Vertigo3d

Introduction

I am impressed by C3.ai’s (NYSE:AI) business, which appears well-positioned to harness substantial industry tailwinds. With partnerships forged with some of the largest technological companies and a rapidly expanding customer base, the company’s solid financial footing affords ample opportunities to invest in technological innovation, thereby likely attracting even more customers in the future. Moreover, the wide geographical and end-market diversity bolsters the resilience of the business model. However, despite these strengths, the current valuation appears excessively generous, as evidenced by the significant short interest in the stock. Therefore, I am assigning AI a “Hold” rating until a more balanced valuation is achieved.

Fundamental analysis

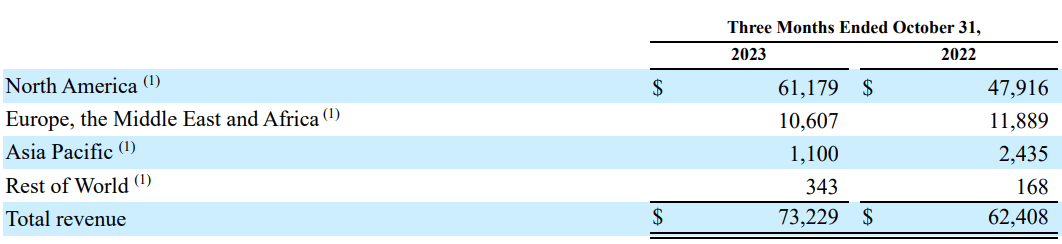

According to the company’s latest 10-Q report, C3.ai is an enterprise artificial intelligence software provider. The company’s platform supports accelerating digital transformation across various industries with prebuilt and configurable applications for business use cases, including predictive maintenance, fraud detection, sensor network health, supply network optimization, energy management, anti-money laundering, and customer engagement. AI operates across the world, but the major portion of revenue is generated in North America.

AI’s 10-Q report

AI operates within one of the most dynamic and rapidly expanding industries, experiencing unprecedented growth and acceleration. The artificial intelligence sector has attained such momentum that anticipating a slowdown in growth over the next few years seems unlikely. Rather, 2023 appears to have been merely the beginning, with the industry poised to continue its rapid evolution and expansion in the foreseeable future. I recently saw an interesting Forbes article where technology experts share their views on how several growth and expansion opportunities for artificial intelligence capabilities may emerge in 2024. For example, the power of artificial intelligence can be used more in sustainability projects as algorithms can help businesses reduce their carbon footprint, according to Kaitlyn Albertoli, CEO and co-founder of Buzz Solutions. Other experts also emphasize that artificial intelligence capabilities have a lot of potential to penetrate deeper into commerce and enterprise use. Therefore, AI is expected to be backed by solid industry tailwinds, and it is essential to understand how well the company is prepared to capture this opportunity.

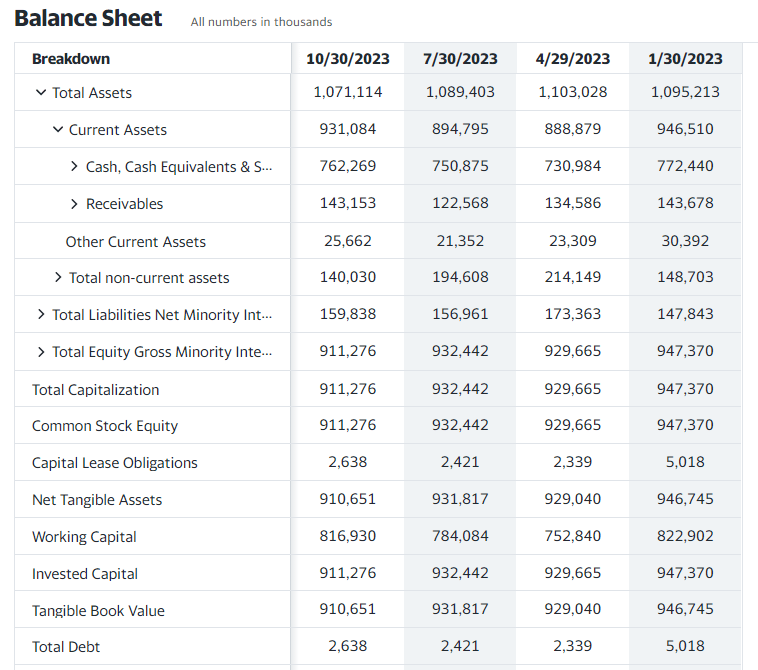

Since the industry is in the early stages of development, I think that the ability to invest in innovation is crucial at this stage of artificial evolution. Therefore, we need to understand whether AI has sufficient financial resources to fuel innovation. From this perspective, the company looks strong and flexible because the balance sheet is clean with almost no debt and is consistently high, with around $750 million in cash balance over the last multiple quarters.

Yahoo Finance

That said, AI is positioned well to continue investing heavily in R&D to help the company stay competitive in the technological race of the rapidly evolving artificial intelligence industry. Now let me move on to the company’s latest earnings presentation to analyze how well the company is able to convert its reinvestments in innovation to attract new customers. The significant achievement of securing 43 new agreements during the quarter, resulting in a remarkable 59% YoY growth, serves as a strong testament to the widespread appeal of AI’s applications. Furthermore, the current remaining performance obligation (“cRPO”) of $186 million stands as a solid indicator of the company’s robust position relative to its scale. Additionally, the caliber of AI’s partners underscores the company’s technological prowess and further validates its strength in the market.

AI’s earnings presentation

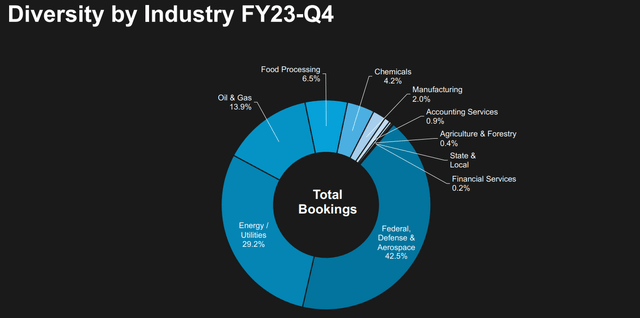

In addition to AI’s evident financial strength and its adeptness in cultivating a robust customer portfolio, I commend the management’s focus on building a resilient business model. This commitment is evident through their emphasis on expanding the subscription portion of revenue, as well as the wide diversification of the company’s geographical and industry exposures. Notably, C3.ai predominantly serves defensive sectors such as Federal Defense & Aerospace and Energy/Utilities, further contributing to the company’s stability. Moreover, the promising pipeline of projects and trials underscores the company’s commitment to innovation and diversification across various sectors. This comprehensive approach to business resilience instills confidence in AI’s ability to navigate challenges and capitalize on opportunities in the evolving market landscape.

AI’s earnings presentation

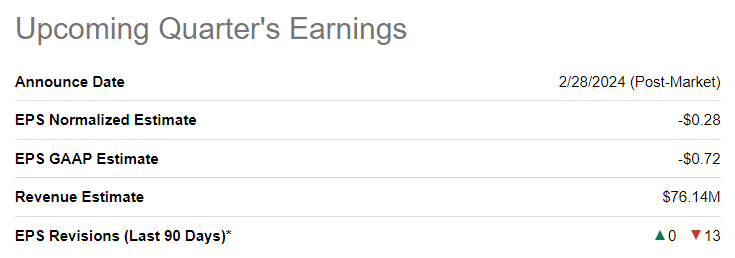

The upcoming earnings release, slated for the end of February, is being met with notable pessimism from Wall Street analysts, as evidenced by 13 EPS downgrade revisions in the past three months. Consensus projections anticipate a quarterly revenue of $76 million, signaling a 15% YoY growth rate, aligning closely with the previous quarter’s performance trajectory. However, the company’s profitability is anticipated to remain volatile, with anticipated dips both sequentially and YoY. Predicting the stock’s reaction to the earnings release of a relatively young company like AI feels akin to playing “Russian Roulette,” with the potential for significant movement in either direction. For instance, in the previous quarter, the stock experienced a sharp decline post-earnings, whereas in the quarter prior, it saw a substantial upward surge. Consequently, investors considering an investment in AI should brace themselves for the possibility of a considerable downside move should the report or guidance prove weak. That being said, it’s important to note that AI has rarely missed quarterly consensus estimates throughout its brief tenure as a public company.

Since AI delivered solid revenue growth in all three previous quarters and demonstrated positive EPS surprises by beating estimates by a wide margin, I expect the company to deliver a solid quarter. Considering the company’s robust history of expanding its client base and broadening its partnership network, I find it improbable that any indications of softness in guidance will arise.

SA

In summary, C3.ai presents itself as a resilient enterprise, placing emphasis on sustainable growth rather than pursuing expansion at any expense. Situated within a thriving industry brimming with significant growth prospects, the company’s sturdy balance sheet provides ample flexibility to further enhance its offerings. With products already endorsed by both customers and partners, C3.ai is well-positioned to capitalize on its strengths and continue its trajectory of quality growth.

Valuation analysis

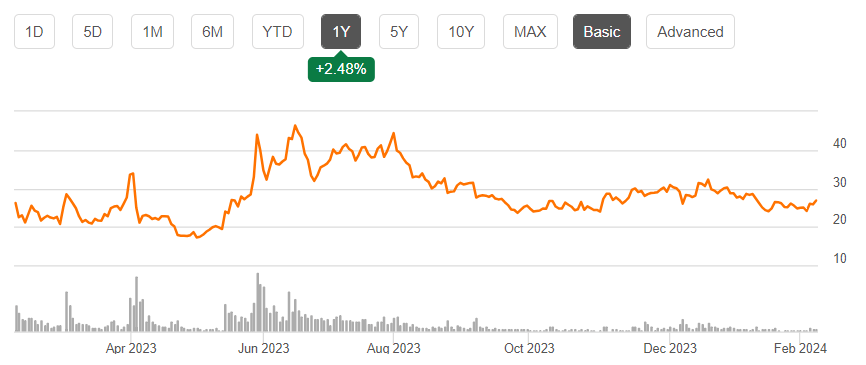

С3.ai went public in late 2020 during the pandemic-fueled IPO frenzy, and there was a short-term spike in share price after the first trading days. The stock currently trades about six times lower than the all-time high, and the last 52-week record demonstrates substantial volatility, with the share price ranging between $17 to $49. You can see how volatile the stock was during the last twelve months in the below chart.

SA

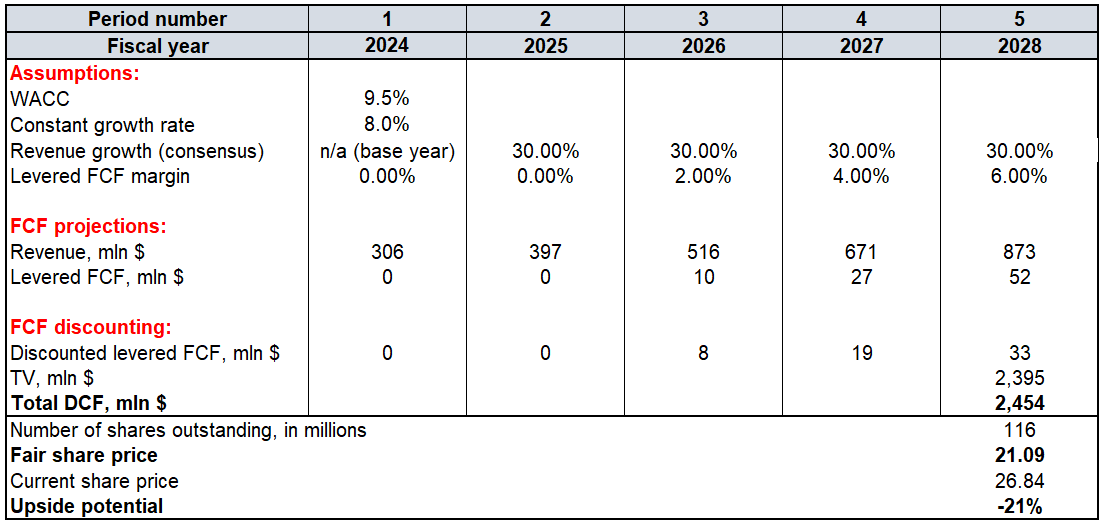

It looks like the market perceives the current $3.1 billion capitalization as unfairly high because there is a massive 37% short interest in the stock. To check the valuation fairness, I will run the discounted cash flow (“DCF”) model using a 9.5% discount rate. Using an 8% constant growth rate is extraordinary, but I believe that it is fair for such a hot trend like artificial intelligence. The whole industry is expected to compound at 37% CAGR for the next decade, so I think that an 8% constant growth rate for the terminal value (“TV”) calculation is fair. By the way, the projected 30% revenue CAGR for 2025-2028 is also based on the expected industry CAGR for the next decade, with an adjustment to be conservative. For the base year revenue, I think that consensus projection will be a reliable option. I expect the free cash flow (“FCF”) to increase in the next two years and the metric to expand by 200 basis points starting from FY 2026. There are around 116 million AI shares outstanding at the moment.

Calculated by the author

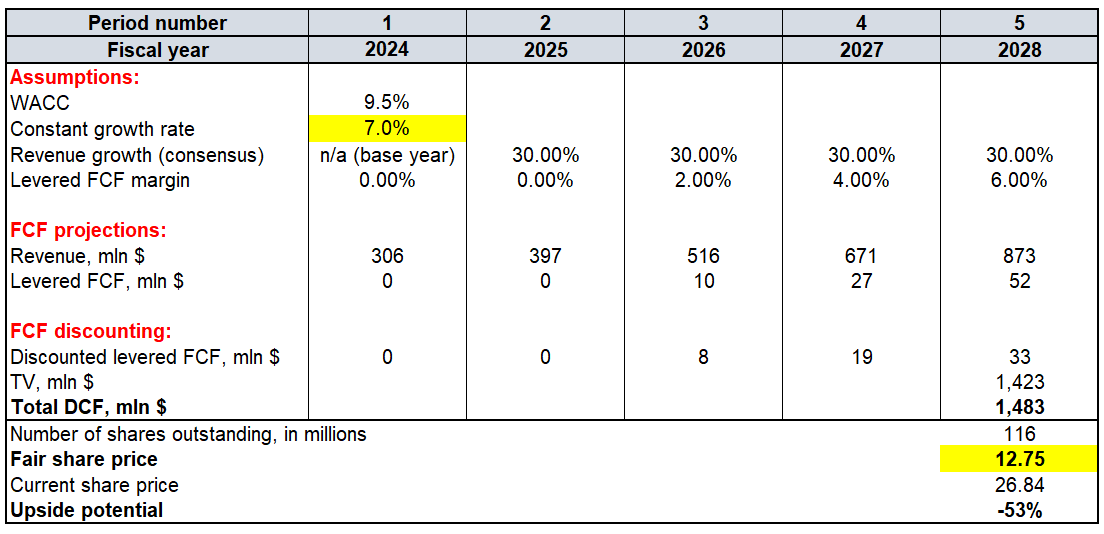

Based on the calculations above, I can conclude that the stock’s fair share price is $21. Therefore, there is a 21% downside potential, and the assumptions I used are a mix of conservative and optimistic. For example, decreasing the constant growth rate from 8% to 7% makes the fair share price almost two times lower. That said, the massive short interest in AI looks fair.

Calculated by the author

Mitigating factors

The company remains in the red, with consensus estimates indicating that positive earnings per share may not become positive until fiscal year 2027. Given its early-stage development, a significant portion of revenue must be reinvested in R&D and marketing efforts, contributing to the volatility of its profitability metrics. Consequently, this instability could introduce notable fluctuations in the stock price.

Prospective investors should take note of the significant customer concentration within the company. As outlined in the latest 10-Q report, the two largest customers collectively accounted for 25% and 13% of last quarter’s revenue, respectively. Such substantial customer concentration underscores the company’s heavy reliance on the financial well-being and strategic decisions of just two clients. For instance, if the company’s largest customer were to transition to a new provider of artificial intelligence applications, a significant portion of AI’s revenue would be at risk. Consequently, AI might be compelled to make concessions to retain this crucial customer, potentially sacrificing favorable terms to safeguard a substantial portion of its revenue stream.

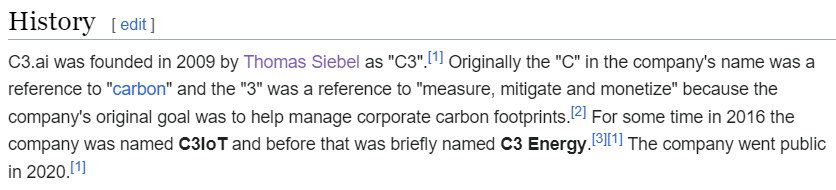

The company’s relatively short history, dating back to 2009, reveals a pattern of shifting business directions over the span of 15 years. Initially targeting diverse sectors such as clean energy and the Internet of Things (“IoT”), it ultimately settled on artificial intelligence. This pattern of inconsistency may raise concerns among investors, suggesting that the company has opportunistically pursued the hottest trends of each decade without maintaining a clear, consistent strategic focus. It is notable that despite these shifts, no leadership changes could reasonably account for such massive strategic pivots into new markets. This lack of leadership turnover raises questions about the underlying motivations behind the company’s directional changes, and may indicate a lack of stability or cohesive vision.

Wikipedia

Conclusion

While I admire the business and anticipate continued robust performance across key metrics, my valuation analysis suggests that the current market optimism may have already been fully priced in. Consequently, there is a strong possibility of a significant correction should sentiment in the broader market shift or if upcoming earnings disappoint. Given these considerations, I am inclined to withhold a recommendation to invest at the current price level and assign AI a “Hold” rating.

Q2 2024 Earnings Call Transcript")