hapabapa/iStock Editorial via Getty Images

Points to note:

1) All values are in CAD unless noted otherwise.

2) Prior to June 17, 2021, Canadian Net operated under the name of Fronsac Real Estate Investment Trust (FRO.UN).

Previous Coverage

We covered the 2023-Q1 results of Canadian Net Real Estate Investment Trust (TSXV:NET.UN:CA) and came away impressed with this internally managed, retail landlord. This triple net business was trading at a discount to its net asset value or NAV at the time, which was at odds with majority of its trading history. Yes, its 8.0X debt to EBITDA was a bit lofty for our taste, but its debt structure (primarily property level) and minimal capital expenditures, made it a no-brainer buy in our books. The icing on the cake was stated in our concluding remarks for that piece.

At present, you are getting a near 7% yield with a 50% payout ratio. That is quite an impressive deal in triple-net land.

Source: Canadian Net REIT: 6.9% Yield From This Triple Net Landlord

Note: Readers looking for a detailed introduction to this REIT can refer to our previous piece (link provided above). We will not rehash the details today.

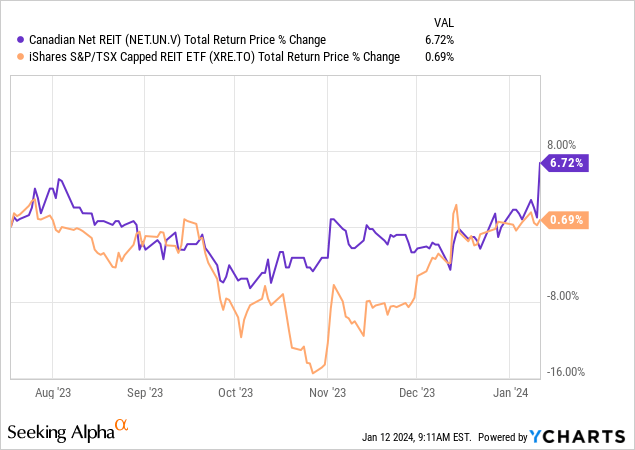

We started accumulating a position thereafter, and today it dwarfs all other REIT positions in our portfolio. It has handily beaten the Canadian REIT Index during this time frame. Though the bulk of the outperformance has literally come in the last two days.

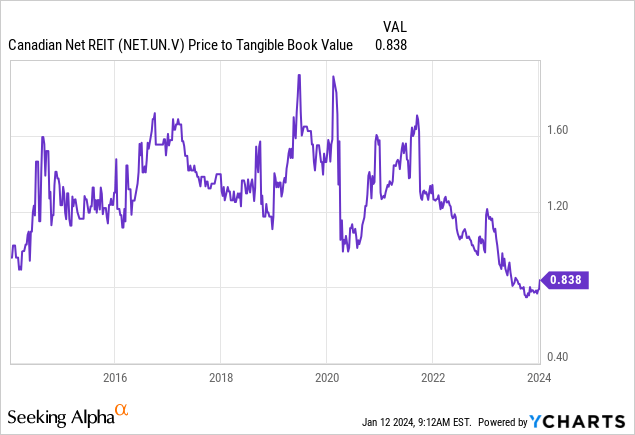

The market is still not awarding this the correct multiple and it continues to trade around the same discount as last July.

It yields 6.7% currently (2.88 cents/monthly distribution, $5.18 price), and has a 55% payout ratio. Today, we review the last published results and explain our current stance on this Canadian retail REIT entity.

Q3-2023 Results

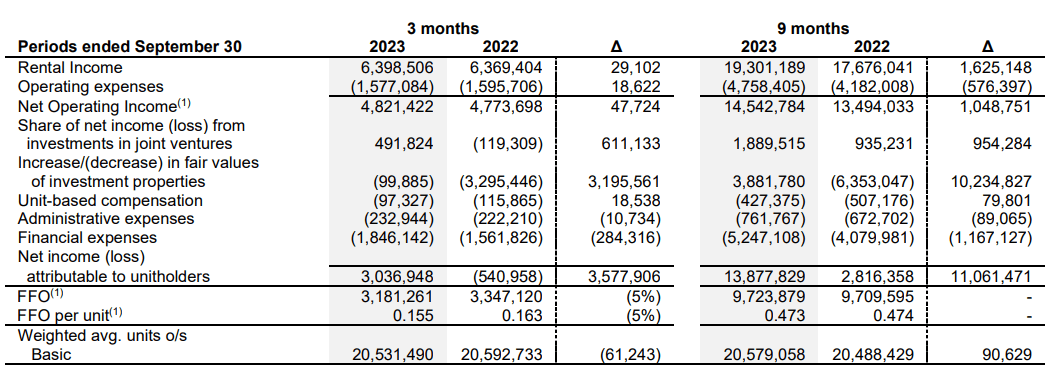

The Canadian Net portfolio comprises properties that primarily house retailers, national service stations, convenience stores, and quick-service restaurant chains. The REIT had 99 investment properties to its name at the end of Q3-2023, bulk of which resided in Quebec (82), with the balance in Ontario (8), Nova Scotia (8), and New Brunswick (1). The portfolio was 101 strong at the end of Q1-2023. Two properties were subsequently disposed, one in April and the other in September. Despite the hit to the rental income from these dispositions, the Q3-2023 top-line inflows still showed a nominal uptick relative to the Q2-2023 numbers.

Q3-2023 MD&A

This outperformance was due to the rent increases on some of the existing properties. The 9-month period, on the other hand, showed a robust 9% increase in the rental revenues due to the net acquisitions since Q4-2021, along with contractual rent step-ups. Management provided color on the rent increases expected for the 2024 renewals during the earnings call.

Patrick Kealey

Perfect. And then just last question here. I don’t want to hog the call too much. Just looking ahead to 2024, could you provide any color insight as to what you’re seeing so far, just sort of respect to leasing spreads and maybe contractual escalators for those expiries?

Kevin Henley

Yes. So 2024, so far, what we’ve seen is, I would say, between 10% and 15% on basically leases in place. On new leases, we’re currently under negotiation, so very hard to tell. But nothing that is not contractual will be leased at a spread lower than 10%, for sure.

Source: Q3-2023 Earnings Call Transcript – Tikr

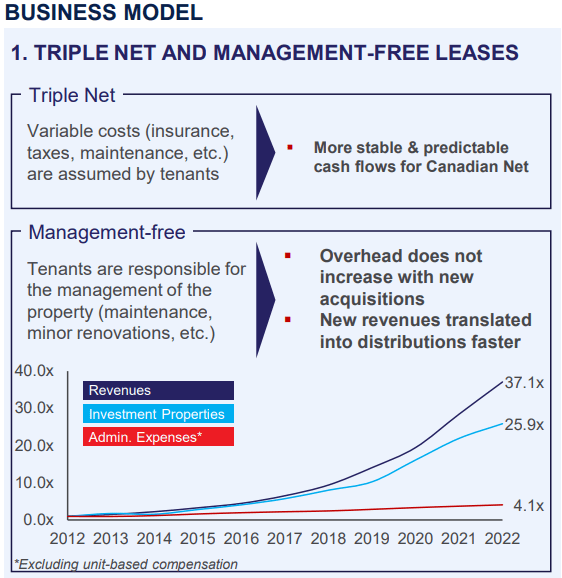

The portfolio continues to be fully occupied at the end of Q3-2023, with a weighted average lease term of 6.6 years. Being a lessor of triple net properties, this REIT’s operating expenses are stable for the most part. It incurs neither the overhead on its rental properties, nor the hassles that come with managing them. Both the responsibilities lie solely on the head of its tenants.

Q2-2023 Fact Sheet

We can see the operating expense stability in action in the net operating income or NOI numbers for the last few quarters, which consistently come in at around 75% of the rental income.

Q3-2023 MD&A

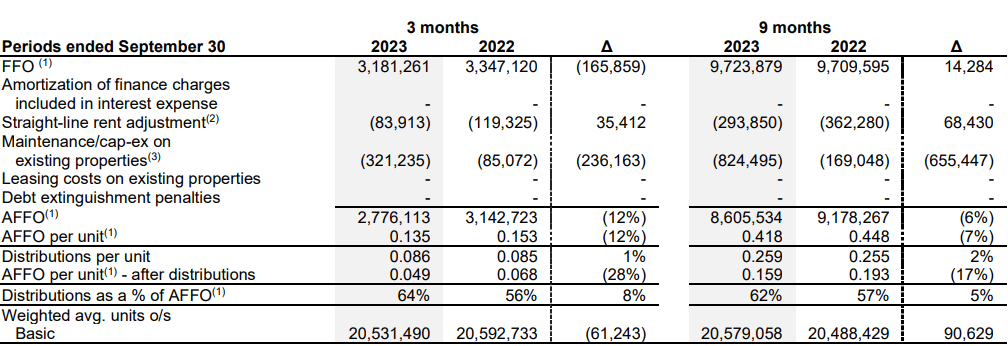

As a result of the close tracking between the rental income and NOI, the sub-nominal increase in rental revenue was matched by sub 1% increase in the year-over-year NOI. While the REIT is shielded from the operating costs of the rental properties, it feels the impact of the higher interest rates on its mortgage renewals, variable rate mortgages, and credit facilities. The weighted average interest rate on its mortgages increased from 3.63% on September 30, 2022 to 3.80% at the end of Q3-2023 and the year-over-year interest coverage reduced from 2.9X to 2.6X. We should add that the interest coverage has been 2.6X since Q1-2023, so it has not been a recent drop. The higher interest expenses easily outpaced the modest NOI increase and the funds from operations came in around 5% lower than the comparative quarter in 2022.

Q3-2023 MD&A

The year-over-year adjusted funds from operations or AFFO declined by 11%, over twice that of the FFO decrease.

Q3-2023 MD&A

The main contributor of this double-digit decline was the maintenance/cap-ex, and the REIT expects to recover the $800 thousand and change, plus 9% from its tenants.

Patrick Kealey

Got it. And then just moving forward on the maintenance CapEx side. Assuming that the bump this quarter is just a little bit of carryover from, I believe, it’s the roof maintenance from — that you discussed last quarter?

Kevin Henley

Exactly. So this year was big, just we had the $805,000 that was spent on the roof replacement on our [ Kirby ] Lake property. This will be recovered with a 9% rate of return. So this is really — we started the work in Q2, finished in Q3, and that’s why you see an uptick there.

Source: Q3-2023 Earnings Call Transcript – Tikr

Excluding this temporary impact, the AFFO still declined, but by 1.4%, which is more in line with the FFO decline.

While 2022 had the REIT making several acquisitions, 2023 was about dispositions. The sale price on these exceeded their respective IFRS valuations i.e., they were accretive. Yes, these too came up during the earnings call.

We are happy to report that in addition to the Timmins property sale in Q2, we also sold a restaurant property operated under the Mikes banner in Trois-Rivières, Quebec, for $1.3 million during the third quarter and a Pizza Hut property in Dartmouth, Nova Scotia for $1.65 million in October. These transactions exceeding our IFRS values continue to show our ability to create value while enhancing our capital structure.

Source: Source: Q3-2023 Earnings Call Transcript – Tikr

The September sale was at a capitalization rate of 5.6%. Despite being able to dispose multiple properties at higher than their reported valuations, Canadian Net maintained the portfolio level capitalization rate at 6.41%, and this has been unchanged since December 2022.

Liquidity and Debt

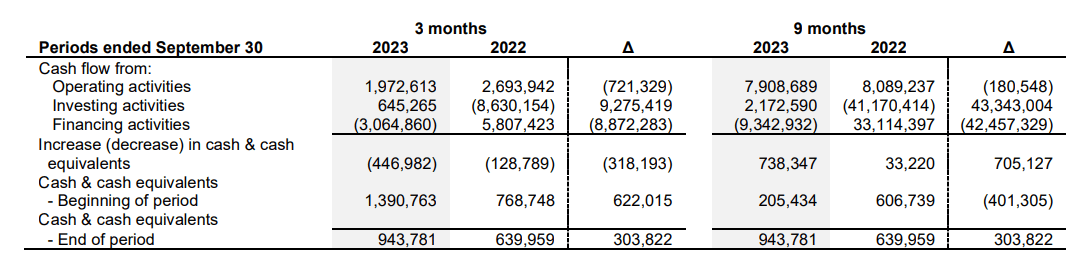

The REIT had around $944 thousand in cash and cash equivalents at the end of Q3.

Q3-2023 MD&A

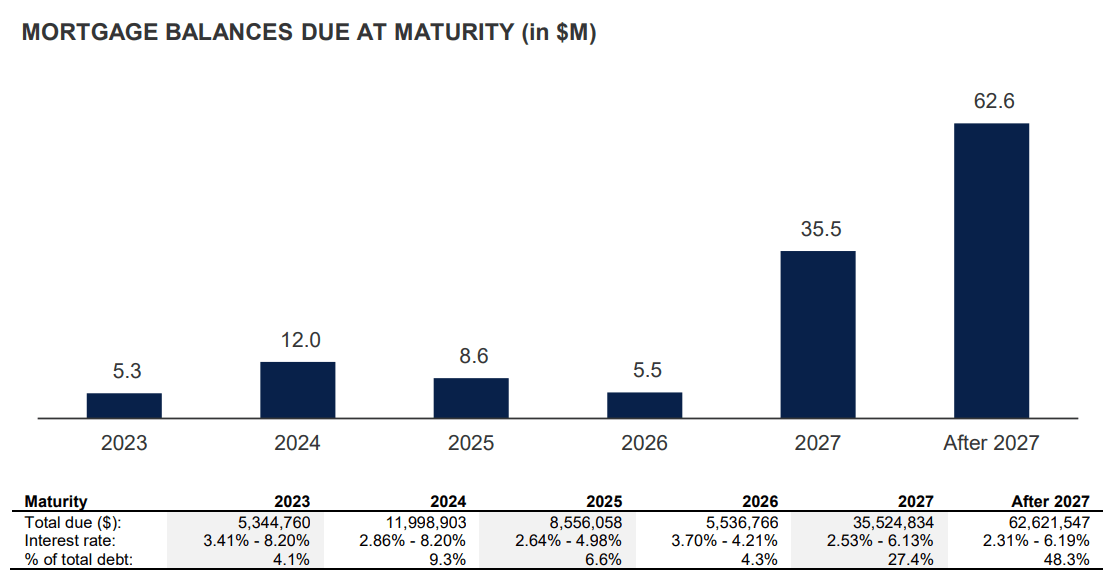

Additionally, it has 3 secured lines of credit, which had a cumulative $3.1 million that was available to draw at the end of the reporting period. Both the credit facilities limits, as well as the usage have increased since Q1-2023, the reporting period we covered previously. The total limit on the facilities was around $19.6 million then, with $15.4 million drawn at the time. At the end of Q3, the two amounts stood at $20.6 million and $7.3 million, respectively. While the bulk of their mortgages do not come up for renewal until 2027, the REIT still has to navigate the current interest rate environment for around 13% of its $152 million mortgages maturing in the 15 months subsequent to Q3-2023.

Q3-2023 MD&A

Management expected to get the 2023 renewals going in the weeks following the earnings call.

About $8.5 million of mortgages, including those in joint venture, remains to be renewed in 2023, with completion expected in the coming weeks. Following mortgage renewals, we anticipate generating around $1.5 million in net proceeds to repay credit facilities.

Source: Q3-2023 Earnings Call Transcript – Tikr

With the interest rates cooling in Q4, management anticipates locking in rates of around 6.25% – 6.5% for the refinancings coming up shortly after the earnings call.

Verdict

We still like it and are maintaining a Buy. It remains a very undervalued situation that is relatively immune from even modest economic weakness or credit stresses. Yes, if we get a severe recession, this will trade down to $4.00 and yes you have to double down then. The key feature here is that the worst case is a few properties don’t get refinancing done. In that case, the REIT may require a small cash infusion for those properties, changing the loan to value ratios. Even if that cash was absent, it might forfeit a couple of properties in a GFC-like setup. But the REIT will survive and your odds of making 10% total annualized returns from here remain extraordinarily high. Buy.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")