance of probabilities), this potential situation could also affect EssilorLuxottica in Italy, which also manufactures eyewear products for Versace and Michael Kors; Euroitalia, which licenses fragrances for Versace and Michael Kors; and Interparfums in France, which manufactures perfumes for Kate Spade, Jimmy Choo, Coach and other mid-market brands.

One characteristic of this licensing market, where Capri and Tapestry license their brands to accessories manufacturers in exchange of royalties, is that, to the best of our knowledge, most contracts are due to expire by 2026, with the exception of Kate Spade’s fragrance and eyewear contracts with Interparfums and Safilo, which run until 2030 and 2031 respectively, and Michael Kors’ agreement with Euroitalia, which lasts until 2036.

We estimate that the licensing business, where part of these complex relationships with European suppliers reside, would contribute about 2.3% of net sales for the merged entity. At this level, and with the potential of growing all six brands in the Americas, EMEA, and Asia, we don’t believe that Tapestry would object to maintaining the status quo with respect to licensing agreements, considering that at least 10 of those are due to expire by 2026.

We’re not saying here that those licensing agreements will be cancelled because of the merger, after all, they provide about $350mn a year, but rather that Tapestry could let some of those contracts expire by 2026 if it deemed them redundant, and this would be fully compliant with contractual obligations among the parties, leaving no room for policy intervention.

On the other hand, EC concerns about the potential impact on European businesses post-merger would be mitigated by the fact that European suppliers are among the most coveted in the luxury market, with hyper-recognizable brands in skins and hides, leather products, perfumes, apparel, jewelry and accessories (just remember that Europe’s largest company by market cap is LVMH Moët Hennessy Louis Vuitton, a giant in the luxury market).

European Competition Deadline

The question of whether the EC will clear this transaction in April or initiate proceedings with a possible deadline in August, requires looking into the closeness of competition for consumers and shifting negotiation power for suppliers.

For women’s luxury footwear, we believe that Jimmy Choo and Stuart Weitzman appeal to different audiences, with brand identities focusing on different demographics. Jimmy Choo is perceived as an occasion piece, not intended to be worn on a routine basis, while Stuart Weitzman is associated with more frequent use, although for a luxury segment of the market. In this sense, and because of the reasons exposed above, we believe that the Commission would not require further proceedings in this particular product market.

The affordable luxury market, however, in which Coach, Kate Spade, and Michael Kors operate, is subject to different competition dynamics. Here, despite the brands trying to appeal to different fashion tribes, we see closeness of competition and a higher degree of substitutability among them. We also note that, despite these characteristics, the market has lower barriers to entry and a number of effective competitors, like Furla, Alexander Wang, Bao Bao Issey Miyake, and others.

With no access to a crystal ball, and purely based on geographic positioning of the Capri and Tapestry brands in Europe, demand elasticity for footwear and leather goods, closeness of competition and substitutability, and the overarching political environment in the EU, we believe that a concentration between relatively small players in the €110bn European luxury market is not likely to create much concern for the EC.

However, for the more restrictive €26bn affordable luxury segment, which excludes luxury leaders like LVMH, Chanel, Kering, and Richemont, we believe that some commitments will be needed from Tapestry in order to secure clearance from an antitrust point of view. These could include maintaining segregated brands and marketing policies for Michael Kors, Kate Spade, and Coach, which could be seen as targeting the same customer base. We don’t believe that there is any need for any of these brands to be divested, as the risk of a significant post-merger lessening of competition is not that high, but again, we are not sitting in Brussels evaluating merger concentrations.

In our view, the probability of this transaction being approved without Phase II proceedings in April is higher than the probability of a Phase II investigation that would extend the European timeline until at least August, and even if the latter were to be the outcome chosen by the EC, we believe that behavioral remedies are available in order to proceed with the transaction.

In the worst-case scenario of the EC asking the merging parties to dial down on any of the brands in Europe, these could be achieved by downscaling Michael Kors in its non-primary European market (only 21% of global revenue, compared to 67% from the Americas), or limiting it to exporting customers in duty-free markets, which include not only airports but high touristic locations.

Spillovers onto the US FTC Investigation

Although the largest competition authorities in Europe and the US tend to have some level of coordination, while keeping full autonomy and independence, we don’t believe that the results in Europe would have much bearing on the FTC investigation in the US, essentially because the market structure is radically different, particularly in the segment where Michael Kors, Kate Spade and Coach compete in.

Tapestry brands are mainly oriented to the North American market, with 65% of global sales allocated to that market, but this figure is only 57% for Capri, however, 81% of Capri’s exposure to the Americas comes directly from Michael Kors.

Based on this, and the provenance of raw materials, the US and European markets are fundamentally different, even though the customer base is comparable. For this reason, we believe that the transaction will be approved in the EU, likely in April but not ruling out August.

Considering that the FTC in the US issued a second request for this transaction in November 2023, and the EC notification was only made in March 2024, we wouldn’t be surprised if Tapestry is sequencing filings, and if both competition authorities are sharing, to the extent that is legally possible, information on the competitive landscape post-merger. In any case, we don’t believe that findings in Europe could be extrapolated into reading what the FTC is about to determine.

On a final note, we highlight that this analysis has been made with independent public information and there are risks to our views, mainly because we don’t have access to requests for information and surveys distributed by competent authorities. In any case, we believe that the relative upside and downside risks and opportunities warrant opening and holding a position in Capri, at least until 15 April 2024, when the EC is expected to issue a press release on the Phase I investigation. Opening of a Phase II investigation at such a time would be seen as a positive, with the counterfactual of referral to Italian or French competition agencies. This could also signal that the merging parties are working on the introduction of remedies, but it’s too soon to assume this is a plausible scenario.

Q2 2024 Earnings Call Transcript")