Petmal/iStock via Getty Images

Background

Though they likely need no reminding, 2023 has been traumatic for Plug Power Inc (NASDAQ:PLUG) shareholders.

PLUG vs SPY YTD (Koyfin)

The stock is down 63% year-to-date, as compared with the 26% return from the broader S&P 500 (SPY) and a 15% return from the Russell 2000 (RTY).

Yet, some of the clouds may be receding. The company announced at the end of August that it had settled with the SEC for $1.5 million, concluding an investigation into previous financial statements the company had issued (though it should be noted that the company could be on the hook for an additional $5 million fine in a year if the material weakness is not remediated).

So, with a beaten down stock price and the specter of the SEC investigation at least partially gone, is this end-to-end hydrogen company a compelling buy? Let’s dive in and see.

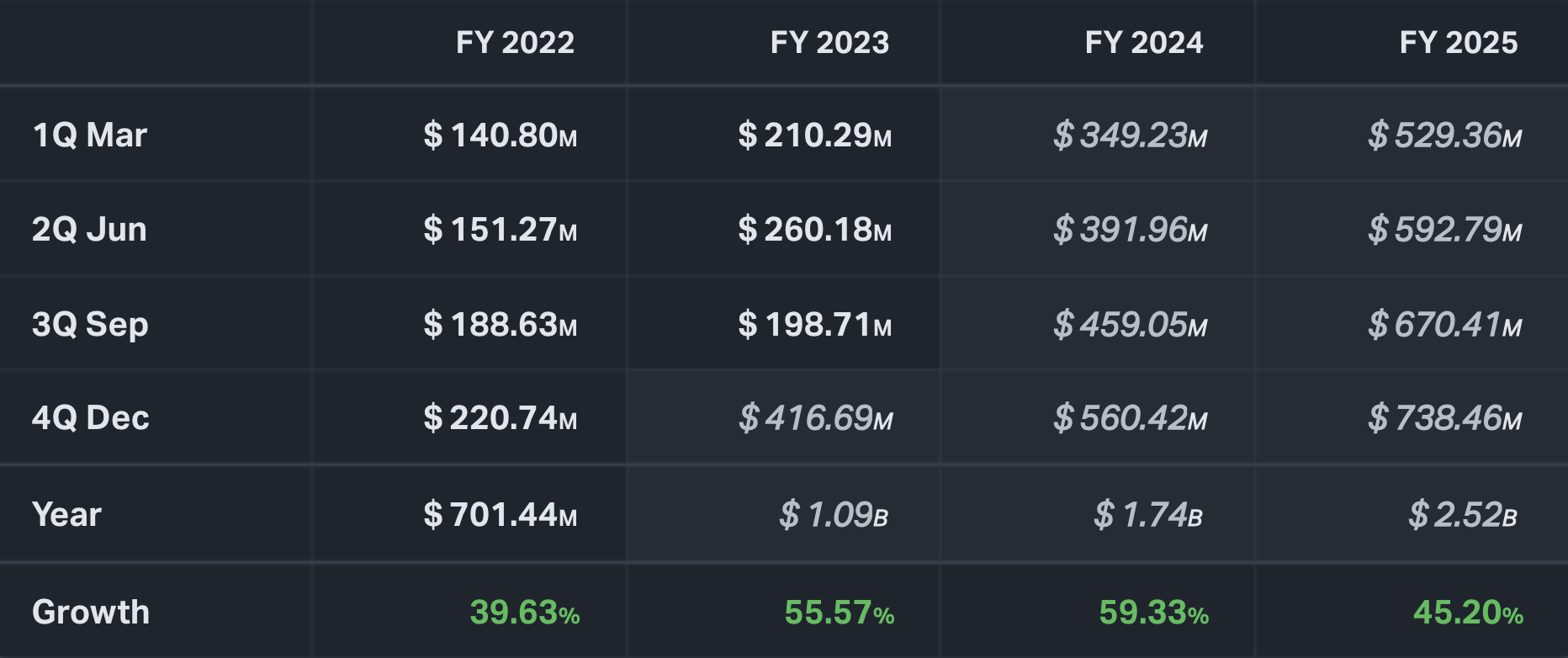

Performance & Expectations

When it comes to growth, analysts certainly seem bought into Plug’s promises of high growth rates.

PLUG revenues and revenue estimates (Koyfin)

After posting 39% year over year growth in 2022, analysts are looking for 55% growth in FY 2023 and an even higher growth rate of 59% for FY 2024.

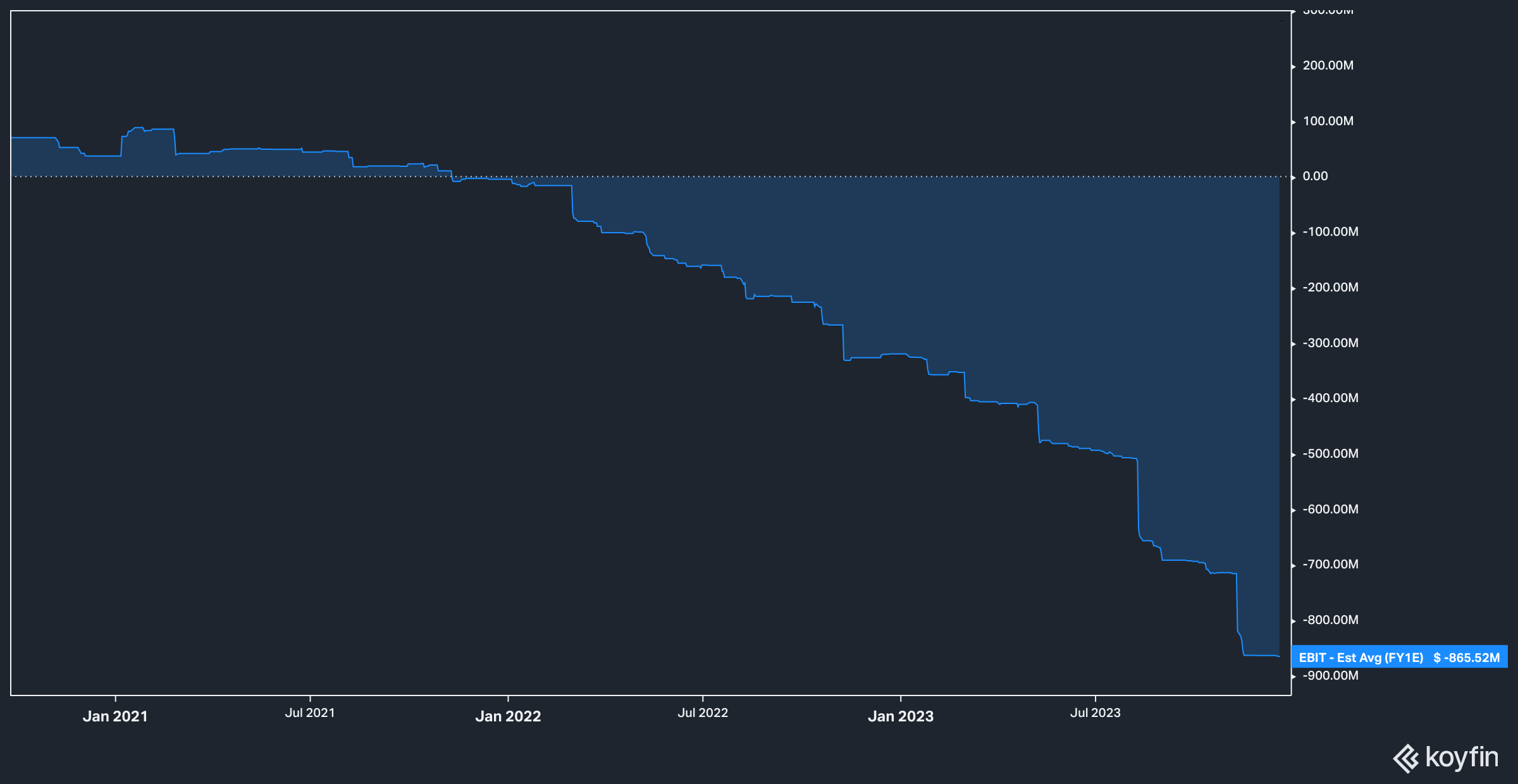

In a non-zero interest rate environment, however, profitability matters quite a bit more than it used to. Operating income, or EBIT, estimates for the next twelve months are lower than they have been in five years, with analysts now estimating that the company will generate a $855 million loss in operating income.

PLUG forward EBIT estimates (Koyfin)

EBIT estimates are negative until four years out from now according to Koyfin, which, again, in a non-zero rate environment is a near-eternity for shareholders of an unprofitable company.

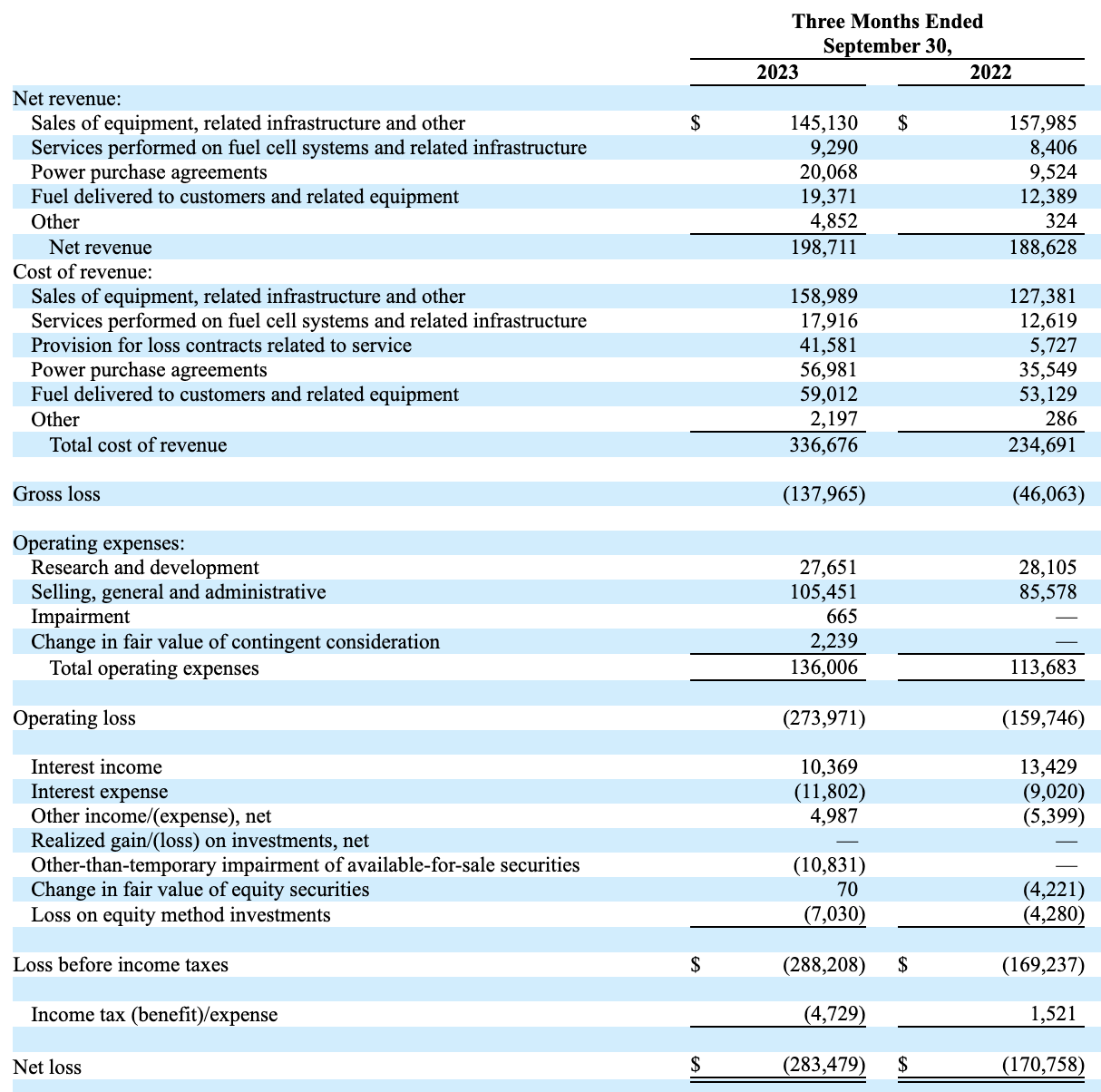

Digging into the financials shows that the company has not yet achieved economies of scale or positive unit economics. Consider the income statement from the company’s latest 10Q:

PLUG Income Statement, Q3 2023 (Company Filings)

The numbers, unfortunately, seem to be going in the wrong direction without much sign of reversing.

Net revenue grew by ~5% to $198 million, largely due to a surge in Power purchase agreements and delivery of fuel. The problem, however, is that costs were much higher than the growth experienced in the top line.

For example, in the 3rd quarter of 2022, Plug’s sales of equipment business unit (it’s largest) was actually profitable on a gross basis, even if only by a little. In that quarter, the company spent $0.81 for every dollar of revenue earned. 2023 saw not only revenue in the segment decline, but expenses go up. In Q3 2023, the company spent $1.10 for every dollar of revenue generated.

Further, total COGS increased by 43% year over year, while operating costs went up 19%.

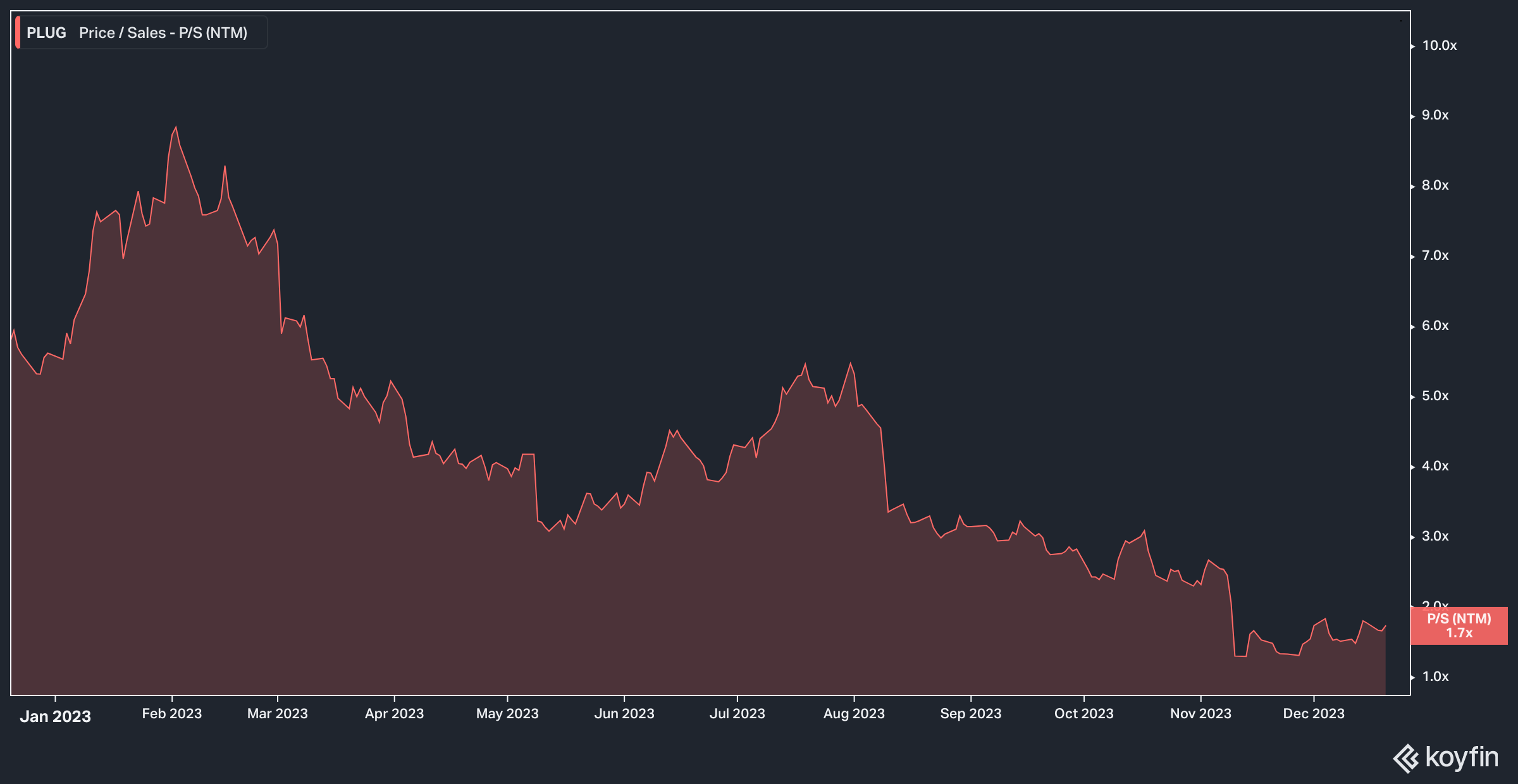

Valuation & Looking Under The Hood

Given the lack of profitability at Plug, we’ll utilize forward price to sales estimates for valuation.

Plug P/S Estimate (Koyfin)

To be sure, Plug’s value on a forward P/S basis has slid in the last year. Today, the stock trades hands for 1.7 times forward sales estimates, down from a high of ~9x sales in the first quarter of 2023.

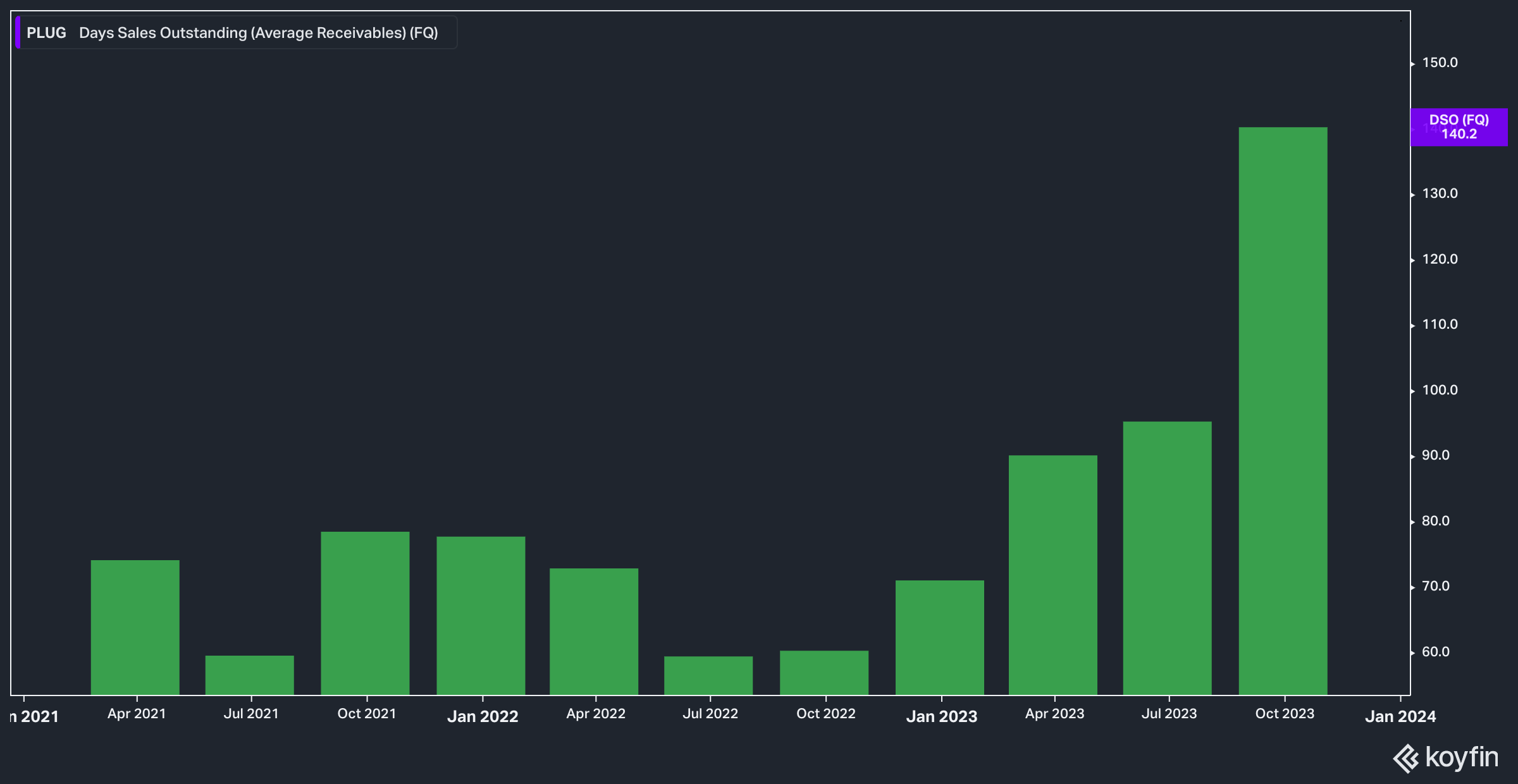

Unfortunately, this also coincides with a troubling trend–rapidly rising Days Sales Outstanding [DSO].

Koyfin

DSO measures how long it takes for a company to actually collect the cash from the revenue it has booked. Growing DSO may indicate that a company has taken a more aggressive revenue recognition posture, or that it is pushing out credit terms to customers in order to book revenue more quickly. While we cannot know exactly what is happening inside Plug to cause the DSO to rise to 140 days in the latest quarter while the 3-year DSO average for the company was 79 days, we nonetheless find this trend disturbing.

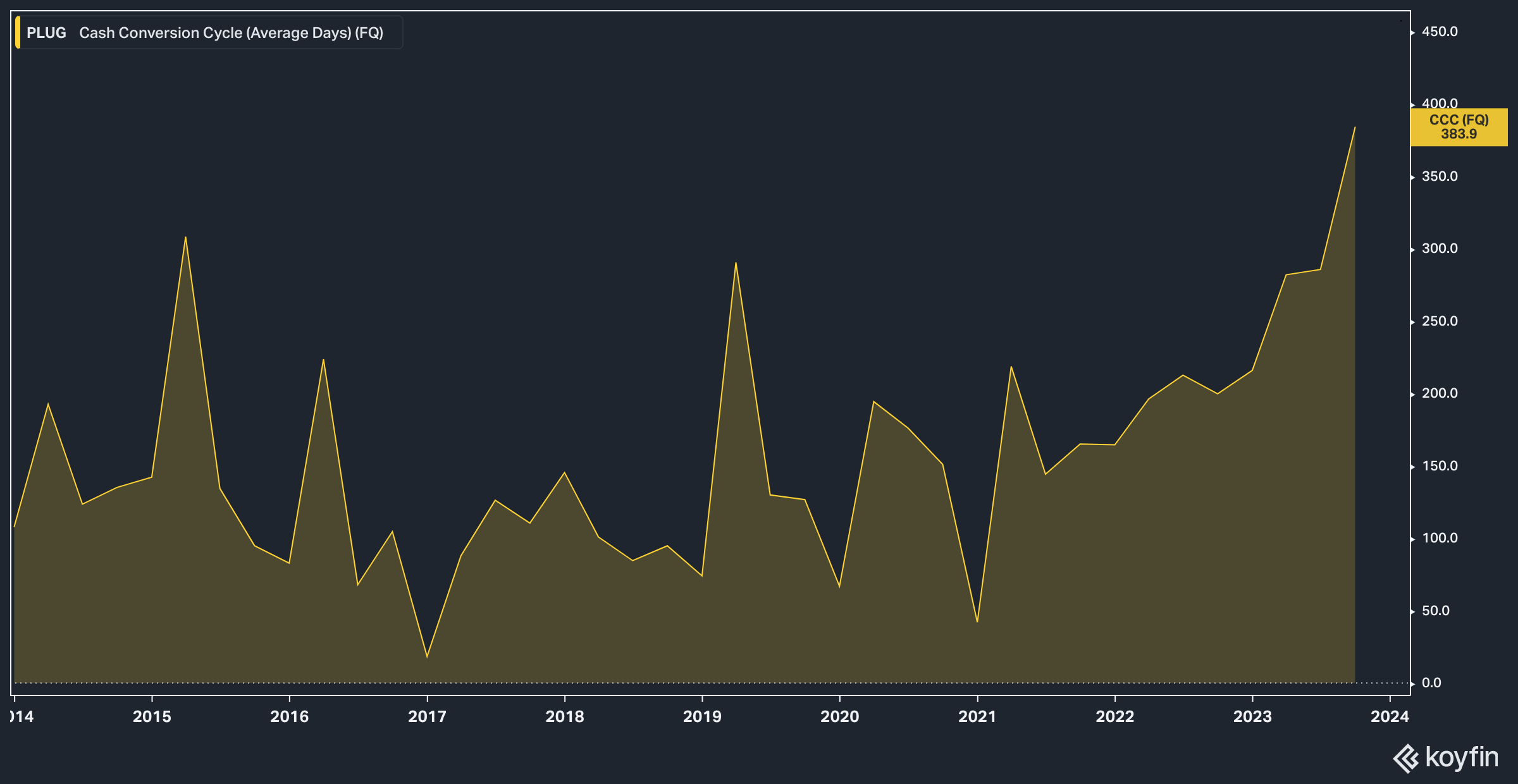

Backing up our concern is the fact that the company’s cash conversion cycle hit a 10-year high of 383 days in the last quarter. We think this is not a good sign for the future if the company continues to take increasingly long times to cycle cash.

Koyfin

The Bottom Line

Bulls contend that the company has an enormous runway in front of it–and that may be true. The demand for products in the hydrogen industrial ecosystem is likely to grow at a high rate for some time. The question, though, is whether or not Plug will be able to partake in the growth of the industry and achieve a profit. While we generally skew towards companies that are already profitable, a move in the right direction on the company’s operating profit (I.e., narrowing losses) and improvement in DSO and CCC would be very positive in our minds.

Today, however, it does not seem like the company has yet turned those corners. For those reasons, we must remain on the sidelines.

Q2 2024 Earnings Call Transcript")