zhengzaishuru

Article Thesis

Canadian Natural Resources (NYSE:CNQ) is a leading Canadian oil sands company that has an excellent track record and strong management. Thanks to superior cash generation, Canadian Natural Resources has recently achieved its net debt target, which will allow the company to return even more cash to its owners. While the share price and valuation have expanded in recent months, this high-quality company remains a good investment.

Past Coverage

I have written about Canadian Natural Resources several times in the past, most recently in June, in an article in which I called Canadian Natural Resources one of the best companies in its industry. My “Buy” rating back then has worked out well so far, as shares have returned 50% in less than a year since then. Since then, the macro picture has changed due to turmoil in the Middle East, while Canadian Natural Resources has hit an important net debt threshold. On top of that, the company has reported quarterly and annual earnings results since then, which is why I want to update my thesis in this article.

Oil Price Macro Picture

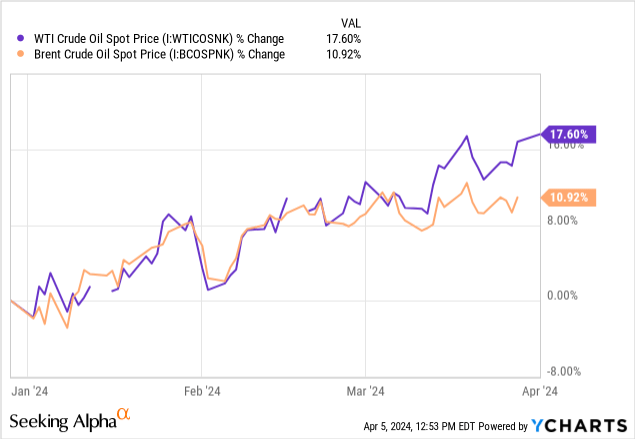

Many people will have noticed at the pump that oil prices have risen considerably in recent months. The following chart shows the extent to which the prices for WTI (CL1:COM) and Brent (CO1:COM) have increased so far this year:

Daily spot prices are up by 11% for Brent and by 18% for WTI so far in 2024, with some futures contracts having risen even more than that.

There are several contributing factors to the significant oil price increase this year. First, it looks like oil demand is stronger than previously thought, even in Europe which is currently battling with weak growth rates.

The ongoing war in the Middle East and attacks on shipping lanes by Houthi rebels also contribute to higher oil prices, as some market participants fear that things could escalate, disrupting oil production and/or transportation further. Attacks on Russian oil infrastructure also added to fears about supply disruption, and last but not least, OPEC+ has decided to maintain current output cuts until the middle of the year (or longer).

All in all, this made for a supply-demand picture that was beneficial for global oil prices. Of course, oil producers such as Canadian Natural Resources benefit from higher oil prices, all else equal.

Higher oil prices are not the only positive external news for the company, however. Canadian Natural Resources will also benefit from the start-up of the Trans Mountain pipeline expansion which will happen sooner than previously thought. This new pipeline will help move Canadian oil to export markets and should thus have a positive impact on Canadian oil prices — the differential between Canadian oil prices and global oil prices should decline, which will make for a revenue tailwind for Canadian Natural Resources and its Canadian peers.

Canadian Natural Resources: Balance Sheet Is Strong

During the initial phase of the pandemic, and also in some years before that, oil prices were not especially strong. This made for rather weak results for many oil companies, which caused them to add debt to finance growth projects. But since 2022, oil prices have been pretty attractive for oil producers such as CNQ, and many oil companies decided to clean up their balance sheets. Since interest rates rose as well, getting rid of debt, or reducing debt levels, made a lot of sense — paying down debt when interest rates are rising results in considerable interest expense savings, which adds to a company’s net profits, all else equal.

Many of the Canadian oil companies, including CNQ, announced shareholder return frameworks. Depending on their respective net debt levels, they operate with fixed allocations of free cash flow to debt reduction, dividends, capital expenditures, and so on. Canadian Natural Resources set a net debt target of C$10 billion — when net debt gets reduced to that level, the company will pay out roughly 100% of free cash flows to investors, as further debt reduction is, in the eyes of the company’s management, not necessary. Canadian Natural Resources hit the C$10 billion net debt level during the fourth quarter, which is why the company announced that it will not pursue shareholder returns at a level equal to 100% of the free cash flow the company generates. Analysts praised the company for hitting this milestone, with CNQ being the first major Canadian oil company to do so, although Suncor (SU), Cenovus (CVE), etc. will likely hit their respective net debt targets in the foreseeable future as well.

CNQ: Strong Shareholder Returns

On the same day the company announced its plan to return 100% of free cash flow to its owners going forward, Canadian Natural Resources also announced a 5% dividend increase. Canadian Natural Resources would have to increase its dividend a lot more to lift its payout ratio dramatically, of course, but the higher base dividend is a nice start. We can take a look at what shareholder returns could look like in the future.

During 2023, Canadian Natural Resources generated excess free cash flows of C$6.9 billion after accounting for dividend payments of C$3.9 billion. In total, that makes for free cash flows in the C$11 billion range. Today, Canadian Natural Resources is valued at around C$116 billion, thus the free cash flow yield of the company’s shares is around 9.5%. That sounds pretty attractive, considering the company plans to return all of that cash to its owners via dividends and share repurchases.

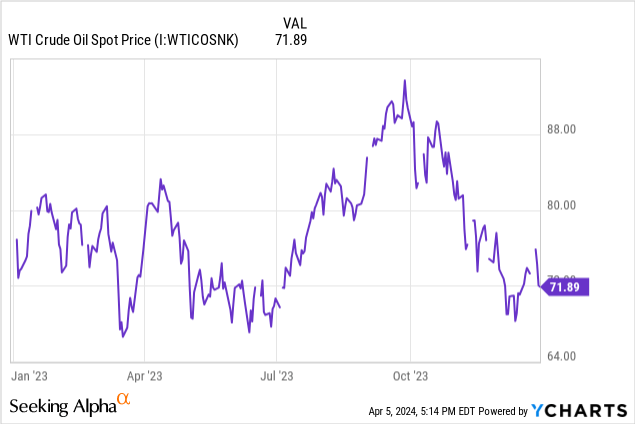

Of course, free cash flows could differ from last year’s free cash flows in the future. Oil prices were solid, but not overly high in 2023, unlike in 2022 which had been a very strong year for oil prices:

Oil prices were mostly in the $75 to $80 range last year, with a quick spike toward $90 in September. Today, the WTI crude oil price stands at $87, meaning it is higher than the average last year. If oil prices were to remain where they are right now for all of 2024, CNQ’s free cash flows in 2024 should be higher than those from 2023 — especially when we also consider the tailwind from the Trans Mountain pipeline expansion starting up in May. I would thus not be surprised if CNQ’s free cash flows for the current year come in somewhat higher than C$11 billion, although this depends a lot on where oil prices are headed for the remainder of the year. In case we see a pullback in oil prices, free cash flows could also come in lower than C$11 billion. I don’t see any immediate catalyst for lower oil prices, but in case the US was to get into a recession, oil prices could head lower for sure.

In a base case scenario, Canadian Natural Resources could thus return around 10% of its market capitalization via dividends and buybacks this year, although this isn’t set in stone, depending on oil prices.

CNQ won’t raise its base dividend dramatically, as this would mean less flexibility in case oil prices head lower at some point in the future. Instead, moderate growth in the base dividend seems likely, while CNQ will also continue to buy back shares — which is good news, as buybacks make the dividend safer and since they give a nice boost to per-share cash flows. On top of that, CNQ could return extra dollars to investors via special or one-time dividends.

Is CNQ A Good Investment?

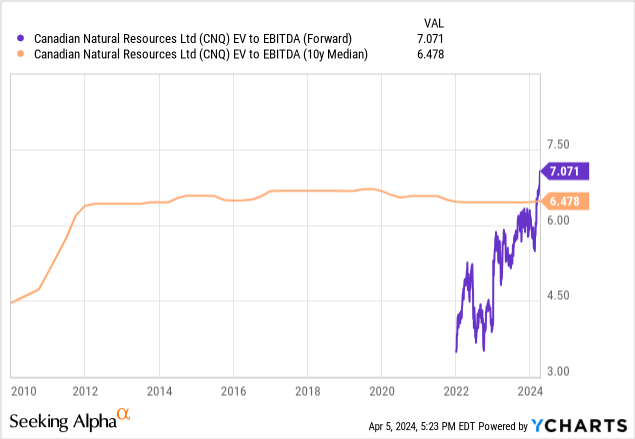

Canadian Natural Resources has generated a return of 25% so far in 2024 alone, while returns over the last year are even higher, at more than 35% before dividends. This means that the valuation has expanded as well:

With an enterprise value to EBITDA multiple of 7, CNQ is still pretty inexpensive in absolute terms. EV/EBITDA ratios below 10 are oftentimes seen as undemanding. Compared to the 10-year median, CNQ trades at a small premium of around 10% right now, however. It is thus arguably not the best time to enter or expand a position.

That being said, buying CNQ at a small premium to fair value has worked out fine in the past, as the company’s fair value has risen rapidly and since the company is very well managed. For those looking for a high-quality oil company with excellent shareholder return prospects and a steadily growing dividend, CNQ is still a quality pick right here. Waiting for a better entry point might pay off as we could get a better buying opportunity in the future, but that’s not guaranteed, of course. In the long run, someone buying at current prices should do well anyway.

Q2 2024 Earnings Call Transcript")