Recently, I received a capital distribution from a private real estate fund, and it couldn’t have come at a better time. The experience brought me both joy and relief, prompting me to share it in the hope that it might inspire you to invest more for your future.

After purchasing a new home in October 2023, my liquidity resembled a lake after a three-year drought. I felt like a fish flopping around on the cracked lakebed, desperately in search of water. Furthermore, I was bombarded with unexpected capital calls from various private funds.

As the primary financial provider for my family, I experienced heightened stress for six months, knowing that a single large expense could force me into expensive consumer debt. Please roof, don’t blow off during the storm!

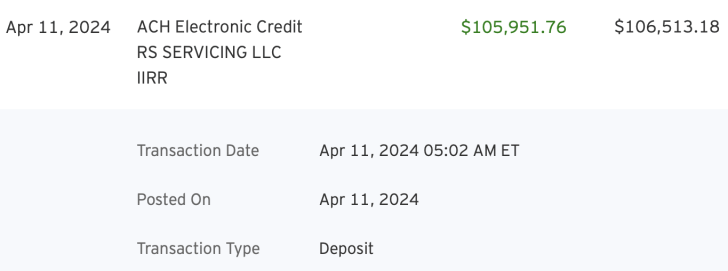

However, with this recent capital distribution of $105,951.76, I now have some much-needed liquidity and relief. The initial investment was $47,000 for a compound annual return of roughly 12.2% after seven years.

This post will discuss:

- The benefit of treating your investments like expenses

- Why investing in private funds and companies is good for patience, which in turn, is good for your future

- The importance of responsibly buying big ticket items like houses or cars

- How so much can change over a 5-10-year time period, so you must invest for the unexpected

- Not to take your liquidity for granted.

Investing Is An Expense Until It Isn’t

Two years after graduating college, I began treating investing as an expense. It was a strategy to deceive myself into investing more, knowing my tendency to splurge on unnecessary things.

In those early days of employment, I made impulsive purchases like a Honda CBR 600 motorbike, even though I didn’t have an official license. Racing up and down Joe Dimaggio Highway was undoubtedly risky. To counterbalance this, I then bought a Volvo 850 GLT, all while living in Manhattan where the subway system was highly efficient. What a dummy.

No one advised me to save and invest diligently, preparing for the possibility of burning out from a miserable job. Consequently, I spent lavishly until the dot-com crash in 2000 and after not being renewed for a third-year analyst position at Goldman Sachs. These events were stark reminders of the fragility of my financial situation.

Since becoming an accredited investor around 2003, I’ve focused on investing in private funds and individual private equity and private real estate deals. Between 15-20% of my investable capital is in private investments.

Each investment entails a leap of faith, requiring locking up capital for 5-10 years with no liquidity and no certainty of what the fund investments will be. However, I reasoned that by consistently investing in private opportunities each year, I would eventually receive regular capital distributions.

The Importance of Patience To Build Wealth

My approach to private investing resembled waiting for the latest movie to hit Netflix twelve months later. While my friends joyfully discussed their favorite films, I patiently waited. By waiting, I could watch new movies every month on streaming and save a significant amount on movie tickets and transportation.

The initial waiting period poses the challenge.

Some individuals are unwilling to wait twelve months to save money on a movie; they’d rather pay a premium to watch it in the theater immediately. YOLO, baby! Similarly, few are willing to lock up their capital for 5-10 years with no liquidity and no guarantees of investment returns.

If you can convince yourself that investing money is akin to spending it on a movie ticket, a luxury car, or a family skiing trip, you might find yourself investing more and ultimately becoming wealthier as a result.

Every New Expense After A Big Investment Can Feel Like Bad Luck

The reason why you should follow my 30/30/3 home buying guideline is because once you buy a house, every new expense may seem unexpected or larger than it really is. You might even start feeling cursed if you didn’t buy a home responsibly.

For example, two months after purchasing my house, my check engine light came on. I thought it was just time for a routine oil change, but it turned out to be a $1,200 expense for an oil change, a new PVC valve, and a new vacuum pump. Curses! What bad luck!

Then, I received another $20,000 capital call from a venture debt fund that had already called $20,000 in capital in November 2023, just a month after I closed on my house. After being dormant for a year, why was the venture debt fund suddenly making two relatively large capital calls within five months? Curses again!

The reality is, these capital calls and car maintenance issues would have occurred regardless of my home purchase. They just felt much more painful and unfortunate because I was living paycheck-to-paycheck at the time.

The Joy of Receiving Capital Distributions

Even though I’m well within the window to receive capital distributions for this particular fund I started investing in 2016, it still feels wonderful to receive them.

As a private fund investor, you tend to forget or mentally write off each private investment after a year. Part of the reason why is because unlike investing in public stocks, private investment valuations are harder to track day-to-day.

If you consistently invest most of your savings, as most people in the FIRE community do, you naturally adapt to a lower-than-normal cash flow situation. Because you’ve been accustomed to living on a minority of your income for so long, receiving a capital distribution can feel like winning the lottery!

In your mind, you either forgot about the investment or expected the money to never come back. So when it does, it feels like a brave son returning home after the war. You feel blessed to have him back.

To a lesser extent, receiving a capital distribution feels like getting a tax refund. Even though the money is yours to begin with, you’re still grateful.

So Much Can Happen Since You First Invested

After eight years of investing in this private real estate fund, the fund has had some decent wins (~50%), some great wins (~40%), and some total losses (~10%). The fund invested in a mix of multifamily, student housing, hotels, and office buildings mainly in the heartland of America.

Most of the 17 deals were going well until COVID hit. Unfortunately, office properties around the country have taken a big valuation hit due to the slow adoption of the return to work. For the sake of my investments, it would be nice to see everybody return to work and stop playing pickleball while working from home!

A downtown Minneapolis office property deal, which accounted for 6.4% of the fund, failed.

Meanwhile a Boston office property deal (7.1% of the fund) is sucking wind partially thanks to a tenant called Pharma Models, who signed a 10-year lease at the end of 2022, but hasn’t paid rent since March 2023. Do the right thing Pharma Models!

Unless you have a tremendous amount of capital to build your own select real estate portfolio, most people are better off investing in a diversified real estate fund.

Didn’t Have Kids in 2016 When I Made My Initial Investment

When I began investing in this private real estate fund, I also didn’t have kids yet. My household expenses were about half of what they are today. Consequently, I ended up investing the majority of my cash and free cash flow. Ah, the good old days before I blew up my passive income!

Now that I do have kids, this capital distribution feels especially gratifying since it will be used to support my family. The gears in my Provider’s Clock just received a nice greasy injection.

Back in 2016, while I certainly wanted to have kids, I wasn’t sure if it would happen thanks to biology. I was just investing in hopes of one day having a family. Today, with the high cost of raising kids in San Francisco, I have a clear purpose for this capital distribution.

By 2014, I had already purchased a modest home and spent a year renovating it. I was also leasing a 2014 Honda Fit for $220 a month. So, I had no other major expenses or desires.

The feeling of receiving a capital distribution is akin to feeling like my vacation property is finally realizing its full potential 17 years after I acquired it.

Keep Investing For An Unknown Future Purpose

I enjoy investing because of the potential to generate income with minimal effort. The best passive income investments provide the greatest effort-adjusted returns. The longer we remain invested, the greater our chances of achieving positive returns and overall success.

When you find yourself with surplus cash flow, even without a clear investment purpose, it’s wise to invest most of it anyway. In ten years, you’ll likely be glad you did. There are countless unforeseen expenses your future self may encounter, making saving and investing for the future imperative.

With the IPO market gradually reopening, M&A activity picking up, and more capital distributions occurring from private funds, I’m optimistic about the private markets.

My Investment Plan Moving Forward

Over the next one to two years, I’m focused on rebuilding my liquidity. This entails saving approximately 60% of my cash and cash flow in 5%+ yielding money market and Treasury bonds, aiming to reach a cash reserve of ~$200,000.

Simultaneously, I plan to invest half of the remaining 40% of cash into the S&P 500 after every 0.5% or greater pullback. It’s challenging to consistently outperform the S&P 500 long-term, and the liquidity of an S&P 500 ETF provides flexibility if needed.

My remaining cash will be dollar-cost averaged into the Fundrise Innovation Fund, given its low investment minimum of $10. The other benefit of the fund is that I can gain liquidity if I need it.

Over the next three years, my objective is to establish $500,000 of exposure to private artificial intelligence companies. This way, I hope to benefit if AI revolutionizes the world. If it doesn’t, then at least I’m hedged against potential risks while providing opportunities for my children.

Never Want to Feel So Illiquid Again

The past six months of experiencing a liquidity crunch were unpleasant. It was manageable when I didn’t have kids and held a day job, but now too much is at stake.

For the next three years, I’ll prioritize investments in Treasury bonds, the S&P 500, individual stocks, and open-ended real estate and venture capital funds with liquidity. I’m going to reduce my allocation to illiquid, closed-end venture capital funds by 50% going forward.

Best of luck diversifying your wealth and investing for the future. Here’s to more unexpected capital distributions!

Reader Questions And Suggestions

Have you received any large capital distributions recently? How do you account for future capital distributions for cash flow and tax minimization purposes? Are the private markets finally thawing?

To invest in real estate without all the hassle, check out Fundrise. Fundrise offers funds that mainly invest in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher. The firm manages over $3.5 billion in assets for over 500,000 investors looking to diversify and earn more passive income.

I’ve personally invested $954,000 in private real estate since late 2016 to diversify my holdings, take advantage of demographic shifts toward lower-cost areas of the country, and earn more passive income. We’re in a multi-decade trend of relocating to the Sunbelt region thanks to technology.

Fundrise is a sponsor of Financial Samurai and Financial Samurai is an investor in Fundrise.

Q2 2024 Earnings Call Transcript")